South America Data Center Immersion Cooling Fluid Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

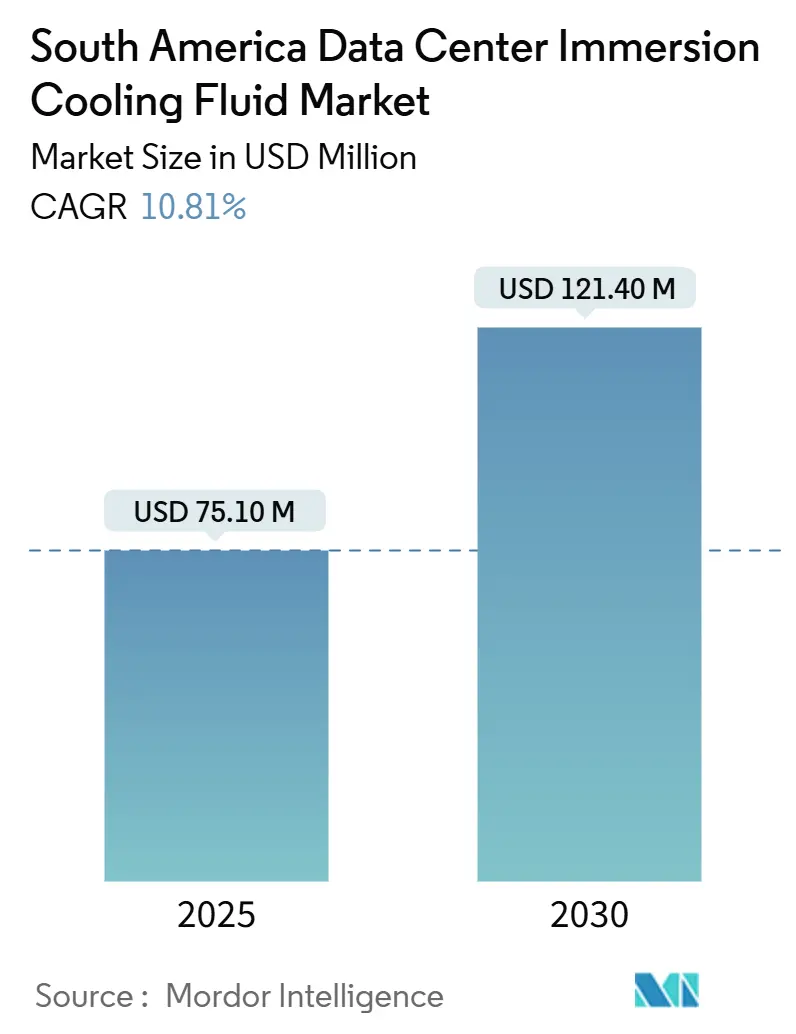

| Market Size (2025) | USD 75.10 Million |

| Market Size (2030) | USD 121.40 Million |

| Growth Rate (2025 - 2030) | 10.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Data Center Immersion Cooling Fluid Market Analysis by Mordor Intelligence

The South America data center immersion cooling fluid market size reached USD 75.3 million in 2025 and is forecast to climb to USD 121.2 million by 2030, advancing at a 10.4% CAGR over the period. This trajectory underscores how digital-first public- and private-sector initiatives, record hyperscale construction and stringent sustainability targets are reshaping data-center thermal design in the region. Operators are scaling power-dense racks packed with AI and machine-learning accelerators, creating heat loads that conventional air solutions cannot manage cost-effectively. Large capital inflows amplify the opportunity: Amazon Web Services pledged USD 4 billion for Chilean capacity in May 2025, while Patria Investments established a USD 1 billion vehicle devoted to Brazilian facilities. Water scarcity across the Andean belt, electricity-cost inflation topping 15% year-over-year in Brazil and emerging ESG mandates are accelerating the switch to liquid media that cut power-usage-effectiveness ratios by up to 40%.

Key Report Takeaways

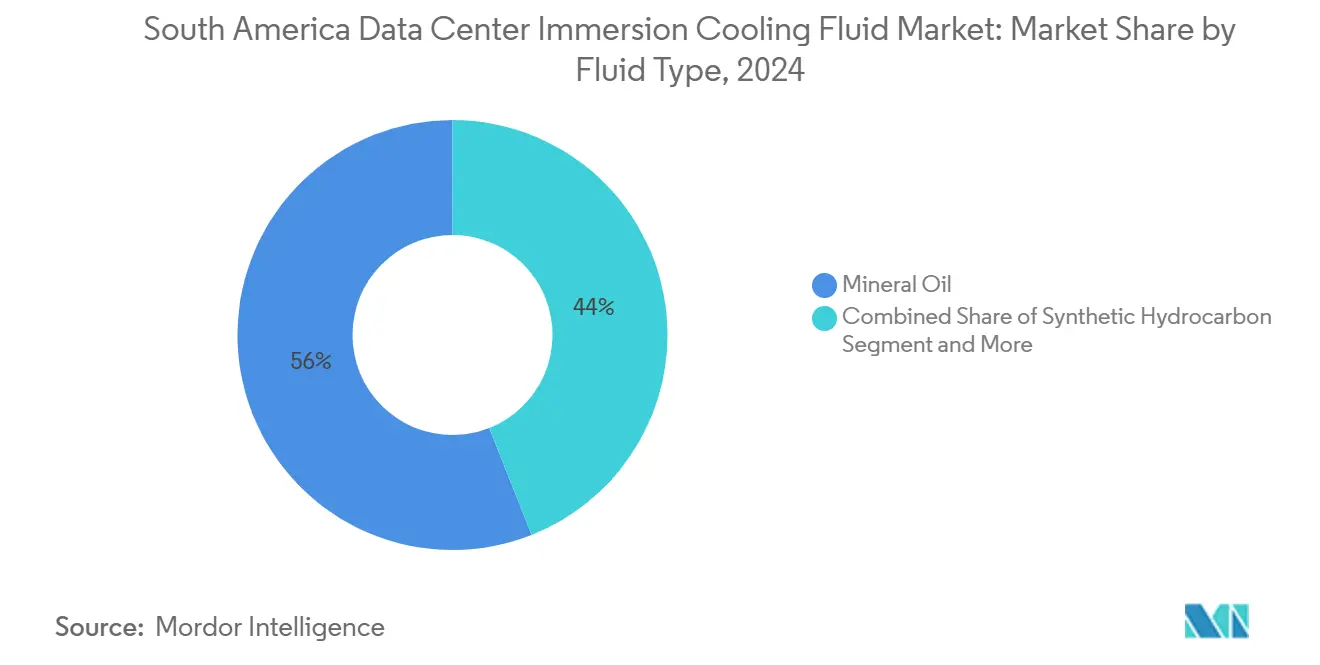

- By fluid type, mineral oil led with 56% of South America data center immersion cooling fluid market share in 2024, while bio-based esters posted the fastest 10.81% CAGR through 2030.

- By phase type, single-phase solutions commanded 69% share of the South America data center immersion cooling fluid market size in 2024 and are projected to expand at an 11.21% CAGR to 203

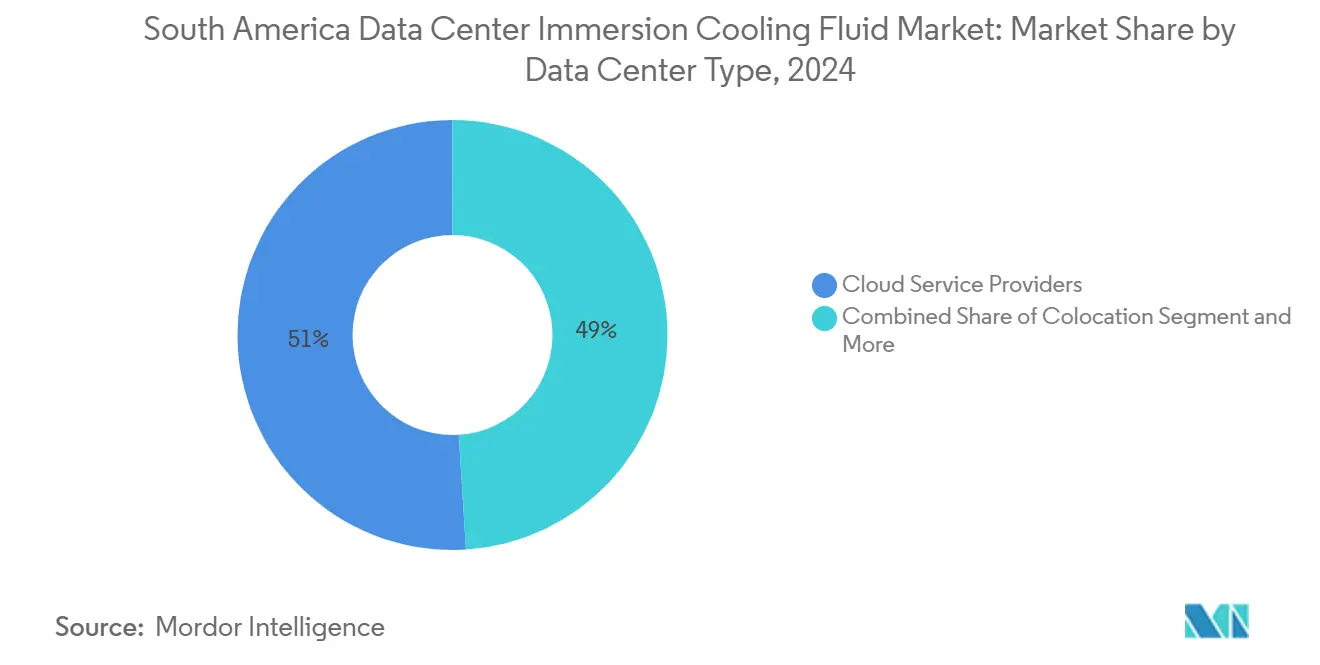

- By data center type, cloud service providers accounted for 51% revenue share in 2024; edge and on-premise facilities are forecast to be the fastest-growing, at 12.11% CAGR to 2030.

- By end-user industry, IT/ITES held 41% share of the South America data center immersion cooling fluid market size in 2024, while healthcare exhibits the highest projected 11.3% CAGR through 2030.

South America Data Center Immersion Cooling Fluid Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing hyperscale investments across Brazil and Chile | +2.8% | Brazil, Chile, spillover to Argentina | Medium term (2-4 years) |

| Rising electricity prices pushing TCO optimization | +2.1% | Region-wide; strongest in Brazil, Argentina | Short term (≤ 2 years) |

| Water scarcity in Andean regions encouraging liquid cooling | +1.9% | Chile, Peru; influence on Colombia | Long term (≥ 4 years) |

| Regional AI/ML cluster deployments in fintech and e-commerce | +1.7% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Government green-data-center incentives | +1.2% | Brazil, Chile; expanding to Colombia | Medium term (2-4 years) |

| Lower-carbon bio-based ester adoption to meet ESG reporting | +0.8% | Early adoption in Brazil, Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Hyperscale Investments Across Brazil and Chile

Amazon Web Services earmarked USD 4 billion for Chilean infrastructure in May 2025, while Scala Data Centers proposed a USD 50 billion AI City campus in São Paulo that will rely on immersion tanks to cool >40 kW-per-rack clusters, elevating demand for South America data center immersion cooling fluid market solutions. Tecto’s 200 MW expansion delivered in December 2024 further illustrates scale benefits that compress fluid procurement costs region-wide.

Rising Electricity Prices Pushing TCO Optimization

Brazilian tariffs rose 15% in 2024 and Argentine subsidy cuts tightened operating margins, prompting operators to adopt single-phase baths that lower fan energy draw and eliminate CRAC units.[1]Brazilian Ministry of Mines and Energy, “Electricity tariffs rise 15% in 2024,” gov.br iM Data Centers achieved a 1.15 PUE at its Miami site using Accelsius direct-to-chip loops, far below the 1.6 regional air-cooled average, validating total-cost-of-ownership gains. Shell’s May 2025 Intel certification assures fluid reliability for scale rollouts.

Water Scarcity in Andean Regions Encouraging Liquid Cooling

Google redesigned its Chile projects after authorities flagged Atacama water stress, highlighting how immersion eliminates 1.8 liters per kWh of cooling demand.[2]Google Cloud, “Chile region redesign for water sustainability,” cloud.google.com Peru now requires usage reporting for facilities >5 MW, and Colombia’s 2025 standards effectively mandate closed-loop systems, positioning South America data center immersion cooling fluid market adoption as a compliance lever.

Regional AI/ML Cluster Deployments in Fintech and E-commerce

MercadoLibre’s fraud-detection GPU grids in São Paulo and Buenos Aires run at 45 kW per rack; CloudWalk logged 99.9% uptime during Brazil’s 2024 Black Friday after switching to immersion cabinets, illustrating performance resilience critical to a fintech sector predicted to grow 28% annually.[3]MercadoLibre Investor Relations, “AI logistics expansion uses liquid cooling,” mercadolibre.com

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited local production of specialty coolants increasing imports | –1.8% | Highest in Peru, Colombia | Short term (≤ 2 years) |

| Higher upfront CAPEX versus legacy air cooling | –1.5% | Pronounced in Argentina, Peru | Short term (≤ 2 years) |

| Lack of regional standards and certification bodies | –1.2% | Region-wide | Medium term (2-4 years) |

| Supply-chain uncertainties amid PFAS regulatory transitions | –0.9% | Global impact felt locally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront CAPEX Versus Legacy Air Cooling

Immersion systems may require 40–60% higher day-one spend because of tanks, pumps and fluid monitoring; currency depreciation in Argentina and Peru amplifies sticker shock, extending payback horizons despite long-run savings.

Limited Local Production of Specialty Coolants Increasing Import Costs

The region imports nearly all synthetic ester and fluorocarbon stock. Chinese R32 spot prices jumped 108% in 2024, lifting delivered costs by 25-35% once tariffs and freight are added, a hurdle for smaller operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fluid Type: Bio-Based Esters Drive Sustainability Transition

Bio-based esters are on track to expand at a 10.81% CAGR to 2030, narrowing the gap with mineral oil’s 56% 2024 share. Products such as Envirotemp 360 meet OECD 301B biodegradability and flash point >283 °C, supporting ESG scorecards. Mineral oil still anchors large-scale single-phase deployments because of low cost per liter and proven compatibility. TotalEnergies’ Cell-Shield EV pilot shows ester chemistry can cross from vehicles to racks, widening addressable demand.

Second-tier synthetics and fluorocarbons cater to niche two-phase nodes but face PFAS scrutiny. Dow’s ISCC-PLUS-certified bio-propylene-glycol illustrates supplier pivots to low-carbon feedstocks likely to influence procurement in the South America data center immersion cooling fluid market.

By Phase Type: Single-Phase Systems Dominate Through Operational Simplicity

Single-phase baths captured 69% revenue in 2024 and should retain dominance at 11.21% CAGR. Castrol’s ON PG25, launched December 2024, targets direct-to-chip loops with low viscosity and material compatibility. Lubrizol’s CompuZol adds higher heat-flux headroom, cutting throttling incidents.

Two-phase demand is steady in extreme AI-training hubs; Chemours partnered in Q1 2025 with Navin Fluorine to shore up local capacity, signaling maturation without eclipsing single-phase simplicity.

By Data Center Type: Edge Computing Drives Fastest Growth

Cloud service providers held 51% in 2024, yet edge and on-premise nodes will post a 12.11% CAGR as latency-sensitive AI inference and sovereignty rules proliferate. Financial-service firms deploying 30 kW-plus racks in constrained metro sites treat liquid cooling as an enabler. CyrusOne’s Intelliscale offering packages tanks and CDU skids for both hyperscale and micro-edge footprints.

Colocation operators blend immersion suites into existing campuses to capture premium tenants. The South America data center immersion cooling fluid market thus spans megawatt-class halls and 100-kW containerized pop-ups, creating parallel supply-chain channels for bulk and packaged fluids.

By End-User Industry: Healthcare Emerges as Growth Leader

IT/ITES retained 41% share in 2024, yet hospital groups and genomic labs will log an 11.3% CAGR, chasing AI-powered diagnostics that push power density to 50 kW per rack. Pharmaceutical modeling workloads rely on sustained GPU clocks only achievable under liquid cooling. BFSI institutions adopt tanks for real-time risk engines, while government and defense installations favor sealed baths to meet air-gap protocols. Media studios rendering 8K content also join the South America data center immersion cooling fluid market adoption curve, underscoring thermal versatility across verticals.

Geography Analysis

Brazil anchors more than half of South America's data center immersion cooling fluid market revenues, thanks to tax holidays enacted in April 2025, Patria’s USD 1 billion fund, and São Paulo’s AI City blueprint. The fintech cluster led by MercadoLibre and CloudWalk sustains baseline consumption.

Chile ranks second; its USD 2.5 billion National Data Centers Plan, plus AWS’s USD 4 billion spend, leverages liquidity into a water-stressed landscape where immersion’s zero-water trait is pivotal. Cyber-security law enacted in January 2025 localizes compute, further tightening domestic demand.

Argentina and Colombia show early-stage momentum. Buenos Aires free-trade zones trim import duties on fluids, and Colombia’s 2025 water-efficiency code nudges new builds toward closed-loop cooling. Peru and secondary markets remain nascent but mining digitalization initiatives could lift immersion adoption as rack densities grow.

Competitive Landscape

The supplier field is moderately fragmented: petro-chem majors (Shell, Chemours, 3M) provide base fluids, while integrators (Submer, Green Revolution Cooling) deliver turnkey deployments. Intel’s certification of Shell in May 2025 elevates multi-vendor credibility. Chemours’ Navin tie-up expands two-phase output to hedge PFAS transitions.

Sustainability creates whitespace for bio-ester specialists such as Cargill and TotalEnergies; FUCHS entered in July 2025 with RENOLIN FECC single-phase line, leveraging lubricant channels to reach regional distributors. Lubrizol targets cross-sector EV and compute thermal needs. As customers pivot to outcome-based service contracts, vendors bundling fluid supply, monitoring and reclamation are positioned to gain share within the South America data center immersion cooling fluid market.

South America Data Center Immersion Cooling Fluid Industry Leaders

3M

The Dow Chemical Company

Exxon Mobil Corporation

Shell plc

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: 3M rolled out Novec 7300 engineered fluid aimed at single-phase racks.

- July 2025: FUCHS unveiled RENOLIN FECC 5, FECC 5 SYNTH and FECC 7 fluids for data-center tanks.

- June 2025: Chemours raised Q2 guidance on surging Opteon demand; Corpus Christi capacity ramps.

- May 2025: AWS confirmed USD 4 billion Chile expansion incorporating water-saving cooling.

South America Data Center Immersion Cooling Fluid Market Report Scope

| Mineral Oil |

| Synthetic Hydrocarbon |

| Fluorocarbon-based Fluids |

| Bio-based Esters |

| Single-Phase |

| Two-Phase |

| Cloud Service Providers |

| Colocation |

| On-Premise / Enterprise / Edge |

| IT / ITES |

| BFSI |

| Healthcare |

| Government and Defense |

| Media and Entertainment |

| Other End-Users |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Fluid Type | Mineral Oil |

| Synthetic Hydrocarbon | |

| Fluorocarbon-based Fluids | |

| Bio-based Esters | |

| By Phase Type | Single-Phase |

| Two-Phase | |

| By Data Center Type | Cloud Service Providers |

| Colocation | |

| On-Premise / Enterprise / Edge | |

| By End-User Industry | IT / ITES |

| BFSI | |

| Healthcare | |

| Government and Defense | |

| Media and Entertainment | |

| Other End-Users | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America data center immersion cooling fluid market in 2025?

It stands at USD 75.3 million with a projected rise to USD 121.2 million by 2030.

Which fluid type leads current deployments?

Mineral oil holds 56% share, though bio-based esters are growing fastest at 10.81% CAGR.

Why are operators switching from air cooling to immersion?

Immersion lowers PUE by up to 40%, removes water use and handles 40 kW-plus rack densities common in AI and fintech workloads.

Which country offers the strongest policy support?

Brazil, thanks to April 2025 tax exemptions and a forthcoming National Data Center Plan.

What segment will grow quickest through 2030?

Edge and on-premise facilities are projected to post a 12.11% CAGR as latency and sovereignty rules proliferate.

How fragmented is the supplier landscape?

Moderately fragmented; top five hold roughly 60%, earning a concentration score of 6.

Page last updated on: