Citric Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.93 Billion |

| Market Size (2031) | USD 4.81 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

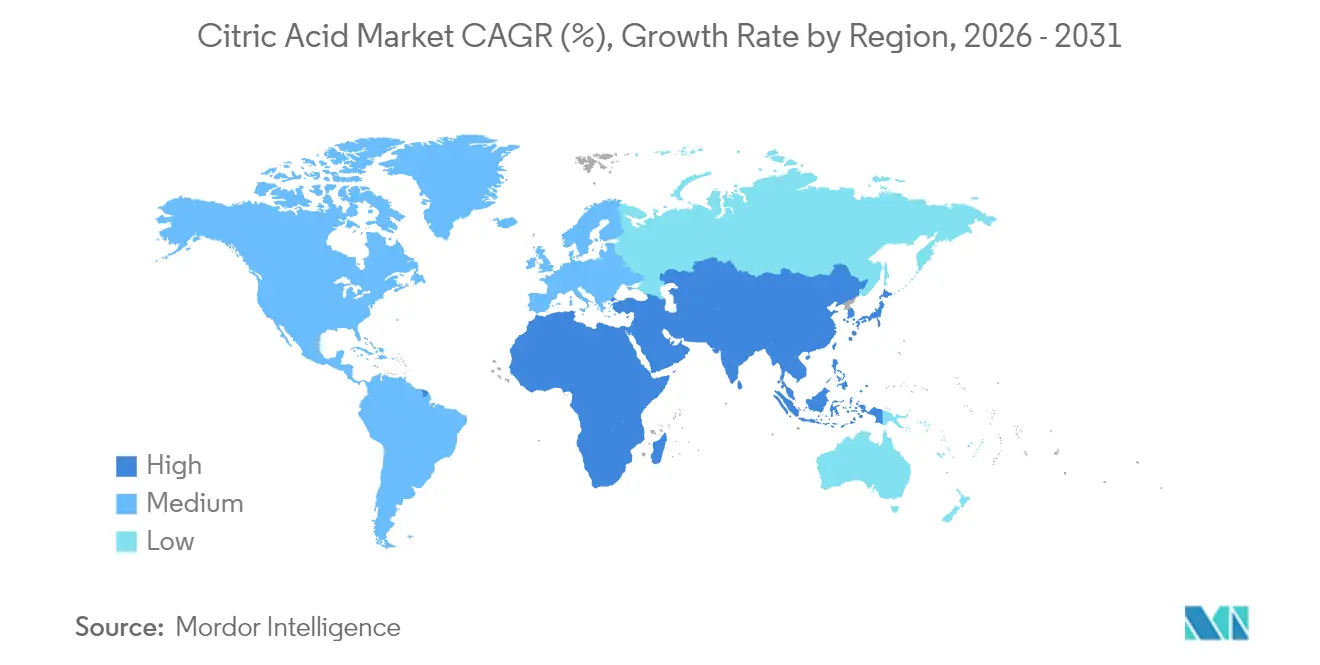

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Citric Acid Market Analysis by Mordor Intelligence

The citric acid market size is expected to grow from USD 3.77 billion in 2025 to USD 3.93 billion in 2026, and reach USD 4.81 billion by 2031, growing at a CAGR of 4.12% from 2026 to 2031. Global adoption of clean-label food formulations, widening phosphate restrictions in detergent chemistry, and the roll-out of cost-efficient Asian fermentation capacity are combining to keep demand on an upward path. Food and beverage producers accounted for 49.74% of 2025 consumption as bakery, beverage, and dairy brands switched out synthetic preservatives in favor of citric acid that carries explicit approvals under FDA 21 CFR 184.1033 and EFSA E330[1]Source: U.S. Food and Drug Administration, “Substances Added to Food,” fda.gov. At the same time, phosphate bans anchored in EU Regulation 648/2004 pushed household-cleaner formulators toward biodegradable citrate builders, generating the fastest-growing application pool. Asia-Pacific’s 35.43% share in 2025 reflected China’s 1.067 million-kilogram export machine and India’s new molasses-sourced plants, while the Middle East and Africa emerged as the highest-growth territory on the back of beverage and confectionery investment pipelines.

Key Report Takeaways

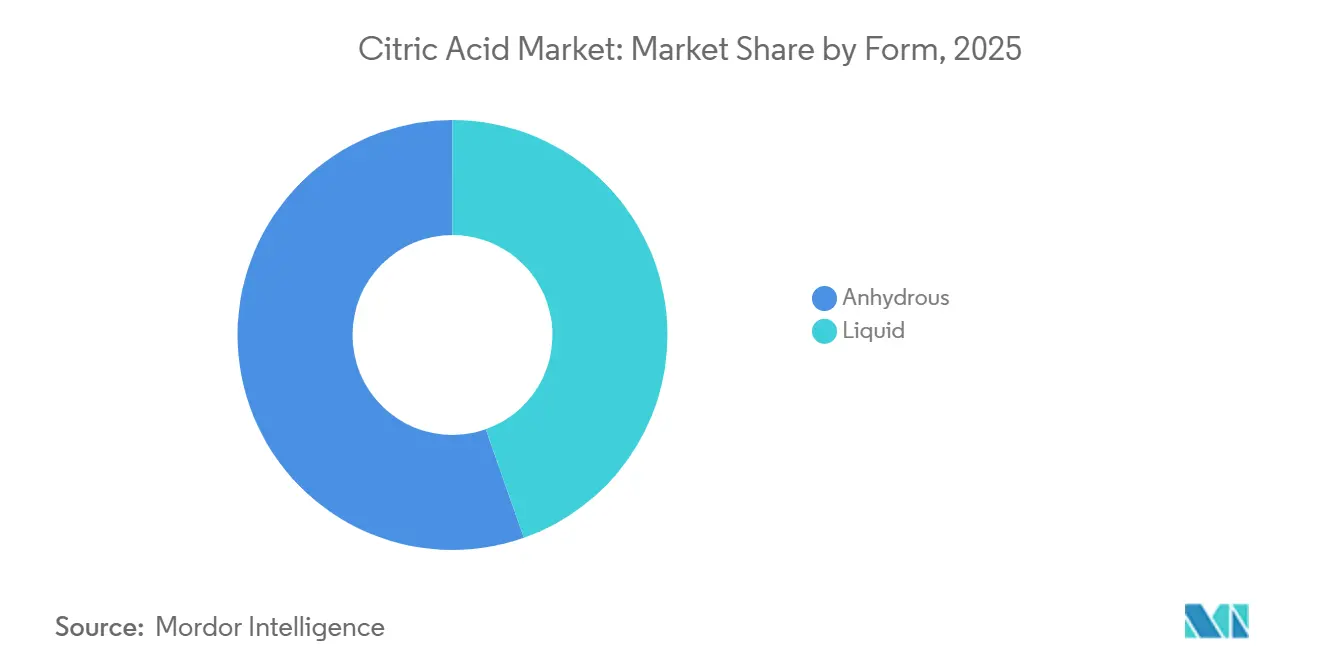

- By form, anhydrous grade captured 55.62% of volume in 2025; liquid citric acid is forecast to expand at a 5.80% CAGR through 2031.

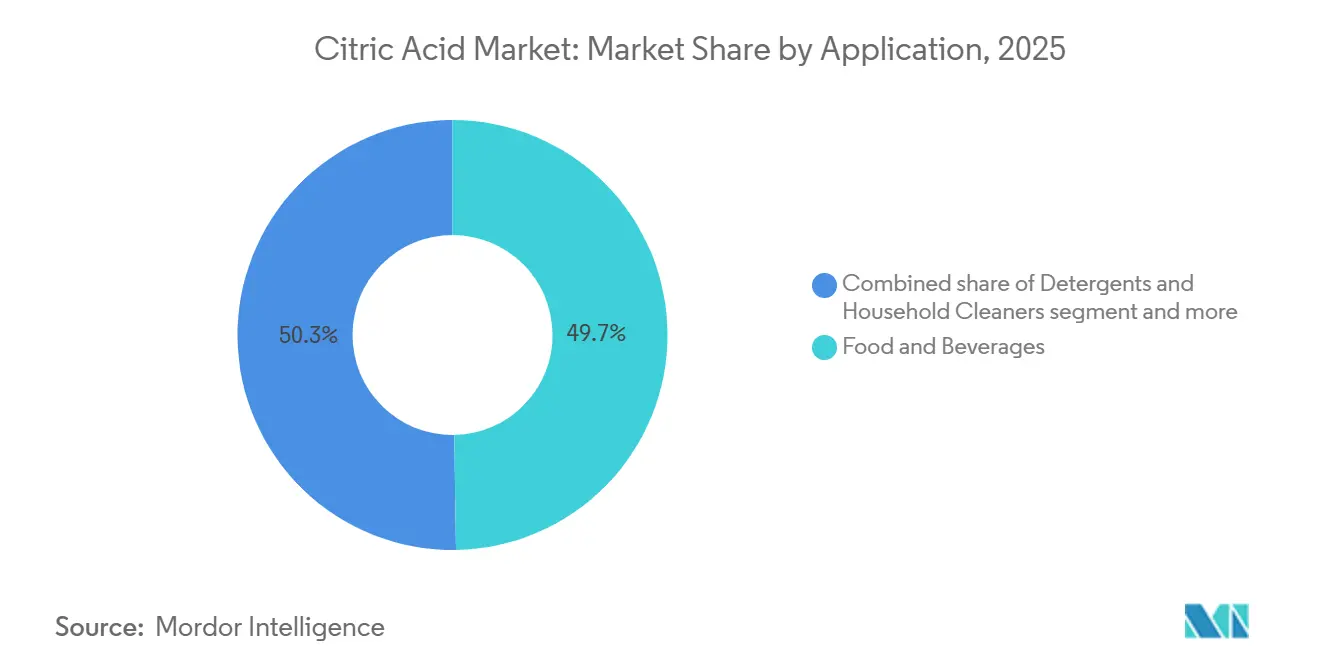

- By Application, food and beverages led with 49.74% revenue share in 2025; detergents and household cleaners are advancing at a 6.03% CAGR through 2031.

- By geography, Asia-Pacific held 35.43% of the citric acid market share in 2025; the Middle East and Africa are set to post a 6.56% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Citric Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-label demand surge in processed foods and beverages | +1.2% | Global, with North America and Europe leading the reformulation | Medium term (2-4 years) |

| Phosphate bans boosting citrate use in detergents | +0.9% | Europe (primary), North America (emerging), Asia-Pacific (selective) | Short term (≤ 2 years) |

| Expanding pharmaceutical excipient applications | +0.6% | North America, Europe, India (generics hub) | Long term (≥ 4 years) |

| Growth of bio-based production capacity in Asia | +0.8% | China, India, Thailand, Indonesia | Medium term (2-4 years) |

| Commercialization of Yarrowia lipolytica waste-glycerol routes | +0.4% | Europe (pilot scale), Asia-Pacific (scale-up potential) | Long term (≥ 4 years) |

| EU Green Deal incentives for biodegradable chelants | +0.5% | Europe (core), spill-over to the Middle East and North Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Clean-label demand surge in processed foods and beverages

Consumer preference for recognizable ingredients has compelled food manufacturers to replace synthetic preservatives with naturally derived alternatives, positioning citric acid as a dual-function acidulant and antimicrobial agent in bakery, confectionery, and dairy applications. FDA recognition under 21 CFR 582.1033 as a direct food substance affirmed as generally recognized as safe (GRAS) eliminates regulatory friction, enabling formulators to declare citric acid on ingredient panels without consumer skepticism. Beverage producers are leveraging citric acid's tartness to mask off-notes in reduced-sugar formulations, a trend accelerating as sugar taxes proliferate across Latin America and Southeast Asia. Bakery applications benefit from citric acid's ability to extend shelf life by lowering pH below 4.6, inhibiting Clostridium botulinum growth without imparting the metallic aftertaste associated with sorbates or benzoates. The clean-label imperative is further amplified by retailer mandates; major European grocery chains now require suppliers to eliminate E-number additives from private-label lines, driving reformulation cycles that favor citric acid over calcium propionate or sodium benzoate.

Phosphate bans boosting citrate use in detergents

Regulatory restrictions on phosphates in household detergents, codified in EU Regulation (EC) 648/2004 and reinforced by amendments limiting phosphorus content to 0.3 grams per standard dose, have catalyzed substitution with citric acid and its sodium salts as builders and chelating agents[2]Source: European Chemicals Agency, “Detergents Regulation,” echa.europa.eu. Citric acid sequesters calcium and magnesium ions in hard water, preventing scale deposition on fabrics and washing-machine components, while its biodegradability under OECD 301B protocols satisfies environmental criteria that phosphates fail. European consumption of household cleaning products reached approximately 100,000 tonnes in 2025, with Germany, France, and the United Kingdom accounting for the majority of uptake. North American jurisdictions are following suit; several U.S. states have enacted phosphate bans in automatic dishwasher detergents, and Canadian provinces are considering similar measures. The detergent segment's 6.03% CAGR through 2031 reflects not only regulatory push but also formulator recognition that citric acid enables concentrated liquid formats by maintaining stability at lower pH, reducing packaging weight and transport emissions, a dual benefit as brands pursue sustainability claims.

Expanding pharmaceutical excipient applications

Citric acid's role as a buffering agent, effervescent component, and taste-masking excipient in pharmaceutical formulations is broadening as generic-drug manufacturers in India and China scale production of orally disintegrating tablets and pediatric suspensions. Compliance with United States Pharmacopeia (USP) and European Pharmacopoeia (EP) monographs ensures batch-to-batch consistency, a non-negotiable requirement for regulatory approval by the FDA and European Medicines Agency. Effervescent tablets, widely used for analgesics, vitamins, and electrolyte replacements, rely on citric acid reacting with sodium bicarbonate to generate carbon dioxide, enhancing dissolution and patient compliance. The shift toward patient-centric dosage forms, particularly in geriatric and pediatric populations, is driving demand for pharmaceutical-grade citric acid that meets stringent heavy-metal limits (≤10 ppm lead, ≤5 ppm arsenic per USP standards). India's emergence as a generics powerhouse, supplying over 40% of global generic-drug demand, positions the subcontinent as a growth engine for pharmaceutical excipient consumption, with citric acid benefiting from its dual utility in both active pharmaceutical ingredient (API) synthesis and final formulation.

Growth of bio-based production capacity in Asia

Asia-Pacific's 35.43% market share in 2025 rests on integrated fermentation complexes in China, India, and Thailand that convert molasses and corn-steep liquor into citric acid via Aspergillus niger submerged fermentation, achieving yields exceeding 90% on a substrate basis. China's COFCO Biochemical, RZBC Group, and Weifang Ensign operate plants with individual capacities surpassing 100,000 tonnes per annum, leveraging proximity to sugarcane and corn-processing hubs to minimize feedstock logistics costs. India is witnessing greenfield investments; a feasibility study for a 30,000-tonne-per-annum anhydrous citric acid plant estimates total capital expenditure at INR 18.12 billion, with a projected rate of return of 47% and break-even at 45% capacity utilization. Thailand's anti-dumping duties on Chinese imports (57.79% as of January 2025) are incentivizing domestic capacity additions to serve ASEAN markets, where beverage and processed-food consumption is rising at double-digit rates Thailand Department of Foreign Trade. The region's cost advantage, molasses priced 30-40% below refined sugar on a dry-matter basis, sustains competitiveness even as Western producers pursue premium-grade segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corn and sugar price volatility | -0.7% | Global, with acute exposure in North America (corn) and Brazil (sugar) | Short term (≤ 2 years) |

| Margin pressure from the Chinese overcapacity and anti-dumping duties | -0.9% | Asia-Pacific (export-dependent), North America and Europe (import-competing) | Medium term (2-4 years) |

| Surge in gypsum-waste disposal compliance costs | -0.4% | North America, Europe (stringent landfill regulations) | Long term (≥ 4 years) |

| Substitution threat from emerging multi-acid blends | -0.5% | Global, concentrated in premium food and personal-care segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Corn and sugar price volatility

Citric acid production economics hinge on feedstock costs, with molasses, corn-steep liquor, and refined sugar accounting for 40-50% of total manufacturing expenses in fermentation-based processes. Sugar production in the 2023/24 crop year totaled 179.4 million tonnes globally, with Brazil exporting 34 million tonnes, yet prices remain susceptible to weather anomalies. El Niño-induced droughts in Thailand and India curtailed 2024 cane yields, tightening molasses availability and elevating spot prices by 18-22% year-over-year[3]Source: Food and Agriculture Organization, “Sugar Market Review 2025,” fao.org. Corn prices, critical for U.S. and European producers, oscillate with biofuel mandates; the U.S. Renewable Fuel Standard's requirement for 15 billion gallons of corn ethanol annually diverts feedstock, creating competition that spikes during short-crop years. Fertilizer cost collapses, from USD 815 per tonne in April 2022 to USD 327 per tonne in April 2024, providing temporary relief, yet freight-rate volatility linked to container-shipping disruptions (Red Sea diversions, Panama Canal draft restrictions) has inflated import bills for molasses and raw sugar by 12-15% in 2025. Producers lacking vertical integration into sugar refining or corn wet-milling face margin compression when feedstock inflation outpaces their ability to pass costs downstream, particularly in price-sensitive food-grade segments where buyers resist mid-contract adjustments.

Margin pressure from Chinese overcapacity and anti-dumping duties

In recent years, China's citric acid exports reached 1,067 million kilograms, showcasing a domestic capacity three times higher than local consumption. About 300,000 tonnes are consumed domestically, with the rest allocated for exports, as reported by the U.S. Environmental Protection Agency. This oversupply has triggered anti-dumping duties globally. In January 2025, Thailand imposed a 57.79% duty after its fifth sunset review. U.S. duties range from 0.48% to 156.45%, depending on the producer, while the European Union has implemented similar measures, according to the Thailand Department of Foreign Trade. These trade barriers have fragmented the global market, forcing Chinese producers to absorb duties or redirect exports to less-regulated markets in Africa and Latin America, where infrastructure and purchasing power constraints limit pricing. Western producers benefit from import protection but face retaliation risks. China's Ministry of Commerce has launched countervailing-duty investigations on U.S. and European specialty chemicals, creating uncertainty for diversified firms. The result is margin volatility: Chinese exporters operate on thin spreads (often under 5% EBITDA margins) to maintain market share, while North American and European producers struggle to justify capacity investments amid periodic dumping in spot markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Anhydrous Dominance Anchored in Dry-Mix Stability

In 2025, anhydrous citric acid dominated the market with a 55.62% share, solidifying its role in dry-blend applications sensitive to moisture. Its crystalline stability is crucial for powdered beverage mixes, effervescent tablets, and bakery enhancers, preventing premature reactions with bicarbonates and hygroscopic ingredients. Liquid citric acid, projected to grow at a 5.80% CAGR through 2031, is gaining traction in pharmaceutical and personal-care products, where precise pH control in aqueous systems and ease of handling are prioritized. The pharmaceutical industry's shift to liquid orally disintegrating films and pediatric syrups is driving liquid citric acid adoption, avoiding dust and static-electricity issues in cleanrooms. Food-service operators are also favoring liquid formats for beverage dispensing and dressing preparation, as pre-dissolved citric acid eliminates mixing and reduces labor costs. While anhydrous citric acid benefits from lower production costs due to crystallization and drying, liquid suppliers are closing the gap by co-locating with fermentation plants to reduce water transport costs.

Both forms of citric acid comply with ISO 9001 and HACCP protocols. However, anhydrous citric acid, classified as a non-hazardous solid under UN transport regulations, simplifies logistics compared to liquid citric acid, labeled as corrosive (UN 1760, Class 8), which requires specialized containers and handling. Innovations in spray-drying and fluidized-bed granulation are enabling anhydrous producers to customize particle sizes for specific uses, such as coarse granules (40-100 mesh) for tableting and fine powders (200+ mesh) for beverage clouding. These tailored products command a 10-15% premium over standard anhydrous citric acid. Liquid citric acid suppliers are countering with stabilized formulations, removing chelated trace metals to sub-ppm levels to meet stringent cosmetic and injectable-pharmaceutical standards, where even minor iron or copper contamination can cause discoloration or oxidation.

By Application: Food and Beverages Lead, Detergents Accelerate

In 2025, food and beverages held a 49.74% market share, while detergents and household cleaners were the fastest-growing application with a 6.03% CAGR projected through 2031. This reflects the dual forces driving citric acid demand: clean-label reformulations in edibles and phosphate-replacement mandates in cleaning products. Beverages dominate the food and beverage sector, using citric acid's tartness to balance sweetness in carbonated drinks, energy drinks, and teas. Coca-Cola and PepsiCo typically use 0.05-0.15% citric acid, achieving a pH of 2.5-3.5 to curb microbial growth and enhance flavor. In bakeries, citric acid extends the shelf life of breads and cakes by 20-30% by chelating metal ions. Dairy processors use it in processed cheese to emulsify fats and adjust pH for optimal protein solubility, critical for cheese-sauce and spread formulations. Confectionery producers use citric acid to prevent sugar crystallization in hard candies and add sour notes in gummies, with usage rates of 2-3% in extreme-sour variants. Savory snacks are increasingly coated with citric acid to enhance tanginess and flavor, driven by demand for bold, global flavors.

In pharmaceuticals, citric acid acts as an effervescent agent and buffer, benefiting from India's generics boom, where over 40% of U.S. FDA-approved generic-drug facilities are located. In personal care, citric acid adjusts pH in shampoos and conditioners (pH 4.5-5.5) and serves as an alpha-hydroxy acid in anti-aging serums, promoting exfoliation and collagen synthesis. The "Others" category includes industrial applications, metal cleaning, textile processing, and concrete admixtures, where citric acid's chelating properties remove rust and scale. However, these segments face substitution pressures from cheaper alternatives like EDTA and gluconic acid. Detergents' growth is driven by phosphate bans and the rise of concentrated liquid formats, where citric acid ensures stability at pH 3-4, preventing precipitation of surfactants and enzymes. Growth is uneven geographically; European detergent consumption rose 8% year-over-year in 2025, while North America lagged at 4% due to slower regulatory adoption and a preference for powder formats that tolerate higher pH levels.

Geography Analysis

In 2025, Asia-Pacific commands a 35.43% market share, largely due to China's robust production capabilities and its surging domestic appetite in food processing and industrial sectors. The region's advantages include a well-established fermentation infrastructure, competitive production costs, and close access to vital raw materials like corn and sugarcane derivatives. Yet, trade tensions and anti-dumping measures are altering the regional landscape. Countries like India, Thailand, and other Southeast Asian nations are ramping up production capacities to cater to both local and export demands. Japan's sophisticated pharmaceutical and food processing sectors present lucrative market prospects, while Australia's burgeoning beverage industry bolsters regional consumption.

The Middle East and Africa are the regions to watch, boasting a 6.56% CAGR through 2031. This growth is largely attributed to the burgeoning food processing sectors and infrastructural investments in nations such as Saudi Arabia and the UAE. Government initiatives in the region, aimed at bolstering food security and diversifying industries, are birthing new demand hubs for citric acid. NEOM's collaboration with Liberation Labs to set up precision fermentation facilities underscores the region's ambition in advanced biomanufacturing. Meanwhile, North America and Europe, with their entrenched food and pharmaceutical sectors, offer stable demand, albeit with tempered growth rates due to market saturation and regulatory consistency.

Europe, with its robust demand from the food, beverage, and personal care sectors, remains a stable player, bolstered by stringent quality standards and established processing facilities. North America's growth is steady, driven by a surge in ready-to-drink beverages, convenience foods, and pharmaceuticals. Consumers here increasingly lean towards clean-label ingredients, using citric acid as a natural preservative and flavor enhancer. South America, particularly in nations like Brazil and Argentina, is on the rise, thanks to its expanding food processing sectors and a growing appetite for packaged foods. South American manufacturers enjoy the dual advantage of abundant agricultural feedstocks for citric acid production and a reduced reliance on imports. Across Europe, North America, and South America, regulatory frameworks that favor natural additives further enhance citric acid's market potential, presenting opportunities for both global giants and local players.

Competitive Landscape

The citric acid market is moderately consolidated, with a few dominant multinational players, including Cargill Incorporated, Shandong Ensign Industry Co., Ltd., Jungbunzlauer Suisse AG, COFCO Corporation, and RZBC Group Co., Ltd. These companies hold significant market shares due to their extensive production capacities and well-established global distribution networks. This market concentration enables these leaders to achieve economies of scale and exert strong bargaining power over both raw material suppliers and downstream buyers. However, the presence of numerous regional and niche manufacturers prevents the market from becoming fully consolidated. These smaller players effectively address localized demand by offering flexible pricing and customized solutions.

Competition in the market is further driven by advancements in bio-based production technologies and the increasing demand for citric acid across diverse applications, such as food preservation, pharmaceuticals, and personal care products. The competitive landscape reflects a balance between the dominance of global leaders and the adaptability of regional players, resulting in a moderately consolidated market structure. Emerging markets present significant growth opportunities, as local production capabilities often lag behind rising consumption levels. This import dependency creates a favorable environment for established players to expand through greenfield investments or strategic partnerships.

Technological advancements play a critical role in shaping the competitive dynamics of the market. Companies with expertise in advanced fermentation processes and process optimization are better positioned to gain a competitive edge. Additionally, the regulatory complexities associated with pharmaceutical applications create barriers to entry, favoring suppliers with the necessary certifications and robust quality management systems. While the market's moderate fragmentation allows niche players to compete effectively in specialized applications, achieving scale becomes increasingly important in commodity-grade segments, where pricing pressures are more pronounced.

Citric Acid Industry Leaders

Cargill, Incorporated

Shandong Ensign Industry Co. Ltd

COFCO Corporation

RZBC Group Co., Ltd.

Jungbunzlauer Suisse AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Brenntag Pharma has extended its partnership with Citribel for the distribution of citric acids and citrate pharma excipients, expanding beyond France, Spain, Germany, and Benelux to now include Israel, Turkey, and South Africa.

- June 2024: Tate & Lyle made a strategic acquisition of CP Kelco, a move centered on pectin and specialty hydrocolloids but with significant repercussions for the citric acid market. As a result, this acquisition bolsters Tate & Lyle's foothold in the realm of clean-label and natural ingredients.

- March 2024: Jungbunzlauer has started up Austria’s largest photovoltaic power station, a 56 MWp installation of over 84,000 modules on 40 hectares, generating more than 60 GWh of renewable electricity annually, enough to power about 16,000 households, and feeding directly into its production site’s private grid to minimize losses and save around 15,000 metric tons of CO₂ per year.

Global Citric Acid Market Report Scope

Citric acid is a weak organic acid naturally found in several citrus fruits, such as lemons, limes, etc.

The citric acid market is segmented by form, application, and geography. By form, the market is segmented into liquid and anhydrous. By application, it is segmented into food and beverage, pharmaceuticals, personal care, and other applications. The food and beverage segment is further sub-segmented into the bakery, confectionery, dairy drinks, and other foods and beverages. By geography, the market studied is segmented into North America, South America, Europe, Asia Pacific, the Middle East, and Africa.

For each segment, market sizing and forecasts have been conducted based on value (USD) and Volume (tons).

| Anhydrous |

| Liquid |

| Food and Beverages | Bakery |

| Confectionery | |

| Dairy | |

| Beverages | |

| Savory and Snacks | |

| Other Foods and Beverages | |

| Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Detergents and Household Cleaners | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| Form | Anhydrous | |

| Liquid | ||

| Application | Food and Beverages | Bakery |

| Confectionery | ||

| Dairy | ||

| Beverages | ||

| Savory and Snacks | ||

| Other Foods and Beverages | ||

| Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Detergents and Household Cleaners | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the citric acid market expected to be by 2031?

Forecasts indicate that the citric acid market will reach USD 4.81 billion by 2031, with a 4.12% CAGR from 2026 to 2031.

Which application category currently uses the most citric acid?

Food and beverages account for 49.74% of global demand thanks to clean-label reformulation across bakery, beverage, and dairy items.

Why are detergents a high-growth outlet for citric acid?

Phosphate bans in Europe and several U.S. states push cleaners toward biodegradable citrate builders, driving a 6.03% CAGR in detergent applications.

Which region is growing fastest for citric acid consumption?

The Middle East and Africa are projected to expand at a 6.56% CAGR through 2031 as local beverage and confectionery capacity scales up.

Page last updated on: