Middle East Data Center Immersion Cooling Fluid Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

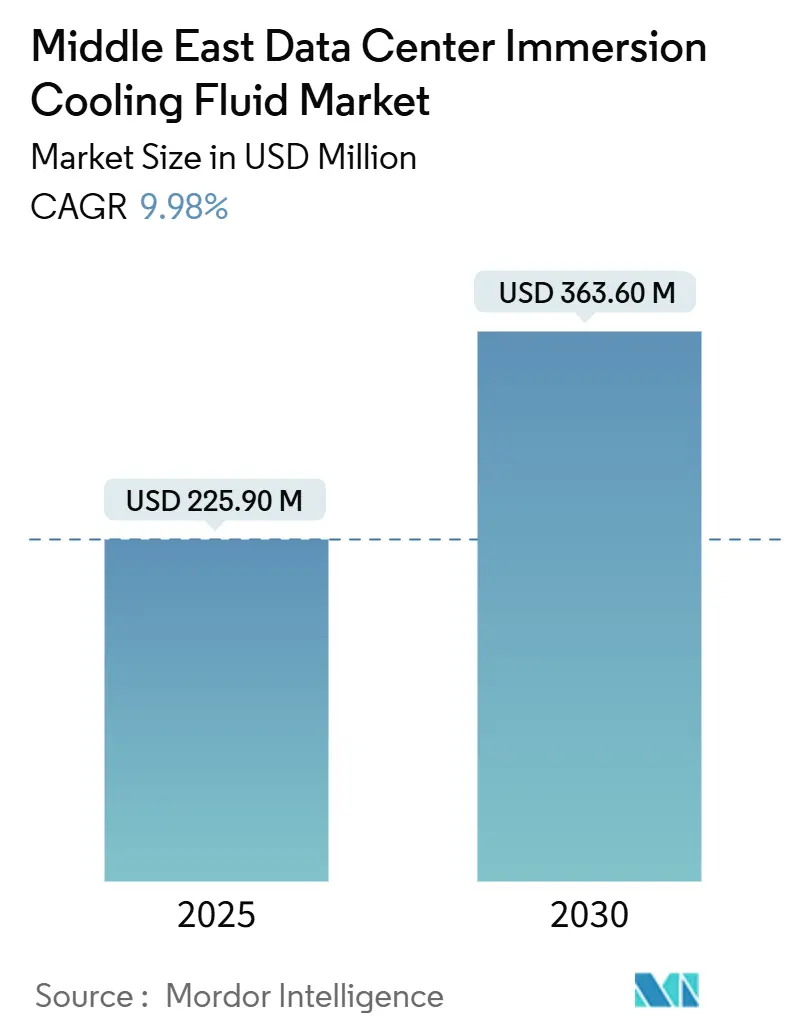

| Market Size (2025) | USD 225.90 Million |

| Market Size (2030) | USD 363.60 Million |

| Growth Rate (2025 - 2030) | 9.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Data Center Immersion Cooling Fluid Market Analysis by Mordor Intelligence

The Middle East data center immersion cooling fluid market size is USD 225.9 million in 2025 and is projected to reach USD 363.6 million by 2030, registering a 9.95% CAGR. This growth mirrors a rapid build-out of hyperscale facilities across Saudi Arabia and the UAE, where compute densities already surpass 30 kW per cabinet and regularly push toward 50 kW. Mineral-oil and synthetic-hydrocarbon baths remain the baseline fluids in most hyperscale halls, yet sovereign wealth funds and technology ministries now attach procurement incentives to bio-based ester solutions that deliver lower carbon intensity. Budget reallocations caused by rising Gulf electricity tariffs further highlight total-cost-of-ownership benefits, because immersion platforms cut cooling energy by up to 70% compared with legacy CRAC rooms. Finally, severe water scarcity across the GCC reinforces the business case; immersion architectures eliminate evaporative losses entirely, sparing up to 426 billion L of potable water in 2030 versus status-quo designs. These intertwined drivers collectively spur steady demand for specialty fluids, custom power-distribution units, and pre-engineered tanks that support the region’s next generation of AI accelerators.

Key Report Takeaways

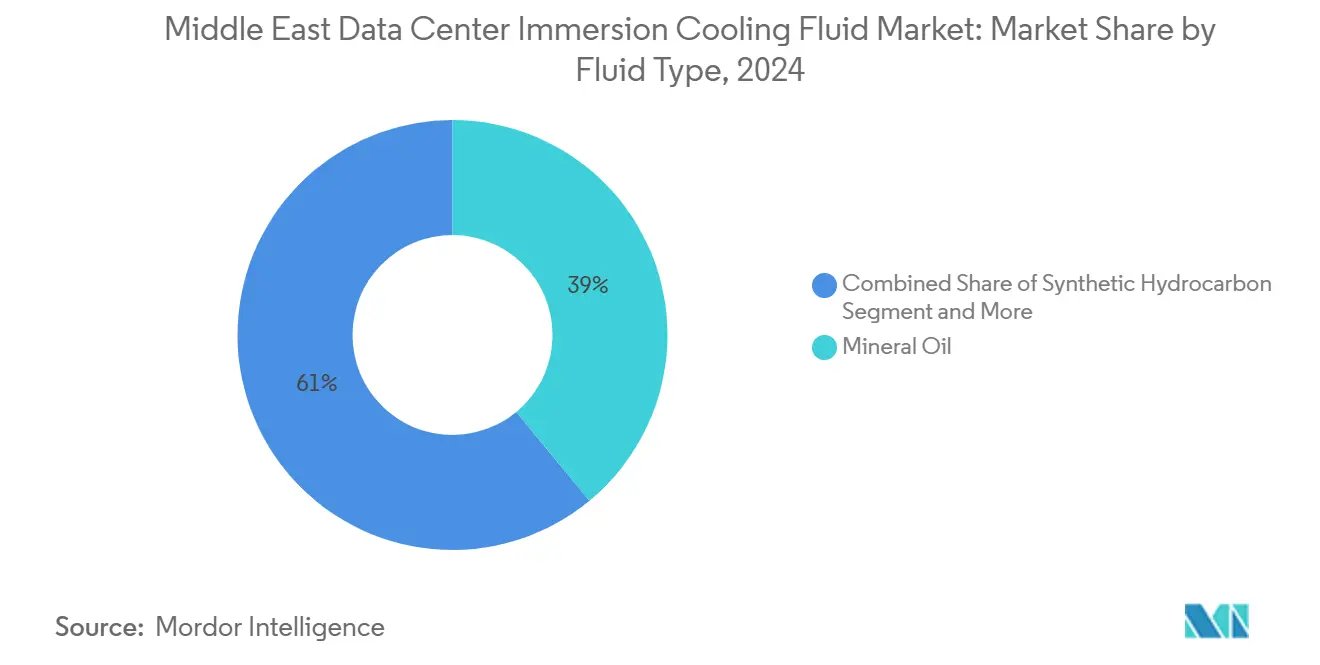

- By fluid type, mineral oil held 39% of the Middle East data center immersion cooling fluid market share in 2024.

- By phase type, single-phase systems captured 64% of the Middle East data center immersion cooling fluid market size in 2024.

- By data center type, hyperscale and cloud service providers commanded 55% share of the Middle East data center immersion cooling fluid market size in 2024 and are growing at 12.11% CAGR through 2030.

- By end-user industry, healthcare usage is set to climb at an 11.1% CAGR between 2025-2030.

Middle East Data Center Immersion Cooling Fluid Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Mega-scale cloud investments by Saudi Vision 2030 hyperscalers | 2.8% | Saudi Arabia, with spillover to UAE and Qatar | Medium term (2-4 years) |

| Accelerating AI/ML cluster build-outs in UAE fintech and sovereign funds | 2.1% | UAE core, expansion to Kuwait and Bahrain | Short term (≤ 2 years) |

| Electricity-tariff reforms boosting focus on TCO optimisation | 1.9% | GCC-wide, strongest impact in Saudi Arabia and UAE | Long term (≥ 4 years) |

| Severe water-stress across GCC favouring liquid over evaporative cooling | 1.7% | GCC countries, particularly Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Green-data-center incentives (e.g., KSA's tax holidays for >PUEx1.3) | 1.2% | Saudi Arabia, with policy replication across GCC | Long term (≥ 4 years) |

| Shift toward PFAS-free, bio-ester fluids to meet ESG and Shariah screens | 0.8% | Regional, strongest in UAE and Qatar sovereign funds | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mega-scale Cloud Investments by Saudi Vision 2030 Hyperscalers

Saudi Arabia is channeling more than USD 20 billion into AI infrastructure that mandates cabinets able to dissipate 50 kW-plus loads. DataVolt’s USD 5 billion pact with Supermicro specifies immersion tanks for every new hall, anchoring a domestic supply chain for high-flash-point mineral oils and synthetic hydrocarbons.[1]DataVolt Technologies, “Supermicro Collaboration Targets Immersion,” datavolt.com The Saudi Telecom Company’s USD 266 million capacity addition also embeds liquid baths as standard, confirming acceptance beyond experimental pilots. Demand for immersion fluids in the kingdom is therefore forecast to rise 180% between 2025-2027, a surge that positions Saudi vendors as regional leaders in fluid reclamation and recycling services. Beyond hyperscale halls, the Global AI Hub Law classifies data centers as critical infrastructure, unlocking tax credits for installations that reach PUE below 1.3 and accelerating volume orders for bio-ester blends.

Accelerating AI/ML Cluster Build-outs in UAE Fintech and Sovereign Funds

The UAE’s fintech sector deploys always-on AI engines for trading and compliance that need stable sub-50 °C chip temperatures. G42’s 5 GW AI campus integrates two-phase immersion as its base design, setting a benchmark for regional service-level agreements.[2]G42, “5 GW AI Campus Announcement,” g42.ai Capital mandates from Mubadala and ADIA layer ESG screens onto every procurement cycle, pushing operators toward bio-ester fluids that align with Shariah investment principles. Microsoft’s local Azure region offers servers pre-qualified for immersion, which normalizes the technology for regulated banking workloads. Edge nodes within the Dubai International Financial Centre adopt compact single-phase tanks, expanding addressable demand outside the country’s mega-campuses.

Electricity-Tariff Reforms Boosting Focus on TCO Optimisation

Progressive withdrawal of Gulf power subsidies means operators now see electricity as a controllable cost rather than a public entitlement. Immersion facilities consume 30-40% less site power and reduce cooling OpEx by up to 95%, slicing payback periods to roughly three years under the new tariff tables. Saudi Arabia’s banded pricing policy, rolled out in 2024, magnifies these savings as servers cycle through seasonal peak rates. The UAE’s time-of-use schedules provide further arbitrage: immersion’s flat efficiency curve delivers predictable bills regardless of ambient spikes above 45 °C. Qatar’s regulator ties permits for ≥10 MW halls to aggressive PUE limits, which in practice prescribes liquid cooling for license compliance. Together, these reforms re-weight capex models toward higher upfront spend and lower lifetime energy outlays.

Severe Water-Stress Across GCC Favouring Liquid Over Evaporative Cooling

Traditional open-loop towers can evaporate nearly 7 L per kWh of heat rejected, a liability in a region that already ranks among the world’s most water-scarce. The International Energy Agency estimates data centers would otherwise absorb 426 billion L annually by 2030 if legacy cooling persists.[3]International Energy Agency, “Data-Center Efficiency in the Middle East,” iea.org Immersion baths remove evaporative stages entirely, satisfying National Water Security Strategy targets in the UAE and dovetailing with Saudi circular-economy regulations. Desalination costs of USD 0.50-0.80 per m³ mean each liter saved carries real monetary value, strengthening internal rate-of-return models for bio-ester upgrades. Water-free operation also broadens site-selection options, allowing facilities to move inland where land is cheaper and grid connections stronger.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited in-region specialty-fluid manufacturing inflating import costs | -1.8% | Regional, strongest impact on smaller markets like Bahrain and Oman | Short term (≤ 2 years) |

| Higher upfront CAPEX versus legacy CRAC / CRAH air cooling | -1.5% | Regional, particularly affecting SME data center operators | Medium term (2-4 years) |

| Absence of Middle-East-specific safety and performance standards | -0.9% | Regional, with strongest impact in emerging markets | Long term (≥ 4 years) |

| Supply-chain uncertainty amid global PFAS phase-out timelines | -0.7% | Global impact, affecting all regional markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited In-Region Specialty-Fluid Manufacturing Inflating Import Costs

Most immersion fluids still originate in Europe or North America, so Gulf buyers incur 25-35% landed-cost premiums and endure lead times beyond eight weeks. Smaller operators struggle to hedge inventory risk or gain favorable payment terms, delaying project roll-outs and tempering immediate penetration. Shell’s decision to launch local blending lines and Cargill’s ester expansion by 2026 should narrow the cost delta, yet capacity additions must keep pace with hyperscale demand spikes. Until then, the logistics burden hollows margins for integrators and slows procurement calendars for government tenders.

Higher Upfront CAPEX Versus Legacy CRAC / CRAH Air Cooling

Turn-key immersion halls cost 40-60% more than mid-range air-cooled suites because tanks, dielectric fluids, and fluid-handling rigs are still niche items. Financing hurdles intensify for SME colocation providers that lack sizable balance sheets or familiarity with residual-value guarantees. Nevertheless, component prices are falling roughly 7% annually as vendors scale volume and standardize part numbers. Industry roadmaps suggest cost parity with high-efficiency air systems by 2028, after which capex objections will ease further. In the interim, creative leasing packages and performance-based energy contracts are emerging to bridge the affordability gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fluid Type: Bio-Based Esters Gain Ground as Compliance Catalyst

Bio-ester blends held 18% of 2024 volume but are tracking a 10.11% CAGR, the fastest among all fluid classes. Their renewable feedstocks satisfy ESG audits and Shariah rules, factors that weigh heavily on GCC sovereign allocators. Cargill and TotalEnergies added Gulf distribution points in 2025, improving supply resilience and lowering freight surcharges. Mineral oil retains leadership with a 39% Middle East data center immersion cooling fluid market share due to proven field reliability, broad OEM lists, and accessible pricing. Shell’s certified immersive blend cleared all major hyperscale acceptance tests in 2025, preserving mineral oil’s relevance for cost-sensitive halls.

Performance and lifecycle economics continue to converge across fluid families as additive chemistries extend ester service life past five years. Meanwhile, PFAS-free synthetic hydrocarbons such as Chemours Opteon 2P50 give operators a middle path between cost and environmental credentials. Over the forecast horizon, demand bifurcates: mineral oils anchor volume in retrofit halls, while bio-esters dominate new sovereign builds that target PUE ≤ 1.2 and zero-waste aspirations. Collectively, these trends reinforce a dual-fluid supply model with localized regeneration hubs.

By Phase Type: Two-Phase Adoption Accelerates at AI Density Thresholds

Single-phase baths still captured 64% of the Middle East data center immersion cooling fluid market size in 2024 because they are easier to operate and provide gentler learning curves for facilities teams. Two-phase designs however register an 11.11% CAGR, propelled by AI training clusters that push rack loads beyond 40 kW. LiquidStack’s CDU-1 MW skid demonstrates the format’s 1,350 kW modular ceiling, a specification rapidly becoming a regional reference for giga-scale campuses. Edge suites in fintech, gaming, and smart-city command centers favor single-phase because of lower maintenance and spill-containment simplicity.

Fluid vendors respond with dual-certified chemistries that run in either phase regime, trimming SKUs and easing lifecycle management. Training programs coordinated by OEMs and integrators shrink skills gaps, helping smaller colocations weigh the twin factors of density and complexity. Over time, immersion cabinets are migrating toward hybrid cooling rails that allow operators to toggle between phase states as compute ratios evolve.

By Data Center Type: Hyperscale Builds Anchor Volume and Growth

Hyperscale operators owned 55% of segment revenue in 2024 and also drive the fastest expansion at 12.11% CAGR. The Middle East data center immersion cooling fluid market therefore skews toward large-lot sourcing, long-term supply contracts, and turnkey service agreements. Colocation suppliers adopt immersion to differentiate SLAs that guarantee rack densities above 30 kW without surcharges, while enterprise self-builds grow more gradually as IT budgets adjust to capex cycles. Edge and micro data centers represent just 4% of current fluid volume but enjoy triple-digit growth potential as 5G and IoT frameworks proliferate.

New campus layouts in Saudi economic zones now embed immersion tanks inside initial blueprints rather than retrofit pathways. This design-in approach locks fluid demand into 15-year purchase commitments, strengthening bargaining power for local blend houses expected to come online post-2026.

By End-User Industry: Healthcare Emerges as Standout Growth Story

Hospitals, diagnostic labs, and genomics institutes rely on AI-assisted imaging, molecular simulation, and EMR analytics that require constant high-density compute. Consequently, healthcare records the highest 11.1% CAGR through 2030. The NEOM Health City blueprint alone reserves 25 MW of immersion-cooled HPC by 2027. IT and ITES still contribute the largest 30% slice of 2024 fluid demand given the sheer volume of back-office and SaaS workloads, yet its growth moderates as the installed base matures.

BFSI workloads, especially low-latency trading engines, migrate to immersion because they benefit from stable chip junction temperatures that cut transaction jitter. Media, energy, and defense segments follow, each attracted by operational resilience in dusty, high-heat desert operating envelopes. Cross-sector AI rollouts ensure fluid demand remains diversified, mitigating exposure to any single vertical’s capital-spending cycle.

Geography Analysis

Saudi Arabia commands the largest share of the Middle East data center immersion cooling fluid market, underpinned by Vision 2030 fiscal incentives that rebate up to 40% of capital outlays for facilities achieving sub-1.3 PUE. DataVolt’s and STC’s expansions set local sourcing precMoreover, the establishment of a local Azure region removes perceived risk around enterprise adoption, unlocking financial services and government cloud demand within existing colocation facilities.edents for mineral oil and synthetic hydrocarbons, while emerging bio-ester alliances receive backing from the Ministry of Energy. The kingdom’s Global AI Hub Law also grants expedited permits to liquid-cooled projects, compressing build timelines and accelerating fluid uptake.

The UAE maintains momentum through G42’s multi-gigawatt AI campus and pervasive smart-city initiatives inside Dubai and Abu Dhabi. Time-of-use power tariffs and mandatory water-efficiency audits create natural alignment with immersion footprints. Moreover, the establishment of a local Azure region removes perceived risk around enterprise adoption, unlocking financial-services and government-cloud demand within existing colocation facilities.

Qatar targets standards harmonization with U.S. and EU regulatory baselines, which steers operators toward globally validated fluid chemistries and hardware. Kuwait and Bahrain tap into spill-over technical capacity and funding streams yet remain modest in absolute tonnage. Oman leverages its coastal fiber landings to pitch connectivity-rich campuses, pairing them with immersion gear to combat inland heat loads when halls sit farther from marine air currents. Turkey and Israel close the regional map with focused proof-of-concept sites; Vodafone’s USD 100 million Izmir build and the Timna mine conversion both rely on immersion to protect servers from abrasive dust and wide diurnal swings.

Competitive Landscape

Global chemical majors such as Shell, ExxonMobil, and Chemours collectively captured 32% of 2024 fluid liters, giving the market a moderate concentration. Their competitive edge lies in vertically integrated petrochemical supply, ISO-certified blending, and extensive R&D labs for additive packages. Yet disruptors like LiquidStack, Submer, and Green Revolution Cooling reshape the field through turnkey hardware-fluid ecosystems that promise lower total cost of ownership and faster commissioning.

Partnership models now dominate. Shell bundles certified fluids with Submer tanks; ExxonMobil signs fluid-supply plus performance-warranty accords with Stellium; Chemours pairs Opteon lines with LiquidStack’s two-phase CDU skids. White-space exists in recycling services: regional operators seek cradle-to-cradle programs that reclaim or re-refine spent fluids, curbing both cost and waste. Intellectual-property filings grew 40% year-on-year in 2024, signaling intensifying patent races around dielectric additives, nanofluid suspensions, and smart control algorithms.

Competitive differentiation increasingly resides in AI-driven telemetry that predicts fluid oxidative decay and orchestrates pump curves in real time. ZutaCore’s HyperCool platform, for instance, integrates machine-learning models that modulate flow rates and maintain chip-edge temperatures within ±1 °C even at 95% rack utilization. Facility owners value such predictive maintenance because unplanned downtime penalties have climbed as hyperscale SLAs tighten.

Middle East Data Center Immersion Cooling Fluid Industry Leaders

3M

The Dow Chemical Company

Exxon Mobil Corporation

Shell plc

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: ZutaCore and Munters partnered to integrate direct-on-chip liquid cooling for hyperscale halls across the GCC, combining HyperCool technology with Munters’ HVAC portfolio.

- November 2024: Stellium Data Centers joined with Submer and ExxonMobil to roll out immersion cooling across regional facilities, using ExxonMobil fluids under a long-term supply and service pact.

- November 2024: DeepCoolAI and Sanmina announced joint development of AI-optimized immersion packages for edge nodes.

- October 2024: Supermicro enlarged its DataVolt alliance to USD 20 billion, embedding immersion racks in Saudi AI campuses.

Middle East Data Center Immersion Cooling Fluid Market Report Scope

| Mineral Oil |

| Synthetic Hydrocarbon |

| Fluorocarbon-based Fluids |

| Bio-based Esters |

| Single-Phase |

| Two-Phase |

| Hyperscale / Cloud Service Providers |

| Colocation |

| On-Premise / Enterprise |

| Edge / Micro DC |

| IT / ITES |

| BFSI |

| Healthcare |

| Government and Defense |

| Media and Entertainment |

| Energy and Utilities |

| Other End Users |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| Turkey |

| Israel |

| Rest of Middle East |

| By Fluid Type | Mineral Oil |

| Synthetic Hydrocarbon | |

| Fluorocarbon-based Fluids | |

| Bio-based Esters | |

| By Phase Type | Single-Phase |

| Two-Phase | |

| By Data Center Type | Hyperscale / Cloud Service Providers |

| Colocation | |

| On-Premise / Enterprise | |

| Edge / Micro DC | |

| By End-User Industry | IT / ITES |

| BFSI | |

| Healthcare | |

| Government and Defense | |

| Media and Entertainment | |

| Energy and Utilities | |

| Other End Users | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Oman | |

| Turkey | |

| Israel | |

| Rest of Middle East |

Key Questions Answered in the Report

How large is the Middle East data center immersion cooling fluid market in 2025?

The market stands at USD 225.9 million in 2025 and is projected to grow to USD 363.6 million by 2030.

What CAGR is expected for immersion cooling fluids in the region?

A 9.95% CAGR is forecast from 2025 to 2030 as hyperscale campuses and AI workloads expand.

Which fluid type is growing fastest?

Bio-based esters record the highest 10.11% CAGR because they align with ESG and Shariah investment screens.

Why are two-phase systems gaining traction?

They can dissipate heat from racks exceeding 40 kW, a density common in AI training clusters.

Which country leads adoption?

Saudi Arabia leads, driven by Vision 2030 incentives, large hyperscale investments, and mandatory PUE thresholds below 1.3.

How does immersion cooling impact water consumption?

It eliminates evaporative losses, potentially saving up to 426 billion L of water annually across GCC data centers by 2030.

Page last updated on: