Automotive Plastic Fasteners Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.96 Billion |

| Market Size (2030) | USD 5.04 Billion |

| Growth Rate (2025 - 2030) | 4.93% CAGR |

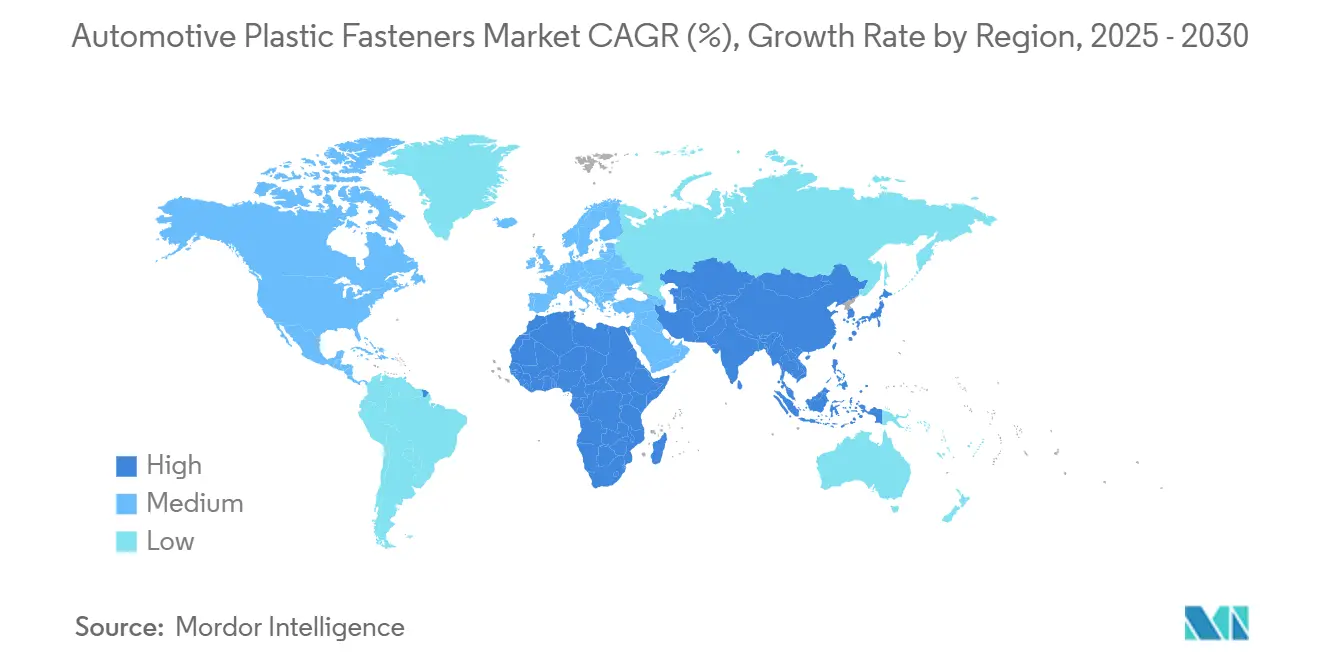

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Plastic Fasteners Market Analysis by Mordor Intelligence

The Automotive plastic fasteners market size stood at USD 3.96 billion in 2025 and is forecast to reach USD 5.04 billion by 2030, reflecting a 4.93% CAGR over the period. Lightweighting mandates, electrification needs, and the shift toward non-conductive components underpin this outlook, as agencies such as the EPA and NHTSA tighten fuel-economy rules that penalize excess vehicle mass. Automakers increasingly select engineered polymers to avoid galvanic corrosion, simplify mixed-material joints, and streamline automated assembly lines. Suppliers accelerate innovation around snap-fit geometries, mono-material recyclability, and vibration-damping properties to satisfy circular-economy and acoustic performance specifications. Price volatility in polypropylene and nylon remains a near-term headwind, yet robust production growth in Asia-Pacific, rising electric-vehicle (EV) volumes, and expanding ADAS content continue to widen revenue opportunities across passenger- and commercial-vehicle programs.

Key Report Takeaways

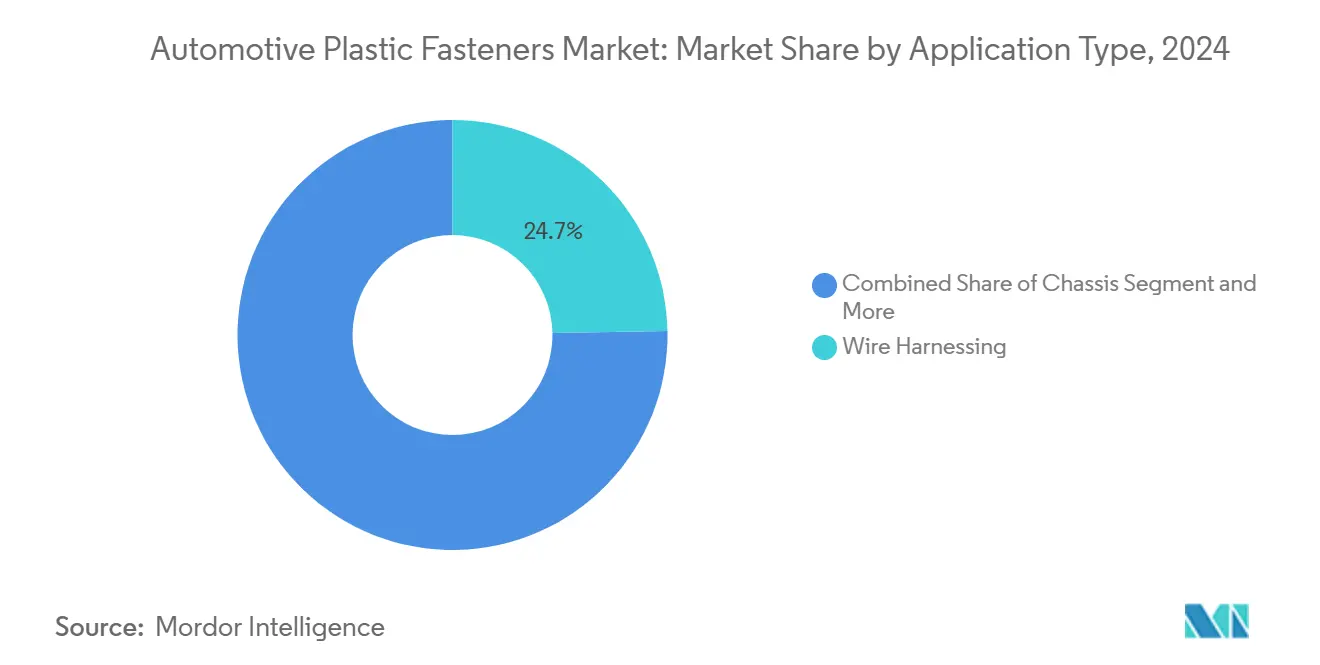

- By application type, wire harnessing led with 24.73% of the Automotive plastic fasteners market share in 2024, whereas electronics is projected to post the fastest 11.34% CAGR through 2030.

- By vehicle type, passenger vehicles accounted for 78.29% of the 2024 Automotive plastic fasteners market size, while the EV subset is advancing at a 9.52% CAGR to 2030.

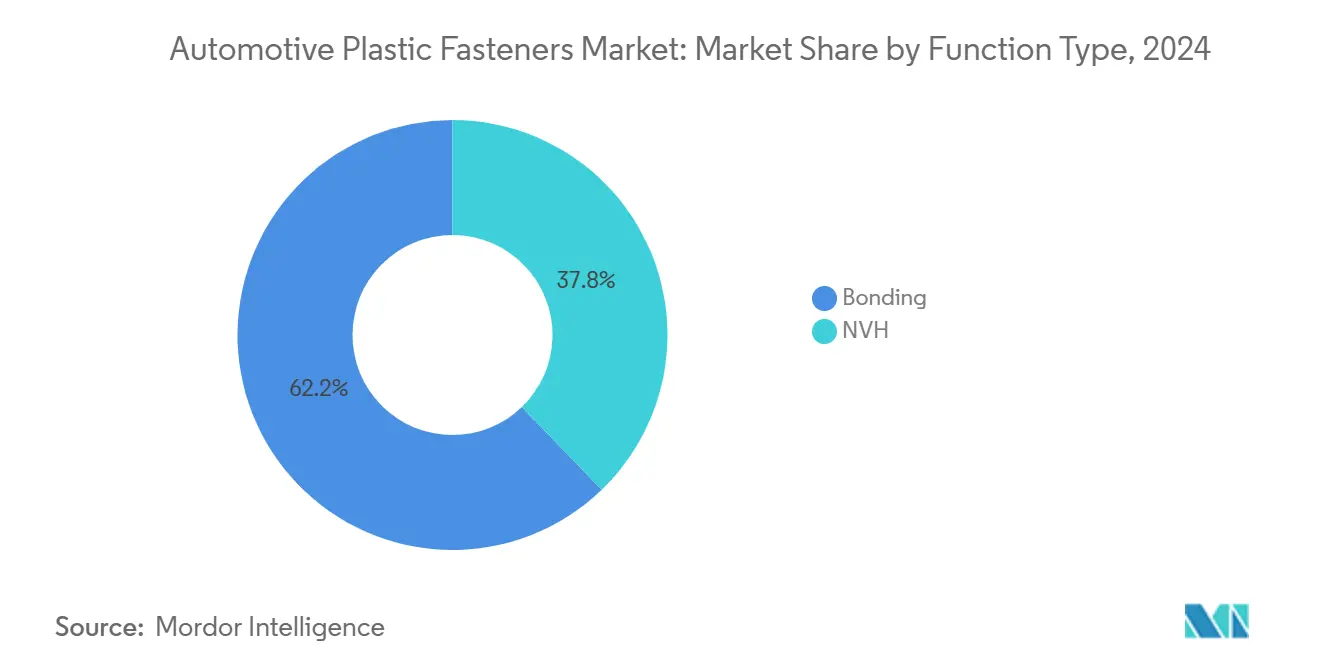

- By function type, bonding dominated with a 62.18% share in 2024, yet NVH applications are forecast to grow at a 10.87% CAGR through 2030.

- By characteristics, permanent fasteners captured 55.46% of the 2024 Automotive plastic fasteners market size, whereas removable solutions are pacing at 9.14% CAGR amid right-to-repair momentum.

- By geography, Asia-Pacific held 39.23% revenue in 2024 and is set to expand at an 8.93% CAGR, propelled by passenger-car build-outs in China and India

Global Automotive Plastic Fasteners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Global Vehicle-Light-Weighting Mandates | +1.2% | Global, with strongest impact in North America and EU | Medium Term (2-4 Years) |

| Surge in EV Production Requiring Non-Conductive Fastening | +0.8% | Asia-Pacific Core, Spill-over to North America and EU | Long Term (≥ 4 Years) |

| Explosion of In-vehicle Electronics and Wiring Complexity | +0.7% | Global, Led by Premium Segments in Developed Markets | Short Term (≤ 2 Years) |

| Automation-Ready Snap-fit Designs Cut Assembly Costs | +0.6% | Asia-Pacific Manufacturing Hubs, Expanding to Mexico and Eastern Europe | Medium Term (2-4 Years) |

| Circular-economy Specs Favour Recyclable Mono-Material Clips | +0.5% | EU Leadership, Spreading to North America and Asia-Pacific | Long Term (≥ 4 Years) |

| Asia-Pacific Passenger-car Build-out Sustains High-Volume Demand | +0.4% | Asia-Pacific Core, with Supply Chain Effects Globally | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Tightening Global Vehicle-Light-Weighting Mandates

Regulatory agencies worldwide are intensifying fuel economy standards that directly incentivize plastic fastener adoption over heavier metal alternatives. The EPA's Corporate Average Fuel Economy requirements mandate fleet-wide improvements of 5% annually through 2026, while the European Union's CO2 emission standards target 95g/km for new passenger cars. These mandates create measurable cost penalties for automakers exceeding weight thresholds, with fines reaching EUR 95 per gram of CO2 excess multiplied by vehicle sales volumes. Geely's recent Altair Enlighten Award recognition for converting metal stator cooling systems to polyphthalamide achieved 47% weight reduction while enabling integrated snap-fit assembly, demonstrating the strategic value of plastic fastener integration in lightweighting programs[1]Austin Weber, "EV Manufacturers Lauded for Lightweighting Efforts," Assembly Magazine, assemblymag.com. . The regulatory influence extends beyond passenger vehicles, as commercial vehicle emissions standards in California and the EU are driving similar material substitution trends in heavy-duty applications.

Surge in EV Production Requiring Non-Conductive Fastening

Electric vehicle architectures fundamentally alter fastening requirements due to high-voltage safety protocols and electromagnetic interference concerns that metal fasteners can exacerbate. Battery pack assemblies operating at 400V and 800V systems require non-conductive fastening solutions to prevent electrical shorts and maintain thermal management integrity. Cooper Standard's eCoFlow Switch Pump technology, recognized with a 2025 Automotive News PACE Pilot Award, integrates electric water pumps with electrically driven valves while reducing electrical wire harness complexity through strategic plastic fastener placement[2]"Cooper Standard Receives 2025 Automotive News PACE Pilot Recognition," Cooper Standard, ir.cooperstandard.com.. The shift toward solid-state batteries and silicon carbide inverters will further amplify demand for specialized plastic fasteners that can withstand higher operating temperatures while maintaining electrical isolation. ISO 26262 functional safety standards increasingly mandate non-conductive fastening in safety-critical EV systems, creating regulatory tailwinds for market expansion.

Explosion of In-Vehicle Electronics and Wiring Complexity

Modern vehicles integrate over 100 electronic control units connected by wiring harnesses exceeding 4 kilometers in total length, creating exponential demand for cable management and retention solutions. Advanced driver assistance systems, infotainment platforms, and connectivity modules require precise wire routing that traditional metal clips cannot accommodate due to electromagnetic interference risks. HellermannTyton's cable management solutions demonstrate how specialized plastic fasteners enable automated harness installation while meeting DIN 72036 automotive standards for vibration resistance and temperature cycling. The transition to zonal architectures and software-defined vehicles will concentrate wiring complexity in specific vehicle zones, intensifying fastener density requirements in those areas. Compliance factors include electromagnetic compatibility testing per ISO 11452 standards, which favor plastic fastener solutions over conductive alternatives.

Automation-Ready Snap-Fit Designs Cut Assembly Costs

Automotive manufacturers are prioritizing fastening solutions that eliminate secondary operations and reduce labor intensity in high-volume production environments. Snap-fit plastic fasteners enable single-motion installation that robotic systems can execute with greater precision and speed than threaded alternatives requiring torque control. ARaymond's smart glove technology for assembly workers demonstrates how even manual installation benefits from tactile feedback systems that ensure proper snap-fit engagement, reducing quality defects and rework costs. The economic advantage becomes pronounced in Asia-Pacific manufacturing hubs where labor costs are rising and automation adoption accelerates. Fastener designs incorporating visual and audible confirmation features support Industry 4.0 quality monitoring systems that track installation success rates in real-time, creating competitive advantages for suppliers offering these capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lower Strength and Heat Limits Versus Metal Alternatives | -0.9% | Global, with Acute Impact in High-Performance Applications | Short Term (≤ 2 Years) |

| Engineering-Polymer Price Volatility | -0.6% | Global, with Supply Chain Concentration in Asia-Pacific | Medium Term (2-4 Years) |

| Stricter Interior Fire-Retardancy Rules Raise Compliance Costs | -0.4% | North America and EU Leadership, Expanding Globally | Long Term (≥ 4 Years) |

| Right-to-Repair Laws Boosting Demand for Removable Metal Fixings | -0.3% | EU Core, with Legislative Momentum in North America | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

Lower Strength and Heat Limits Versus Metal Alternatives

Plastic fasteners face fundamental material limitations in high-stress and elevated-temperature applications where metal alternatives maintain superior performance characteristics. Engine compartment applications exceeding 150°C and structural mounting points requiring tensile strengths above 50 MPa continue favoring steel and aluminum fasteners despite weight penalties. The challenge intensifies in electric vehicle applications where battery thermal runaway events can generate temperatures exceeding 800°C, necessitating metal fastening solutions for safety-critical components. Advanced engineering polymers like PEEK and PPS offer improved temperature resistance but command premium pricing that limits adoption to specialized applications. Regulatory compliance with crash safety standards often mandates metal fasteners in structural applications where plastic alternatives cannot meet energy absorption requirements during impact events.

Engineering-Polymer Price Volatility

Raw material cost fluctuations for key engineering polymers create unpredictable pricing pressures that challenge long-term supply contracts and margin stability. Nylon 6/6 prices increased 40% in 2024 due to adipic acid supply constraints, while polypropylene costs fluctuated with crude oil price volatility and refinery capacity utilization rates. Stanley Black & Decker's Q3 2024 results highlighted automotive market softness partly attributed to material cost pressures affecting engineered fastening business profitability. Supply chain concentration in Asia-Pacific petrochemical complexes creates geographic risk exposure when regional disruptions affect global polymer availability. Currency fluctuations between USD and regional currencies further amplify cost volatility for multinational fastener suppliers managing global supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Type: Wire Harnessing Dominance Drives Electronics Growth

Wire harnessing applications command 24.73% market share in 2024, reflecting the critical role of cable management systems in modern vehicle architectures that integrate over 100 electronic control units per vehicle. The segment's leadership stems from increasing wiring complexity as vehicles transition toward software-defined architectures requiring precise cable routing and electromagnetic interference shielding. Electronics applications, while holding a smaller current share, demonstrate the fastest growth trajectory at 11.34% CAGR through 2030, driven by ADAS sensor integration and infotainment system expansion that demand specialized mounting solutions. Interior applications benefit from lightweighting initiatives and aesthetic requirements that favor plastic over metal alternatives, while exterior applications face durability challenges from UV exposure and temperature cycling that limit growth potential.

Powertrain applications are experiencing transformation as electric vehicle adoption reduces traditional engine-related fastening requirements while creating new opportunities in battery pack and thermal management systems. Chassis applications maintain steady demand driven by suspension component lightweighting initiatives, though growth remains constrained by structural performance requirements that often necessitate metal alternatives. The regulatory influence of electromagnetic compatibility standards per ISO 11452 increasingly favors plastic fasteners in electronics applications where metal alternatives can create interference issues. Wire harnessing segment growth correlates directly with vehicle electrification levels, as electric vehicles require 40% more wiring harness content than conventional powertrains.

By Vehicle Type: Passenger Dominance Masks EV Acceleration

Passenger vehicles maintain overwhelming market leadership at 78.29% share in 2024, reflecting the segment's volume dominance in global automotive production and the standardization of plastic fastener applications across mainstream vehicle platforms. However, the electric vehicle subset within passenger vehicles drives disproportionate growth at 9.52% CAGR, significantly exceeding the overall passenger vehicle growth rate due to specialized fastening requirements for battery systems and high-voltage components. Commercial vehicles represent a smaller but strategically important segment where durability requirements often favor metal fasteners, though lightweighting regulations are gradually shifting specifications toward engineered plastic alternatives in non-structural applications.

The passenger vehicle segment benefits from economies of scale that enable cost-effective plastic fastener adoption across multiple vehicle platforms, while premium segments drive innovation in advanced materials and integrated designs. Commercial vehicle applications face unique challenges from extended duty cycles and harsh operating environments that test plastic fastener durability limits, creating opportunities for suppliers to develop enhanced material formulations. Electric commercial vehicles, including delivery vans and urban buses, represent an emerging growth vector where non-conductive fastening requirements align with plastic fastener capabilities. The regulatory influence of vehicle safety standards like FMVSS and ECE regulations increasingly accommodates plastic fastener solutions in passenger vehicle applications while maintaining stricter requirements for commercial vehicle structural components.

By Function Type: Bonding Leadership Faces NVH Challenge

Bonding applications dominate with 62.18% market share in 2024, encompassing structural adhesive systems and mechanical fastening solutions that create permanent joints between dissimilar materials in vehicle assemblies. The segment's leadership reflects the automotive industry's shift toward multi-material construction, where plastic fasteners enable joining of steel, aluminum, and composite components without galvanic corrosion concerns. NVH applications, though currently smaller, demonstrate the fastest growth at 10.87% CAGR through 2030, driven by electric vehicle adoption that amplifies acoustic challenges previously masked by internal combustion engine noise.

The transition to electric powertrains creates new NVH requirements where plastic fasteners must provide vibration isolation and acoustic damping properties beyond traditional mechanical fastening functions. Vibracoustic's global NVH expertise, generating EUR 2.634.7 billion in sales with 10,351 employees, demonstrates the market opportunity for specialized fastening solutions that address electric vehicle acoustic challenges[3]"Vibracoustic," freudenberg.com.. Ascend Materials' Vydyne Anti-Vibration System achieves a 75-84% reduction in cabin noise while providing a 30-40% weight reduction versus die-cast aluminum alternatives, illustrating how advanced plastic fastener materials can simultaneously address multiple performance requirements. Compliance factors include acoustic testing per ISO 362 standards that increasingly favor plastic fastener solutions offering integrated damping properties.

By Characteristics: Permanent Solutions Drive Removable Innovation

Permanent fastening solutions command 55.46% market share in 2024, reflecting the automotive industry's preference for one-time installation systems that reduce assembly complexity and eliminate potential failure points from repeated fastener cycling. The segment's dominance stems from cost advantages and reliability benefits in high-volume production environments where permanent installation eliminates secondary operations and reduces labor content. Removable fasteners, while holding a smaller current share, grow at 9.14% CAGR through 2030, influenced by right-to-repair legislation in the European Union and emerging regulations in North America that mandate serviceable component access.

The regulatory landscape increasingly favors removable fastening solutions as Extended Producer Responsibility frameworks assign end-of-life vehicle processing costs to manufacturers, creating economic incentives for disassembly-friendly designs. Right-to-repair legislation, particularly the EU's repair clause implementation, requires automotive manufacturers to ensure component accessibility for independent repair facilities, driving demand for removable fastener solutions in service-critical applications. However, permanent fasteners maintain advantages in structural and safety-critical applications where regulatory agencies prioritize joint integrity over serviceability considerations. The balance between permanent and removable solutions varies by vehicle segment, with luxury vehicles increasingly adopting removable fasteners to support premium service experiences while mass-market vehicles prioritize permanent solutions for cost optimization.

Geography Analysis

Asia-Pacific leads the global automotive plastic fasteners market with 39.23% share in 2024 and maintains the fastest regional growth rate of 8.93% through 2030, driven by China and India's combined passenger vehicle production exceeding 25 million units annually. China's automotive manufacturing ecosystem, supported by government incentives for electric vehicle adoption and domestic supply chain development, creates sustained demand for cost-effective plastic fastening solutions that support high-volume production requirements. Japan's automotive sector, with established suppliers like Nifco leading plastic component innovation, provides technological leadership while expanding overseas manufacturing capacity to serve global markets.

North America and Europe represent mature markets where regulatory mandates drive plastic fastener adoption through lightweighting requirements and circular economy initiatives. The European Union's End-of-Life Vehicles Directive mandating 95% recyclability by weight creates direct incentives for mono-material plastic fastener adoption, while CAFE standards in North America impose cost penalties for vehicle weight excess that favor plastic over metal alternatives. These regions demonstrate slower volume growth but higher value content per vehicle as premium segments adopt advanced plastic fastener technologies for NVH control and aesthetic applications. The regulatory influence of agencies like EPA, NHTSA, and European Commission continues shaping fastener specifications through evolving safety and environmental standards.

Middle East and Africa, along with South America, represent emerging markets where automotive production growth and increasing local content requirements create opportunities for plastic fastener suppliers establishing regional manufacturing capabilities. Brazil's automotive sector benefits from government policies supporting local production while Argentina's economic volatility creates challenges for long-term supply contracts and currency hedging strategies. These regions typically prioritize cost-effective fastening solutions over advanced materials, though electric vehicle adoption in urban centers like São Paulo and Mexico City is beginning to drive demand for specialized non-conductive fasteners.

Competitive Landscape

The automotive plastic fasteners market exhibits moderate fragmentation with established players like Illinois Tool Works, ARaymond, and Nifco competing through technological innovation and regional manufacturing capabilities rather than pure scale advantages. Market concentration remains limited as OEM customers prioritize supply chain diversification and regional sourcing strategies that prevent excessive dependence on single suppliers.

Competition intensifies around automation-ready designs and integrated functionality, where suppliers differentiate through snap-fit mechanisms that reduce assembly costs and enable robotic installation with visual confirmation features. Strategic patterns reveal increasing emphasis on circular economy compliance and material innovation, with suppliers developing recyclable mono-material solutions that meet European Union end-of-life vehicle regulations while maintaining performance characteristics.

White-space opportunities exist in electric vehicle-specific applications where non-conductive fastening requirements and thermal management challenges create demand for specialized solutions that traditional metal fastener suppliers cannot address.The competitive landscape increasingly rewards suppliers that can integrate fastener functionality with adjacent technologies like sensors, heating elements, or acoustic damping materials to create higher-value system solutions rather than commodity fastening products.

Automotive Plastic Fasteners Industry Leaders

-

Illinois Tool Works (ITW)

-

ARaymond

-

Nifco Inc.

-

Stanley Black and Decker

-

Bulten AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Freudenberg Group's Vibracoustic division reported annual sales of EUR 2,634.7 million with 10,351 employees. This demonstrates sustained demand for NVH (Noise, Vibration, Harshness) control systems, which increasingly integrate plastic fastening components for automotive applications. The company's global network of development and production facilities supports growing requirements for vibration isolation and acoustic damping solutions.

- August 2024: Ascend Materials published comprehensive technical documentation for its Vydyne Anti-Vibration System (AVS) technology. This polyamide-based material suite is specifically designed for electric vehicle (EV) applications, targeting the 3,000–4,000 Hz frequency range where conventional dampers are ineffective. The Vydyne AVS achieves a 75–84% reduction in cabin noise and a 30–40% weight reduction compared to die-cast aluminum alternatives.

Global Automotive Plastic Fasteners Market Report Scope

| Interior |

| Exterior |

| Electronics |

| Powertrain |

| Chassis |

| Wire Harnessing |

| Others |

| Passenger Vehicle |

| Commercial Vehicle |

| Bonding |

| NVH |

| Permanent |

| Removal |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application Type | Interior | |

| Exterior | ||

| Electronics | ||

| Powertrain | ||

| Chassis | ||

| Wire Harnessing | ||

| Others | ||

| By Vehicle Type | Passenger Vehicle | |

| Commercial Vehicle | ||

| By Function Type | Bonding | |

| NVH | ||

| By Characteristics | Permanent | |

| Removal | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the 2025 size of the Automotive plastic fasteners market?

It is valued at USD 3.96 billion in 2025.

How fast is the market expected to grow?

The forecast calls for a 4.93% CAGR to 2030, reaching USD 5.04 billion.

Which region leads in revenue?

Asia-Pacific accounts for 39.23% of global sales in 2024 and remains the fastest-growing region.

Which application dominates demand?

Wire harnessing commands 24.73% share due to rising in-vehicle electronics content.

Why are plastic fasteners gaining traction in EVs?

They provide non-conductive, lightweight, and automation-friendly solutions essential for 400 V and 800 V battery systems.

What factor limits broader plastic adoption?

Strength and heat resistance constraints versus metal restrict usage in high-load, high-temperature zones.

Page last updated on: