Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

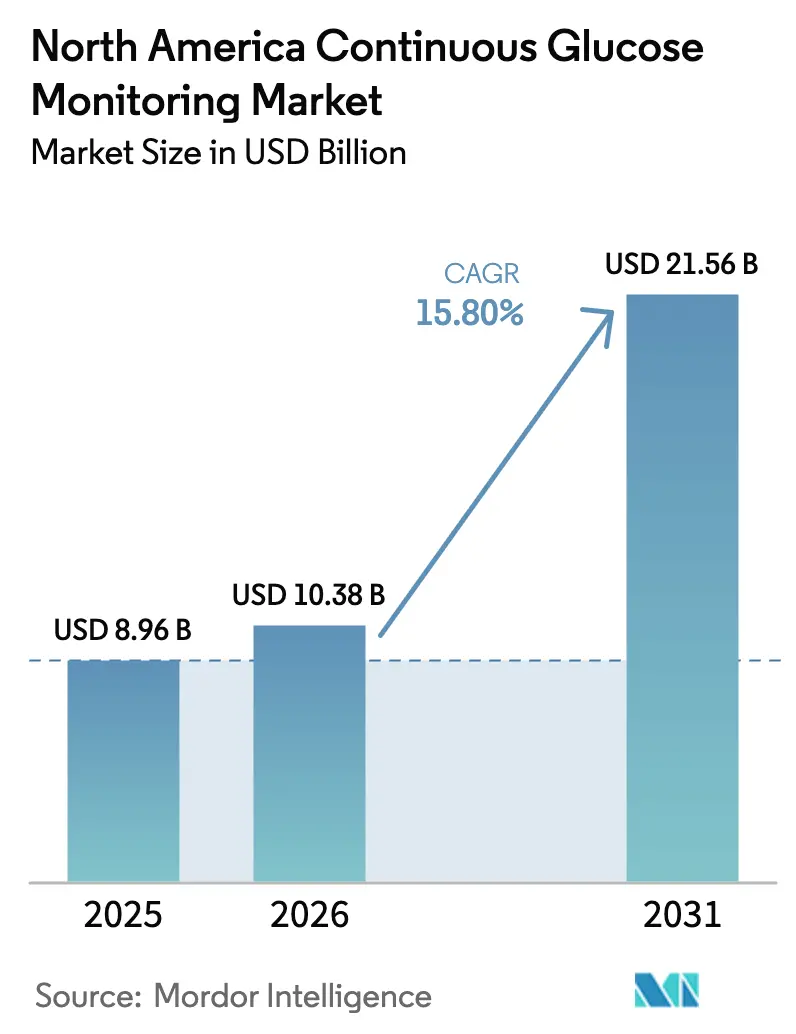

| Base Year Market Size (2025) | USD 8.96 Billion |

| Market Size (2026) | USD 10.38 Billion |

| Market Size (2031) | USD 21.56 Billion |

| Growth Rate (2026 - 2031) | 15.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Continuous Glucose Monitoring Market Analysis by Mordor Intelligence

The North America continuous glucose monitoring market size is expected to grow from USD 8.96 billion in 2025 to USD 10.38 billion in 2026 and is forecast to reach USD 21.56 billion by 2031 at 15.80% CAGR over 2026-2031. This acceleration reflects a structural shift from episodic finger-stick testing to continuous, real-time data that feeds automated insulin delivery, remote care, and population-scale disease-management programs. Regulatory approvals that drop the minimum age for use to 2 years, payer policies that waive prior authorization for non-insulin-using adults, and the rapid integration of CGM into closed-loop systems jointly sustain expansion. Sensor miniaturization now delivers ≤8% mean absolute relative difference (MARD), approaching laboratory precision. Parallel growth in remote-monitoring CPT codes allows clinicians to bill USD 64 per patient each month for asynchronous CGM review, cementing reimbursement momentum.

Key Report Takeaways

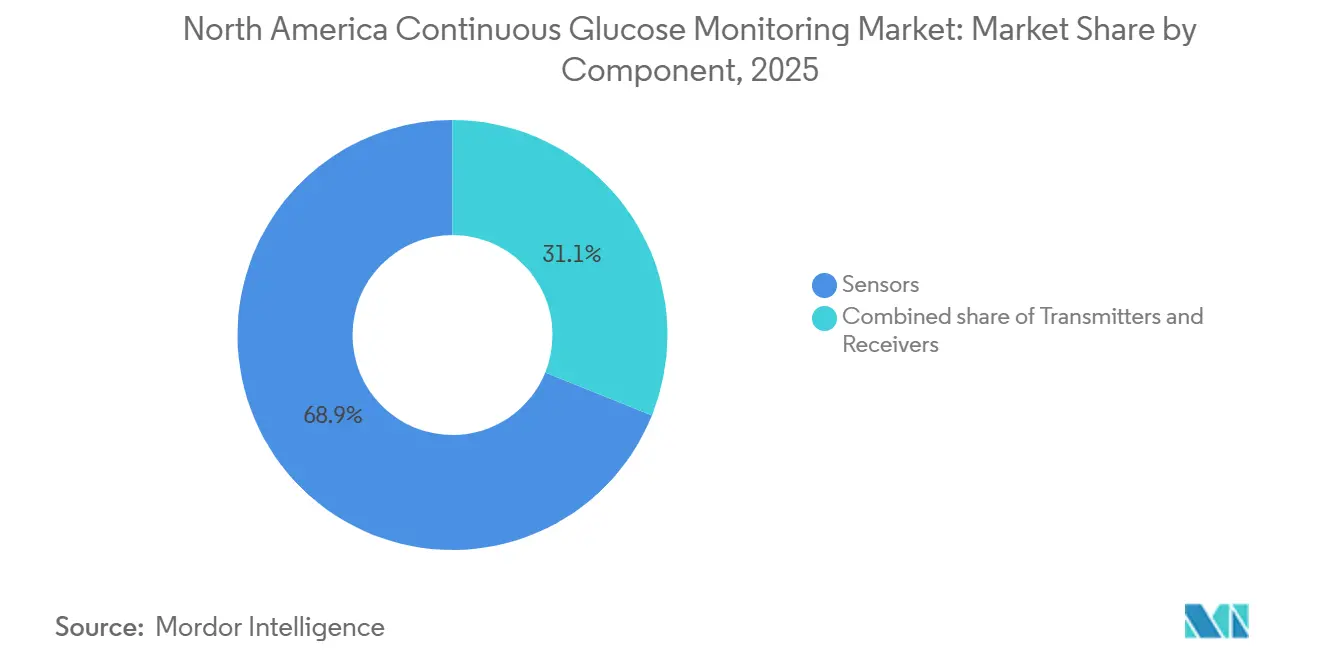

- By component, sensors captured 68.9% of the North America continuous glucose monitoring market share in 2025, while their 16.87% CAGR is the highest among components.

- By demography, adults held 71.2% revenue share in 2025; the pediatric segment is projected to grow at 18.92% CAGR through 2031.

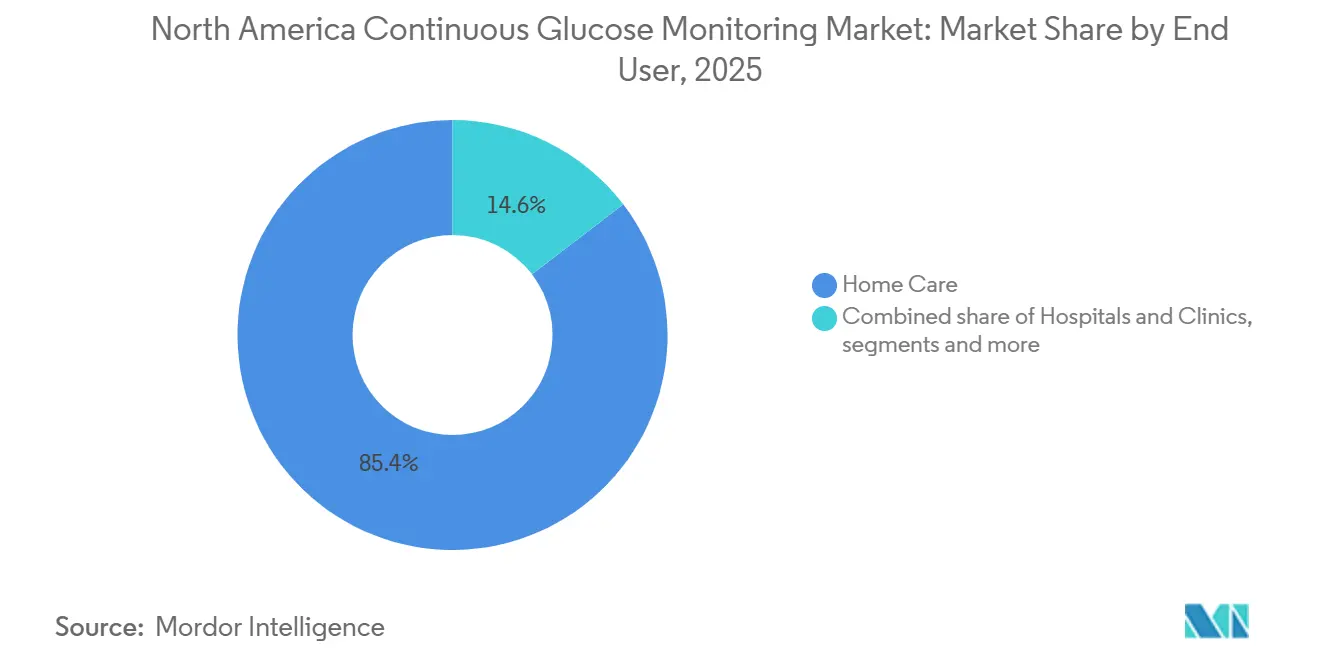

- By end user, home care accounted for 85.4% revenue in 2025 and is set to advance at a 17.87% CAGR to 2031.

- By country, the United States commanded an 88.5% share in 2025, whereas Canada leads growth at a 16.43% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Continuous Glucose Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Diabetes & Earlier Diagnosis | +2.8% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Rapid Uptake of Remote Monitoring & Tele-Health Integration | +3.2% | United States, Canada | Medium term (2-4 years) |

| Sensor Miniaturization & Accuracy Breakthroughs | +2.5% | United States, Canada | Medium term (2-4 years) |

| Employer-Sponsored Wellness Plans Subsidising CGM | +1.4% | United States | Short term (≤ 2 years) |

| Pharmacy-Chain Subscription Programs Accelerating First-Time Users | +1.6% | United States | Short term (≤ 2 years) |

| Integration with Automated Insulin Delivery Systems | +2.9% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Of Diabetes & Earlier Diagnosis

Diabetes prevalence reached 38.4 million in the United States in 2024, 3.7 million in Canada in 2025, and 12.4 million in Mexico in 2025. Screening guidelines now recommend testing all adults aged 35+ and overweight adults with a risk factor, expanding the addressable base by roughly 15 million individuals[1]Centers for Disease Control and Prevention, “National Diabetes Statistics Report,” CDC, cdc.gov. Newly diagnosed adults receive CGM within 90 days because randomized evidence shows a 0.9% additional A1c reduction versus finger-stick monitoring. Commercial insurers mirrored the science by adding first-line CGM coverage for non-insulin users in 2025[2]American Diabetes Association, “Standards of Care in Diabetes—2025,” Diabetes Care, diabetes.org. The result is a durable, long-tail driver across the North American continuous glucose monitoring market.

Rapid Uptake of Remote Monitoring & Telehealth Integration

CPT codes 99453, 99454, and 99457 reimburse remote physiologic data review, creating a recurring USD 64 monthly revenue stream per CGM patient. The Veterans Health Administration cut in-person endocrinology visits 38% after systemwide CGM-telehealth rollout in 2025 while sustaining glycemic outcomes. Kaiser Permanente’s virtual clinic documented a 1.2% mean A1c drop among 4,800 enrollees by pairing CGM with asynchronous coaching. FDA guidance clarified that cloud-connected CGM platforms qualify for RPM billing, ending payer ambiguity [3]U.S. Food and Drug Administration, “Real-Time Continuous Glucose Monitoring Systems Guidance,” fda.gov. These forces intertwine reimbursement and telehealth growth, lifting the North American continuous glucose monitoring market.

Sensor Miniaturization & Accuracy Breakthroughs

Abbott’s FreeStyle Libre 3 shrank sensor volume 70% and achieved 7.9% MARD. Dexcom’s G7 cut warm-up to 30 minutes and landed at 8.2% MARD. Senseonics’ Eversense 365 delivers 365-day wear and removes adhesive dermatitis risk for the estimated 10% of users with skin reactions. FDA draft guidance suggests CGM with <10% MARD may support insulin dosing without confirmatory finger sticks, unlocking an 8.4 million-strong type 1 population. Accuracy gains, therefore, amplify both clinical utility and payer acceptance.

Integration With Automated Insulin Delivery Systems

Tandem’s Control-IQ held a significant U.S. automated-delivery share in 2025, operating exclusively on Dexcom CGM inputs. Insulet shipped 1.2 million Omnipod 5 pods in 2024, a 68% increase driven by Dexcom sensor pairing. Beta Bionics’ iLet bionic pancreas, approved May 2024, doses insulin using only patient weight plus CGM data. ADA 2025 guidelines recommend automated delivery for all type 1 patients who can safely use the technology. Medicare now requires ≥80% CGM usage to qualify for pump reimbursement, effectively hard-linking sensor adoption to insulin-pump funding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device & Consumable Costs to Payers & Patients | -1.9% | United States, Mexico | Medium term (2-4 years) |

| GLP-1 Weight-Loss Drugs Reducing Testing Frequency | -1.3% | United States, Canada | Short term (≤ 2 years) |

| Rising Reports of Sensor-Adhesive Skin Dermatitis | -0.9% | United States, Canada | Medium term (2-4 years) |

| Regulatory Uncertainty Around Multi-Analyte Sensors | -0.7% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Device & Consumable Costs to Payers & Patients

A 10-day sensor wholesales for USD 75-95, producing yearly consumable costs up to USD 3,467 before insurance. Medicare Part B’s 20% coinsurance still leaves users with USD 547-693 out-of-pocket annually. Medicaid coverage is fragmentary: 38 states reimburse CGM for type 1, only 22 for non-insulin type 2, excluding 14 million beneficiaries. Mexico’s social-security formulary omits CGM entirely, forcing retail prices equal to 12-16% of the monthly minimum wage, restricting adoption to affluent urban consumers. Elevated cost, therefore, moderates penetration and dampens the North America continuous glucose monitoring market CAGR.

GLP-1 Weight-Loss Drugs Reducing Testing Frequency

Ozempic and Mounjaro posted combined U.S. sales of USD 14.3 billion in 2024, reducing A1c 1.5-2.0 percentage points and flattening glucose excursions. A Lancet study showed CGM time-in-use dropping from 85% to 62% six months post-GLP-1 initiation. Cigna now limits CGM coverage to patients with A1c > 8% or documented hypoglycemia, excluding 40% of GLP-1 users who achieve A1c < 7%. This pharmacologic substitution tempers addressable demand in the non-insulin type 2 cohort.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Sensors Dominate on Accuracy and Longevity Gains

Sensors accounted for 68.9% of the North America continuous glucose monitoring market share in 2025 and are projected to expand at a 16.87% CAGR through 2031. Their integration of Bluetooth Low Energy allows disposable form factors to communicate directly with smartphones, removing transmitters and trimming bill-of-material cost by 22%. Wearable sensors represent 92% of revenue; implantables grow faster at 21.3% by alleviating dermatitis complaints. Transmitters and receivers decline as stand-alone categories but persist among pediatric and senior users who lack smartphones.

Continued miniaturization underpins the competitive edge: Abbott’s 5-mm Libre 3 disk and Dexcom’s sleeker G7 both meet ISO 15197:2013 accuracy thresholds, positioning sensors as the hardware linchpin of the North America continuous glucose monitoring market size for the foreseeable future. FDA interoperability rules will further commoditize transmitters, concentrating value creation in sensor chemistry, wear duration, and algorithmic signal processing.

By Demography: Pediatric Segment Surges on Label Expansions

Adults generated 71.2% of 2025 revenue, but the pediatric group will grow at 18.92% CAGR after regulatory age floors fell to 2 years. The International Society for Pediatric and Adolescent Diabetes finds that CGM reduces hypoglycemia risk by 72% versus finger-stick monitoring. Ontario’s Assistive Devices Program funds 80% of the device cost for children, expanding access to 12,000 users. U.S. school-access legislation now allows students to view live glucose on smartwatches, normalizing classroom use. Meanwhile, adult adoption accelerates in the 35 million-strong non-insulin type 2 segment now served by over-the-counter Stelo and Libre 3. The demographic mix will therefore rebalance the North America continuous glucose monitoring market size toward younger cohorts without sacrificing adult revenue.

By End User: Home Care Leads on Telehealth and Reimbursement Tailwinds

Home settings captured 85.4% revenue in 2025 and will sustain a 17.87% CAGR thanks to RPM billing codes and direct-to-consumer shipment. Veterans Health Administration data show 38% fewer in-person visits after CGM-telehealth deployment. Private insurers erased prior authorization for millions of non-insulin users, further entrenching home distribution. Hospitals remain a niche, bound by infection-control protocols that prefer arterial lines for inpatients, while specialty centers focus on intensive education.

Remote data review is proving cost-effective; hence, health-system stakeholders increasingly steer patients toward at-home initiation, reinforcing the home-care dominance of the North America continuous glucose monitoring market share through 2031.

Geography Analysis

The United States accounted for 88.5% of 2025 revenue, energized by Medicare’s national coverage determination and over-the-counter clearances that enable pharmacy and e-commerce distribution. Removal of prescription requirements is forecast to add 4.2 million first-time users by 2027. However, surging GLP-1 uptake has already reduced CGM use frequency by 27% among type 2 cohorts, tempering upside.

Canada will post the fastest national growth at 16.43% CAGR through 2031 as Ontario, Quebec, and British Columbia eliminate prior-authorization and extend coverage to insulin-using adults. Health Canada approvals of Dexcom G7 and Libre 3 bring technology parity with the United States.

Mexico represents roughly 3% of regional value because social-security formularies exclude CGM and retail sensors cost MXN 1,500-2,000 (USD 88-117) each, 12-16% of the minimum wage. Private insurance penetration below 8% confines adoption to affluent urban consumers despite the nation’s 12.4 million-person diabetes burden.

Competitive Landscape

Market concentration remains high. Abbott, Dexcom, and Medtronic (MiniMed) captured the majority of revenue, but the North America continuous glucose monitoring market is fragmenting through over-the-counter models and pump interoperability mandates. Abbott’s FreeStyle Libre franchise generated USD 5.3 billion worldwide in 2024, half from North America.

Dexcom delivered USD 4.1 billion global revenue, fueled by G7 plus Stelo cash sales and integration deals with Tandem and Insulet. Medtronic booked a 12% integrated-pump share but faces interoperable competition after FDA guidances require open connectivity.

New entrants pursue white-space niches. Senseonics offers a 365-day implant for dermatitis-prone users. Biolinq’s microneedle array finished pivotal trials with 9.1% MARD and zero calibrations, targeting mid-2026 clearance. POCTech uses flexible electronics to chase sub-USD 50 sensors for retrospective review. Patent cliffs loom: core Dexcom sensing patents expire 2027-2028, potentially enabling biosimilar challengers, though algorithm patents extend to 2032. Strategic responses include Abbott’s USD 450 million California plant expansion and Medtronic’s sensor partnerships with Abbott and Instinct, signaling cost and interoperability battles ahead.

North America Continuous Glucose Monitoring Industry Leaders

DexCom, Inc.

Senseonics Holdings Inc.

Ascensia Diabetes Care

Abbott Laboratories

MiniMed

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Abbott completed phase-one expansion of its Alameda, California, plant, adding 100,000 square feet of Libre 3 manufacturing capacity

- September 2025: FDA cleared Medtronic MiniMed 780G for type 2 use with Abbott’s Instinct sensor, marking the first cross-vendor closed-loop pairing

- April 2025: Medtronic received FDA approval for the Simplera Sync sensor to accompany MiniMed 780G .

North America Continuous Glucose Monitoring Market Report Scope

As per the scope of the report, Continuous glucose monitoring (CGM) systems are wearable medical devices that provide real-time tracking of glucose levels throughout the day and night. Unlike traditional finger-prick tests that provide only a single "snapshot" of blood sugar at one moment, CGMs use a tiny sensor inserted just beneath the skin to measure glucose in the interstitial fluid, the fluid surrounding the body's cells.

The North American continuous glucose monitoring market is segmented by component, demography, end users, and country. By component, the market is categorized into sensors, transmitters, and receivers. By demography, the market is categorized into Pediatric (<18 Years) and Adult (≥18 Years). By end users, the segmentation includes hospitals & clinics, ambulatory surgical & specialty diabetes centers, and home care. Country-wise, the market is segmented across the United States, Canada, and Mexico. The market report also covers the estimated market sizes and trends for 3 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

By Component

| Sensors | Wearable |

| Implantable | |

| Transmitters | |

| Receivers |

By Demography

| Paediatric |

| Adult |

By End User

| Hospitals & Clinics |

| Ambulatory Surgical & Specialty Diabetes Centers |

| Home Care |

By Country

| United States |

| Canada |

| Mexico |

| By Component | Sensors | Wearable |

| Implantable | ||

| Transmitters | ||

| Receivers | ||

| By Demography | Paediatric | |

| Adult | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical & Specialty Diabetes Centers | ||

| Home Care | ||

| By Country | United States | |

| Canada | ||

| Mexico |

Key Questions Answered in the Report

How large is the North America continuous glucose monitoring market?

The market is expected to reach USD 10.38 billion in 2026 and is projected to grow to USD 21.56 billion by 2031.

Which component contributes the most revenue?

Sensors deliver 68.9% of 2025 revenue and lead the market’s 16.87% CAGR.

Why is Canada the fastest-growing geography?

Provincial reimbursement expansions in Ontario, Quebec, and British Columbia drive a 16.43% CAGR through 2031.

How are over-the-counter CGM models changing access?

FDA clearances for Abbott Libre 3 and Dexcom Stelo remove prescription barriers, enabling retail and e-commerce sales.

What is the main cost hurdle for uninsured users?

Annual consumable costs can reach USD 3,467, which equals more than 12% of median household income for many.

Page last updated on: