Data Center Immersion Cooling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

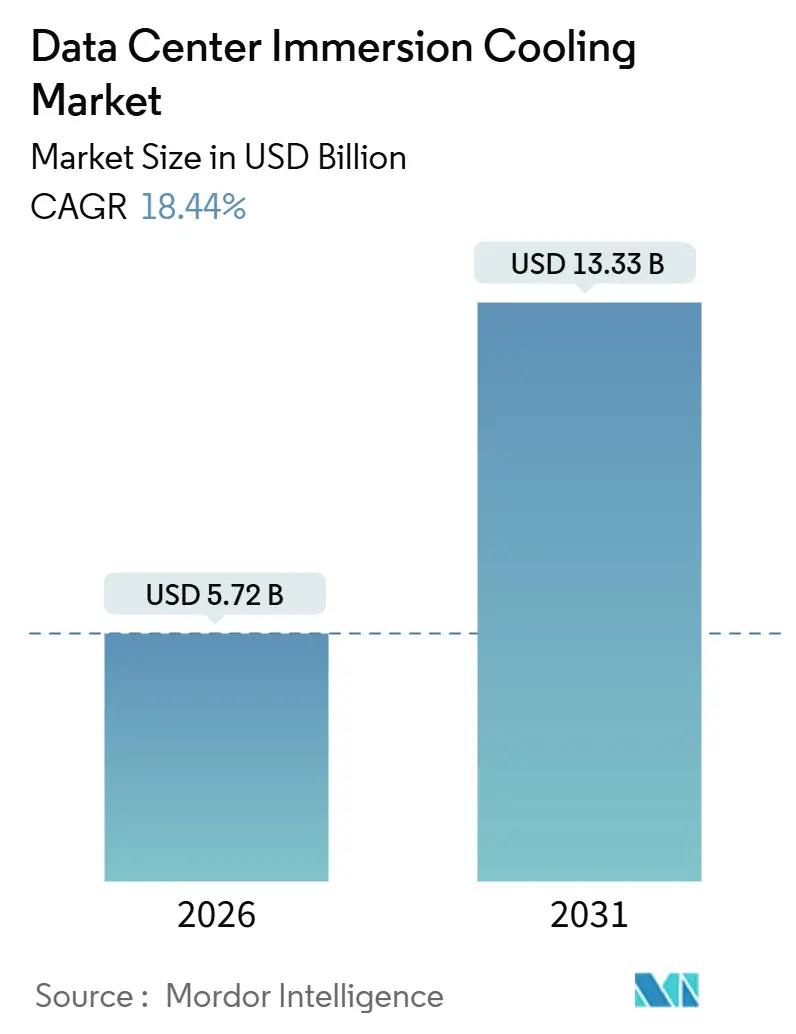

| Market Size (2026) | USD 5.72 Billion |

| Market Size (2031) | USD 13.33 Billion |

| Growth Rate (2026 - 2031) | 18.44% CAGR |

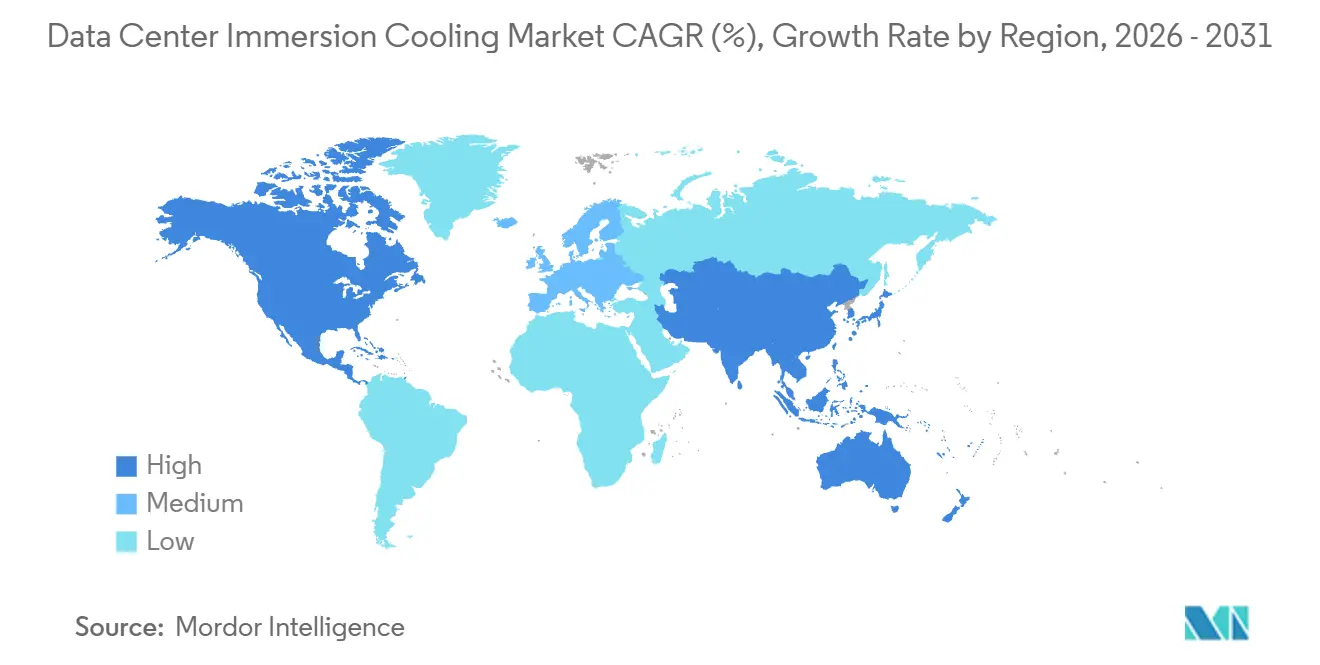

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

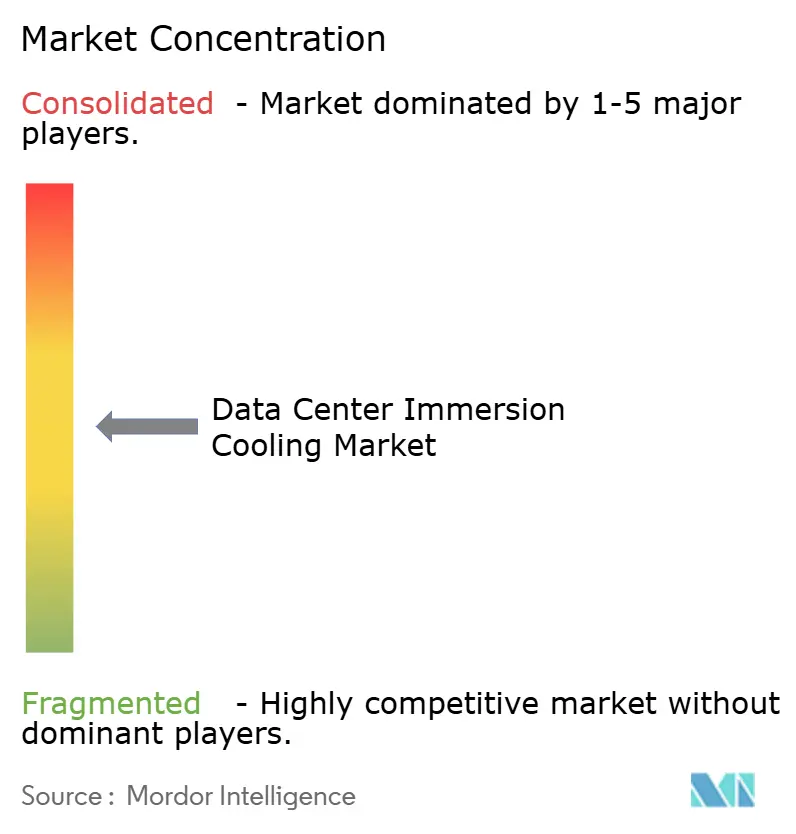

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Center Immersion Cooling Market Analysis by Mordor Intelligence

The Data Center Immersion Cooling Market size is estimated at USD 5.72 billion in 2026, and is expected to reach USD 13.33 billion by 2031, at a CAGR of 18.44% during the forecast period (2026-2031). Soaring rack power densities above 100 kilowatts, a rapid pivot to graphics accelerators, and tightening sustainability mandates have moved liquid thermal management from proof of concept to mainstream choice. Hyperscalers now deploy immersion systems to avoid the escalating fan energy of air cooling, while edge operators rely on liquid baths to fit inference-optimized hardware into small footprints. Mineral oil still dominates fluid demand because of cost, but bio-based and synthetic hydrocarbon alternatives are gaining traction under European PFAS restrictions. Capital costs remain two to three times higher than raised-floor air architectures, yet operators view the energy and waste-heat monetization upside as sufficient to clear investment hurdles.

Key Report Takeaways

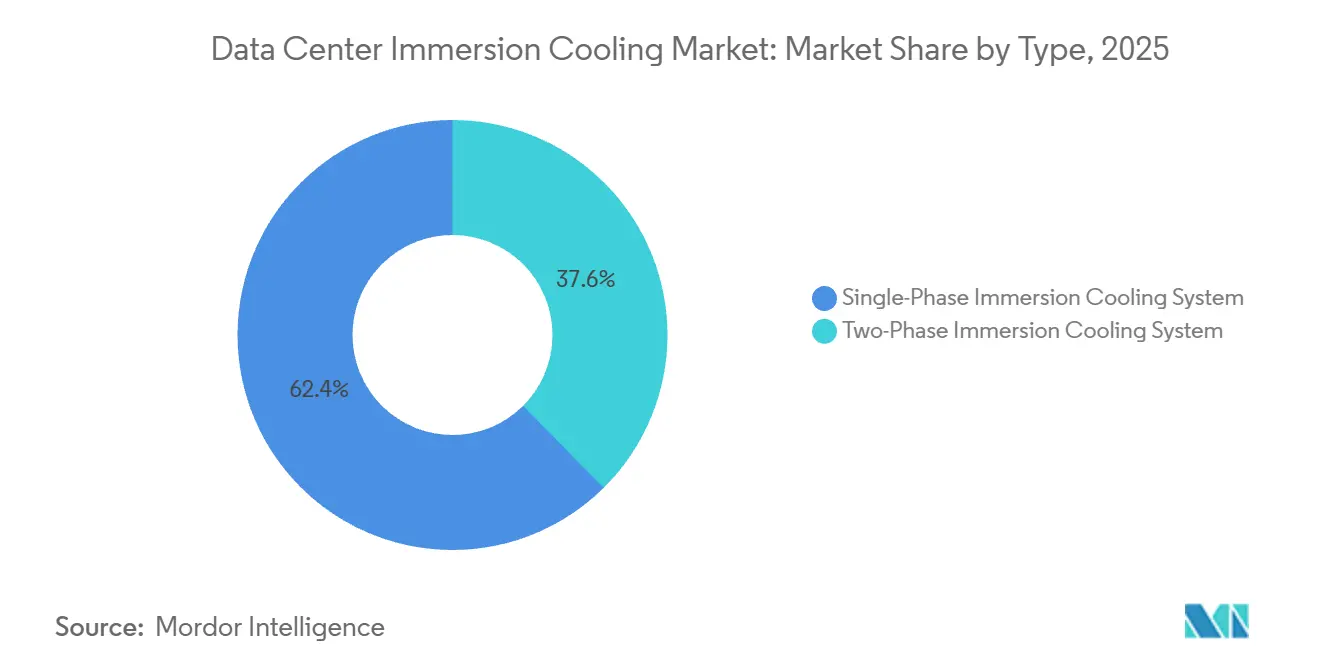

- By system type, single-phase technology held 62.43% share in 2025 while two-phase platforms are expected to grow at a 19.42% CAGR through 2031.

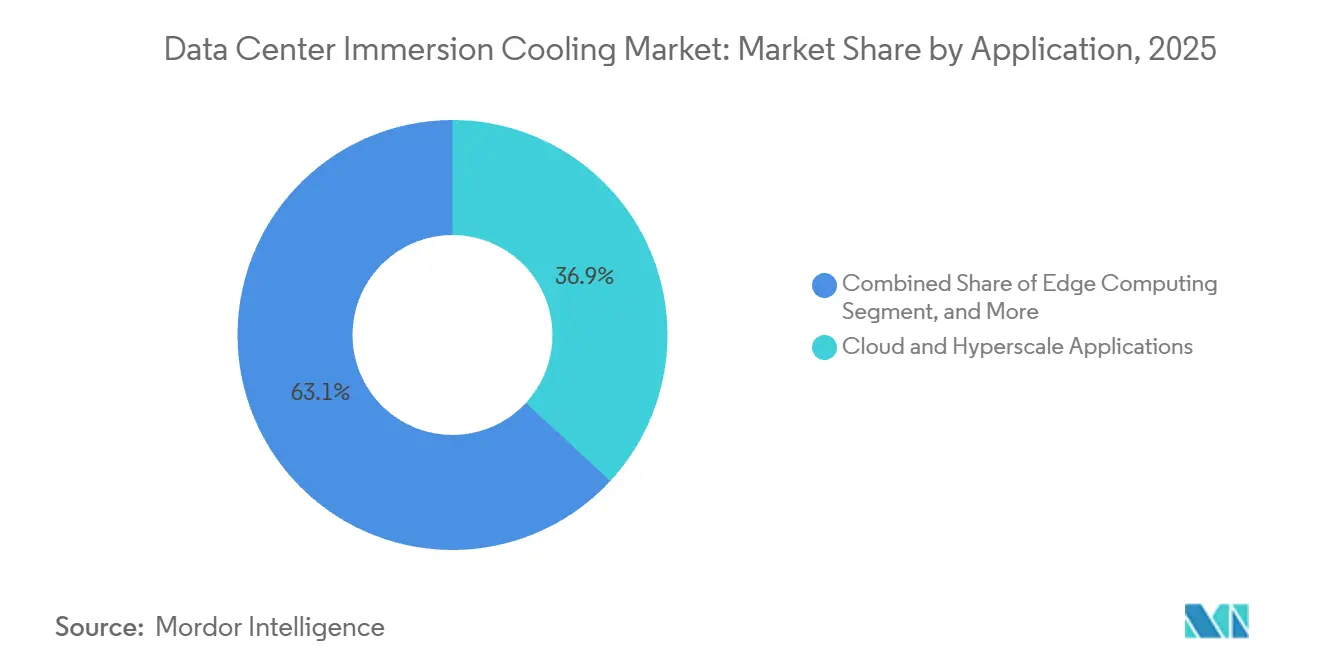

- By application, cloud and hyperscale deployments contributed 36.88% revenue in 2025, whereas artificial intelligence and machine learning workloads are slated to expand at 19.73% CAGR to 2031.

- By cooling fluid, mineral oil retained 48.65% share in 2025, yet bio-based alternatives are forecast to post a 19.56% CAGR through 2031.

- By tier classification, tier 3 installations captured 58.43% share in 2025; tier 4 centers are projected to register a 19.22% CAGR between 2026 and 2031.

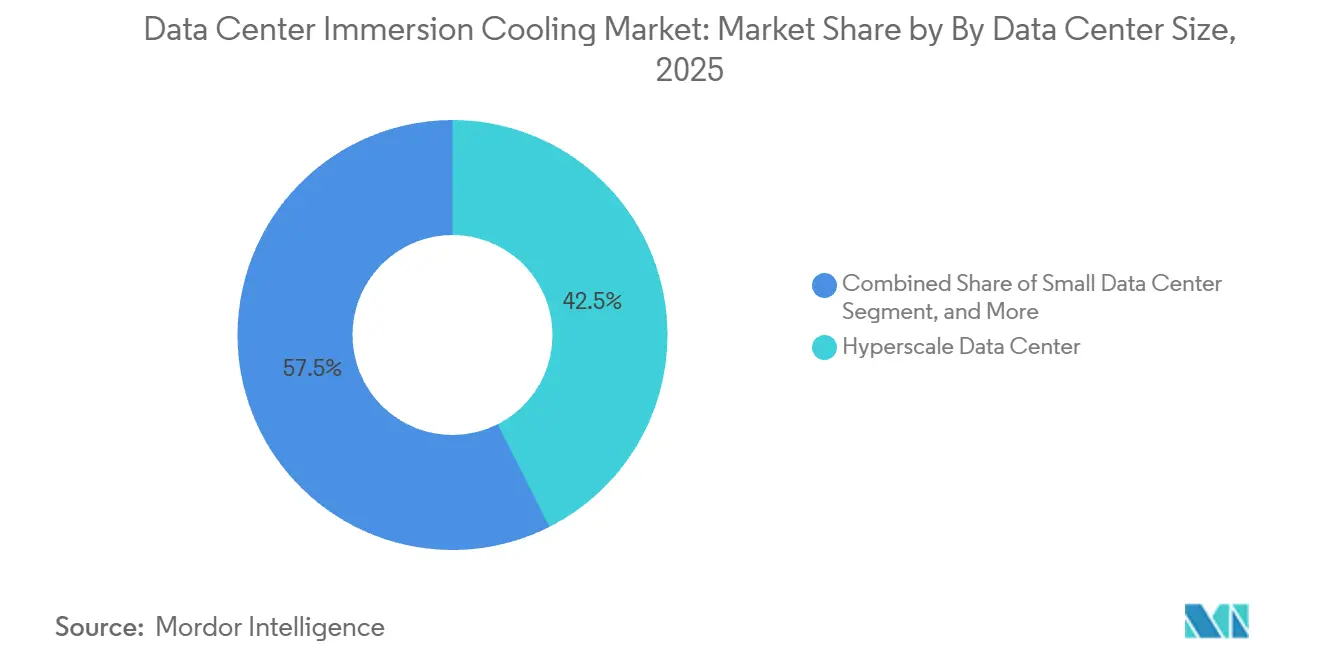

- By data-center size, hyperscale facilities accounted for 42.54% of capacity in 2025, while small sites are positioned for 19.39% CAGR on the back of edge computing rollouts.

- By data-center type, hyperscalers and cloud service providers secured 55.54% share in 2025; enterprise and edge locations are anticipated to grow at a 19.81% CAGR by 2031.

- By geography, North America dominated with 40.32% share in 2025, whereas Asia-Pacific is forecast to compound at 19.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Data Center Immersion Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Hyperscale Data Centers | +4.2% | Global with focus in North America, Asia-Pacific, and Western Europe | Medium term (2-4 years) |

| Rising Rack Power Densities From AI and ML Workloads | +5.1% | Global led by North America and Asia-Pacific GPU clusters | Short term (≤ 2 years) |

| Superior Energy-Efficiency and PUE Gains Over Air Cooling | +3.8% | Europe and North America driven by energy cost and carbon mandates | Medium term (2-4 years) |

| Regulatory Push Toward PFAS-Free Bio-Based Coolants | +2.3% | Europe and North America with spillover to Asia-Pacific | Long term (≥ 4 years) |

| Monetization of Waste Heat for District Heating Networks | +1.6% | Northern Europe with pilots in Germany, Denmark, and Sweden | Long term (≥ 4 years) |

| AI-Assisted Discovery of Next-Generation Dielectric Fluids | +1.4% | Global led by United States, Europe, and Japan consortia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Hyperscale Data Centers

Operators are consolidating compute into gigawatt-class campuses that can negotiate renewable power at scale and amortize large capital projects. Meta ran 21 such sites in 2025 averaging more than 100 megawatts each, and its filings credit immersion cooling for raising server density per floor tile. Microsoft lifted liquid penetration to 15% of its fleet during 2025 and targets 40% by 2028, citing a route to sub-1.15 power usage effectiveness in temperate zones.[1]Microsoft Corporation, “Azure Infrastructure Update,” microsoft.com Google began retrofitting eight legacy halls to house Tensor Processing Unit clusters that top 350 watts per chip. With each build exceeding USD 500 million, shifting to immersion lowers land, mechanical, and fan energy per compute unit.

Rising Rack Power Densities From AI and ML Workloads

Large language model training now fills racks that draw 80-120 kilowatts. NVIDIA’s H100 hits 700 watts per device, so eight dual-GPU servers inside a 42U cabinet breach 100 kilowatts.[2]NVIDIA Corporation, “Fiscal 2025 Form 10-K,” nvidia.com Intel’s Gaudi 3 accelerator checks in at 600 watts, and customer clusters above 1,000 chips specify immersion to avoid expanding chilled-water loops. AMD’s MI300X peaks at 750 watts, with total cost of ownership modeling showing 20%-30% savings over five years once rack densities cross 60 kilowatts. Air’s low heat capacity cannot cost-effectively move that load, whereas liquid’s 25-times-higher thermal conductivity preserves performance margins and delays building expansions.

Superior Energy-Efficiency and PUE Gains Over Air Cooling

Eliminating computer-room air handlers pares auxiliary loads and lets facilities post power usage effectiveness below 1.10. Green Revolution Cooling logged a 1.03 figure at a Texas cryptocurrency mine in 2025. Submer achieved 1.05 at a European supercomputing site while selling 65 °C return water to a municipal network, generating EUR 120 000 (USD 135 000) revenue. Uptime Institute surveys place the liquid median at 1.12 against 1.32 for air, underscoring cost and carbon advantages. With data centers already consuming 1.5% of the world's power, immersion offers a path to sustain AI growth without proportional energy escalation.

Regulatory Push Toward PFAS-Free Bio-Based Coolants

European Union Regulation 2024/573 curbs fluorinated compounds, steering operators toward mineral oil, synthetic hydrocarbons, and bio-derived esters. 3M will retire its Novec line by 2028. Cargill’s NatureCool, sourced from soybean and rapeseed oil, secured contracts topping 2 million liters in 2025. Shell introduced a synthetic hydrocarbon fluid with 90% biodegradation in 28 days, meeting IEC dielectric benchmarks while sidestepping PFAS scrutiny. Regulation thus acts as a tailwind for new chemistries that balance performance with green credentials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX and Facility-Redesign Costs | -3.1% | Global, most acute for colocation and enterprise sites | Short term (≤ 2 years) |

| Fragmented Standards and Vendor Interoperability Gaps | -1.8% | Global with regional certification differences | Medium term (2-4 years) |

| Supply-Chain Risk for Fluorinated Dielectrics | -1.2% | North America and Europe where PFAS rules tighten supply | Medium term (2-4 years) |

| Limited Field Data on Long-Term Fluid Hardware Compatibility | -0.9% | Global, affecting risk-averse finance and public sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Facility-Redesign Costs

Immersion tanks, manifold plumbing, and structural reinforcements push turnkey expense for a 1 megawatt block to USD 2.5-3.5 million, roughly double air cooling levels.[3] Vertiv Holdings, “Form 10-K 2025,” vertiv.com Retrofit projects add 15%-25% due to floor strengthening, Class K suppression upgrades, and staff retraining. Payback stretches four to six years unless local power prices exceed USD 0.10 per kilowatt-hour or heat-offtake deals materialize. Colocation operators running thin margins hesitate, while smaller enterprises lack balance-sheet capacity, slowing broad uptake.

Fragmented Standards and Vendor Interoperability Gaps

IEC 61000-4-2 ignores submerged electronics, and UL 2755 certification remains optional with only eight vendors listed by 2025. Dell tests PowerEdge servers against four specific fluids, limiting buyer flexibility. Non-standard tank geometries and sensor protocols tie customers to single suppliers, curbing competitive bidding and elongating procurement cycles. Work on IEC 60364-7-729 started in 2025 and could harmonize safety rules by 2027, but until then interoperability challenges remain a drag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Two-Phase Platforms Target Ultra-Dense AI Clusters

Two-phase architectures will outgrow the wider data center immersion cooling market at 19.42% CAGR between 2026 and 2031. In 2025 single-phase systems still commanded a 62.43% data center immersion cooling market share thanks to compatibility with commodity servers and minimal fluid volatility. LiquidStack documented a European AI lab that removed pumps altogether by exploiting latent heat, cutting auxiliary loads 40%. Single-phase remains preferred for cryptocurrency and general HPC workloads, yet operators chasing 100 kilowatt racks view two-phase as the only route to passive rejection at scale.

Pumpless operation lowers total energy draw, and gravity-fed condensate return simplifies maintenance. However, reliance on hydrofluoroether fluids keeps costs high and exposes buyers to PFAS restrictions. Manufacturers are racing to qualify synthetic hydrocarbon and low-GWP chemistries, suggesting the two-phase premium will narrow over the forecast horizon. Interoperability efforts may also make mixed-phase deployments practical inside a single hall, giving operators a menu of thermal tools.

By Cooling Fluid: Bio-Based Esters Challenge Mineral Oil

Mineral oil supplied 48.65% of liters in 2025 because of USD 3-5 per liter pricing and mature supply chains. Yet bio-based options are set for a 19.56% CAGR as operators in Europe and North America look to decarbonize. Cargill’s ester delivers 0.17 W-m-K conductivity, 85% of oil levels, but satisfies ISO 14001 and Scope 3 accounting. Fluorocarbon fluids still enable two-phase cycles and held 22% share, though 3M’s exit and Chemours’ reformulation underscore supply and compliance risk.

Shell’s synthetic hydrocarbon variant blended 0.16 W-m-K performance with a 265 °C flash point, removing the need for extensive fire suppression. De-ionized water, while not a full-immersion medium, earned 8% share inside direct-to-chip loops at hyperscalers. Going forward, fluid choice will hinge on local regulation, waste-heat goals, and insurer preferences, with operators likely to diversify chemistry portfolios to hedge risk.

By Application: AI and ML Drive New Procurement Priorities

Artificial intelligence and machine learning workloads are on track for a 19.73% CAGR to 2031, the fastest of any segment. Cloud and hyperscale halls delivered 36.88% of 2025 revenue, but their internal mix is shifting from general compute to inference engines. High-performance computing held 18%, backed by academic and weather agencies that pack petaflops into fixed real estate. Edge deployments claimed 12%, relying on small immersion modules to meet sub-20 millisecond latency budgets.

NVIDIA’s DGX H100 nodes draw 10.2 kilowatts each, prompting 256-node clusters to default to baths. Cryptocurrency mining slid to 9% share after policy scrutiny, freeing capacity for enterprise AI pilot clusters. As inference runs proliferate inside factories, hospitals, and distribution centers, immersion’s compactness and noise reduction will resonate beyond hyperscale campuses.

By Tier Type: Tier 4 Facilities Adopt Redundant Liquid Loops

Tier 4 sites will expand at 19.22% CAGR through 2031 as finance, healthcare, and government workloads demand 99.995% availability. Tier 3 remains the workhorse with 58.43% of 2025 installations, striking a balance between uptime and cost. Schneider Electric reports that Tier 4 buyers specify dual fluid circuits and independent reservoirs to permit maintenance without downtime. The Uptime Institute Tier rubric lacks liquid-specific language, but upcoming IEC rules and OEM reference designs should ease certification.

Tier 1 and Tier 2 footprints are smaller, often serving batch compute or content delivery tasks where occasional thermal throttling is tolerable. As vendors roll out pre-certified immersion bundles, mid-tier operators may climb the reliability ladder without prohibitive engineering studies.

By Data Center Size: Small Sites Lead Edge Expansion

Hyperscale campuses held the largest slice at 42.54% of capacity in 2025 and will continue to dominate absolute megawatts. Yet small data centers below 1 megawatt are forecast for 19.39% CAGR, mirroring edge compute trends in retail, telecom, and smart-manufacturing. Asperitas supplied 24-server immersion blocks for a European telco, delivering 15 millisecond inventory-analytics latency inside city storefronts.

Medium 1-10 megawatt facilities posted 28% share, often modular expansions by colocation landlords. Large 10-50 megawatt halls, at 18%, remain specialty builds for HPC and AI training. As 5G densifies and autonomous fleets mature, containerized immersion systems capable of rooftop or parking-lot placement will move more compute closer to users.

By Data Center Type: Enterprise and Edge Operators Accelerate Adoption

Hyperscalers and cloud providers owned 55.54% share in 2025 and continue to bulk order immersion-ready racks. Colocation businesses landed 22%, bundling liquid bays as a premium SKU to GPU tenants. Enterprise and edge deployments, though smaller today, are primed for 19.81% CAGR. Wiwynn observed liquid-ready chassis shipments jump to 18% of volume in 2025, a three-fold leap in two years.

Turnkey managed services, where vendors deliver tanks, fluid, and upkeep for a subscription fee, are emerging to soothe warranty and skills anxiety. Midas Green Technologies and DCX are piloting cooling-as-a-service contracts that shift capex to opex, helping mid-market firms adopt immersion without balance-sheet strain.

Geography Analysis

North America retained a 40.32% share in 2025 on the strength of hyperscale spend in Virginia, Oregon, and Texas. Microsoft earmarked USD 10 billion for U.S. liquid builds through 2028, citing temperate climates that allow direct air economization on the dry side. Meta’s Prineville campus operated 15 000 submerged servers and posted a 1.06 annual power usage effectiveness, among the best globally. Canada gathered 8% of regional megawatts thanks to hydroelectric power in Quebec and British Columbia, while Mexico captured 4% serving nearshore manufacturing nodes.

Asia-Pacific is projected to grow at a 19.94% CAGR to 2031, led by China’s sovereign AI push and India’s incentive scheme worth USD 2 billion.[4]India Ministry of Electronics and Information Technology, “Data Center Incentive Program,” meity.gov.in Alibaba and Tencent already run immersion halls in Hangzhou and Shenzhen, each claiming cooling energy cuts above 30%. Japan contributed 18% of regional revenue in 2025, supported by subsidies under the Green Transformation program. South Korea, Australia, and New Zealand share the remainder, each targeting low-latency service for local consumption.

Europe controlled 28% of the global tally in 2025, propelled by efficiency mandates and heat-recovery incentives. Germany’s EUR 500 million grant package for district heating tapped operators in Frankfurt and Munich, while the Netherlands leveraged renewable grids near Amsterdam. The United Kingdom added liquid rooms in London Docklands and Manchester to meet a 1.3 power usage effectiveness threshold. Middle East builds, though only 6% of world capacity, highlight immersion’s thermal edge in 45 °C deserts, exemplified by a 150 megawatt Abu Dhabi project set to complete in late 2026. South America sits at 3%, dominated by Brazil’s finance sector, and Africa at 2%, held back by grid stability.

Regulatory Landscape

In Europe, data center sustainability reporting requirements have tightened, shaping procurement toward measurable energy and resource performance. EU Delegated Regulation 2024/1364 requires operators to report indicators such as energy efficiency, water use, and waste-heat reuse via national schemes or the European database starting September 15, 2024, with annual submissions due by May 15. At the same time, scrutiny of fluorinated chemistries is influencing fluid selection in immersion systems, reinforcing the shift away from PFAS-adjacent dielectric options toward mineral oil, synthetic hydrocarbons, and bio-based esters.

Standards and policy initiatives are also reducing uncertainty around liquid-cooled facility design. The Telecommunications Industry Association published TIA-942-C with an annex addressing liquid immersion cooling and alignment to ASHRAE thermal guidance for high-density environments, supporting more consistent engineering and audit practices across regions. In the United States, the Liquid Cooling for AI Act of 2025 (H.R. 5332) signals federal attention to efficiency standards for AI-supporting data centers, while California AB-2619 (2025-2026 session) directs state agencies to develop data center water-use efficiency guidelines by January 1, 2029, elevating water metrics alongside energy performance in site approvals and operating disclosures.

Competitive Landscape

Specialist suppliers Green Revolution Cooling, Submer, LiquidStack, and Asperitas collectively held around 35% of tank shipments in 2025. They benefited from early GPU mining work that proved single-phase reliability at scale. Diversified infrastructure majors Schneider Electric, Vertiv, and Dell expanded into immersion via acquisition and partnerships, offering single-vendor accountability that appeals to enterprise buyers. Patent activity jumped 40% in 2025 as Shell, 3M, Cargill, and Chemours filed for PFAS-free fluids with dielectric strength over 40 kilovolts per millimeter.

Hardware alliances tightened, with NVIDIA, AMD, and Intel publishing reference rack designs co-branded with cooling vendors to accelerate cluster deployment. Hyperscalers negotiated exclusive fluid contracts to secure supply amid competition from electric-vehicle battery plants. Edge computing presents white space, and newcomers like Midas Green Technologies promote subscription cooling-as-a-service to bring liquid economics to sub-100-kilowatt sites. Standardization work at IEC Technical Committee 64 aims to unlock multi-vendor ecosystems by 2027, which could soften today’s lock-in and sharpen price competition.

The Open Compute Project ratified its first immersion cooling facility guideline in late-2025, providing reference tank geometries, sensor buses, and maintenance procedures that any vendor can adopt, and more than 20 suppliers pledged compliance within six months. The specification is expected to cut qualification cycles by 30% for enterprise buyers and may compress margins for incumbents as component-level competition intensifies. Fluid producers are also moving up the stack, with Shell and Cargill launching integrated monitoring software that tracks thermal performance and degradation, positioning themselves as end-to-end service providers rather than commodity suppliers. As vertical integration accelerates, pricing visibility is improving, which should encourage mid-tier colocation operators that previously hesitated over opaque total-cost-of-ownership models.

Data Center Immersion Cooling Industry Leaders

Fujitsu Limited

Green Revolution Cooling (GRC) Inc.

Submer Technologies SL

LiquidStack Inc.

Asperitas

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Standardization and interoperability work is creating whitespace for multi-vendor ecosystems and faster qualification of immersion deployments across hyperscale and enterprise buyers. The Open Compute Project published an immersion cooling facility guideline in late 2025, and in April 2026 ISO/IEC formally approved a new project (ISO/IEC AWI TS 22237-44) to guide application of liquid cooling in data centers. These efforts reduce the practical lock-in associated with proprietary tank geometries, monitoring protocols, and optional certification pathways, and they widen the opportunity for component suppliers (tanks, sensors, CDUs, manifolds, fluids, and monitoring software) to compete within more common design envelopes.

Scale-up and regional build programs are also expanding the addressable footprint beyond early-adopter GPU clusters. Vertiv announced about USD 50 million to expand manufacturing in Ohio to increase capacity for liquid cooling and chilled water systems by about 45% by Q2 2027, and Furukawa Electric disclosed JPY 55 billion to expand production capacity for water-cooling modules and heat sinks across the Philippines, Thailand, and China. On the demand side, immersion adoption is moving into new geographies where policy and infrastructure constraints are shaping site selection, including Asia-Pacific initiatives such as Indias data center incentive scheme (USD 2 billion) and Japan support under the Green Transformation program, while European operators are pairing liquid systems with heat-recovery monetization pilots already cited in the report (for example, Submer heat sales to municipal networks).

Recent Industry Developments

- July 2026: Submer announced a EUR 1 billion investment to build a sustainable AI data center at the former Ercros chemical plant in Flix, Catalonia, under its Rubix Data Centers division. The project elevates an immersion-cooling specialist into a full-stack infrastructure owner-operator, tightening the link between cooling technology choices and site-level economics. It also adds a high-visibility European reference for liquid-cooled, AI-ready capacity that can influence colocation and sovereign AI procurement.

- February 2026: Trane Technologies entered into a definitive agreement to acquire LiquidStack. The transaction accelerates consolidation as large HVAC and thermal-management groups absorb specialized immersion capabilities to broaden their AI data center portfolios. Integration with a scaled global service organization can reduce buyer concerns around warranties, spares, and lifecycle support for immersion deployments.

- June 2025: Green Revolution Cooling (GRC) secured investment from Samsung Ventures and formed a strategic partnership with Samsung C&T. The partnership supports faster commercialization and broader project delivery reach, combining immersion-cooling specialization with a major construction and engineering channel. It also signals increasing strategic interest from large industrial players in immersion platforms for high-density compute rollouts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers immersion cooling used inside data centers, where IT hardware is cooled by being placed in a dielectric liquid. We track spend across the systems, the dielectric fluids, and the supporting services used for installation and ongoing operation.

Scope exclusions: We exclude conventional air cooling and non-immersion liquid cooling approaches that do not submerge the hardware in dielectric fluid.

Segmentation Overview

- By Type

- Single-Phase Immersion Cooling System

- Two-Phase Immersion Cooling System

- By Cooling Fluid

- Mineral Oil

- De-Ionized Water

- Fluorocarbon-Based Fluids

- Synthetic Hydrocarbon Fluids

- Bio-Based Fluids

- By Application

- High-Performance Computing (HPC)

- Edge Computing

- Artificial Intelligence and Machine Learning

- Cloud and Hyperscale Applications

- Cryptocurrency Mining

- Other Applications

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Size

- Small Data Center

- Medium Data Center

- Large Data Center

- Hyperscale Data Center

- By Data Center Type

- Colocation Data Center

- Hyperscalers Data Center/CSPs

- Enterprise and Edge Data Center

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping what drives immersion adoption in data centers and which indicators can be tracked consistently across countries. We rely on public sources such as U.S. DOE materials on data center energy use, U.S. EPA ENERGY STAR guidance, IEA data on electricity demand trends, and ITU publications on digital infrastructure to keep assumptions grounded.

To translate those signals into a market model, we also review filings and investor presentations of relevant suppliers and data center operators, along with standards and best practice material from groups such as ASHRAE and public technical papers in IEEE and similar journals. Where helpful, patent databases and paid subscriptions for company financials and for news and financials are used to confirm product direction, pricing ranges, and timing of major deployments. These examples are not exhaustive, and many other public sources were also referenced for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focuses on reality checks that are hard to get from public data, such as typical rack density thresholds that trigger immersion, the mix between single-phase and two-phase deployments, and what buyers include in project budgets (fluids, tanks, heat exchangers, monitoring, and services). We speak with a spread of technology providers, fluid ecosystem participants, integrators, and data center stakeholders across major regions so that assumptions on adoption pace, price movement, and retrofit versus new build splits can be corrected before finalizing results.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 16% | APAC: 43% |

| Mid tier: 45% | Functional/Unit leaders: 28% | EMEA: 32% |

| Smaller Players: 19% | Managers: 56% | Americas: 25% |

Market-Sizing & Forecasting

For sizing, the main build uses a top-down approach where the addressable demand pool is reconstructed from data center capacity growth and workload intensity. We then filter that pool by the share of deployments that can realistically shift to immersion given power density and heat removal needs. Results are cross-checked with selective bottom-up approximations such as sampled project volumes times typical system and fluid pricing, plus channel checks on the timing of larger rollouts.

Inputs used in the model include trends in AI and HPC deployments, rack power density ranges, new build versus retrofit activity, dielectric fluid pricing direction, and the availability of heat reuse infrastructure where it changes the economics. Forecasting is anchored through scenario analysis, since adoption is sensitive to capex cycles and local energy costs. Those scenarios are tuned using the consensus ranges gathered from interviews. When bottom-up signals are missing in smaller countries, we fill gaps using proxy indicators like data center pipeline announcements and power capacity additions, and then normalize back to regional totals.

Data Validation & Update Cycle

Validation happens in layers so that one weak input does not drive the final number. We compare model outputs against independent signals such as announced data center capacity additions, typical deployment lead times, and observed shifts in cooling technology preferences, then review outliers before sign-off.

If a major variance shows up, we re-check units, currency timing, and adoption rates. We also re-contact select interviewees to confirm whether the change is real or a reporting artifact. The report is refreshed annually, and interim updates are made when there are material events like a step-change in GPU roadmaps, fluid supply constraints, or sudden changes in power pricing. Right before delivery, an analyst does a fresh review pass so clients receive the most current view available.

Mordor Intelligence's Data Centers Immersion Cooling Market Size Compared Against Other Published Estimates

Published market sizes for immersion cooling in data centers often look far apart because the same words are used for different scopes and different spend lines. The biggest differences typically come from what gets counted as the market, which year is treated as the starting point, and whether the model is tied to data center capacity signals or mainly to vendor shipment assumptions.

The main gap comes from whether the estimate counts only data center immersion deployments (systems plus dielectric fluids tied to real installation activity) or if it mixes in broader immersion use cases, which is why Mordor Intelligence reports USD 5.72 B (2026) at a much larger scale than narrower solution-only views. Differences also show up when studies assume aggressive adoption across all facility types, or when pricing is held flat even though early projects can be costlier and later projects tend to standardize. Currency conversion timing and refresh cadence add more spread, especially when energy costs and AI-related demand move quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.72 B (2026) | |

| Global Consultancy A | USD 0.35 B (2025) | Uses a smaller starting year and a tighter definition that reads like solution revenue only, which can undercount fluids and supporting hardware and can miss multi-year build-outs tied to data center capacity additions. |

| Industry Publisher B | USD 0.29 B (2025) | Keeps the scope closer to near-term deployments and does not clearly show how adoption is linked to rack density triggers, so the model can stay anchored to early-stage penetration rather than scaling with AI and HPC expansion. |

The comparison shows that most of the spread is created by scope and by what spending lines are included, rather than by math alone. By keeping assumptions traceable to data center expansion and power density triggers, and then validating with practical pricing and adoption feedback, the final number remains repeatable and easier to explain on a single set of drivers.

Key Questions Answered in the Report

What value is data center immersion cooling expected to reach by 2031?

USD 13.33 billion, reflecting robust uptake in AI, edge, and hyperscale sites

Which cooling architecture is expanding fastest?

Two-phase immersion systems, projected to rise at a 19.42% CAGR between 2026 and 2031

What share did mineral oil hold among coolants in 2025?

48.65% of deployed fluid volume, though its dominance is fading under PFAS restrictions

How do operators justify higher capex for immersion cooling?

Energy savings, sub-1.10 power usage effectiveness, and waste-heat revenue shorten payback to four to six years in high-cost power markets

Which region shows the highest growth momentum?

Asia-Pacific, with a forecast 19.94% CAGR on the back of sovereign AI investments in China, India, and Japan

What new standard supports multi-vendor interoperability?

The Open Compute Project immersion guideline published in 2025, which defines common tank, monitoring, and safety specifications

Page last updated on: