Middle East And Africa Jet Charter Services Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

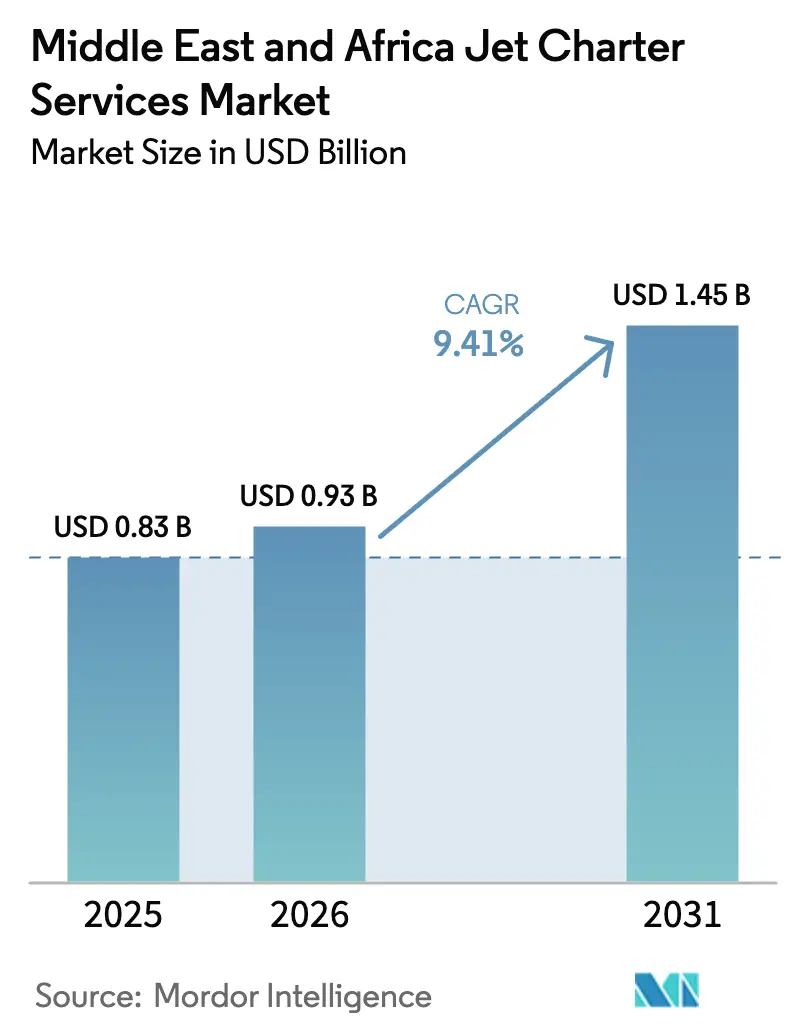

| Base Year Market Size (2025) | USD 0.83 Billion |

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.45 Billion |

| Growth Rate (2026 - 2031) | 9.41% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Jet Charter Services Market Analysis by Mordor Intelligence

The Middle East and Africa jet charter services market size is expected to grow from USD 0.83 billion in 2025 to USD 0.93 billion in 2026 and is forecast to reach USD 1.45 billion by 2031 at a 9.41% CAGR over 2026-2031. Large aircraft led demand in 2025 due to cross-border corporate travel needs across the Gulf, Africa, and Europe, while mid-size jets are set to rise fastest as Saudi domestic liberalization unlocks frequent intra-GCC shuttles that do not require ultra-long-range capacity. Operators are shifting toward digitally enabled bookings and prepaid programs as platforms like XO improve transparency and availability, thereby increasing repeat usage among corporate travelers across the market. New purpose-built FBOs in the UAE and Saudi Arabia are adding private terminal and hangar capacity, shortening ground times and relieving slot pressure at mainline hubs, supporting sustained growth through the decade. Rising HNWI counts in the Gulf and growth in Africa’s millionaire base are expanding the addressable customer pool, while talent constraints and fuel volatility remain headwinds that operators must price and plan around.

Key Report Takeaways

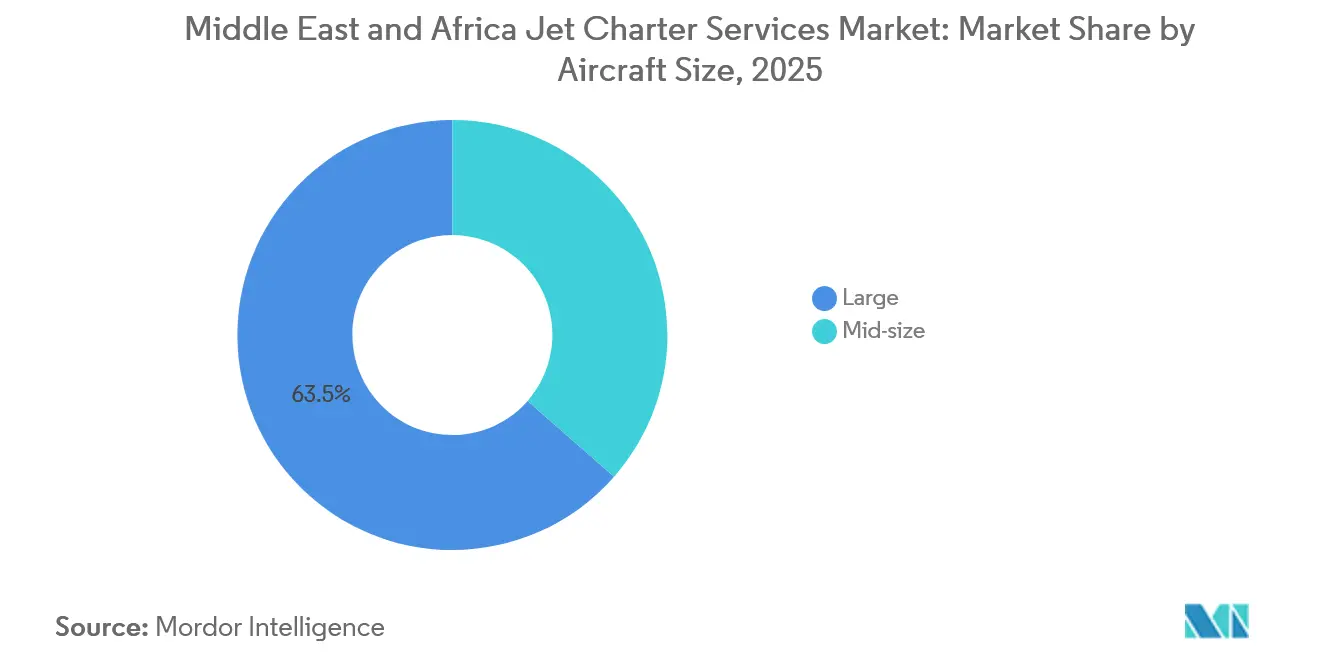

- By aircraft size, large jets dominated the market, accounting for 63.54% of revenue in 2025. Mid-size jets are projected to grow at a 10.45% CAGR through 2031, driven by the opening of Saudi domestic routes to foreign operators.

- By service model, the on-demand charter service model accounted for 72.40% of the Middle East and Africa jet charter services market size in 2025. Jet card membership is expected to grow at a CAGR of 12.87% through 2031, supported by digital platforms that reduce friction and ensure availability.

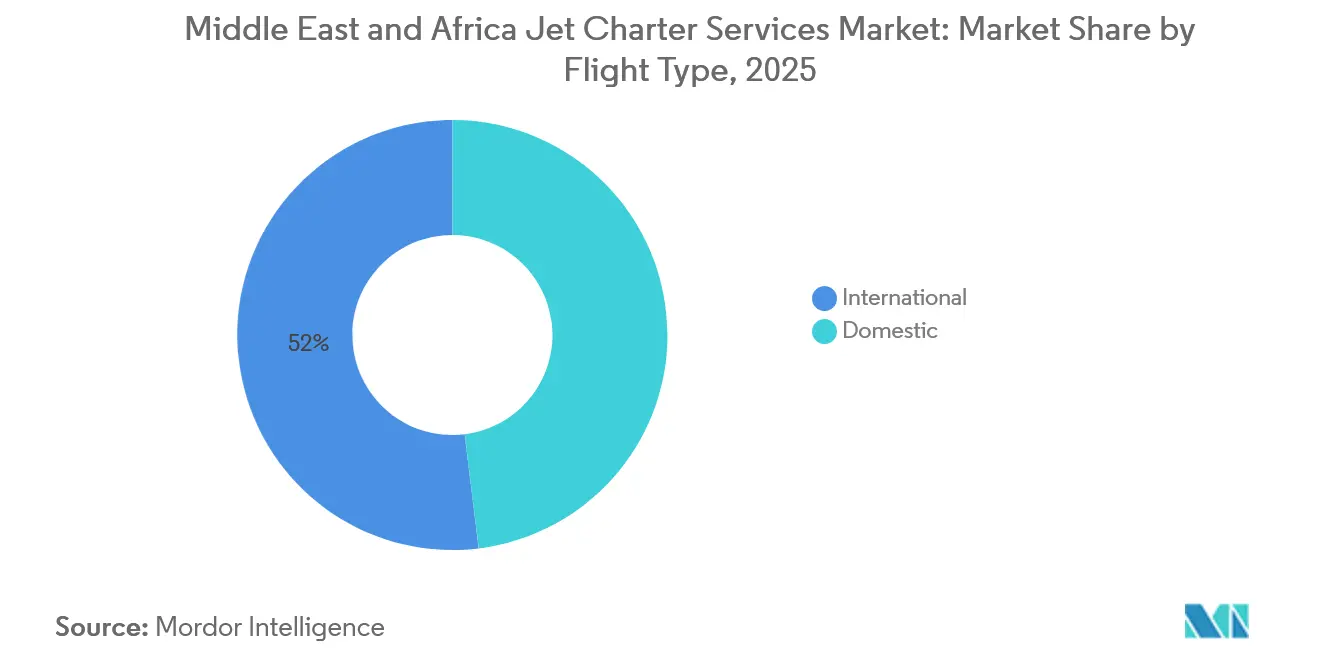

- By flight type, international flights accounted for 51.95% of the Middle East and Africa jet charter services market in 2025. Domestic routes are forecast to grow at a CAGR of 11.40% through 2031.

- By end user, corporates and SMEs accounted for 41.25% of the market in 2025. Sports and entertainment bookings are projected to grow at a CAGR of 11.80% through 2031, driven by events such as Expo 2030 Riyadh and the FIFA World Cup 2034.

- By geography, the Middle East held a 75.45% share of the market size in 2025.The region is expected to achieve the fastest growth, with a CAGR of 9.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Jet Charter Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HNWI and UHNWI population in GCC and key African economies | +2.8% | GCC core, South Africa, Morocco, Mauritius | Medium term (2-4 years) |

| Regulatory liberalization of Saudi domestic charter market | +1.9% | Saudi Arabia, spill-over to Kuwait and Oman | Short term (≤ 2 years) |

| Expansion of purpose-built FBO and private-terminal capacity across UAE, KSA, Qatar | +1.6% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Rapid adoption of digital and app-based booking platforms | +1.2% | UAE, Saudi Arabia, South Africa | Short term (≤ 2 years) |

| Boom in group charters for mega-events | +0.9% | Saudi Arabia, UAE, Qatar, Bahrain | Medium term (2-4 years) |

| Energy mega-projects in Namibia, Angola and Senegal triggering site-access charters | +0.7% | West and Southern Africa, spill-over to South Africa hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising HNWI and UHNWI Population in GCC and Key African Economies

HNWI growth across the Gulf is expanding the buyer base for premium on-demand and program charter. The surge in HNWI and UHNWI wealth across the GCC and Africa, backed by USD 7.3 trillion sovereign assets and USD 9.36 billion private capital flows, is fueling unprecedented demand for private aviation. Rising affluence, luxury real estate investments, and cross‑border mobility are driving high‑frequency private travel across regional and global hubs.[1]Source: Knight Frank Research, “The Private Capital Report 2025,” Knight Frank, knightfrank.com The UAE is projected to attract 9,800 millionaires by 2025, increasing the potential for repeat use of jet cards and corporate shuttle programs focused on Dubai and Abu Dhabi. In Africa, the millionaire population of 122,500 is forecast to grow 65% over the next decade, with South Africa at 41,100 HNWIs and Morocco rising to 7,500 millionaires in 2025, underscoring multipolar demand centers that complement Gulf hubs. Regional wealth expansion adds to cross-continental itineraries as family offices and corporates rotate investments into Africa, Europe, and Asia, which favors private charter for complex multi-leg trips within the Middle East and Africa jet charter services market. Rising wealth density in GCC capitals also drives fleet upgrades to newer, larger-cabin jets and supports operator strategies that bundle connectivity and concierge services to sustain premium yields.

Regulatory Liberalization of Saudi Domestic Charter Market

Saudi Arabia removed cabotage restrictions in May 2025, opening the domestic charter market to foreign operators and shifting demand toward higher-frequency, multi-leg itineraries under a single contract. The policy change aligns with the General Aviation Roadmap, which targets a USD 2 billion private aviation industry by 2030, and new dedicated business aviation airports and terminals that will deepen domestic route density. Business jet activity in Saudi Arabia had already risen in 2024, a signal of latent demand that liberalization is now bringing into the addressable base across the Middle East and Africa jet charter services market. VistaJet became the first foreign operator approved for domestic flights in August 2025 and reported strong growth in Saudi members during the first half of 2025, demonstrating a first-mover advantage in a newly opened segment. Air Charter Service opened its Riyadh office in September 2025 to capture corporate shuttle demand, which reflects the industry’s rapid mobilization following the regulatory shift.[2]Source: Air Charter Service, “Air Charter Service Opens First Office in Saudi Arabia, and 39th Globally,” Air Charter Service News, aircharter.co.uk

Expansion of Purpose-Built FBO and Private-Terminal Capacity Across UAE, KSA, Qatar

New FBOs and private terminals in the UAE and Saudi Arabia are adding hangar and passenger capacity, reducing turnaround times and relieving pressure on commercial terminals. Gama Aviation opened the USD 65 million Sharjah Business Aviation Centre in January 2026, featuring a large hangar and VIP terminal, creating a practical alternative to slot-constrained Dubai International for private flights. Ras Al Khaimah International Airport is adding a private aviation complex to further diversify departure options for business aviation users in the UAE. Dubai World Central is scaling its business aviation infrastructure following a 20,289 movement increase in 2025, reinforcing Dubai South as the region’s private aviation nucleus in the Middle East and Africa jet charter services market. In Saudi Arabia, the expansion of King Salman International Airport includes a dedicated private aviation terminal and VIP facilities, strengthening business aviation capacity in the capital. Qatar’s Hamad International Airport includes general aviation infrastructure that supports premium charter flights tied to major events, complementing Qatar Executive's fleet growth.

Rapid Adoption of Digital/App-Based Booking Platforms

Digital platforms are compressing quote times and enabling real-time pricing, which is changing how corporate buyers and HNWIs access charters. Vista’s XO Marketplace added features in late 2025 tailored to Middle Eastern clients, aggregating wide aircraft availability, fast quoting, and improving price transparency across the Middle East and Africa jet charter services market. Elevate Jet’s instant-booking app launch in February 2026 underlines the growing expectation for mobile-first access and rapid confirmations in private aviation. Air Charter LLC deployed an AI-powered booking engine in October 2025 that automates quote generation and demand-based adjustments, reducing transaction friction and enabling consistent lead times. VOO’s integration with corporate booking tools shows that private jet inventory is being integrated into the broader business travel technology stack to meet enterprise policy and reporting needs. At the regional scale, Vista reports a significant share of international business jet flights, which gives technology-led operators pricing power and network advantages over fragmented local brokers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fuel-price volatility and high OPEX for long-range fleets | -1.4% | Global, elevated cost exposure in Middle East and Africa | Short term (≤ 2 years) |

| Inadequate airport infrastructure and permit delays across Sub-Saharan Africa | -0.9% | Sub-Saharan Africa outside primary hubs | Long term (≥ 4 years) |

| Slot and apron congestion at Gulf hubs limiting peak-season capacity | -0.7% | Dubai, Abu Dhabi, Doha, with spill-overs | Medium term (2-4 years) |

| Regional pilot and maintenance talent shortage | -0.6% | Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fuel-Price Volatility and High OPEX for Long-Range Fleets

Fuel price swings continue to pressure operator margins and complicate pricing for spot charters. US data show jet fuel costs per gallon rose in January 2026 versus December, signaling ongoing volatility that operators in all regions must hedge or pass through in BTS pricing. The Argus US Jet Fuel Index also shows higher prices across major hubs in early 2026, consistent with tighter supply-demand balances and disruptions to refined product supply (A4A). The Middle East conflict elevated regional jet fuel benchmarks in March 2026. It widened crack spreads, which raised costs for long-range fleets operating transcontinental flights that are common in the Middle East and Africa jet charter services market. Operators are prioritizing newer aircraft with lower fuel burn to defend margins during spikes, helping stabilize program pricing for repeat corporate and HNWI clients. Multi-year contracts offer a path to absorb surcharges more predictably. At the same time, pure spot buyers face larger swings in trip quotes during volatile periods across the Middle East and Africa jet charter services market.

Inadequate Airport Infrastructure and Permit Delays Across Sub-Saharan Africa

Structural infrastructure gaps and complex permitting processes constrain addressable demand in Africa, particularly outside primary hubs. AFRAA notes a substantial aviation infrastructure funding gap through 2040, resulting in capacity bottlenecks at many airports that affect charter schedule reliability.[3]Source: AFRAA, “Masterclass 2: Capturing Rising Africa Travel Demand,” AFRAA, afraa.org Many secondary cities lack efficient ground handling and technology, which increases turnaround times and reduces aircraft utilization in the Middle East and Africa jet charter services market. Operators also report extended permit lead times in key markets such as South Africa, which can force conservative scheduling buffers and erode the time-saving value proposition. Capital plans at major hubs in South Africa aim to improve capacity. However, upgrades remain concentrated in primary gateways rather than in secondary cities where energy and safari routes are growing. The effect is a two-speed landscape where well-run hubs are improving. At the same time, secondary fields still require long lead times and resilient contingency planning for operators serving Africa-focused routes in the Middle East and Africa jet charter services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Size: Mid-Size Jets Gaining Ground as Cabotage Opens

Large aircraft led with 63.54% of the market share in 2025, as cross-border executive travel favored longer-range, larger cabins for multi-leg missions. Mid-size jets are expected to grow fastest at a 10.45% CAGR through 2031 as Saudi domestic liberalization creates steady demand for intra-GCC shuttles that balance range, cabin comfort, and hourly cost. Light jets serve niche city pairs within a single country and short regional hops. However, competition from frequent business-class schedules can narrow the charter's value proposition on the shortest routes. Corporations planning site visits to energy markets are using mid-size jets to optimize fuel efficiency and duty time while maintaining productivity on board. FBO developments in Sharjah and Ras Al Khaimah favor higher-frequency operations, which align with mid-size deployment strategies in the Middle East and Africa jet charter services market.

Operators are positioning fleets to capture growth in Saudi domestic and cross-border GCC flying, where mission profiles fit mid-size performance envelopes. Vista Global’s recent commitment to Bombardier Challenger 3500 aircraft strengthens its mid-size capacity and signals confidence in sustained growth from 2026. The Middle East and Africa jet charter services industry is also seeing operators diversify fleets to balance ultra-long-range demand against growing mid-size utilization. As utilization rises on mid-size types, operators can deliver more departures per day without compromising comfort, which benefits return on capital in the market.

By Service Model: Jet Card Membership Disrupting Traditional On-Demand

On-demand charter held a 72.40% share of the Middle East and Africa jet charter services market in 2025, as transactional bookings remained the default behavior among corporate and HNWI clients. Jet card membership is forecast to be the fastest-growing model, with a 12.87% CAGR to 2031, as prepaid hours and guaranteed availability attract repeat users who prioritize time certainty over price volatility. Subscription models and fractional integration remain smaller in the region due to regulatory complexity around aircraft registration and import duties. Shared charter has limited traction due to privacy preferences, though some predictable trunk routes show modest adoption.

As digital marketplaces standardize real-time pricing and inventory visibility, friction declines and repeat usage increase for prepaid programs. VistaJet's growth in Saudi Program Members in 2025 underscores the mutual reinforcement of program economics and domestic liberalization within the Middle East and Africa jet charter services market. Saudi Arabia has established itself as a critical growth market for VistaJet, presenting numerous opportunities. In the first half of 2025, the company recorded a 32% year-over-year increase in VistaJet Program Members in the Kingdom, indicating rising demand for both domestic and international flying solutions among local and international clients. The jet charter services industry in Middle East and Africa is moving from occasional purchasing to relationship-based commitments that support guaranteed access during event peaks. Operators with robust tech stacks and program management capabilities are best positioned to win wallet share as clients lock in hours and service levels.

By Flight Type: Domestic Routes Accelerate Post-Regulatory Reform

International flights accounted for 51.95% of flight-type revenue in 2025, driven by Gulf-to-Europe corridors and intra-African connections that lack convenient scheduled options for executive travel. Domestic routes are projected to grow at 11.40% CAGR to 2031, with the Saudi General Aviation Roadmap and cabotage removal allowing foreign operators to run in-Kingdom itineraries. Short-haul domestic shuttles, such as Riyadh to Jeddah or Abu Dhabi to Dubai, compress travel time versus long ground transfers. Long-haul domestic routes, such as Riyadh to Neom, extend charters to development zones and tourist areas. International long-haul continues to anchor revenue on ultra-long-range jets, where nonstop capability sustains premium yields, supporting the fleet mix in the Middle East and Africa jet charter services market.

The opening of Saudi domestic services to foreign AOCs enables multi-leg contracts that previously required aircraft swaps, thereby removing friction and reducing time on itineraries. VistaJet’s first-mover entry in August 2025 underscores the immediate opportunity as operators reposition aircraft regionally to reduce empty legs and tighten pricing. International short-haul remains more price sensitive due to plentiful commercial schedules, but time-critical executive trips continue to support private demand. The Middle East and Africa jet charter services industry benefits from asset utilization gains on domestic sectors where aircraft can complete multiple rotations per day, improving revenue per day and fuel economics. Permit and compliance planning remains critical for cross-border operations in Africa, where timelines can stretch without careful coordination.

By End User: Sports and Entertainment Charters Surge on Event Calendar

Corporations and SMEs accounted for 41.25% of demand in 2025 as executive travel, board meetings, and energy site access required flexible scheduling and direct routing. Sports and entertainment are set to be the fastest-growing end-user segment, with a 11.80% CAGR through 2031, as the region hosts the F1 calendar, Expo 2030 Riyadh, and the FIFA World Cup 2034. HNWI and private travelers remain a large cohort, while governments and NGOs rely on charter for diplomatic and humanitarian missions. Event peaks compress departure windows and ramp congestion, which rewards operators who pre-secure hangar space and crew accommodations.

Pricing dynamics during events illustrate the willingness to pay for guaranteed timing. Pricing dynamics during events highlight the willingness to pay for guaranteed timing. For instance, during the Saudi Arabian Grand Prix in Jeddah, long-range jet charters from Paris typically cost EUR 70,000 -90,000 (USD 76,300 - USD 98,100) one-way, demonstrating surcharge acceptance when alternatives involve significant connection risks. Program membership helps corporates cap exposure during volatile periods and ensures availability for critical meetings. Government and NGO charters provide repeat volumes and reliable collections that balance seasonal variability in the Middle East and Africa jet charter services market. Qatar Executive’s revenue gains alongside fleet growth show how national operators can serve state and private-use cases in parallel.

Geography Analysis

The Middle East accounted for 75.45% of 2025 demand and is projected to grow fastest at a 9.87% CAGR through 2031, as Saudi domestic liberalization and UAE FBO expansions enable more flying and shorter turn times. Dubai South recorded 20,289 business aviation movements in 2025, confirming the hub’s central role for regional private traffic within the Middle East and Africa jet charter services market. Saudi Arabia’s flight activity rose, and VistaJet’s domestic authorization in 2025 points to a rapid build-out of in-Kingdom services that reduce friction for corporates and HNWIs. Qatar Executive’s fleet additions support long-range capability and strengthen Doha’s role in connecting GCC and Europe for premium travelers.

Africa represented 24.55% of 2025 demand but faces infrastructure and permit hurdles that slow growth outside primary hubs. AFRAA highlights a material funding gap and capacity constraints that increase operating costs and reduce predictability on secondary routes. South Africa’s regulatory progress enables certified providers like ExecuJet to perform heavy maintenance on aircraft registered in local registries, thereby improving airworthiness and turnaround times for regional fleets. West African energy logistics in Ghana and Nigeria require crew rotations where charter remains the efficient solution for site access. Morocco’s growing millionaire base strengthens North Africa to Europe routes that align with premium leisure and business travel.

Looking ahead, Middle East growth is likely to remain underpinned by new private-terminal capacity and event-driven traffic, while Africa’s growth depends on permit reform and targeted investments at secondary airports. Operators are forming regional partnerships and subsidiaries to navigate regulatory limits and capture more of the value chain in-country. The Middle East and Africa jet charter services market will reward operators that connect Gulf and African networks with reliable scheduling and consistent service levels, supported by modern fleets and purpose-built FBO infrastructure.

Competitive Landscape

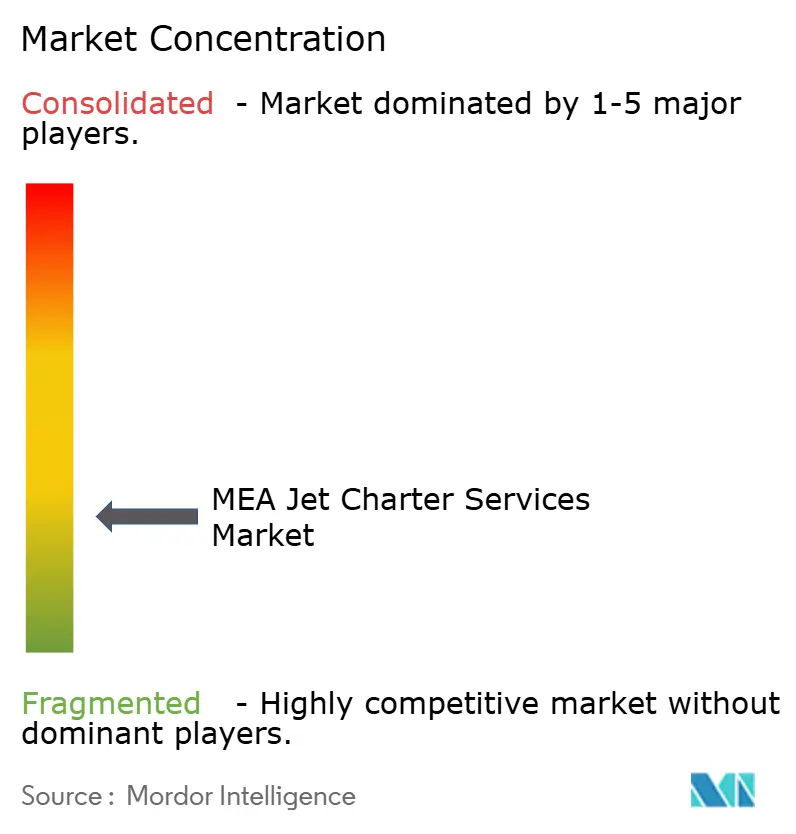

The competitive landscape remains fragmented. Royal Jet LLC, Qatar Executive, VistaJet, Empire Aviation Group, ExecuJet, NASJET, and DC Aviation Al-Futtaim compete on fleet quality, connectivity, and consistent service outcomes across the Middle East and Africa jet charter services Market. VistaJet’s domestic authorization in Saudi Arabia created a first-mover window, and its member growth in 2025 suggests a successful early land grab in a newly opened segment. Empire Aviation is investing in new headquarters at Dubai’s Mohammed Bin Rashid Aerospace Hub, securing hangar access and enhancing operational control as Dubai South scales its private aviation infrastructure.

Operators are also using connectivity and technology to differentiate. Qatar Executive’s Starlink installation on the G650ER fleet enhances real-time collaboration onboard, which matters for clients who conduct business in-flight. Digital aggregators like XO and innovators like AirCharter.com reduce booking times and expose real-time pricing, which can shift share from traditional brokers toward platform-enabled operators in the Middle East and Africa jet charter services market. ExecuJet’s MRO expansion and partnerships, including new painting capacity, increase in-house control of turnaround times, and reduce reliance on third-party queues during peaks.

Balance sheet strategies and fleet commitments are also shaping competitive positioning. Air Charter Service’s Riyadh office expands local presence and supports government and enterprise demand for domestic shuttles and multi-leg journeys. As FBO capacity proliferates in Sharjah and Ras Al Khaimah, operators with early leases and hangar slots can capture logistical advantages that translate into faster turn times and better peak-hour access. The competitive arc will be shaped by how quickly regulatory liberalization spreads beyond Saudi Arabia and whether operators can scale programs and technology to convert frequent travelers into long-term members across the Middle East and Africa jet charter services market.

Middle East And Africa Jet Charter Services Industry Leaders

Royal Jet LLC

VistaJet Group Holding Limited

ExecuJet Aviation Group AG

Empire Aviation Group

Qatar Executive (Qatar Airways Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Empire Aviation’s addition of a Gulfstream G600 to its fleet reflects the increasing regional demand for high-performance, long-range business jets. This move reinforces the Middle East’s position as a key market for private aviation, driving fleet modernization and expanding charter service capabilities to meet evolving client needs.

- January 2025: Qatar Executive’s acquisition of two additional Gulfstream G700 aircraft, increasing its fleet to 24, highlights its strategic investment in expanding ultra-long-range capabilities. This development reflects the growing demand for premium private aviation services, added operational capacity, and positions the company to strengthen its market share in the global luxury travel segment.

Middle East And Africa Jet Charter Services Market Report Scope

A charter business model involves renting an aircraft to users based on their specific operational needs. A charter service provider or operator is a licensed and accredited organization responsible for providing pilots, maintaining the aircraft, and managing its operations. Charter services cater to individuals, corporations, businesses, VIPs, sportspeople, and government officials, following an agreement with the charter operator on the terms and conditions of the rental program. Additionally, charter aircraft can be adapted for other purposes, such as emergency medical services, cargo transportation, or equipment resupply. The market scope is confined to the Middle East and Africa.

The Middle East and Africa jet charter services market is segmented based on aircraft size. service model, flight type, end user, and geography. By aircraft type, the market is segmented into light jets, mid-size jets, and large jets. By service model, the market is segmented by on-demand charter, jet card membership, subscription-based charter, fractional charter integration, and shared charter. By flight type, the market is segmented into domestic and international, with further sub-segmentation into short- and long-haul. By end user, the market is segmented into corporates and SMEs, HNWI/private individuals, sports and entertainment, government, and NGO. The report also covers the market size and forecasts for the Middle East and Africa jet charter services market in 5 major countries across the Middle East and 4 major countries across Africa. For each segment, the market sizing and forecasts have been provided based on revenue (USD).

| Light |

| Mid-size |

| Large |

| On-Demand Charter |

| Jet Card Membership |

| Subscription-based Charter |

| Fractional Charter Integration |

| Shared Charter |

| Domestic | Short Haul |

| Long Haul | |

| International | Short Haul |

| Long Haul |

| Corporates and SMEs |

| HNWI/Private Individuals |

| Sports and Entertainment |

| Government and NGO |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Kuwait | |

| Oman | |

| Rest of the Middle East | |

| Africa | South Africa |

| Ghana | |

| Morocco | |

| Nigeria | |

| Rest of Africa |

| By Aircraft Size | Light | |

| Mid-size | ||

| Large | ||

| By Service Model | On-Demand Charter | |

| Jet Card Membership | ||

| Subscription-based Charter | ||

| Fractional Charter Integration | ||

| Shared Charter | ||

| By Flight Type | Domestic | Short Haul |

| Long Haul | ||

| International | Short Haul | |

| Long Haul | ||

| By End User | Corporates and SMEs | |

| HNWI/Private Individuals | ||

| Sports and Entertainment | ||

| Government and NGO | ||

| By Geograghy | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Ghana | ||

| Morocco | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

Where is new private aviation infrastructure easing capacity pressures?

The sector is projected to grow at a 9.41% CAGR over 2026-2031, reaching USD 1.45 billion by 2031.

Which aircraft category leads demand in Middle-East and Africa jet charter services?

Large jets led with 63.54% share in 2025, supported by long-range corporate missions that connect GCC hubs with Africa and Europe.

How are digital platforms changing charter buying in the region?

Marketplaces like XO and AI-enabled systems are speeding quote times and improving price transparency, which boosts repeat usage and supports program membership growth.

Which end user segment is growing fastest across Middle East and Africa charters?

Sports and entertainment is forecast to grow at 11.80% CAGR through 2031, supported by the F1 calendar, Expo 2030 Riyadh, and FIFA World Cup 2034.

Where is new private aviation infrastructure easing capacity pressures?

New and expanded private terminals and hangars in Sharjah, Dubai South, Ras Al Khaimah, and Riyadh are reducing turnaround times and adding based-aircraft capacity.

Page last updated on: