North America Car Air Freshener Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

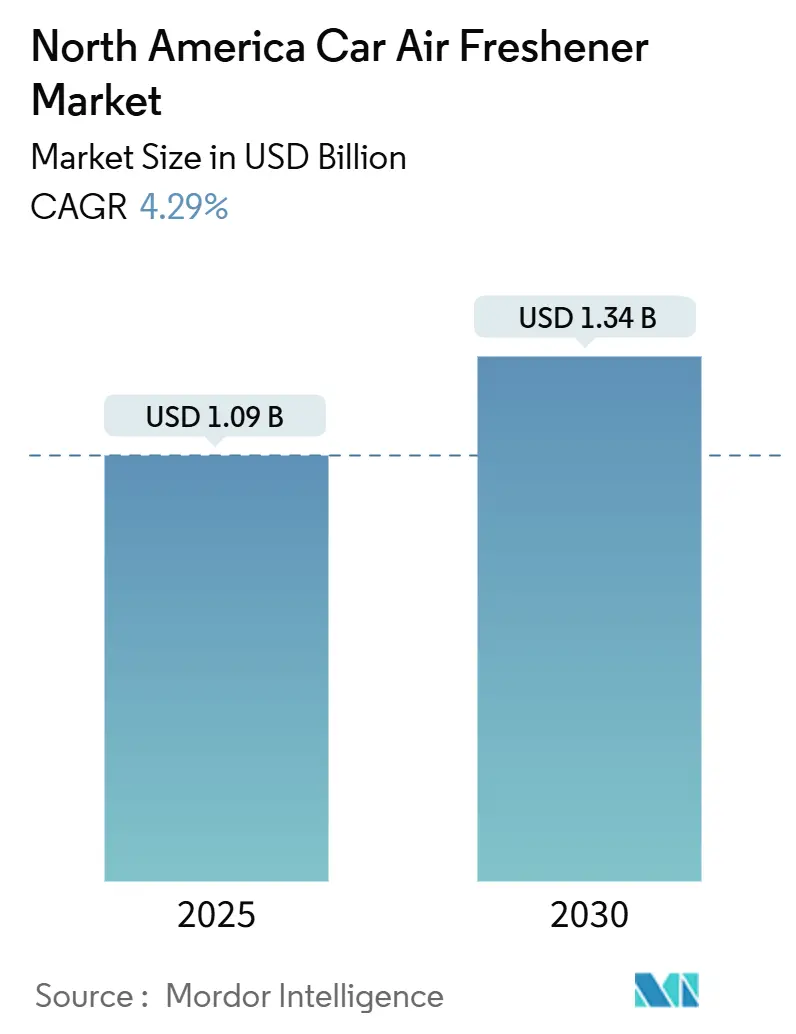

| Market Size (2025) | USD 1.09 Billion |

| Market Size (2030) | USD 1.34 Billion |

| Growth Rate (2025 - 2030) | 4.29% CAGR |

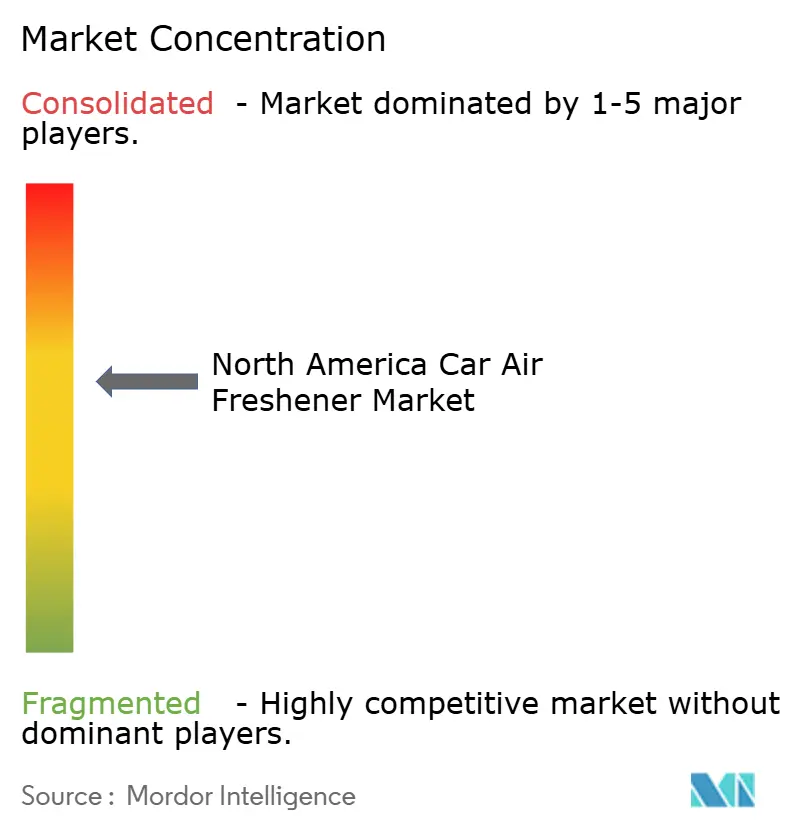

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Car Air Freshener Market Analysis by Mordor Intelligence

The North America car air fresheners market size stands at USD 1.09 billion in 2025 and is forecast to reach USD 1.34 billion by 2030, advancing at a 4.29% CAGR. The outlook reflects robust demand for natural formulations, deeper penetration of e-commerce, and a growing commercial‐vehicle fleet that elevates cabin-care spending. Hanging products remain the volume anchor, yet vent clips accelerate fastest as HVAC-linked formats gain favor. Gel forms lead by value today, but sprays post the strongest growth on the back of instant-application convenience. Passenger cars dominate purchases, while light commercial vehicles surge as ride-hailing and last-mile delivery scale. Regulatory moves that cap volatile organic compounds (VOC) spur formula innovation and reward manufacturers that pivot early to compliant, plant-based ingredients.

Key Report Takeaways

- By product type, hanging air fresheners held 41.87% of the North America car air fresheners market share in 2024; vent clips are poised to expand at a 6.88% CAGR to 2030.

- By form, gel captured 37.79% of the North American car air fresheners market size in 2024, whereas spray variants are projected to climb at a 7.59% CAGR through 2030.

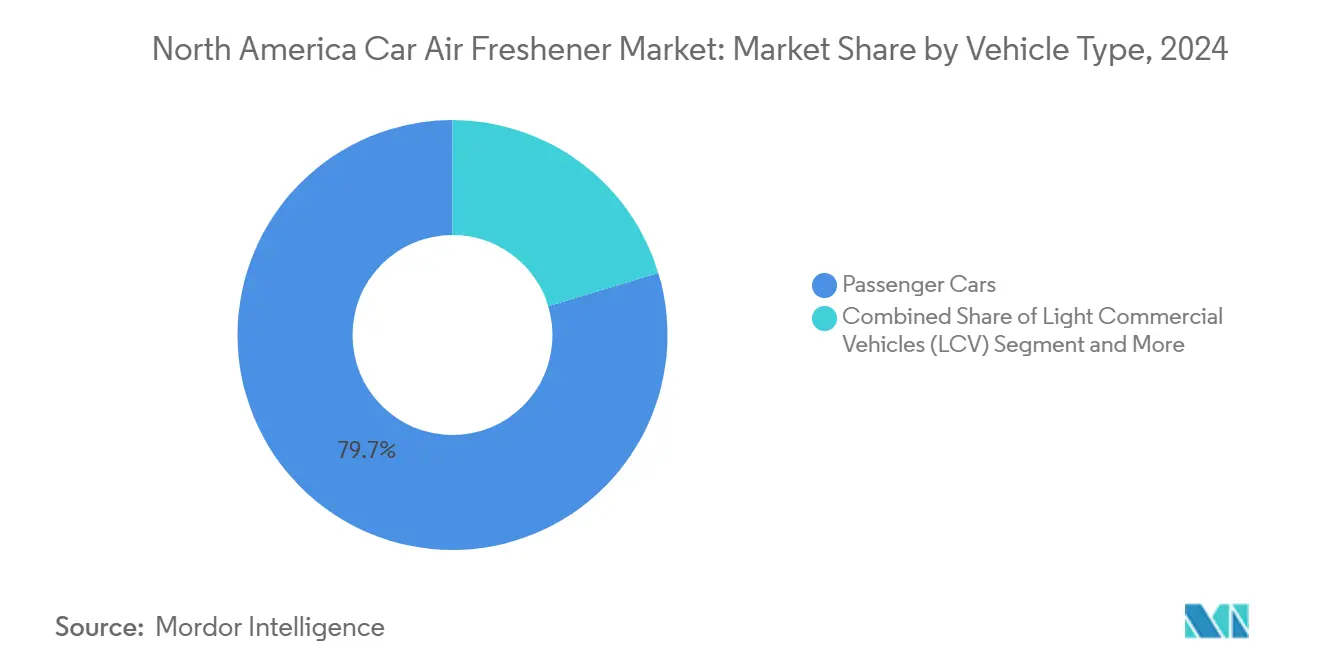

- By vehicle type, passenger cars commanded 79.66% of the North American car air fresheners market size in 2024, but light commercial vehicles are advancing at a 5.97% CAGR over the same horizon.

- By distribution channel, the aftermarket controlled 82.73% of the North American car air fresheners market share in 2024, while OEM integration is forecast to register a 6.38% CAGR up to 2030.

- By country, the United States captured an 87.84% share in 2024, while Mexico is projected to grow at a 5.87% CAGR to 2030.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on car air freshener market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America Car Air Freshener Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural and Eco-Friendly Formulations | +1.1% | United States, Canada, Mexico | Medium term (2-4 years) |

| Automotive Consumables' Penetration | +0.9% | United States, Canada | Short term (≤ 2 years) |

| Ride-Hailing and Last-Mile Delivery Fleets | +0.8% | United States, Canada, Mexico | Medium term (2-4 years) |

| Air Quality Regulations and VOC Limits | +0.6% | California, United States, Canada | Long term (≥ 4 years) |

| In-Car Wellness | +0.5% | United States, Canada | Medium term (2-4 years) |

| Smart Dispensing Systems | +0.3% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Natural and Eco-Friendly Formulations

Plant-based ingredients and biodegradable packaging reshape product pipelines as adults have reported discomfort from conventional fragranced items, and have been diagnosed with multiple chemical sensitivity. Brands remove phthalates, parabens, and synthetic musks, trading up to essential oils that command a 15-25% price premium. California Air Resources Board rules reinforce the shift by favoring low-VOC blends. Large players now market transparency labels to win trust, and smaller eco specialists leverage online channels to reach wellness-focused drivers. The net effect lifts average selling prices while raising formulation-testing costs.

Rapid E-Commerce Penetration for Automotive Consumables

Automotive consumables migrate online faster than brick-and-mortar sales. Subscription packs for air fresheners simplify replenishment and secure predictable cash flow for vendors. Premium and niche aromas, once crowded out of store shelves, gain visibility through algorithmic merchandising. Younger buyers, who account for approximately 40% of new-vehicle purchases, rely on digital research and checkout, pushing brands to invest in influencer collaborations and augmented-reality scent previews.

Growing Ride-Hailing and Last-Mile Delivery Fleets

Expanding commercial mobility requires consistent, subtle scents to elevate passenger comfort. Fleet managers buy in bulk, prioritizing lavender, citrus, and sandalwood notes that rate highly in passenger feedback surveys. The 5.97% CAGR in light commercial vehicles creates a parallel demand for long-lasting gels and discreet vent-clip systems that withstand high utilization. Suppliers tailor SKUs with extended fragrance cycles, minimizing downtime for replacements and ensuring uniform odor control across fleet assets.

Cabin-Air Quality Regulations and VOC Limits Tightening

California caps double-phase aerosol VOC at over 20%, prompting research into alternative propellants and encapsulation technologies. Industry compliance spending rises, but first movers build entry barriers and secure OEM endorsements for low-emission lines. Emerging state proposals mirror California’s stance, suggesting wider U.S. adoption. On a global level, the International Fragrance Association’s 51st amendment restricts select compounds, synchronizing North American compliance with European safety protocols and adding testing complexity that favors scale players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chemical-Safety VOC Regulation | -0.8% | California, United States, Canada | Medium term (2-4 years) |

| Raw-Material Price Volatility | -0.6% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Interior Odor Source Reduction | -0.3% | United States, Canada | Long term (≥ 4 years) |

| Fragrance-Sensitivity Backlash | -0.3% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Chemical-Safety VOC Regulation Compliance Costs

Escalating regulatory compliance requirements impose significant cost burdens on air freshener manufacturers, particularly smaller companies lacking dedicated regulatory affairs departments. California's AB 617 Community Air Protection program intensifies scrutiny of mobile-source emissions, potentially expanding VOC regulations beyond the current scope. Smaller firms face resource strain, slowing innovation cadence, and narrowing competitive choice. Larger incumbents, however, amortize compliance costs across broad portfolios, reinforcing share stability under stricter rules.

Volatility in Fragrance-Grade Raw-Material Prices

Price instability in essential oils and synthetic fragrance compounds creates margin pressure and supply chain uncertainty for manufacturers. Global fragrance ingredient sourcing spans multiple countries with varying quality standards and cost structures, exposing companies to currency fluctuations and geopolitical disruptions. Synthetic substitutes mitigate some spikes but clash with the natural trend, forcing strategic hedging and inventory buffers that tie up working capital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hanging Stability, Vent-Clip Momentum

Hanging fresheners retained 41.87% of the North American car air fresheners market share in 2024 due to decades-long consumer familiarity and widespread availability. Vent clips, leveraging HVAC airflow for even diffusion, are on track for a 6.88% CAGR, signaling evolving preferences toward discreet, set-and-forget formats. Sprays and aerosols sustain relevance for on-demand odor neutralization, while gels and cans satisfy drivers seeking multi-week performance at a low cost per day. Paper variants remain a budget niche for fleets that accept frequent replacement cycles to manage per-vehicle expenditure.

The competitive narrative now spotlights sensor-ready vent-clip shells that house micro-cartridges, aiming to bridge aftermarket simplicity with OEM-grade sophistication. Hanging SKUs still dominate seasonal gift packs and brand collaborations, buoyed by emotive shapes and novelty scents. Meanwhile, premium gel capsules coated in plant-based resins meet the dual call for sustainability and longevity. The North American car air fresheners market continues to diversify formats, ensuring channel partners carry broader assortments for upsell and cross-merchandising.

By Form: Gel Commands Today; Spray Seizes Growth

Gel forms commanded 37.79% of the North American car air fresheners market size in 2024, prized for leak-proof containers and gradual scent release. Spray lines, expected to progress at a 7.59% CAGR, capture impulse purchase occasions and align with consumer desire for immediate odor relief before rideshare pick-ups or passenger boarding. Solid blocks underpin traditional hanging cards, whereas liquids serve refillable diffusers, especially in luxury marques that integrate factory-mounted scent ports.

From a cost standpoint, gels yield attractive margins because smaller fragrance payloads deliver prolonged effect via polymer matrices. Conversely, spray manufacturers invest in atomizer technology and propellant alternatives to comply with VOC limits. Usage data suggests ride-hailing drivers carry sprays to address unpredictable passenger odors, while family car owners value gel inserts for continuous freshness. Sustainability also sways form choice as brands introduce compostable gel cups and recyclable metal spray cans to signal environmental responsibility.

By Vehicle Type: Passenger Car Dominance, Commercial Upswing

Passenger cars accounted for 79.66% of the North America car air fresheners market size in 2024, mirroring the region’s large personal-vehicle base. Light commercial vehicles, buoyed by app-based delivery and ridesharing, are projected to rise at a 5.97% CAGR through 2030, driving interest in bulk purchasing and standardized fragrances that uphold service brand perception. Medium and heavy trucks hold steady demand, focusing on driver comfort during long hauls, while buses and coaches require high-volume diffusers compatible with HVAC circulation.

Fleet dynamics differ markedly: procurement officers value durability and cost per hour more than aroma novelty, pushing manufacturers to supply concentrated formulations in larger canisters. Passenger-car owners, by contrast, experiment with seasonal scents and themed collaborations, sustaining brand churn and limited-edition releases. The North America car air fresheners industry, therefore, balances mass-customization for retail with industrial-grade continuity for fleets, a duality that shapes R&D pipelines.

By Distribution Channel: Aftermarket Rule, OEM Catch-Up

The aftermarket controlled 82.73% of the North America car air fresheners market share in 2024, unlocked by auto-parts chains, big-box retailers, convenience stores, and emerging direct-to-consumer websites. OEM installations, however, are climbing at a 6.38% CAGR as automakers embed fragrance systems in new models to enhance cabin experience and tap accessory revenue. Subscription ecommerce within the aftermarket further erodes physical-shelf constraint, letting niche scents reach national audiences.

OEM success stories, such as Mercedes’ Air Balance Package, showcase willingness among premium buyers to pay triple the aftermarket sticker price for factory integration. For suppliers, OEM channels demand multi-year durability testing, driving collaboration with Tier-1 interior suppliers and electronics integrators. Aftermarket brands respond by releasing plug-and-play cartridges that mimic OEM fit, protecting incumbency while leveraging online tutorials and social media influencers to drive installation confidence.

Geography Analysis

The United States retained 87.84% of regional value in 2024, underpinned by the world’s largest light-vehicle fleet and diverse retail footprint that spans mass merchants to specialty auto centers. Stringent California VOC caps catalyze innovation toward low-emission blends that later cascade nationwide. E-commerce channels flourish as free-shipping thresholds and subscription models simplify replenishment. Seasonal promotional calendars, think summer road trips and holiday travel, continue to spur volume spikes, prompting suppliers to synchronize inventory with consumer mood cycles.

Canada tracks U.S. trends but exhibits sharper seasonality shaped by cold winters that limit window ventilation, heightening demand for odor neutralization. Eco certifications resonate strongly, reflecting broader national environmental consciousness. Cross-border logistics under USMCA underpin cost-efficient supply, while provincial labeling rules add moderate complexity. Specialty aromas, such as maple-inspired or alpine-forest notes, slot into Canadian cultural identity and fetch modest premiums during tourism seasons.

Mexico emerges as the growth pacesetter with a 5.87% CAGR, fueled by record auto production of 3.99 million units in 2024 and rising middle-class ownership supported by 59.4% vehicle financing penetration[1]Óscar Goytia, “Mexico January Vehicle Sales Up 5.9%, Slowdown Expected,” mexicobusiness.news. Retail still skews toward traditional outlets and roadside kiosks, but smartphone adoption is nudging consumers online. Tropical and citrus scents outsell musky profiles, aligning with climate and local taste. Domestic manufacturing hubs near Monterrey and Puebla shorten supply chains, letting brands offer competitive pricing while meeting regional content rules.

Competitive Landscape

Market concentration is moderate, with the top five suppliers. CAR-FRESHNER Corp leads via its Little Trees franchise, cemented by universal brand recall and ubiquitous peg-hook presence across retail. Multinational household-care firms, Procter & Gamble, Reckitt Benckiser, SC Johnson, and Henkel, deploy cross-category brand equity and scaled distribution to defend shelf real estate. These incumbents emphasize limited-edition launches to maintain consumer excitement, exemplified by Febreze’s “Vanilla Suede” 2025 Scent of the Year[2]Business Wire, “Febreze Reveals Vanilla Suede as its 2025 Scent of the Year,” bakersfield.com.

Innovation now rests on integrating electronics and sustainability. Lincoln’s microchip-enabled fragrance cartridges illustrate a bridge between traditional consumables and connected-car ecosystems. SC Johnson, for instance, spotlights ingredient transparency and allergen exclusion to reassure health-minded drivers. Pricing wars are rare because air fresheners represent a low-ticket indulgence relative to vehicle O&M spending, allowing firms to prioritize differentiation over discounting.

New entrants carve space through eco labels, artisanal scents, or fleet-service bundles. The barrier to entry remains manageable from a capital standpoint, yet regulatory compliance and large-scale marketing challenge small brands. Strategic alliances with rideshare operators or automotive interior suppliers offer pathways to rapid volume. Meanwhile, incumbents explore refillable formats and closed-loop recycling to pre-empt environmental scrutiny and reinforce brand citizenship narratives.

North America Car Air Freshener Industry Leaders

Procter & Gamble

Reckitt Benckiser

SC Johnson & Son

Henkel

Little Trees (CAR-FRESHNER Corp.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Jamie Laing’s Candy Kittens brand debuted hanging fresheners promising up to 45-day performance, broadening lifestyle crossover appeal.

- April 2025: Febreze introduced “Vanilla Suede” as its 2025 Scent of the Year, sustaining its seasonal limited-edition cadence.

- November 2024: KFC partnered with Homesick Candles to release chicken- and biscuit-inspired fresheners for holiday gifting.

North America Car Air Freshener Market Report Scope

| Hanging Air Fresheners |

| Vent Clips |

| Sprays/Aerosols |

| Gels and Cans |

| Paper Fresheners |

| Others |

| Solid |

| Liquid |

| Gel |

| Spray |

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Medium and Heavy Commercial Vehicles (MHCV) |

| Buses and Coaches |

| OEM (Original Equipment Manufacturer) |

| Aftermarket |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Hanging Air Fresheners |

| Vent Clips | |

| Sprays/Aerosols | |

| Gels and Cans | |

| Paper Fresheners | |

| Others | |

| By Form | Solid |

| Liquid | |

| Gel | |

| Spray | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles (LCV) | |

| Medium and Heavy Commercial Vehicles (MHCV) | |

| Buses and Coaches | |

| By Distribution Channel | OEM (Original Equipment Manufacturer) |

| Aftermarket | |

| By Country | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How large is the North America car air fresheners market in 2025?

The North America car air fresheners market size is USD 1.09 billion in 2025.

What is the forecast CAGR for North America?

The market is projected to grow at a 4.29% CAGR from 2025 to 2030.

Which product type leads sales?

Hanging fresheners hold the lead with a 41.87% share in 2024.

Which segment will grow fastest by 2030?

Vent clips are forecast to post the highest 6.88% CAGR through 2030.

What channel dominates distribution?

The aftermarket captures 82.73% of regional value, although OEM integration is gaining ground.

Which country shows the fastest growth?

Mexico is set to expand at a 5.87% CAGR to 2030, outpacing the United States and Canada.

Page last updated on: