Microcontroller (MCU) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 38.34 Billion |

| Market Size (2031) | USD 62.74 Billion |

| Growth Rate (2026 - 2031) | 10.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microcontroller (MCU) Market Analysis by Mordor Intelligence

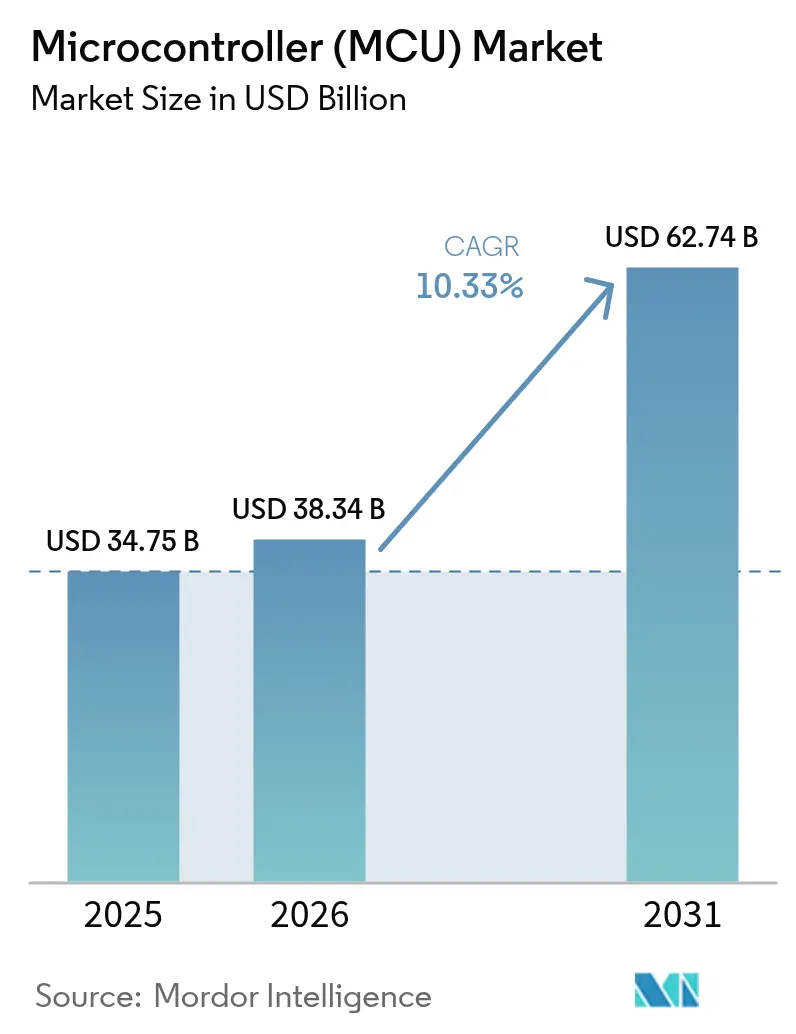

The Microcontroller market size was valued at USD 34.75 billion in 2025 and estimated to grow from USD 38.34 billion in 2026 to reach USD 62.74 billion by 2031, at a CAGR of 10.33% during the forecast period (2026-2031). This trajectory reflects the rising demand for embedded intelligence across electrified vehicles, Internet of Things (IoT) endpoints, and next-generation consumer devices. Content per car is increasing as functional-safety mandates expand MCU counts, while predictive-maintenance programs in factories accelerate the rollout of smart sensors. Open instruction-set architectures reduce licensing costs, helping smaller vendors address edge-AI workloads. Meanwhile, regional near-shoring and supply-chain diversification stimulate fresh capacity investments even as average selling prices (ASP) remain under pressure.

Key Report Takeaways

- By application, automotive electronic control units led the microcontroller market with a 30.42% share in 2025; industrial IoT sensors are expected to advance at a 11.12% CAGR through 2031.

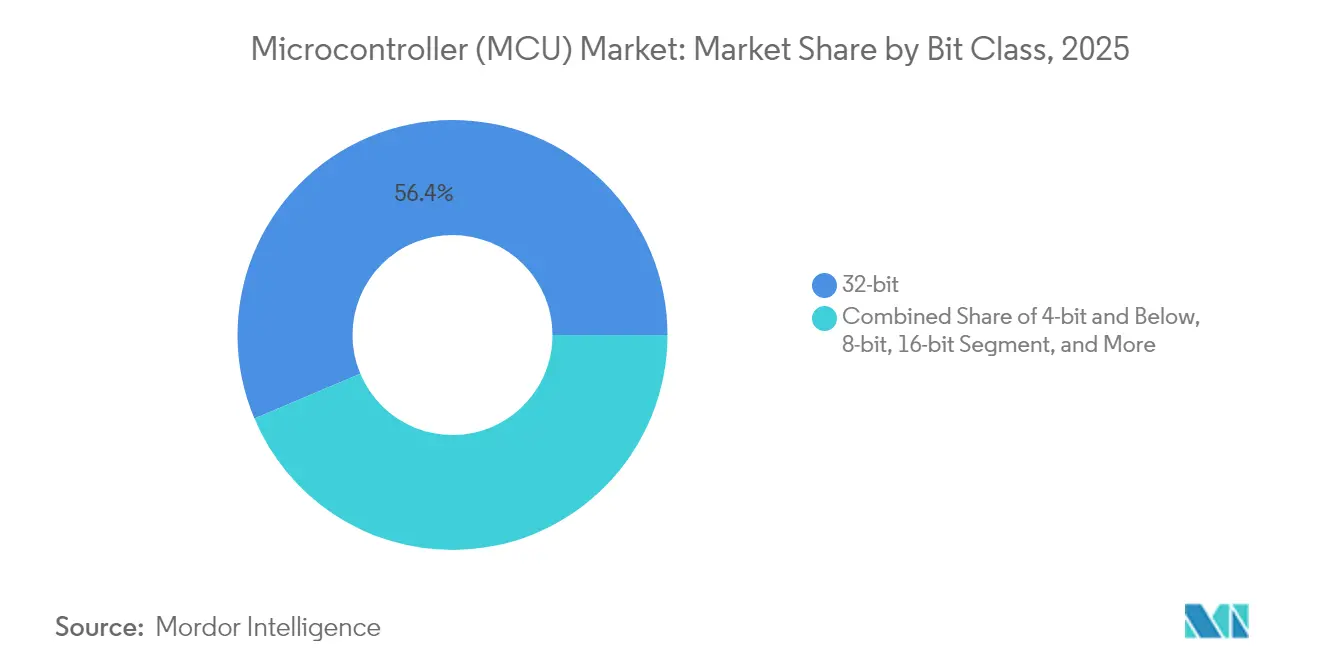

- By bit class, 32-bit devices commanded a 56.35% share of the Microcontroller market size in 2025.

- By core architecture, ARM Cortex-M retained 68.25% share in 2025, while RISC-V is expanding at a 15.09% CAGR through 2031.

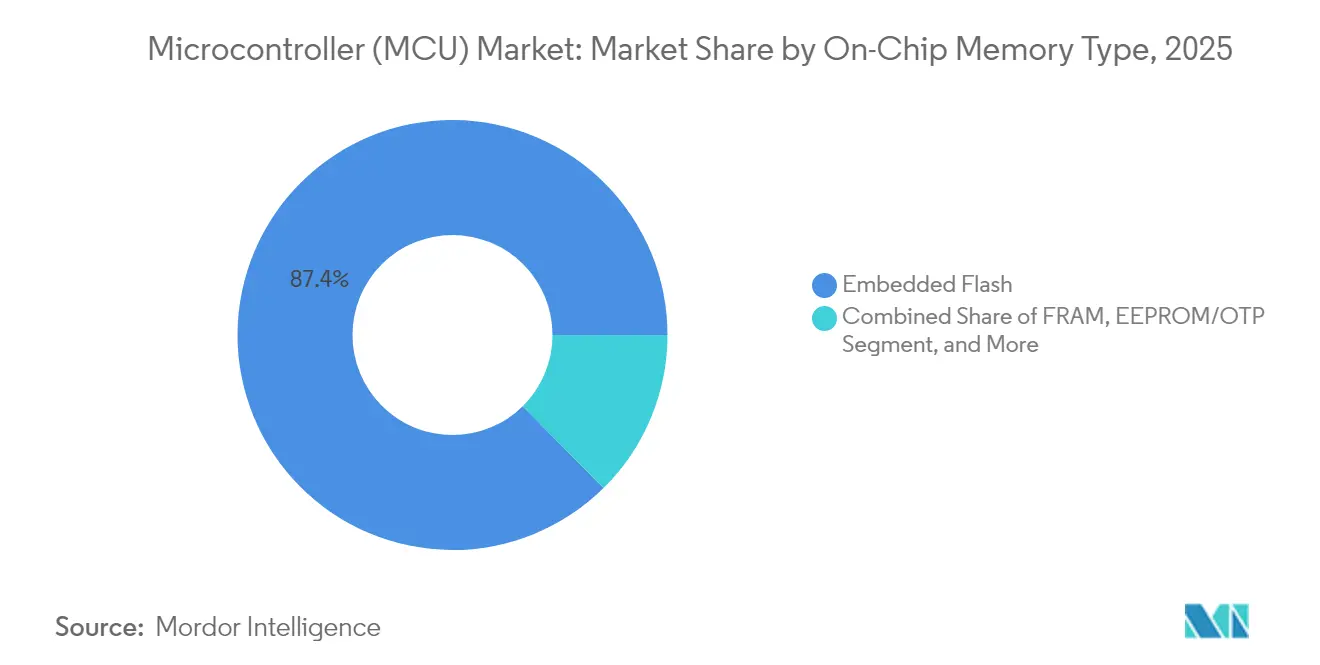

- By 2025, on-chip memory, specifically embedded flash, captured 87.40% of the Microcontroller market size; FRAM is growing at a 12.07% CAGR.

- By geography, APAC accounted for 47.30% of the revenue in 2025; South America is projected to grow at a 10.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microcontroller (MCU) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IoT node proliferation | +2.8% | Global, APAC leadership | Medium term (2-4 years) |

| Automotive electrification and ADAS | +2.1% | North America and EU, China EV expansion | Long term (≥ 4 years) |

| Smart-home and appliance MCU integration | +1.6% | North America and EU, accelerating APAC adoption | Medium term (2-4 years) |

| Shift to RISC-V open ISA | +1.4% | Global, led by China and India | Long term (≥ 4 years) |

| Ultra-low-power edge-AI MCUs | +1.2% | Global, early automotive and industrial | Medium term (2-4 years) |

| Industrial cybersecurity mandates | +0.9% | EU, North America, critical infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

IoT Node Proliferation Drives Embedded Intelligence Demand

Connected endpoints are projected to exceed 20 billion units by 2030, forcing manufacturers to embed multi-protocol radios and efficient processors into cost-sensitive designs. Nordic Semiconductor’s nRF54 series combines Bluetooth LE 5.4, Thread, and Matter in a single device, while maintaining a battery-friendly current draw, thereby reducing the bill of materials and firmware complexity [1]Source: Nordic Semiconductor, “Nordic Semiconductor to Launch First Products in Class-Leading nRF54 Series,” nordicsemi.com. Premium-priced analytics services, enabled by richer local processing, shift revenue models away from pure hardware sales. Semiconductor suppliers, such as Synaptics, are repositioning their portfolios toward IoT-optimized solutions rather than pursuing general-purpose computing.

Automotive Electrification and ADAS Integration Accelerate MCU Content Growth

A battery-electric vehicle can host up to 3,000 semiconductor components, quadrupling the MCU footprint versus internal-combustion models. Mercedes-Benz relies on discrete microcontroller clusters to manage the battery, thermal, and regenerative braking systems in accordance with ISO 26262. Continental’s cooperation with NXP centralizes multiple chassis functions into software-upgradable domain controllers, cutting wiring weight and enabling seamless over-the-air updates. EU regulations mandating the deployment of advanced driver-assistance systems across all classes by 2026 further amplify this shift. Honda’s partnership with Renesas to co-develop 2,000 TOPS SoCs highlights how computational demands are reshaping the Microcontroller market.

Smart-Home and Appliance MCU Integration Transforms Consumer Electronics

Open-standard Matter firmware allows white-goods firms to serve Apple Home, Google Home, and Amazon Alexa with a single hardware platform. STMicroelectronics’ ready-made Matter code examples accelerate compliance testing [2]Source: STMicroelectronics, “Connectivity: Matter Develop and Prototype,” stmicroelectronics.com. Cascoda’s SMARTRange radio doubles indoor range without raising power budgets, solving multi-story connectivity gaps [3]Source: Thread Group, “Case Studies,” threadgroup.org. Case studies demonstrate that IoT-enabled appliances can reduce household energy consumption by 27%, prompting retailers to favor models with this technology. u-blox’s MAYA-W2 module integrates Wi-Fi 6, Bluetooth LE, and Thread into a single, certified package, reducing product cycles for mid-tier brands [4]Source: u-blox, “Selecting the Right Hardware for Smart Home Solutions,” u-blox.com .

Shift to RISC-V Open ISA Disrupts Traditional Licensing Models

Royalty-free cores help emerging economies localize chip supply. Government-funded programs in China and India subsidize RISC-V tool-chain training, easing entry barriers for fabless startups. Renesas is diverting resources from SiC to open-ISA microcontrollers, signaling that even incumbents see sustainability in customized extensions over blanket license fees. Tailored instruction sets enable automotive suppliers to add hardware redundancy for ASIL-D compliance, while IoT designers integrate neural-network accelerators onto the same base architecture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain cyclicality | -1.8% | Global, APAC manufacturing concentration | Short term (≤ 2 years) |

| ASP erosion from Chinese fabs | -1.4% | Global, mature-node pricing pressure | Medium term (2-4 years) |

| Rising NRE for sub-28 nm embedded flash | -0.7% | Advanced-node applications | Long term (≥ 4 years) |

| Talent shortage in mixed-signal design | -0.6% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Cyclicality Creates Inventory and Pricing Volatility

Foundry scheduling swings expose MCU vendors to abrupt wafer-allocation shifts. Recent inventory digestion phases forced Nordic Semiconductor to cut 8% of its workforce after revenue fell 30% in 2023 [5]Source: Nordic Semiconductor, “Annual Report 2023,” nordicsemi.com . The oversupply of metal-silicon pulled benchmark spot prices down 2.3% to USD 2.95/kg in April 2025, yet tariffs threaten to reverse the cost gains [6]Source: Wafer World, “Falling Silicon Prices: Why Are They Going Down—and Will It Last?” waferworld.com. The concentration of mature-node capacity in Taiwan, mainland China, and South Korea magnifies geopolitical risk premiums, prompting OEMs to fund buffer stocks that tie up working capital.

ASP Erosion from Chinese Fabs Intensifies Pricing Competition

Aggressive 10-15% price cuts at domestic foundries squeeze incumbents in 8-bit and 16-bit lanes where differentiation is thin. The “China shock” forces players like GlobalFoundries to chase volume in automotive and telecom while accepting margin compression. Persistent headwinds risk diverting R&D budgets away from next-generation edge AI microcontrollers, potentially delaying the market-wide adoption of safety-critical features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bit Class: Rising Performance Needs Sustain 32-Bit Leadership

In 2025, 32-bit devices captured 56.35% of the Microcontroller market share, illustrating a decisive tilt toward complex workloads. The segment is projected to grow at an 8.76% CAGR, driven by ADAS sensor fusion, industrial drive control, and voice-enabled consumer gadgets. 32-bit architectures enable larger addressable memory and integrate digital-signal-processing extensions, thereby reducing the need for external components. MCU designers now embed neural engines and cybersecurity accelerators directly on the die, eliminating the need for discrete coprocessors. Lower-cost 8-bit and 16-bit parts remain viable in interface logic, while sub-4-bit variants linger in remote controls and thermostats serving ultra-thin margin categories.

Developers are increasingly requesting single-chip prototypes that incorporate secure boot, CAN-FD, and multi-protocol radio in a single package. This all-in-one trend supports platform reuse across product lines, reducing firmware maintenance. Meanwhile, integrated FRAM options on 32-bit units provide instant-write capability without charge-pump overhead, which is critical for data-logging sensors that operate in high-vibration environments.

By Core Architecture: ARM Ecosystem Strength Meets RISC-V Momentum

Cortex-M cores supplied 68.25% of shipments in 2025, bolstered by mature toolchains and robust middleware stacks. Customers value out-of-the-box RTOS support and expansive community libraries that shorten debug cycles. Yet RISC-V’s 15.09% CAGR points to mounting enthusiasm for instruction-set customization at zero royalty cost. Governments deploy domestic RISC-V programs to safeguard technology sovereignty, funneling subsidies toward open-ISA chiplets spanning wearables to automotive gateway nodes. Proprietary cores persist in niche avionics and industrial drives that require deterministic, cycle-accurate responses, whereas x86 processors are used in server-class board management controllers.

For the Microcontroller market, vendor success hinges on the richness of the development environment. ARM continues to extend TrustZone, PSA-Certified security, and M-Profile Vector Extensions, whereas RISC-V groups invest in unified software-layer harmonization to stave off fragmentation. Some suppliers hedge bets by offering pin-compatible ARM or RISC-V alternatives within the same product family.

By On-Chip Memory Type: FRAM Challenges Flash Supremacy

Embedded flash accounted for 87.40% of the Microcontroller market size in 2025, thanks to decades of process maturity and cost efficiency. Nevertheless, FRAM’s 12.07% expansion pace demonstrates rising preference for instant-write endurance in edge-AI logging. Industrial robotics relies on constant state snapshots to comply with safety integrity level ratings; FRAM ensures data retention during brownouts. Suppliers are exploring 3D NOR and MRAM for higher densities without charge-trap issues, although price parity with planar flash has not yet been achieved. EEPROM and OTP retain roles in secure-key storage and calibration trimming, while SRAM-only parts reside in minimal-footprint devices tethered to external code flash.

By Application: Industrial IoT Sensors Outpace Legacy Segments

Automotive ECUs accounted for 30.42% of revenue in 2025, driven by electrification and ADAS. Yet, industrial IoT sensors are expected to lead the fastest growth at an 11.12% CAGR through 2031, as factories retrofit predictive-maintenance nodes to reduce unplanned downtime. Edge-AI-ready MCUs enable local vibration, acoustic, and thermal analytics, reducing cloud bandwidth requirements. Consumer electronics, ranging from wearables to AR glasses, benefit from reduced standby currents and integrated radio subsystems that extend battery life. Healthcare designers adopt ultra-low-leakage architectures for implantable devices that must pass stringent FDA durability testing, while aerospace and defense engineers specify radiation-hardened variants with guarded supply chains. Cloud-server BMCs complete the mix, adding secure out-of-band management to hyperscale racks.

Geography Analysis

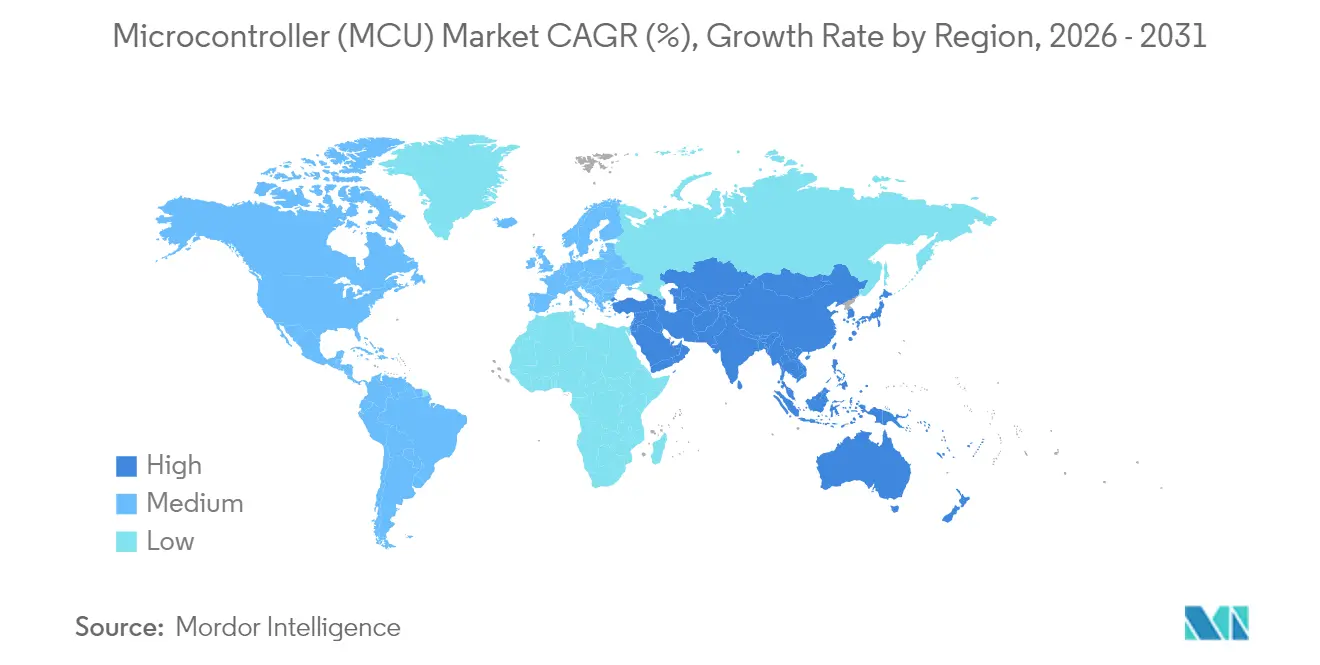

APAC retained 47.30% of global revenue in 2025 on the strength of China’s consumer-electronics assembly ecosystem and Japan’s automotive semiconductor depth. Chinese five-year plans targeting local silicon autonomy create pull for domestic MCU tape-outs across home appliances and public-charging infrastructure. Japanese suppliers maintain traction with powertrain-qualified microcontrollers specifically designed for hybrid drive cycles, leveraging their long-standing OEM ties. South Korean conglomerates integrate native memory IP with logic blocks to build one-chip solutions for smartphones and smart TVs. Rising labor, energy, and geopolitical costs prompt some diversification into Vietnam and Thailand, yet the region’s cohesive component ecosystem preserves its comparative advantage, keeping it as the fastest-growing market for microcontrollers.

South America emerges as one of the fastest-growing regions in the microcontroller market, with a 10.22% CAGR from 2020 to 2031. Brazil’s renewed automotive-production incentives and Mexico’s USMCA-enabled export corridors lure EV platform assembly that requires localized MCU sourcing. Government-directed renewable energy grids are driving the rollout of smart meters, which in turn boosts demand for secure, low-power 32-bit controllers. Local-content mandates spur joint ventures between global silicon vendors and regional design houses, catalyzing the development of talent around embedded software stacks. North America centers on high-value safety-critical niches. The CHIPS Act earmarks billions for wafer-fab construction, though most capacity targets sub-10 nm nodes rather than mature MCU geometries. Defense contractors stipulate onshore production and supply-chain attestations, ensuring steady demand for ITAR-compliant parts. Europe focuses on adhering to ISO 26262 and IEC 62443 within the automotive and process automation verticals. TSMC’s planned Dresden fab will supply 40,000 300 mm wafers monthly to European Tier-1s, shortening lead times for high-reliability microcontrollers .

Competitive Landscape

The Microcontroller industry is moderately fragmented. Infineon, NXP, and STMicroelectronics lead the way with multi-domain portfolios that bundle processors, power management, and connectivity. Their platform strategies emphasize common software, driving economies of scale and time-to-market advantages. Renesas’ AUD 9.1 billion acquisition of Altium adds a board-design toolchain, creating an end-to-end ecosystem from schematic to compiled firmware. Patent filings increased by 22% in 2024; Samsung alone filed 10,000, underscoring the intensifying intellectual property rivalry.

Niche innovators such as Ambiq Micro and Nordic Semiconductor gain share by specializing in sub-200 nA sleep currents and advanced radio stacks, respectively. Open-ISA specialists target cost-sensitive deployments with differential advantages in configurability and licensing. Automotive networking consolidation continues: Infineon has acquired Marvell’s automotive Ethernet assets for USD 2.5 billion, aiming to supply complete zonal architecture chipsets. Strategic collaborations dominate go-to-market moves, for example, Texas Instruments teaming with Delta Electronics on high-efficiency onboard chargers for EVs. Customers value suppliers who offer long-term supply guarantees, robust functional safety collateral, and in-house security certifications.

Microcontroller (MCU) Industry Leaders

Infineon Technologies AG

Microchip Technology Inc.

NXP Semiconductors N.V.

STMicroelectronics N.V.

Texas Instruments Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: TI has unveiled the world's smallest microcontroller (MCU), tailored for compact applications like medical wearables and personal electronics. This new MCU is 38% smaller than the industry's previous smallest offering, allowing designers to conserve board space without sacrificing performance. This latest MCU broadens TI's MSPM0 portfolio, which aims to improve sensing and control in embedded systems while reducing cost, complexity, and design time.

- March 2025: Infineon Technologies AG is set to embrace RISC-V technology in the automotive sector. In the coming years, the company plans to introduce a new family of automotive microcontrollers rooted in RISC-V. This upcoming lineup will be integrated into Infineon's well-known AURIX™ brand of automotive microcontrollers. This move will broaden Infineon's current portfolio, which includes microcontrollers based on TriCore™ and Arm® technologies.

- March 2025: STMicroelectronics unveiled its STM32U3 microcontrollers, pushing the boundaries of ultra-low power technology for a range of applications, from remote monitoring to smart utilities and sustainable solutions. These new microcontrollers harness advanced near-threshold chip design, achieving an unprecedented performance-per-watt efficiency. Enhanced cybersecurity features, such as secret-key protection and in-factory provisioning, fortify the devices. Common applications span utility meters, healthcare equipment, and industrial sensors.

- February 2025: Renesas Electronics Corporation unveiled the RA4L1 microcontroller (MCU) group, introducing 14 new devices that boast ultra-low power consumption, enhanced security features, and compatibility with segment LCDs. Leveraging an 80-MHz Arm Cortex-M33 processor equipped with TrustZone support, these new MCUs offer an unparalleled blend of performance, features, and energy efficiency. This empowers designers to cater to diverse applications, from water meters and smart locks to IoT sensors and beyond.

Global Microcontroller (MCU) Market Report Scope

A microcontroller, often referred to as a compact computer, is embedded within a single VLSI integrated circuit (IC) chip. It encompasses one or more CPUs (processor cores), memory, and programmable input/output peripherals. In today's world, these components play a pivotal role in IoT-driven and sensor-based instruments.

The microcontroller (MCU) market is segmented by type (8-bit, 16-bit, and 32-bit), application (defense and aerospace, consumer electronics and home appliances, automotive, industrial, healthcare, data processing, and communication, and other applications), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The report offers market size and forecasts for all the above segments in value (USD).

| 4-bit and below |

| 8-bit |

| 16-bit |

| 32-bit |

| ARM Cortex-M |

| RISC-V |

| x86 |

| Proprietary / Others |

| Embedded Flash |

| FRAM |

| EEPROM/OTP |

| SRAM-only (code-in-RAM) |

| Automotive |

| Consumer Electronics and Home Appliances |

| Industrial and Factory Automation |

| Healthcare |

| Aerospace and Defense |

| Data-Com and Cloud Infrastructure |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Taiwan | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Bit Class | 4-bit and below | |

| 8-bit | ||

| 16-bit | ||

| 32-bit | ||

| By Core Architecture | ARM Cortex-M | |

| RISC-V | ||

| x86 | ||

| Proprietary / Others | ||

| By On-Chip Memory Type | Embedded Flash | |

| FRAM | ||

| EEPROM/OTP | ||

| SRAM-only (code-in-RAM) | ||

| By Application | Automotive | |

| Consumer Electronics and Home Appliances | ||

| Industrial and Factory Automation | ||

| Healthcare | ||

| Aerospace and Defense | ||

| Data-Com and Cloud Infrastructure | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Taiwan | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the Microcontroller market be by 2031?

Forecasts place the market at USD 62.74 billion in 2031, growing at a 10.33% CAGR from 2026.

Which Microcontroller bit class sees the greatest growth?

32-bit devices expand at an 8.76% CAGR on sustained demand for edge-AI and ADAS processing.

Why is South America the fastest-growing geography?

Vehicle-assembly near-shoring and renewable-energy projects lift microcontroller demand, delivering a 10.22% CAGR through 2031.

What drives RISC-V adoption in embedded systems?

Royalty-free licensing and government sovereignty initiatives push RISC-V microcontrollers to a 15.09% CAGR.

Which connectivity option grows fastest in embedded designs?

Wi-Fi-integrated MCUs advance at a significant CAGR as Matter adoption raises bandwidth needs across smart-home products.

How are suppliers addressing rising cybersecurity mandates?

Vendors integrate secure boot, hardware key storage and IEC 62443-certified reference designs to meet industrial and automotive compliance requirements.

Page last updated on: