Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

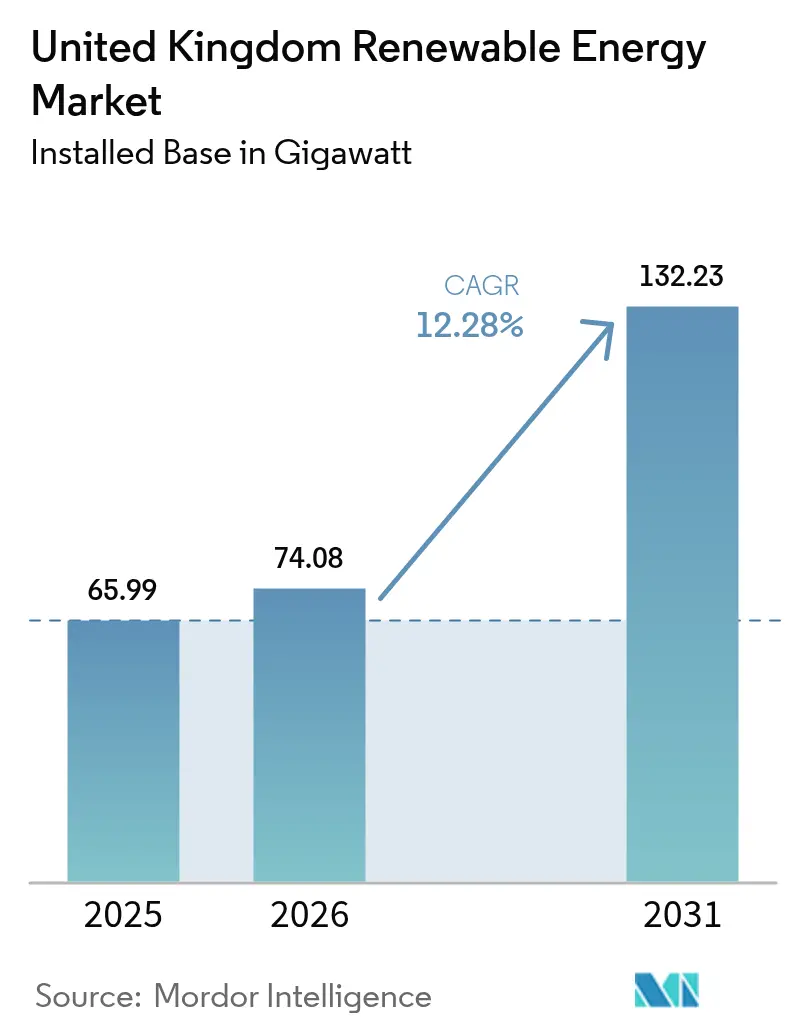

| Base Year Market Size (2025) | 65.99 gigawatt |

| Market Volume (2026) | 74.08 gigawatt |

| Market Volume (2031) | 132.23 gigawatt |

| Growth Rate (2026 - 2031) | 12.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Renewable Energy Market Analysis by Mordor Intelligence

The United Kingdom Renewable Energy market size is expected to grow from 65.99 gigawatt in 2025 to 74.08 gigawatt in 2026 and is forecast to reach 132.23 gigawatt by 2031 at 12.28% CAGR over 2026-2031.

The acceleration is anchored in the Clean Power 2030 Action Plan, unprecedented private capital inflows exceeding GBP 60 billion per year, and renewables already supplying 46.4% of national electricity in 2024, surpassing gas for the first time.[1]DESNZ, “Digest of UK Energy Statistics 2024 – Electricity Chapter,” assets.publishing.service.gov.uk Consistent Contracts-for-Difference (CfD) auctions, rising corporate power-purchase agreements, and grid modernization funds amplify momentum for the UK renewable energy market, while ongoing cost declines in floating offshore wind and electrolyzer systems widen the addressable resource pools. Even with connection bottlenecks and post-Brexit supply chain pressures, investor confidence remains high as Ofgem prioritizes ready-to-build schemes, and government grants bolster local manufacturing.

Key Report Takeaways

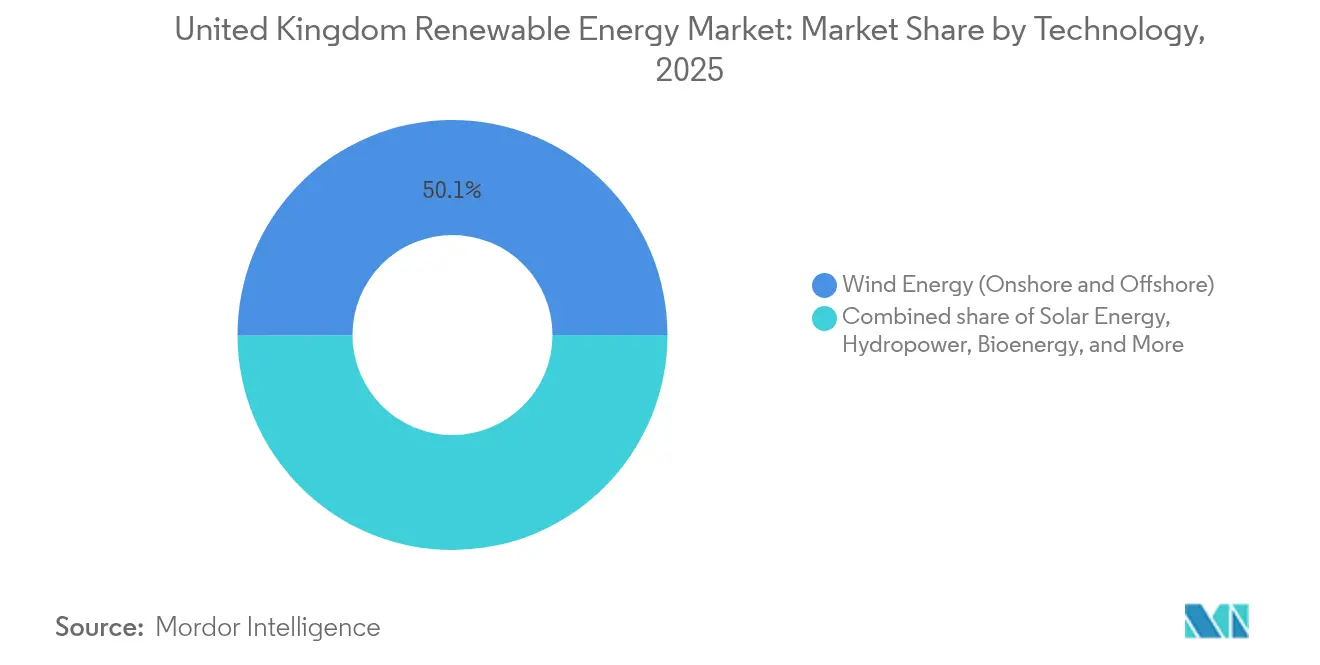

- By technology, wind captured 50.05% of the UK renewable energy market share in 2025; ocean energy is forecast to surge at a 72.9% CAGR through 2031.

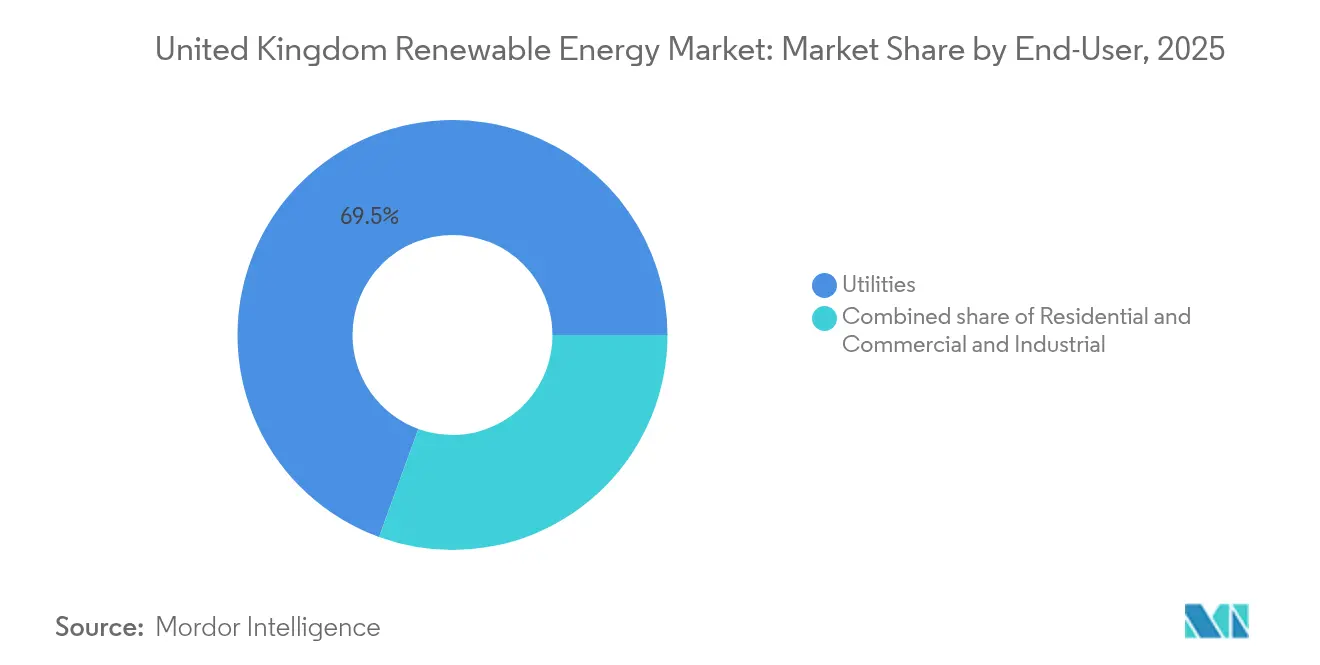

- By end-user, utilities commanded 69.45% of the UK renewable energy market size in 2025, whereas residential installations are projected to advance at an 18.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Offshore-wind CfD Strike-Price Declines Accelerating North-Sea Pipeline | +3.2% | Scotland, North Sea regions, Yorkshire Coast | Medium term (2-4 years) |

| Contracts-for-Difference (CfD) Scheme Providing Revenue Certainty | +2.8% | England, Scotland, Wales | Long term (≥ 4 years) |

| Rise of Corporate PPAs from UK Data-Centre & Heavy-Industry Off-takers | +2.1% | England core, spill-over to Scotland | Medium term (2-4 years) |

| Ofgem RIIO-ED2 Grid-Upgrade Commitments Boosting Distributed Solar | +1.7% | England, Wales distribution networks | Short term (≤ 2 years) |

| Green-Hydrogen Strategy Linking Electrolyser Build-out to Renewables | +1.4% | Scotland, Humber region, Wales | Long term (≥ 4 years) |

| Cost Drop in Floating Offshore Turbines for Deep-water Scottish Sites | +1.1% | Scotland deep waters, North Sea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Offshore-wind CfD strike-price resets accelerating the North Sea pipeline

The government lifted strike prices to GBP 73/MWh for fixed-bottom and GBP 176/MWh for floating projects after the Allocation Round 5 stalemate, unlocking 5.3 GW in Allocation Round 6 and re-energizing the 40 GW development queue. Predictable 6-8 GW annual CfD rounds, coupled with a Clean Industry Bonus worth up to GBP 200 million, de-risk domestic blade factories and port upgrades, further strengthening the UK renewable energy market.[2]Department for Energy Security and Net Zero, “Clean Power 2030 Action Plan,” gov.uk

CfD scheme providing revenue certainty

More than 25 GW of operational capacity benefits from 15-year indexed contracts that protect both developers and consumers from spot-price fluctuations. Eligibility now spans tidal stream, floating wind, and green hydrogen, signaling a policy toolbox designed to future-proof the UK renewable energy market.

Corporate PPAs from UK data-centre and heavy-industry off-takers

ENGIE’s 473 MW Moray West deal with Amazon and Tesco’s 373 MW Cleve Hill solar agreement exemplify how sustainability mandates supply bankable offtake for new assets. As AI-driven data loads climb, the UK renewable energy market gains a stable demand floor insulated from typical recessions.

Ofgem RIIO-ED2 grid-upgrade commitments boosting distributed solar

GBP 25 billion earmarked for 2023-2028 funds real-time monitoring, automated switches, and battery pilots, cutting average connection lead times for sub-100 kW systems by half and accelerating the residential share of the UK renewable energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National-Grid Queue Bottlenecks Causing 5-year Connection Delays | -2.8% | England transmission network, Scotland interconnections | Short term (≤ 2 years) |

| Reduced Smart-Export-Guarantee Tariff Hitting Rooftop Solar ROI | -1.3% | England, Wales residential markets | Medium term (2-4 years) |

| Offshore-Wind Monopile Cost Inflation Post-Brexit Steel Tariffs | -0.9% | North Sea offshore projects | Medium term (2-4 years) |

| Visual-Impact Objections Stalling Onshore Wind Permitting | -0.6% | England rural areas, Wales uplands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Grid queue bottlenecks causing five-year connection delays

The queue ballooned to 739 GW, ten times the 2020 levels, forcing some assets to be assigned to 2035 slots. Ofgem’s TMO4+ “first ready, first connected” reform removes speculative placeholders and could free up 500 GW.[3]National Grid ESO, “Two-step offers process update,” nationalgrideso.com Yet, construction of the GBP 4.3 billion Eastern Green Link 2 will not be completed until 2029, keeping pressure on the near-term buildout of the UK renewable energy market.

Reduced Smart-Export-Guarantee tariff hitting rooftop solar ROI

Average SEG payments have slipped below 10 p/kWh, extending paybacks to 12-15 years for systems without batteries, slowing the residential slice of the UK renewable energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Wind leadership challenged by an ocean-energy revolution

Wind remains the anchor of the UK renewable energy market, supplying 50.05% of 2025 output and earning the largest UK renewable energy market share through high-capacity-factor offshore arrays, such as the 3.6 GW Dogger Bank complex. Yet, ocean energy promises a 72.9% CAGR between 2026 and 2031, catapulting tidal-stream pioneers from demonstrators to bankable assets as CfD carve-outs guarantee price floors. Government R&D grants and predictable export-credit financing shrink levelized costs, raising the UK renewable energy market size for marine technologies and attracting supply-chain investment in coastal hubs from Aberdeen to Cornwall. Solar continues its steady expansion through mandatory rooftop rules starting in 2025, while bioenergy transitions toward carbon-negative configurations under new BECCS trials. Hydropower’s pumped-storage reservoirs add flexibility that mitigates intermittency, and early-stage geothermal pilots diversify the portfolio without diluting wind’s core position in the UK renewable energy market.

Second-generation wave converters and array-scale tidal turbines utilize modular production, reducing both balance-of-plant and installation risks. These learning-curve benefits, when stacked with hydrogen offtake contracts, make ocean assets a compelling hedge within the broader UK renewable energy market size outlook to 2030 and beyond.

By End-User: Utility dominance with residential acceleration

Utilities owned 69.45% of delivered green electricity in 2025, leveraging CfD portfolios and regulated-asset returns to maintain the largest UK renewable energy market share across buyer categories. Long-dated offtake visibility and balance-sheet strength allowed them to bid aggressively in Allocation Round 7, cementing control of mega-scale offshore arrays and multi-gigawatt solar parks. The commercial and industrial cohort leverages corporate PPAs to lock in power costs at inflation-adjusted price indices, ensuring a growing but measured penetration.

Residential uptake, however, posts an 18.25% CAGR as building-code mandates for solar, GBP 7,500 heat-pump grants, and time-of-use tariffs converge. Vehicle-to-grid programs and peer-to-peer trading further empower households, raising the UK renewable energy market size attributed to prosumers. Utilities respond by aggregating rooftop PV into virtual power plants, retaining their system-balancing roles even as customer meters generate more on-site power. The two-way engagement ultimately broadens the UK renewable energy market without eroding the relevance of incumbent utilities.

Geography Analysis

Scotland dominates generation volumes, with more than 60% of installed offshore capacity, thanks to the 851 MW Seagreen project and the emerging 2 GW MachairWind project, which are credited with displacing upward of 2 million tCO₂ each year. Floating-wind readiness, abundant tidal flows, and a pro-renewables planning ethos consolidate Scotland’s leadership. The GBP 4.3 billion Eastern Green Link 2 direct-current cable enhances export capability to English load centers, further integrating regional surpluses into the UK renewable energy market.

England spearheads solar deployment and corporate PPA activity; the 2.9 GW East Anglia Hub alone represents GBP 10 billion of capital and 7.5% of the 40 GW national offshore goal. Onshore wind obstacles keep greenfield momentum modest, yet battery co-location and hydrogen pilots maintain investment vitality across coastal industrial clusters.

Wales leverages its mountainous topography for onshore wind and pumped-storage retrofits, with tidal pilots off Anglesey broadening its renewable energy palette. Northern Ireland participates via the Integrated Single Electricity Market, exporting wind surpluses to the Republic and carving a niche in small-scale solar aggregation. Collectively, these regional vectors ensure the UK renewable energy market remains both geographically diverse and nationally coordinated.

Regulatory Landscape

The United Kingdom renewable energy market operates under a policy-and-regulatory stack led by the Department for Energy Security and Net Zero (DESNZ) and Ofgem, with long-lived revenue support anchored in Contracts for Difference (CfD) and legacy schemes such as the Renewables Obligation (RO). In July 2025, the government response on further CfD reforms for Allocation Round 7 (AR7) formalized process changes, including separating offshore wind from other technologies (AR7 and AR7a). The stated aim was to streamline delivery and reduce delays linked to appeals and administrative complexity.

In 2026, the framework tightened around planning, disclosure, and indexation. DESNZ published the updated National Policy Statement for renewable energy infrastructure (EN-3, 2025), reinforcing the nationally significant infrastructure planning route for large projects. Ofgem also issued 2026 guidance on Renewable Energy Guarantees of Origin (REGOs) for Great Britain Fuel Mix Disclosure. For RO compliance economics, the Renewables Obligation (Amendment) Order 2026 (SI 2026/380) implemented a shift in RO buy-out price and mutualisation cap indexation from RPI to CPI, with Ofgem detailing scheme operation and the transition in its RO annual reporting.

Competitive Landscape

Market concentration is moderate: SSE Renewables, Ørsted, and ScottishPower hold sizeable offshore pipelines, but foreign majors like Equinor and TotalEnergies accelerate entries through targeted deals. SSE’s GBP 17.5 billion Net Zero Acceleration Programme finances hybrid wind-battery clusters, reinforcing its prime seat within the UK renewable energy market. Ørsted’s pivot from Hornsea 4 underscores cost-inflation realities, yet the firm still commands more than 10 GW globally and is adding a 600 MWh storage unit to Hornsea 3.[5]Ørsted A/S, “Global offshore portfolio,” orsted.com

TotalEnergies bought 435 MW of solar-plus-battery assets from Low Carbon in June 2025, signaling multi-technology ambition. Iberdrola’s EUR 5 billion purchase of Electricity North West couples renewable output with grid ownership, creating synergies others may emulate. Equinor channels North Sea engineering heritage into floating foundations, while Octopus Energy scales retail capital into operational offshore stakes, exemplified by its East Anglia One entry.

Technology differentiation shapes advantage: floating-wind patents, hydrogen partnerships, and digital-twin O&M drive scoring opportunities beyond raw megawatts. The public launch of Great British Energy, armed with £8.3 billion, adds mission-driven capital to underserved community schemes, providing a counterbalance to established developer oligopolies in the UK renewable energy market.

United Kingdom Renewable Energy Industry Leaders

SSE Renewables

Ørsted A/S

ScottishPower Renewables

RWE Renewables

Vattenfall AB

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Auction-backed offshore wind awards and consenting progress continue to open near-term whitespace across the UK renewable energy market, especially for large-scale offshore buildout and the supporting segments around it, including ports, O&M, and the supply chain. The UK government published the official Contracts for Difference Allocation Round 7 results, and developers publicized multi-gigawatt awards. RWE secured CfDs for 6.9 GW of offshore wind across multiple projects, while SSE received a CfD for the first 1.4 GW phase of Berwick Bank, with the broader project exceeding 4 GW. Alongside revenue support, project advancement through planning milestones adds additional pipeline visibility, including development consent for the 1.5 GW Outer Dowsing offshore wind farm.

Grid integration and flexibility are a second opportunity axis being shaped through policy and system planning. The July 2026 update to the Clean Flexibility Roadmap provides a programmatic basis for scaling flexibility alongside renewables, and Ofgem, DESNZ, and NESO have been advancing connections and strategic planning reforms through 2026 initiatives. The Reformed National Pricing delivery plan, published in 2026, introduces a locational and siting lever to the investment environment, linking new capacity decisions to a broader strategic spatial planning process. This can translate into implementation demand for developers and investors to pair generation with storage, grid services, or better-sited capacity aligned to network constraints.

Recent Industry Developments

- June 2026: ScottishPower Renewables submitted a Section 36 consent application to the Scottish government for the 2 GW MachairWind offshore wind farm. The filing advances a large Scotland-led offshore pipeline that is central to UK capacity additions and increases demand for marine, ports, and grid-enabling services tied to project development.

- May 2026: SSE Renewables received development consent from DESNZ for the 57-turbine, 1 GW North Falls offshore wind farm. Moving into the consented stage reduces planning risk and supports a clearer path toward procurement and construction activity in the UK offshore wind supply chain.

- June 2025: TotalEnergies acquired 435 MW of UK solar and storage projects from Low Carbon. The deal strengthened TotalEnergies presence in UK renewables and showed ongoing appetite for multi-technology portfolios that combine generation with storage to manage grid and merchant exposure.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers renewable electricity generation capacity in the United Kingdom, measured in installed capacity (GW) across renewable technologies connected to the grid and tracked through commissioning and operational status.

Scope exclusions: We exclude fossil-based generation, nuclear, and most behind-the-meter systems that are not consistently captured in national capacity series.

Segmentation Overview

- By Technology

- Solar Energy (PV and CSP)

- Wind Energy (Onshore and Offshore)

- Hydropower (Small, Large, PSH)

- Bioenergy

- Geothermal

- Ocean Energy (Tidal and Wave)

- By End-User

- Utilities

- Commercial and Industrial

- Residential

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the fact base for capacity additions, operating fleet, and policy timing that affect build rates in the United Kingdom. We mainly rely on public energy statistics and regulatory releases updated on a predictable schedule, which helps keep the history consistent across technologies.

Typical sources include government and regulator publications such as the UK Department for Energy Security and Net Zero releases, National Grid ESO data portals, Ofgem registers, and ONS energy and economy series, along with technology notes from groups such as IEA and IRENA. Company annual reports, project announcements, planning and consenting disclosures, and reputable press are also reviewed to confirm commissioning dates and cancellations. When needed, we use paid subscriptions for company financials and intelligence, and a patent database to track where innovation activity is picking up. The desk sources listed here are not exhaustive, and we use additional public references for cross-checks, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to test what the desk numbers mean in real project pipelines in the United Kingdom, and to pressure-check build assumptions before they go into the model. We interview and survey developers, EPCs, utilities, grid and storage adjacencies, and large buyers, covering the full United Kingdom footprint so regional permitting, grid queues, and supply constraints are reflected in the final view.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | |

| Mid tier: 55% | Functional/Unit leaders: 36% | |

| Smaller Players: 15% | Managers: 50% |

Market-Sizing & Forecasting

Sizing starts from a top-down reconstruction of the installed renewable capacity base using national capacity time series, commissioning schedules, and known retirements, which are then mapped into a consistent GW view for the study period. We then corroborate totals with selective bottom-up approximations, such as rolling up sampled project pipelines by technology, applying typical capacity factors as a reasonableness check, and sanity-checking implied build rates against supply chain and connection constraints.

Key inputs used in the model include annual and quarterly capacity additions, grid connection and queue indicators, auction and contract award volumes, average project lead times from consent to commissioning, and the observed split between repowering and greenfield builds. For forecasting, scenario analysis is applied so policy outcomes and grid readiness can be reflected without overfitting, and then expert consensus is used to choose the most realistic path. Where project-level data is incomplete, gaps are handled through technology-specific build-rate ranges that are tightened using interview feedback and recent commissioning evidence.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as published capacity totals, recent commissioning newsflow, and the implied pace of annual additions by technology, which are reviewed for spikes that do not match policy or grid reality in the United Kingdom. If a variance is detected, assumptions are re-tested, and follow-up calls are triggered with relevant respondents to confirm whether the change is real or data timing related.

Before sign-off, the work goes through multi-step analyst review so definitions, units, and conversions are consistent across the full history and forecast. Reports are refreshed annually, and interim updates are made when material events occur (for example, major auction outcomes or regulatory changes). Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's United Kingdom Renewable Energy Market Size Versus Other Published Estimates

Published estimates for the United Kingdom renewable energy market can look far apart because authors do not always measure the same thing, even when the report title sounds identical. The biggest driver is usually the unit of measurement, followed by what parts of the value chain are counted, and then how future build rates are translated into a single headline figure.

Key gap drivers show up quickly in this market because capacity (GW), generation (TWh), and economic value (revenue or turnover) can each be presented as a market size depending on the study aim. The other common causes are whether corporate turnover across low-carbon activities is mixed with pure renewable generation, whether price assumptions are used to convert electricity or equipment into USD, and whether the history and forecast are aligned to the same policy calendar and currency timing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 65.99 B (2025) | |

| Industry Research Publisher A | USD 23.86 B (2024) | This figure is reported as a revenue value, so it depends on pricing and value-chain boundaries, and it is not a direct read of installed capacity in GW. |

| National Statistics Body B | USD 77.00 B (2024) | This number represents economy-wide turnover across low-carbon and renewable activities, so it can include wider goods and services beyond renewable generation capacity. |

Capacity additions tracked in official energy statistics, along with commissioning and retirement checks from project evidence, are the anchors that keep Mordor Intelligence tied to an installed GW definition instead of mixing in revenue turnover. In practice, the spread in the table mostly comes from unit choice and boundary setting, and we keep ours repeatable by sticking to clear capacity series and then validating build assumptions with field feedback.

Key Questions Answered in the Report

How large is the UK renewable energy market in 2026?

Installed capacity stands at 74.08 GW, with a roadmap to 132.23 GW by 2031.

Which technology currently dominates UK renewables?

Wind contributes 50.05% of national green generation, led by offshore projects.

Why are grid queues delaying projects?

A 739 GW application backlog strains legacy transmission corridors, though Ofgem’s TMO4+ reform is reprioritizing shovel-ready assets.

How fast is residential solar expanding?

Home installations are growing at an 18.25% CAGR as rooftop mandates and heat-pump incentives align.

What role do corporate PPAs play?

Long-term contracts with data-centre and retail giants guarantee revenue streams, often rivaling CfD prices.

Who are the leading market players?

SSE Renewables, Ørsted, and ScottishPower dominate, while Equinor and TotalEnergies increase stakes through acquisitions and floating-wind expertise.

Page last updated on: