Africa Data Center Immersion Cooling Fluid Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

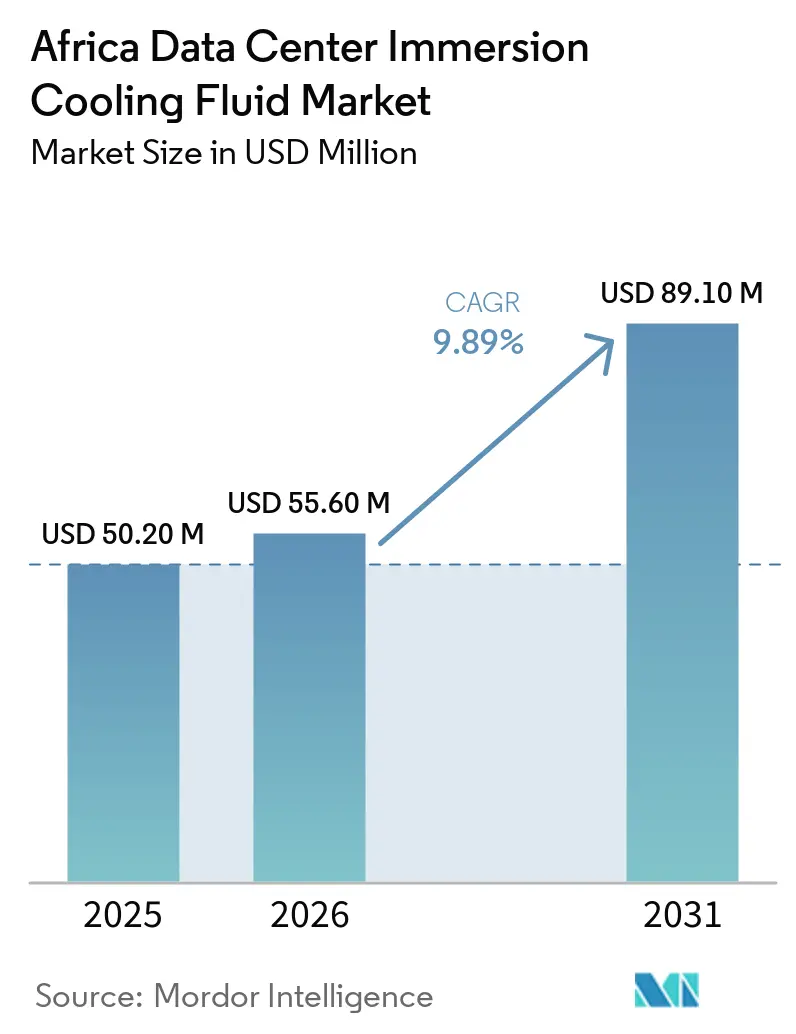

| Base Year Market Size (2025) | USD 50.20 Million |

| Market Size (2026) | USD 55.60 Million |

| Market Size (2031) | USD 89.10 Million |

| Growth Rate (2026 - 2031) | 9.89% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Data Center Immersion Cooling Fluid Market Analysis by Mordor Intelligence

The Africa data center immersion cooling fluid market size is projected to expand from USD 50.20 million in 2025 and USD 55.60 million in 2026 to USD 89.10 million by 2031, registering a CAGR of 9.89% between 2026 to 2031. Rapid hyperscale construction in Johannesburg and Nairobi, electricity‐price inflation, and escalating AI/ML compute density underpin demand for immersion fluids, while 3M’s PFAS exit channels spending into bio-ester substitutes. South Africa and Nigeria jointly contributed more than 60% of 2025 revenue, yet Kenya records the quickest expansion as data-center tax incentives drive project approvals. Mineral oil retained the largest share thanks to price advantage, whereas bio-esters deliver the fastest growth due to ESG mandates. Single-phase systems dominate deployments today, but two-phase variants are scaling inside hyperscale footprints to maximize energy savings. Competitive intensity remains moderate; global chemical suppliers are pairing with local integrators to secure national tenders, while regional blenders eye import-substitution plays.

Key Report Takeaways

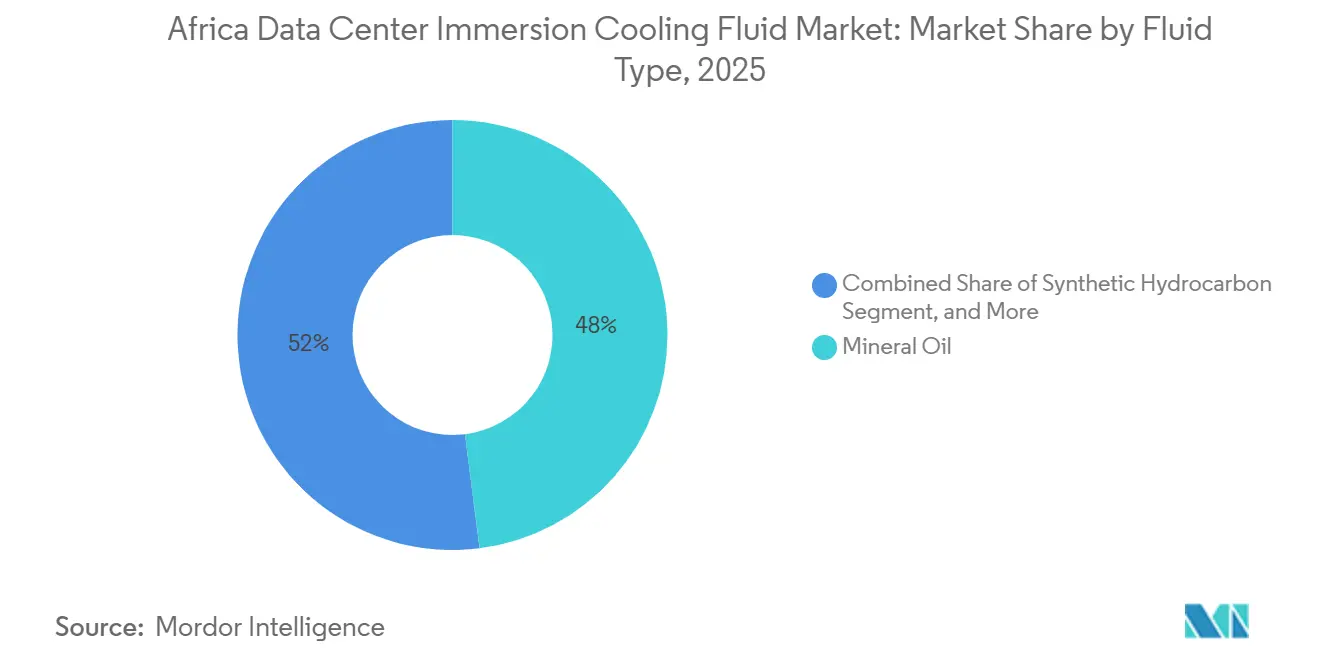

- By fluid type, mineral oil led with 48.0% of the Africa data center immersion cooling fluid market share in 2025.

- By phase type, single-phase systems accounted for 73.5% share of the Africa data center immersion cooling fluid market size in 2025.

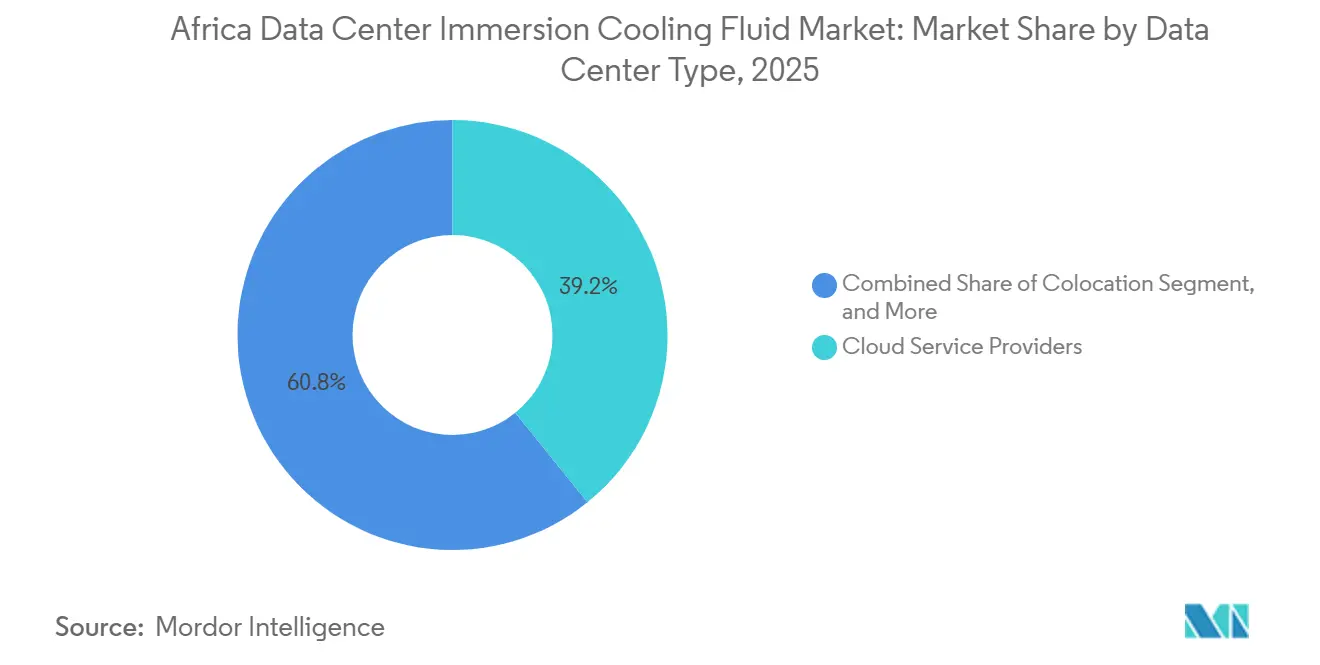

- By data center type, cloud service providers held 39.2% revenue share in 2025.

- By end-user industry, IT/ITES captured 40.1% of 2025 spend.

- By geography, South Africa and Nigeria collectively commanded 60% of 2025 revenue, while Kenya is the fastest-growing country at double-digit CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Data Center Immersion Cooling Fluid Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Hyperscale build-outs in Johannesburg and Nairobi corridors | +2.8% | South Africa, Kenya, Nigeria | Medium term (2-4 years) |

| Rising electricity tariffs driving TCO optimization | +2.1% | Nigeria, Kenya, South Africa | Short term (≤ 2 years) |

| Severe water stress in Cape Town and Sahel favoring liquid cooling | +1.9% | South Africa, West Africa Sahel | Long term (≥ 4 years) |

| Pan-African AI/ML clusters for fintech and e-commerce | +1.7% | Nigeria, Kenya, South Africa, Morocco | Medium term (2-4 years) |

| Data-center tax incentives under Kenya Investment Promotion Act | +1.2% | Kenya, East Africa | Medium term (2-4 years) |

| Shift to PFAS-free bio-ester fluids for ESG reporting | +1.0% | South Africa, Nigeria | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hyperscale build-outs in Johannesburg and Nairobi corridors

Africa’s two most active data-center corridors are now anchored by Teraco’s USD 442 million facility expansion and Equinix’s USD 390 million entry plan, both of which specify immersion-ready halls capable of 100 kW-plus racks. High fiber density, carrier hotels, and submarine-cable proximity let operators guarantee sub-40 ms latency to European hubs, a prerequisite for GPU training workloads. Project lenders insist on PUE targets under 1.2, effectively locking in liquid cooling as the baseline architecture. Equipment OEMs follow the investment, placing forward-stock depots in Gauteng and Kiambu counties to shorten lead times for fluid systems. The clustering effect lowers logistics costs for dielectric suppliers, making bulk contracts viable for secondary metro builds.

Rising electricity tariffs driving TCO optimization

Nigeria’s Band A tariff leap to NGN 225/kWh (USD 0.14/kWh) in 2024 pushed operating expenditure up by more than 30% for Tier III facilities. Kenya’s commercial tariff sits even higher at USD 0.202/kWh, while South Africa’s 2025 Eskom hike averages 18.7% on large-power users. Immersion cooling cuts server-fan draw and eliminates chiller loads, shrinking energy needs 40-50% and pushing blended PUE close to 1.05, which in turn shaves two to three years off payback periods. CFOs now build tariff-inflation scenarios into investment memos, often finding liquid cooling the least-cost option beyond year 4 of asset life. The tariff pressure also boosts interest in on-site solar-plus-battery microgrids, whose capex aligns naturally with immersion’s reduced HVAC footprint.

Severe water stress in Cape Town and Sahel favoring liquid cooling

Day-Zero rationing in 2025 again limited municipal water allocations around Cape Town industrial zones, forcing several air-cooled data centers onto partial shutdown schedules. Immersion systems consume negligible water, allowing operators to comply with drought directives without derating IT loads. The Sahel’s chronic aridity affects cooling-tower performance, driving temperature spikes that immersion designs avoid by using sealed dielectric loops. Local governments increasingly incorporate water-use factors into environmental-impact reviews, giving immersion projects a faster permitting track.[1]World Health Organization, “Drinking Water Fact Sheet,” WHO.int Coastal Mauritius shows a different path with seawater air-conditioning, yet its 86% energy-saving benchmark still trails the efficiency of two-phase tanks now piloted in Gauteng.

Pan-African AI/ML clusters for fintech and e-commerce

Flutterwave’s 40-country payment rail generates bursty inference loads topping 30 kW per rack, far beyond traditional CRAH envelopes.[2]Flutterwave, “Company Overview and Expansion,” Flutterwave.com McKinsey forecasts fintech revenues climbing from USD 10 billion in 2023 to USD 47 billion by 2028, equating to a quadrupling of transaction-processing horsepower. To maintain millisecond-level fraud-detection latency, operators colocate GPU clusters in Lagos, Nairobi, and Casablanca, where immersion enables higher density without air-flow bottlenecks. AI regulatory sandboxes run by Nigeria’s NITDA and Kenya’s CAK further spur local model-training that benefits from liquid cooling’s thermal uniformity. Edge-compute nodes supporting mobile-money agents in rural zones also favor sealed tanks, which tolerate dust and high ambient temperatures better than fan-based rigs.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Scarce local blending of specialty dielectrics inflating imports | –1.8% | West and Central Africa | Medium term (2-4 years) |

| Higher up-front CAPEX vs. legacy air cooling | –1.5% | Nigeria, Kenya | Short term (≤ 2 years) |

| Absence of Africa-specific immersion-cooling safety standards | –1.2% | Continental | Long term (≥ 4 years) |

| Supply-chain risk amid global PFAS phase-out | –0.9% | Import-dependent markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarce local blending of specialty dielectrics inflating imports

Only two sub-Saharan facilities possess ISO-certified blending lines for dielectric fluids, forcing most buyers to import finished product at freight rates exceeding USD 3,000 per ISO tank.[3]C&EN, “3M Exit from PFAS Market Creates Supply-Chain Disruption,” Cen.acs.org Duties range between 5-10% depending on HS code classification, and forex shortages often delay customs clearance by weeks, leaving racks idle. Smaller operators cannot meet minimum-order quantities, paying spot premiums of 15-20% over contract pricing. Domestic chemical firms have considered toll-blending agreements, yet high feedstock purity requirements deter investment without guaranteed take-or-pay volumes. Until local capacity improves, supply risk and elevated landed cost will cap adoption in price-sensitive metros.

Higher up-front CAPEX vs. legacy air cooling

Immersion tanks, CDUs, and fluid inventory add USD 200-300 per server compared with hot-aisle containment, doubling initial mechanical-electrical budgets for new builds in Nigeria and Kenya. Regional banks charge double-digit interest, elongating breakeven timelines for operators without dollar-denominated revenue streams. Although total cost of ownership improves long-term, CFOs often prioritize near-term liquidity over life-cycle savings when exchange-rate volatility clouds payback models. Equipment leasing and vendor-finance packages exist, yet they frequently require hard-currency collateral that local firms lack. Consequently, some developers postpone immersion adoption until expansion phases when cash flow from initial capacity can subsidize the premium.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fluid Type: Bio-esters gain ESG momentum

Mineral oil secured the highest 48.0% share of the Africa data center immersion cooling fluid market in 2025, owing to favorable pricing and broad availability. Bio-esters, though costlier, post the segment’s quickest 11.9% CAGR as asset managers scrutinize sustainability disclosures. The Africa data center immersion cooling fluid market size for bio-esters is projected to climb sharply as PFAS-free mandates spread across procurement frameworks. Synthetic hydrocarbons target niche high-heat applications, while fluorocarbon products trend downward following PFAS prohibitions.

Bio-ester suppliers such as TotalEnergies (BioLife) and Cargill (NatureCool) pitch biodegradability advantages to hyperscale bidders, and Chemours’ May 2025 alliance with Navin Fluorine adds Opteon production closer to the continent. Local formulators explore palm-derivative feedstocks to cut import bills, though financing hurdles persist.

By Phase Type: Two-phase systems target hyperscale

Single-phase designs represented 73.5% of 2025 revenue, anchoring the Africa data center immersion cooling fluid market share among operators seeking straightforward rollout. Two-phase installations, while only a minority today, are forecast to grow 11.7% annually as they enable GPU rack densities exceeding 100 kW. The Africa data center immersion cooling fluid market size for two-phase fluids could double by 2030 if hyperscale AI clusters adopt the topology at scale.

Johnson Controls’ September 2025 modular CDU launch mitigates complexity fears by offering plug-and-play expansion; early pilots in Lagos and Nairobi demonstrate 20% TCO savings versus air-cooled plus CRAH retrofits.

By Data Center Type: Edge computing drives distributed demand

Cloud service providers contributed 39.2% of 2025 spending, setting the benchmark for the Africa data center immersion cooling fluid market. Edge facilities, however, post a 12.7% CAGR as telcos and fintechs place micro-data-centers near population clusters to shave latency. Visa’s Johannesburg processing hub exemplifies edge-adjacent architecture that leans on immersion to minimize moving parts in remote sites.

Colocation operators enlarge footprint to capture multitenant demand, while on-premise enterprise facilities slow amid capital rationing. Governments add immersion pods inside sovereign clouds that host national ID and tax systems, often financed through public-private vehicles backed by regional development banks.

By End-User Industry: Healthcare digitization accelerates demand

IT/ITES users held 40.1% of 2025 revenue, underpinning the Africa data center immersion cooling fluid market share with sustained cloud outsourcing. Healthcare workloads, yet, will advance at 11.05% CAGR, reflecting telemedicine, PACS imaging, and genomics analysis scale-ups. The Africa data center immersion cooling fluid market size linked to healthcare is forecast to outpace BFSI after 2027, supported by donor-funded e-health programs.

BFSI modernization remains robust as Ecobank and others consolidate core banking on AI-capable hardware, while media streaming crews adapt immersion racks to manage transcoding spikes. Defense and public-sector demand persists but is gated by budget cycles and cybersecurity clearances.

Geography Analysis

South Africa anchors regional revenue with mature fiber grids and proactive green-building codes that legitimize immersion CAPEX. Nigeria follows, powered by fintech transaction volumes and data-localization directives that elevate rack densities. Kenya, buoyed by tax holidays under the Investment Promotion Act, records the highest CAGR, attracting East Africa’s first OCP-certified immersion hall in Q4 2025. Egypt and Morocco occupy the next tier; Cairo’s planned USD 450 million campus taps plentiful solar capacity, while Casablanca’s dual-feed wind and hydro mix markets the site as Net-Zero-Ready. Rest-of-Africa markets, notably Ghana and Côte d’Ivoire, open smaller pods near cable landings, using immersion to offset unreliable HVAC parts supply.

Electricity cost differentials shape deployment patterns; Nigeria’s spot PPA deals exceed USD 0.14/kWh, whereas Morocco secures sub-USD 0.08/kWh solar off-takes, influencing fluid payback calculus. Water scarcity further tilts choices, Cape Town mandates 40% water-consumption cuts on new builds, making air-cooled evaporative towers unviable. Currency volatility introduces import-cost risk, leading some operators to stock six-month fluid buffers.

Policy harmonization lags; cross-border data-flow rules and double-taxation treaties remain inconsistent, prompting multinationals to replicate capacity across jurisdictions. Nonetheless, pan-regional fiber corridors (2Africa cable) will compress latency and could spur immersion retrofits in secondary metros by 2028.

Competitive Landscape

Global chemical majors, Chemours, ExxonMobil, and TotalEnergies, supply most fluid volumes, yet none exceeds a 12% individual share, and the top five together control roughly 35%. System integrators such as Vertiv, Submer, and Schneider Electric bundle tanks, CDUs, and monitoring platforms. Schneider’s USD 850 million Motivair deal added a proprietary coolant portfolio that resonates with hyperscale RFPs.

Local participants explore toll-blending partnerships to cut landed costs. Nigerian specialty-chemicals maker Notore is piloting base-oil purification for reuse, while South Africa’s Sasol reviews bio-ester co-processing. Market entrants differentiate via ESG compliance, Engineered Fluids promotes 100% biodegradable formulations, whereas BitCool courts GPU miners with warranty-backed thermal envelopes.

Service wrap-arounds gain importance; vendors now embed leak-detection analytics and on-site fluid reclamation in multiyear contracts. As procurement frameworks increasingly reference OCP and FM Global guidelines, suppliers that certify early should capture outsized share of late-adopter markets.

Africa Data Center Immersion Cooling Fluid Industry Leaders

3M

The Dow Chemical Company

Exxon Mobil Corporation

Shell plc

Vertiv

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Chemours and Navin Fluorine start Opteon™ two-phase fluid production under a multi-year technology licensing accord.

- July 2025: Visa commissions its first African data center in Johannesburg, featuring full-rack immersion tanks for payment authorization workloads.

- September 2025: Johnson Controls debuts modular CDUs optimized for two-phase cooling, enabling 1 MW blocks to be added without process downtime.

- October 2024: Schneider Electric closes the USD 850 million Motivair acquisition, integrating coolant intellectual property into its Galaxy line.

Africa Data Center Immersion Cooling Fluid Market Report Scope

| Mineral Oil |

| Synthetic Hydrocarbon |

| Fluorocarbon-based Fluids |

| Bio-based Esters |

| Single-Phase |

| Two-Phase |

| Cloud Service Providers |

| Colocation |

| On-Premise / Enterprise / Edge |

| IT / ITES |

| BFSI |

| Healthcare |

| Government and Defense |

| Media and Entertainment |

| Other End-Users |

| South Africa |

| Nigeria |

| Kenya |

| Egypt |

| Morocco |

| Rest of Africa |

| By Fluid Type | Mineral Oil |

| Synthetic Hydrocarbon | |

| Fluorocarbon-based Fluids | |

| Bio-based Esters | |

| By Phase Type | Single-Phase |

| Two-Phase | |

| By Data Center Type | Cloud Service Providers |

| Colocation | |

| On-Premise / Enterprise / Edge | |

| By End-User Industry | IT / ITES |

| BFSI | |

| Healthcare | |

| Government and Defense | |

| Media and Entertainment | |

| Other End-Users | |

| By Country | South Africa |

| Nigeria | |

| Kenya | |

| Egypt | |

| Morocco | |

| Rest of Africa |

Key Questions Answered in the Report

How fast is immersion-cooling fluid demand growing across African data centers?

Aggregate spending is projected to reach USD 89.1 million by 2031, equating to a 9.89% CAGR over the period.

Which fluid type is gaining the strongest momentum with African operators?

Bio-ester formulations post the highest 11.9% CAGR as data-center owners pivot toward PFAS-free, ESG-compliant alternatives while mineral oil remains the volume leader.

Why are two-phase cooling systems attracting hyperscale builders?

The topology supports rack densities above 100 kW, delivers energy-use reductions that push PUE toward 1.05, and is now easier to deploy after Johnson Controls' modular CDU launch in 2025.

How do rising electricity tariffs in markets such as Nigeria influence cooling choices?

Tariffs as high as USD 0.14/kWh make energy savings critical; immersion solutions can cut cooling power by 40-50%, often offsetting their higher upfront cost within a few years.

What role do sustainability mandates play in fluid selection?

Institutional investors increasingly require environmental disclosures, prompting operators to replace PFAS-based fluorocarbons with biodegradable bio-esters to secure financing and meet reporting frameworks.

Is supply-chain risk a concern after 3Ms withdrawal from PFAS fluids?

Yes; the exit tightens global supply of fluorocarbon coolants, so African buyers hedge by pre-ordering inventory or sourcing from new entrants like Chemours-Navin Fluorine's Opteon line.

Page last updated on: