Nordic Countries Renewable Energy Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

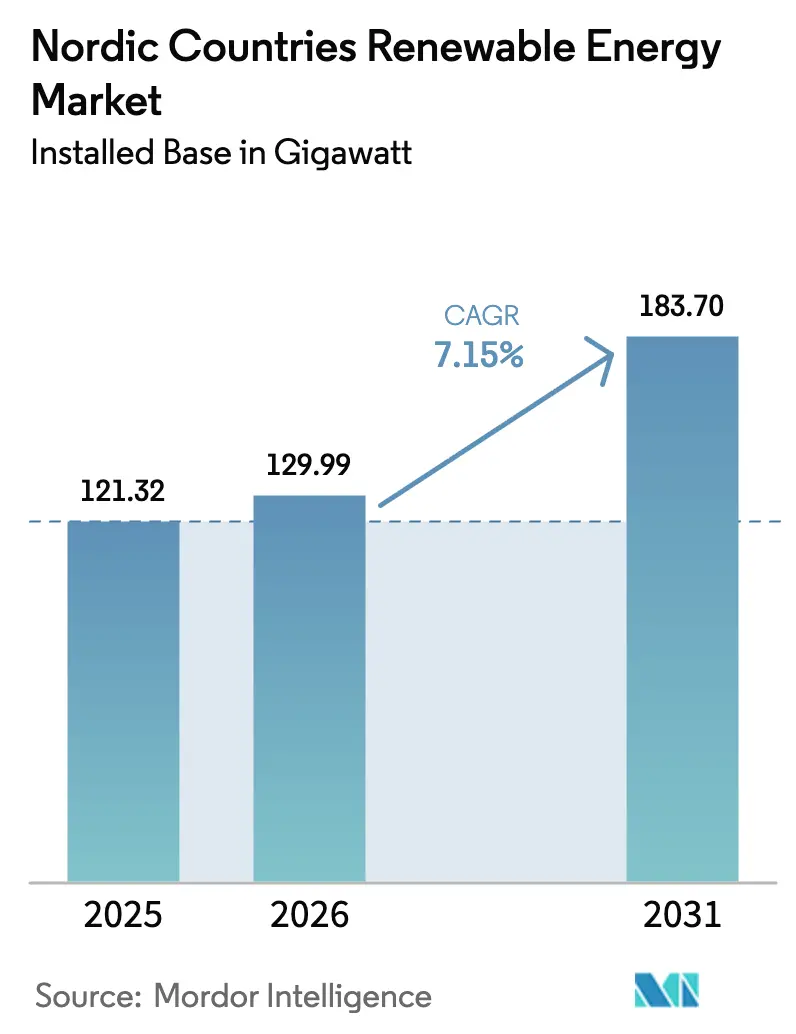

| Base Year Market Size (2025) | 121.32 gigawatt |

| Market Volume (2026) | 129.99 gigawatt |

| Market Volume (2031) | 183.7 gigawatt |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nordic Countries Renewable Energy Market Analysis by Mordor Intelligence

The Nordic Countries Renewable Energy Market size was valued at 121.32 gigawatt in 2025 and estimated to grow from 129.99 gigawatt in 2026 to reach 183.7 gigawatt by 2031, at a CAGR of 7.15% during the forecast period (2026-2031).

Regional growth is driven by the combination of long-established hydropower assets, accelerated offshore wind deployment, and a rapidly developing green hydrogen value chain. Early achievement of the EU 2030 renewables target, renewables accounted for 49% of gross energy use in 2023, allowing Nordic stakeholders to monetize advanced grid-balancing services through dense cross-border interconnectors. Growing corporate demand for clean electricity, declining levelized costs for onshore wind and solar PV, and supportive carbon-pricing reforms further reinforce the upward trajectory of the Nordic countries' renewable energy market. Competitive intensity is moderate as traditional utilities defend market positions against specialist developers, while regulatory uncertainty in Norway introduces a degree of strategic risk.

Key Report Takeaways

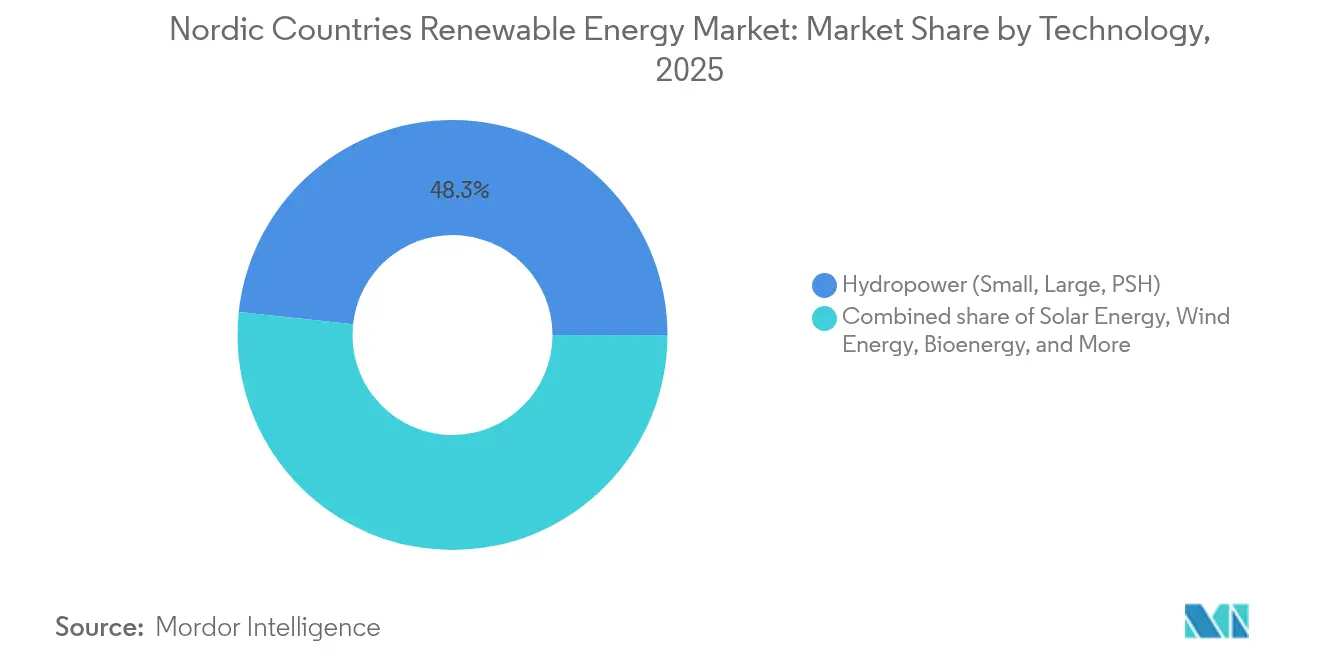

- By technology, hydropower led with 48.30% of the Nordic countries' renewable energy market share in 2025, whereas solar energy is advancing at a 18.24% CAGR through 2031.

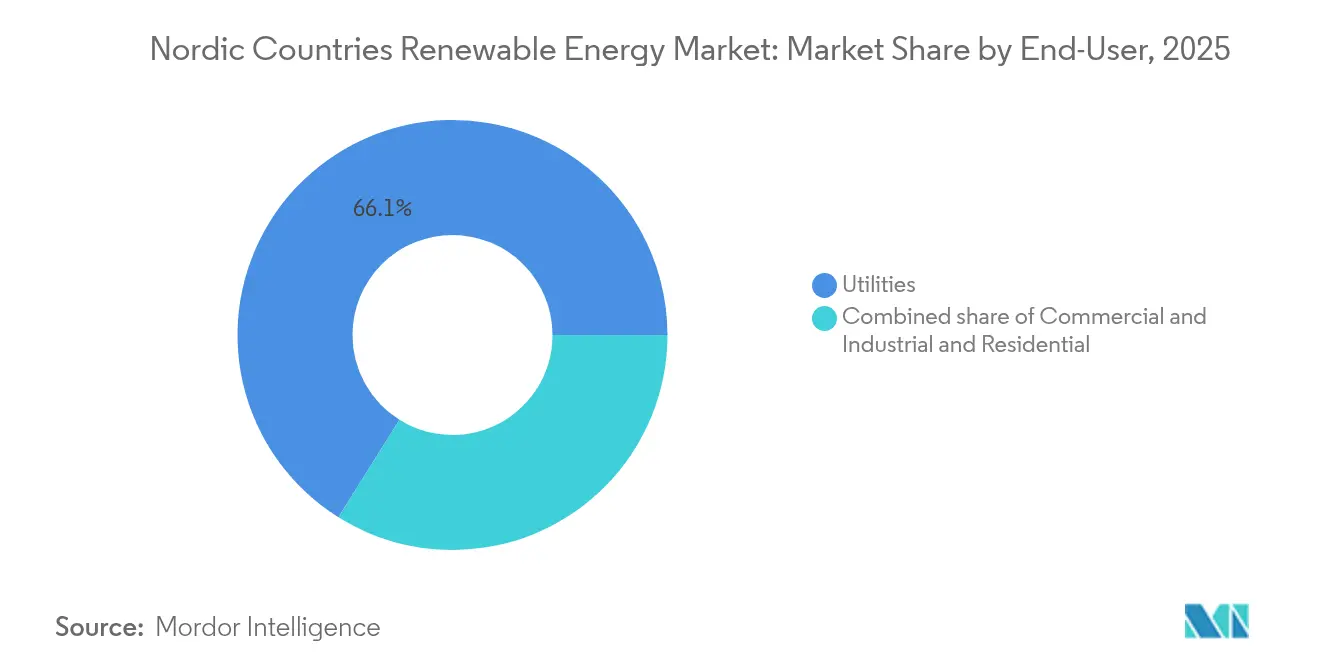

- By end-user, utilities controlled 66.10% of demand in 2025, while the commercial and industrial segment is forecast to expand at a 10.55% CAGR to 2031.

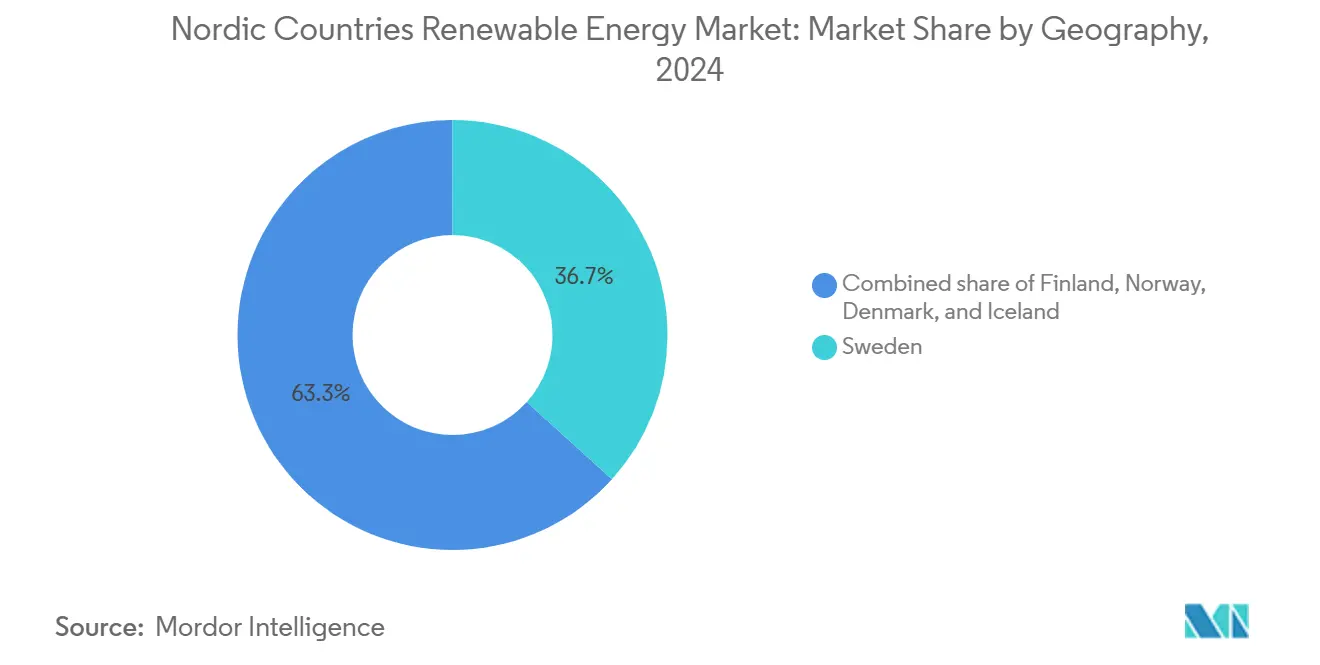

- By geography, Sweden commanded 36.20% of the capacity in 2025; Finland is expected to post the fastest growth rate of 11.95% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nordic Countries Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid build-out of offshore wind hubs | 1.8% | Denmark, Norway, Sweden | Medium term (2-4 years) |

| EU Fit-for-55 targets accelerating PPAs | 1.2% | All Nordic countries (strongest in Sweden, Finland) | Short term (≤ 2 years) |

| Grid-balancing revenues from Nordic cross-border interconnectors | 0.9% | Norway, Denmark | Medium term (2-4 years) |

| Declining LCOE for onshore wind and solar PV | 1.5% | Sweden, Finland, Denmark | Long term (≥ 4 years) |

| Surge in green-hydrogen-linked offtake MOUs | 0.8% | Norway, Sweden | Long term (≥ 4 years) |

| Data-center waste-heat offtake contracts boosting bio-energy CHP | 0.5% | Finland, Sweden | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Build-out of Offshore Wind Hubs

Denmark's North Sea Energy Island, designed to connect 10 GW of offshore capacity by 2030, exemplifies the region's shift toward hub-based development, which maximizes grid utilization and enables high-volume cross-border trading.[1]Ørsted, “North Sea Energy Island Project Details,” orsted.com Complementary projects underway in Sweden and Finland form a continuous offshore wind corridor, leveraging economies of scale in turbine procurement and operations. Floating wind pilots in Norwegian deep waters further enlarge the resource base. Collective progress positions the Nordic countries' renewable energy market as a global proving ground for advanced offshore technologies, creating cost-reduction pathways that are not achievable through isolated projects.

EU Fit-for-55 Targets Accelerating PPAs

The Fit-for-55 package has shifted Nordic procurement dynamics from feed-in tariffs to corporate power purchase agreements, guaranteeing revenue certainty for generators and clean-energy credentials for buyers. Statkraft and regional utilities have structured multi-year PPAs that hedge against price volatility while meeting the countries' additionality rules, as embedded in EU policy.[2]Statkraft, “Corporate PPA Framework in Northern Europe,” statkraft.com Ambitious national solar strategies, such as Denmark's plan to quadruple capacity, dovetail with EU objectives to produce a sustained demand pull. This convergence maintains premium pricing for exports from the Nordic countries' renewable energy market.

Grid-Balancing Revenues from Nordic Cross-Border Interconnectors

Interconnectors, such as Viking Link (Denmark-UK) and NordLink (Norway-Germany), enable the flexible output of hydropower and wind to stabilize neighboring grids during demand peaks. The 2024 Nordic power market experienced over 200 hours of negative pricing due to a hydrological surplus, yet interconnector arbitrage enabled utilities to capture revenue in high-price adjacent markets. Such optimization enhances profitability and underscores the strategic importance of the Nordic renewable energy market in Europe's broader decarbonization efforts.

Declining LCOE for Onshore Wind & Solar PV

IRENA cost data confirm that onshore wind and solar PV reached grid parity across Nordic jurisdictions by 2024.[3]International Renewable Energy Agency, “Renewable Power Generation Costs 2024,” irena.org Larger rotor diameters, higher hub heights, and increasing panel efficiency secure capacity factors that rival those of legacy baseload assets. Merchant renewables have become bankable, fostering a self-reinforcing cycle of investment within the Nordic countries' renewable energy market. Cost competitiveness also unlocks adjacent avenues such as biogas and hybrid projects, broadening the market's technology mix.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited transmission capacity in northern Scandinavia | –0.7% | Norrbotten, Finnmark | Medium term (2-4 years) |

| Lengthy environmental permitting for new wind parks | –0.5% | Norway, Sweden | Short term (≤ 2 years) |

| Turbine-blade recycling bottlenecks | –0.3% | All Nordic, acute in Denmark and Sweden | Long term (≥ 4 years) |

| Volatility in Swedish green certificate prices post-2025 | –0.4% | Sweden | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Transmission Capacity in Northern Scandinavia

Resource-rich northern Scandinavia lacks sufficient high-voltage lines to deliver growing wind and hydropower output to southern demand centers. Curtailment risk erodes project economics and dampens investor confidence. Norway's pledge to invest NOK 400 million (USD 37 million) in the Kaggefoss upgrade signals recognition of the infrastructure gap.[4]Å Energi, “Investment Plan for Kaggefoss Hydropower,” aenergi.no Yet large-scale reinforcement projects demand multi-year planning, so the constraint will continue to temper the Nordic countries' renewable energy market expansion over the long term.

Lengthy Environmental Permitting for New Wind Parks

Comprehensive impact assessments, stakeholder consultations, and legal appeals lengthen approval cycles to three to five years in Sweden and Norway. Smaller developers find it difficult to carry financing costs throughout the extended timeline, concentrating projects in the hands of capital-rich incumbents. The recent clearance of Denmark's Jammerland Bugt and Lillebaelt Syd farms demonstrates that streamlining is possible, but only after protracted review phases. Until permitting reforms gain traction, this bottleneck will act as a drag on the Nordic countries' renewable energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Hydropower Anchors, Solar Surges

Hydropower retained 48.30% of 2025 capacity and commanded ancillary-services income of EUR 1.2 billion, illustrating its foundational role in the Nordic countries' renewable energy market share. However, solar is expanding at 18.24% CAGR, the fastest among technologies, because bifacial modules and trackers improve yields in snow-covered southern Sweden and Denmark. Offshore wind clusters in Danish and Norwegian waters account for most new capacity, aided by energy-island concepts that aggregate exports via HVDC cables. Pumped-storage feasibility studies using abandoned mines may unlock eight-hour storage, yet capital intensity and decade-long build timelines stall near-term decisions. Geothermal beyond Iceland remains niche, but Sweden's 3 MW Västerås pilot confirmed technical viability in crystalline bedrock, hinting at long-term diversification.

Bioenergy's role is shifting from baseload to mid-merit. Fortum retrofitted 12 plants in 2024 to ramp 40% faster, and data-center waste-heat capture trims feedstock costs. Ocean energy trials in Norway reached only 1.5 MW amid grid-connection expenses topping EUR 4 million/MW. Overall, hydropower will continue to anchor flexibility, but multi-technology hybrids and solar outperformance will propel the Nordic countries' renewable energy market size over the forecast period.

By End-User: Utilities Dominate, Industrials Accelerate

Utilities owned 66.10% of 2025 capacity through long-term hydropower concessions and offshore-wind seabed leases, underscoring their scale advantages in the Nordic countries' renewable energy market. Nevertheless, commercial and industrial demand is forecast to rise 10.55% annually, outpacing utility growth. SSAB's 1.2 GW PPA with Vattenfall to power hydrogen-based steel represents the largest single industrial offtake to date. Hyperscale data centers executed 2.4 GW of PPAs in 2024, lured by sub-EUR 35/MWh prices and free-cooling economics. Aluminum smelters in Norway and Iceland are adding load-flex technologies that monetize balancing services, boosting returns without sacrificing metal quality. Residential solar uptake stays muted under wholesale-only net-metering, but battery prices below EUR 150/kWh after 2027 could unlock rooftop growth.

Geography Analysis

Sweden retained 36.20% of total capacity in 2025, drawing on robust hydropower and steady onshore wind additions. Cross-border cables enable the export of surplus generation, and planned offshore projects will further increase variable output. Despite some wind farms operating at a loss during 2024, falling capital expenditures and more accurate forecasting are improving margins. The nation’s untapped geothermal potential could introduce a fresh dispatchable option.

Finland posts the strongest 11.95% CAGR outlook to 2031. The Nurmo liquefied biogas plant confirms diversification beyond hydro and wind, while North’s data center cluster utilizes waste heat for district heating, creating a stacked revenue stream. Strategic interconnectors with the Baltic position Finland as a renewable export bridge into continental Europe.

Denmark continues to lead in technology export and offshore wind know-how. A 2025 reform increased CO₂ taxes on fossil fuels by over 400%, tilting the economics decisively in favor of renewables. Norway’s deep hydropower reserve provides Europe’s key balancing resource; however, political turbulence following the 2025 coalition collapse clouds long-term project certainty. Iceland’s geothermal innovation pipeline, spearheaded by direct magma drilling, can reshape global high-enthalpy markets.

Competitive Landscape

The Nordic countries' renewable energy market features a moderate concentration with dominant incumbents counterbalanced by agile specialists. Ørsted, Vattenfall, and Statkraft leverage multi-technology portfolios and established grid access. Their strategies include upgrading existing hydropower, integrating AI for geothermal optimization, and exploring hybrid offshore concepts, such as wave-wind arrays. Vertical integration into green hydrogen is gaining traction, exemplified by Ørsted's bid to co-locate electrolysers at offshore hubs.

Private equity inflows accelerate consolidation. Nordic Capital's rise to lead shareholder status in Soltech demonstrates financial players' appetite for scalable solar platforms. Asset sweeps by Renewable Power Capital and VINCI signal the pursuit of larger project pipelines to capture economies of scale. Meanwhile, technology-led entrants focus on turbine recycling, floating foundations, and long-duration storage, seeking niches where incumbents hold less advantage.

Government-backed entities, such as Norges Bank Investment Management, co-invest with corporates like RWE, reflecting an increasing sovereign interest in stable renewable returns. Market participants who master integrated solutions—combining generation, flexibility services, and sector-coupled products—are best placed to thrive as the Nordic countries' renewable energy market moves toward cross-sector decarbonization.

Nordic Countries Renewable Energy Industry Leaders

Vattenfall AB

Fortum Oyj

Ørsted A/S

Statkraft AS

Equinor ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Nordic Capital has secured its position as the largest shareholder in Soltech Energy Sweden AB by executing an all-share acquisition of Sesol Group AB.

- March 2025: RWE and Norges Bank Investment Management (NBIM) have joined forces on the Nordseecluster and Thor offshore wind initiatives. NBIM has taken a 49% stake in both ventures, while RWE retains a 51% stake and, according to RWE, will oversee construction and operations.

- March 2025: Renewable Power Capital (RPC), a pan-European renewables firm, has acquired Njordr AS's onshore wind and solar development businesses in Sweden and Finland.

- January 2025: RWE has granted Aker Solutions and Siemens Energy the green light to commence work on the Norfolk Vanguard West and East offshore wind farm projects.

Nordic Countries Renewable Energy Market Report Scope

Renewable energy is energy derived from natural sources that are replenished at a faster rate than they are consumed. Sunlight and wind, for example, are such sources that are constantly replenished. For each segment, the market sizing and forecasts have been done based on installed capacity in gigawatts (GW). The Nordic Countries Renewable Energy Market report includes:

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

| Utilities |

| Commercial and Industrial |

| Residential |

| Norway |

| Sweden |

| Denmark |

| Finland |

| Iceland |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential | |

| By Geography | Norway |

| Sweden | |

| Denmark | |

| Finland | |

| Iceland |

Key Questions Answered in the Report

How large is the Nordic countries renewable energy market in 2026?

It stands at 129.99 GW of installed capacity and is projected to reach 183.7 GW by 2031.

What CAGR is expected for Nordic renewable capacity between 2026 and 2031?

The forecast CAGR is 7.15% over the 2026-2031 period.

Which technology is growing fastest in the Nordics?

Solar photovoltaics lead with a projected 18.24% CAGR to 2031.

Why are corporate PPAs booming in the region?

The EU Fit-for-55 package, low wind and solar LCOEs, and carbon-border-adjustment risks are driving industrial buyers to lock in green electricity.

Which Nordic country will grow capacity quickest to 2031?

Finland, supported by CfD auctions and newly upgraded 400 kV transmission lines, is forecast to expand at 11.95% CAGR.

How concentrated is competitiveness among utilities?

Five vertically integrated utilities control about 60% of the pipeline, yielding a moderate concentration score of 6.

Page last updated on: