North America Automotive Fastener Cold Forming Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

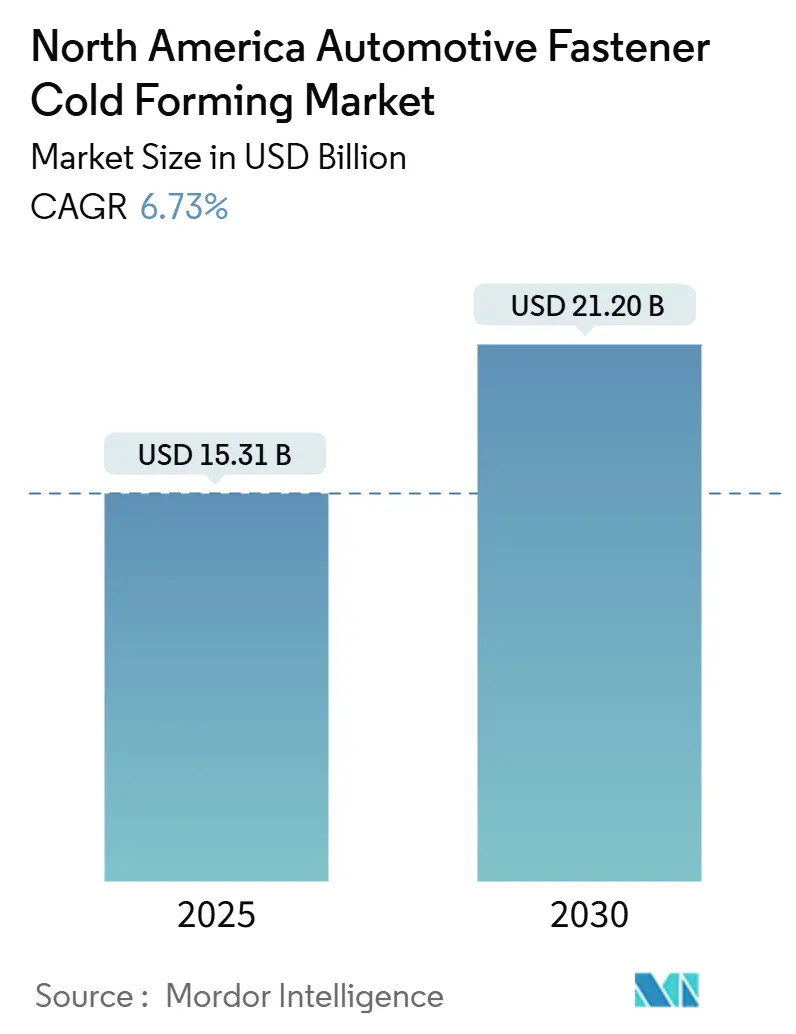

| Market Size (2025) | USD 15.31 Billion |

| Market Size (2030) | USD 21.20 Billion |

| Growth Rate (2025 - 2030) | 6.73% CAGR |

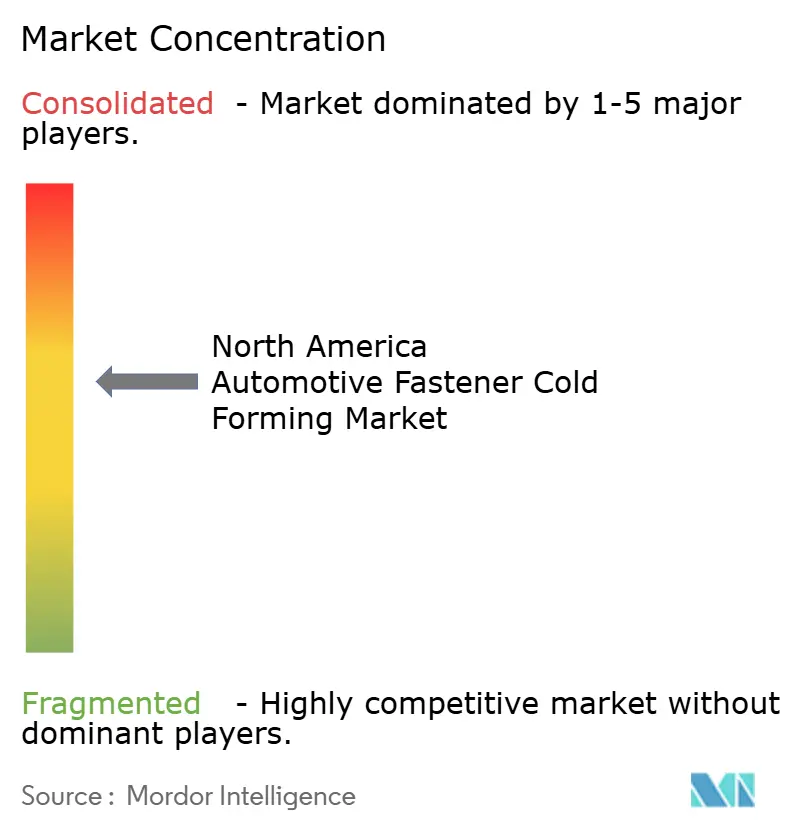

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automotive Fastener Cold Forming Market Analysis by Mordor Intelligence

The North America automotive fastener cold forming market size stood at USD 15.31 billion in 2025 and is forecast to reach USD 21.20 billion by 2030, reflecting a 6.73% CAGR from 2025 to 2030. Strong replacement demand from chassis and power-train production, rapid electrification, and strict regional-content rules are shaping volume growth while encouraging on-shoring of capacity. Lightweight aluminum and magnesium fasteners are gaining share as OEMs accelerate mixed-material vehicle architectures, even as steel retains widespread use for high-load joints. Tax incentives for new cold-heading lines, the build-out of battery gigafactories, and AI-driven defect-reduction programs are lowering unit costs and widening gross margins. Conversely, margin pressure from CHQ wire-rod volatility and a widening skills gap in precision cold forming continue to temper the upward trajectory of the North America automotive fastener cold forming market.

Key Report Takeaways

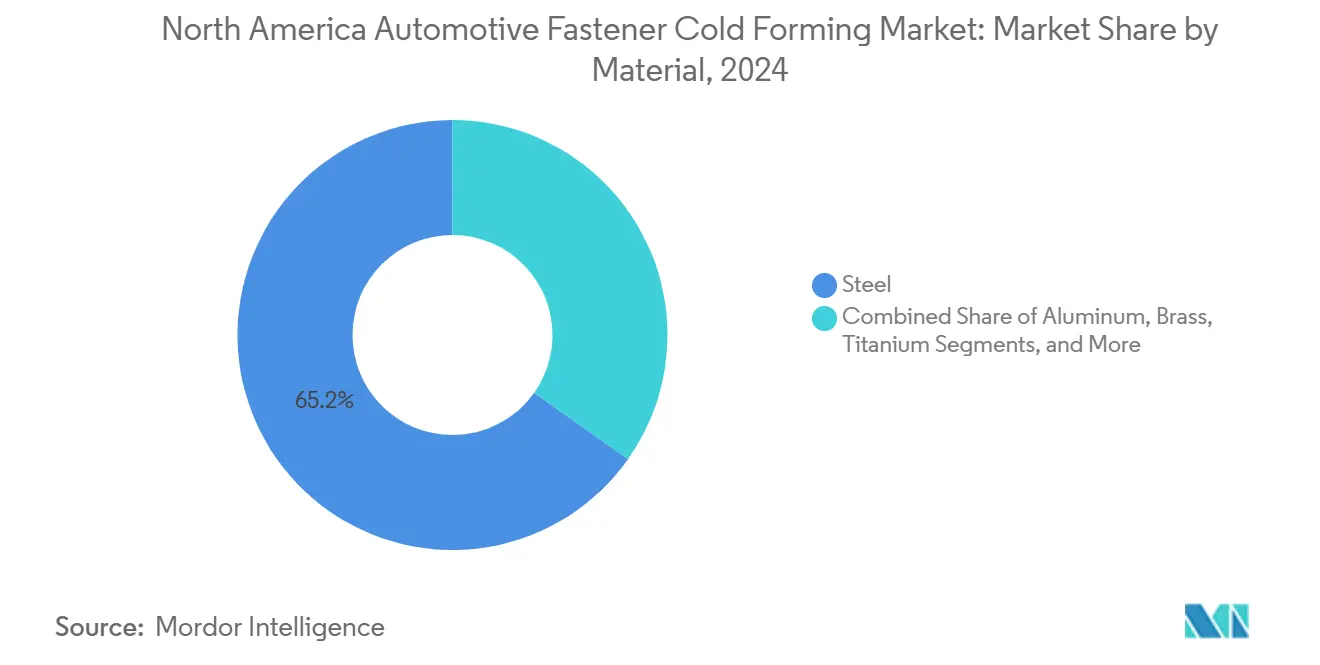

- By material, steel held 65.18% of the North America automotive fastener cold forming market share in 2024; aluminum is projected to expand at a 7.89% CAGR through 2030.

- By fastener type, bolts accounted for 39.25% of 2024 revenue, while rivets recorded the fastest projected CAGR at 6.98% to 2030.

- By application, chassis captured a 30.55% share in 2024, whereas electrical components are poised for an 8.65% CAGR through 2030.

- By distribution channel, OEM procurement commanded 86.33% of 2024 sales; the aftermarket is forecast to rise at a 7.49% CAGR to 2030.

- By end-user, automotive OEMs represented 53.24% of demand in 2024; fastener distributors and assemblers show the highest projected CAGR at 7.13% for 2025-2030.

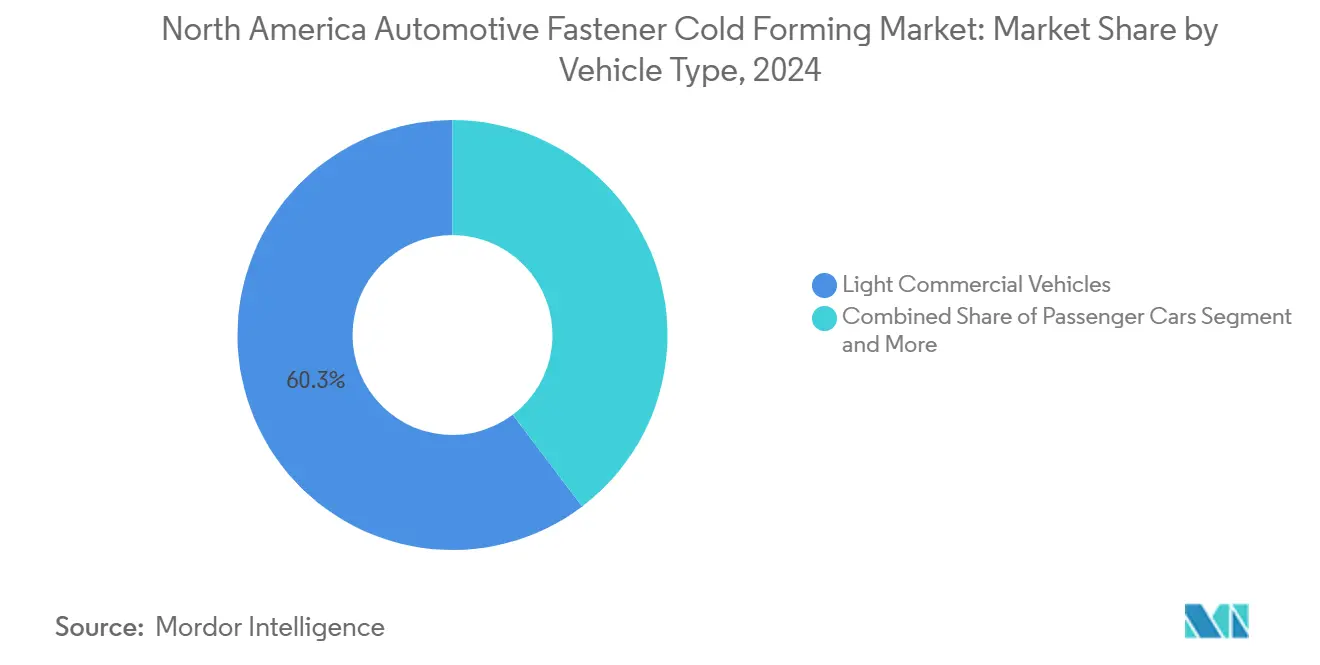

- By vehicle type, light commercial vehicles led with 60.26% in 2024, while medium- and heavy-duty commercial vehicles are projected to advance at an 8.73% CAGR.

- By propulsion, internal-combustion vehicles retained 89.93% of 2024 sales; electric vehicles will post the fastest CAGR, 31.91%, through 2030.

- By country, the United States controlled 84.38% of the 2024 total; Mexico is projected to grow at a 7.21% CAGR, the fastest in the region.

North America Automotive Fastener Cold Forming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV Skateboard Chassis Adoption | +1.5% | United States, Ontario, Nuevo León | Medium term (2-4 years) |

| Lightweight Fasteners Drive Automotive Shifts | +1.2% | United States, Mexico, Canada | Medium term (2-4 years) |

| USMCA Boosts Regional Sourcing | +0.9% | North America | Short term (≤ 2 years) |

| Gigafactories Expand Tier-2 Capacity | +0.8% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Tax Credits Promote Cold Header Onshoring | +0.6% | United States, Canada | Short term (≤ 2 years) |

| AI Cuts Manufacturing Scrap Rates | +0.4% | North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid EV Skateboard Chassis Adoption

Skateboard architecture integrates battery packs into the primary load path, creating fresh use cases for structural blind fasteners, self-piercing rivets, and insulated bushings that accommodate dissimilar materials. Tesla repair manuals list multiple proprietary fastener categories—NeoBolts, AVBolts, bulb rivets—underscoring the specialized mix required in high-voltage enclosures [1]“Cybertruck Collision Repair Procedures,” Tesla, tesla.com. Suppliers leverage cold-heading to embed sensor ports and thermal-interface geometries directly into fastener heads, supporting real-time battery diagnostics.

OEM Push for Lightweight Al and Mg Cold-Formed Fasteners

Aluminum and magnesium fasteners have advanced from niche use to mainstream adoption as vehicle programs target aggressive curb-weight reduction without compromising joint strength. Electric vehicles consume roughly 30% more aluminum than legacy ICE models, driving demand for surface-treated Al fasteners that overcome oxide-layer challenges in battery assemblies. Cold-forming lines are being re-tooled with higher-capacity servo presses and refined lubrication chemistries to control work hardening, while anodizing and conversion-coating steps ensure corrosion resistance in mixed-metal joints. Magnesium fasteners, once reserved for racing, are gaining traction in gear housings and steering columns owing to lower density and superior machinability, further lifting value per vehicle.

USMCA Local-Content Rules Boosting Regional Sourcing

The 75% regional-value threshold and the 70% North American steel/aluminum requirement embedded in USMCA have accelerated near-shoring of fastener production. OEMs risk a 25% tariff on non-compliant vehicles, making localized sourcing mandatory rather than discretionary. U.S. and Canadian cold-forming plants benefit from labor-value rules that reward wages ≥ USD 16/hour, while Mexican producers invest in automation to offset wage gaps. Compliance auditing infrastructure has expanded quickly, and tiered suppliers now embed blockchain-based traceability in purchase orders to verify melt source, chemical certification, and part pedigree throughout the North America automotive fastener cold forming market [2]“USMCA Automotive Rules of Origin,” U.S. International Trade Commission, usitc.gov.

Gigafactory Build-Out Driving Adjacent Tier-2 Capacity

North America’s announced battery capacity is slated to surpass 1,200 GWh by 2030, and each new gigafactory triggers a halo of Tier-2 tooling and component plants within a one-day drive of assembly lines. Precision fasteners rated to ±20 µm are required for electrode stacking machines, module welding fixtures, and clean-room crane systems. Section 48C investment credits covering 30% of capital expenditures are pulling new cold-heading cells into Michigan, Tennessee, and Ontario, reinforcing structural growth in the North America automotive fastener cold forming market [3]“Battery Manufacturing Investment Tracker,” Argonne National Laboratory, anl.gov.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor Shortage in Precision Cold Forming | -1.1% | United States, Canada | Long term (≥ 4 years) |

| CHQ Steel Wire-rod Price Volatility | -0.8% | United States, Canada | Short term (≤ 2 years) |

| CO₂-compliance CAPEX Burden | -0.6% | California & CARB states | Medium term (2-4 years) |

| Adhesive Substitution for Selected Joints | -0.4% | Early EV programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortage in Precision Cold Forming

Roughly 2 million manufacturing positions could remain unfilled by 2033, with die-setup technicians and metallurgy specialists among the hardest to source. Cold-heading demands a blend of hands-on experience and advanced materials science that current vocational pipelines struggle to supply. Firms have responded with in-house academies, AR-guided work instructions, and tuition-sponsorship programs, yet retirements continue to outpace new entrants, creating a structural drag on expansion capacity.

CHQ Steel Wire-Rod Price Volatility

Raw-material spend accounts for 60-70% of COGS in a typical cold-forming plant, leaving profits highly sensitive to swings in melt allocation and rod pricing. Pandemic-era supply shocks, energy surcharges, and ongoing geopolitics have produced double-digit quarterly moves. Top-tier players hedge long-term contracts tied to scrap-metal indices, but smaller operators remain exposed, prompting further consolidation across the North America automotive fastener cold forming market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Steel Dominance, Aluminum Acceleration

Steel retained 65.18% of the North America automotive fastener cold forming market share in 2024, anchored by high-load chassis and power-train applications. Meanwhile, aluminum fasteners achieved the highest growth trajectory at a 7.89% CAGR as OEMs advance lightweight battery housings and thermal plates. Alloy-steel content inches upward within suspension joints that must withstand rising curb weights of electric vans. Stainless steel adoption rises in exhaust and appearance parts, though higher ingot cost caps volume. For every 10 kWh of battery capacity, aluminum fastener demand adds an incremental USD 32 bill-of-materials value, fueling sustained expansion of the North America automotive fastener cold forming market.

OEM mandates for recycled content and closed-loop scrap systems are altering procurement specs. Suppliers now guarantee 25% post-consumer recycled (PCR) steel and up to 70% recycled aluminum for select part numbers. Magnesium applications remain niche but are advancing in transfer-case covers and steering housings, where weight savings translate directly into range extension for electric pickup trucks.

By Fastener Type: Bolts Lead, Rivets Surge

Bolts generated 39.25% of 2024 revenue and continue to dominate engine-mount and frame-rail assemblies. However, self-piercing and structural blind rivets show the quickest uptake at a 6.98% CAGR as mixed-metal body-in-white programs substitute stamping welds with cold-formed fasteners. Integrated sealing glands and captive-washer head designs now roll straight off six-die headers, reducing secondary machining.

Thread-forming screws secure molded connectors and infotainment modules, while studs remain crucial for cylinder-head and exhaust-manifold joints. Washers, spacers, and specialized clip fasteners address NVH and thermal-expansion requirements in EV packs. These evolving designs reinforce demand diversity across the North America automotive fastener cold forming market.

By Application: Chassis Strength, Electrical Innovation

Chassis assemblies accounted for 30.55% of 2024 revenue as OEMs relied on grade 10.9 and 12.9 bolts for cross-member structures. Electrical components rise fastest, advancing at an 8.65% CAGR on the back of high-voltage busbar clips, sensor studs, and EMI-shielding rivets. Battery-tray covers require flush-head blind rivets that avoid intrusion into coolant channels, illustrating the premium placed on geometry control in cold formed blanks.

Engine and transmission segments remain important even as ICE volumes plateau; hybrid power-trains add new joint families for e-drive gearsets and inverter housings. Braking and steering systems adopt zinc-nickel coated steel fasteners to meet cyclic-corrosion tests in salt-sprayed urban environments, helping the North America automotive fastener cold forming market capture value in safety-critical hardware.

By Distribution Channel: OEM Keeps Scale, Aftermarket Gains Speed

OEM purchasing drove 86.33% of 2024 shipments through directed-buy contracts and VMI programs. Automated replenishment portals now exchange EDI signals every 30 minutes with Tier-1 sequencing centers, keeping days of inventory under five for high-volume part numbers. The aftermarket, though smaller in absolute terms, outpaces at 7.49% CAGR as vehicle parc ages and DIY e-commerce storefronts stock proprietary body-panel rivets and infotainment fasteners.

Digital twins of vehicle platforms streamline parts lookup, boosting attachment sales for collision repair shops. Meanwhile, full-service distributors differentiate via torque-audit consulting and kitting services that ship directly to technician workstations, shortening service-bay cycle time and lifting revenue per repair order inside the North America automotive fastener cold forming market.

By End-User: OEM Supremacy, Distributor Expansion

Direct consumption by vehicle manufacturers reached 53.24% in 2024, reflecting the tight integration of fastener engineering into platform launch calendars. Distributors and assemblers are the fastest-growing end users, projected at a 7.13% CAGR, as Tier-2 suppliers outsource kitting and small-batch pre-assembly of complex fastener sets. Outsourced VAVE (value-analysis/value-engineering) projects further shift demand toward service-rich intermediaries that maintain ISO 17025-accredited torque-test labs.

Tier-1 modules, from seat frames to camera housings, use vendor-supplied fasteners packed in sequence according to door-side, vehicle trim, and VIN variant. As modular vehicle platforms proliferate, end-user profiles diversify, further stabilizing volume flows across the North America automotive fastener cold forming market.

By Vehicle Type: Commercial Vehicles Pull Ahead

Light commercial vehicles generated 60.26% of 2024 revenue, buoyed by last-mile e-van rollouts. Medium and heavy trucks grow fastest at 8.73% CAGR as states mandate zero-emissions freight inside urban zones. Dual-motor electric class-6 chassis require roughly 23% more fasteners by weight than diesel equivalents because battery enclosures add mounting and cooling hardware.

Passenger cars, while declining in share, hold steady demand volume because integrated battery cases and aluminum subframes each introduce new joint families. Fleet electrification targets from parcel and beverage companies continue to elevate commercial-vehicle demand, securing long-term stability for the North America automotive fastener cold forming market.

By Propulsion: ICE Persistence, Electric Acceleration

Internal-combustion platforms represented 89.93% of 2024 shipments but will cede share as EV volumes surge at a 31.91% CAGR. Battery-integrated floor pans, high-current busbars, and inverter housings all rely on novel cold-formed parts with insulated coatings and captive O-ring grooves. Hybrid and plug-in hybrid models complicate joint design because they combine high-temperature exhaust zones and water-glycol cooled battery compartments within one architecture.

Fasteners rated for ISO 26262 functional safety now come with traceability codes and QR-engraved heads for automated torque-angle documentation, reinforcing the regulatory pull shaping the North America automotive fastener cold forming market.

Geography Analysis

The United States controlled 84.38% of 2024 demand, leveraging a dense concentration of OEM assembly lines in the Great Lakes and Southern corridors. Michigan hosts roughly one-third of regional fastener output thanks to legacy tool-and-die clusters, proximity to OEM engineering centers, and state-level incentive funds topping USD 1 billion for equipment grants. Section 45X credits further tilt capacity decisions toward the United States, providing production incentives on every qualified cold-formed component.

Canada maintains a stable position as an integrated supplier to U.S. assembly plants. Ontario’s automotive corridor benefits from the province’s low-carbon electricity grid, enabling OEMs to collect ESG credits for low-emission scope-3 inputs. Honda’s CAD 15 billion EV value-chain plan in Ontario will stimulate fastener volumes for battery-tray and motor-housing contracts, ensuring Canada remains integral to the North America automotive fastener cold forming market.

Mexico posts the fastest CAGR at 7.21%, driven by USD 2.5 billion in parts FDI during 2024 aimed at near-shoring EV sub-assemblies. Nuevo León and Chihuahua lead new plant announcements. Wage-adjusted productivity plus tariff-free access under USMCA is compelling European and Asian suppliers to anchor cold-heading lines south of the border, while U.S. and Canadian buyers increasingly dual-source to hedge labor disruptions. Modern industrial parks with built-in natural-gas and renewable power connections are lowering set-up time to as little as 13 months for greenfield cold-forming sites, strengthening Mexico’s position inside the North America automotive fastener cold forming market.

Competitive Landscape

The marketplace remains moderately fragmented. Stanley Engineered Fastening embeds parts in 90% of light vehicles sold in North America and Europe, turning out 23 billion pieces annually from a global network of 100+ facilities. Illinois Tool Works, Acument, and LISI leverage proprietary thread-forming geometries and captive coating lines to secure multi-year platform awards.

Strategic themes focus on vertical integration—from wire-drawing to surface treatment—to lock in metallurgy consistency and cycle-time control. Suppliers increasingly deliver complete fastening systems bundled with fixturing, torque tools, and data analytics dashboards, tightening switching costs at OEM plants. EV-specific product lines—copper-alloy battery-barrel nuts, aluminum blind rivets with dielectric sleeves, and hybrid composite studs—represent high-margin white spaces across the North America automotive fastener cold forming market.

Adhesive and structural-bonding competitors loom as technology disruptors, especially in battery decks where stress distribution favors chem-bond lines. Fastener incumbents respond with combination approaches: stud-weld plus adhesive assist or rivet-bond hybrids that meet crash-energy-absorption specs. M&A activity centers on regional machining shops with deep draw expertise, a trend underscored by PennEngineering’s 2024 purchase of Sherex to broaden rivet-nut portfolios.

North America Automotive Fastener Cold Forming Industry Leaders

Stanley Engineered Fastening

Illinois Tool Works (ITW)

Fontana Gruppo

LISI Automotive

Würth Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: PennEngineering acquired Sherex Fastening Solutions, enhancing its rivet-nut design and installation capabilities for automotive body-in-white and battery enclosures.

- December 2023: Norm Fasteners unveiled a USD 77 million plan for a 365,000-square-foot cold-forming plant in Bath Township, Michigan, scheduled for phased start-up through 2026.

North America Automotive Fastener Cold Forming Market Report Scope

| Steel | Carbon Steel |

| Alloy Steel | |

| Stainless Steel | |

| Aluminum | |

| Brass | |

| Titanium | |

| Plastic/Polymer Composites |

| Bolts |

| Screws |

| Nuts |

| Rivets |

| Studs |

| Washers and Others |

| Engine Assembly |

| Transmission Systems |

| Chassis |

| Powertrain |

| Suspension System |

| Body Interior/Exterior |

| Brake System |

| Steering System |

| Electrical Components |

| OEM |

| Aftermarket |

| Automotive OEMs |

| Tier-1 Suppliers |

| Fastener Distributors and Assemblers |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy-duty Commercial Vehicles |

| Internal Combustion Engine (ICE) |

| Electric |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Material | Steel | Carbon Steel |

| Alloy Steel | ||

| Stainless Steel | ||

| Aluminum | ||

| Brass | ||

| Titanium | ||

| Plastic/Polymer Composites | ||

| By Fastener Type | Bolts | |

| Screws | ||

| Nuts | ||

| Rivets | ||

| Studs | ||

| Washers and Others | ||

| By Application (Vehicle Sub-system) | Engine Assembly | |

| Transmission Systems | ||

| Chassis | ||

| Powertrain | ||

| Suspension System | ||

| Body Interior/Exterior | ||

| Brake System | ||

| Steering System | ||

| Electrical Components | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By End-User | Automotive OEMs | |

| Tier-1 Suppliers | ||

| Fastener Distributors and Assemblers | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy-duty Commercial Vehicles | ||

| By Propulsion | Internal Combustion Engine (ICE) | |

| Electric | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America |

Key Questions Answered in the Report

What is the current value of the North America automotive fastener cold forming market?

The market is valued at USD 15.31 billion in 2025.

How fast is demand for aluminum fasteners growing?

Aluminum fastener revenue is projected to rise at a 7.89% CAGR between 2025 and 2030.

Which fastener type is expanding the quickest?

Rivets lead growth with a forecast 6.98% CAGR through 2030, driven by mixed-material body construction.

Why is Mexico gaining share in regional supply?

Near-shoring under USMCA and USD 2.5 billion of 2024 FDI are lifting Mexican cold-forming capacity at a 7.21% CAGR.

Page last updated on: