Non-Dispersive Infrared (NDIR) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

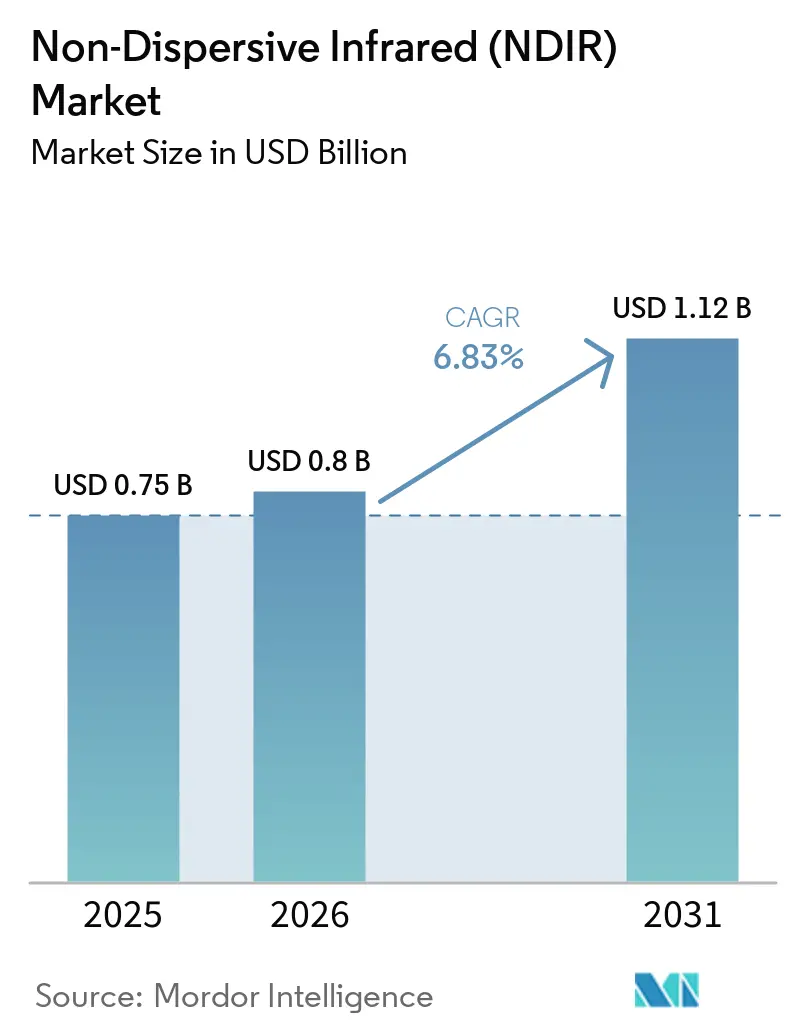

| Market Size (2026) | USD 0.8 Billion |

| Market Size (2031) | USD 1.12 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-Dispersive Infrared (NDIR) Market Analysis by Mordor Intelligence

The Non-Dispersive Infrared market size is projected to expand from USD 0.75 billion in 2025 and USD 0.80 billion in 2026 to USD 1.12 billion by 2031, registering a CAGR of 6.83% between 2026 and 2031. Steady demand is rooted in mandatory indoor-air-quality (IAQ) laws, the growing use of edge analytics in sensor nodes, and the migration of NDIR modules from plant floors into consumer devices and vehicle cabins. Continuous CO₂ monitoring has become the default compliance path for school districts in California, metro offices in Beijing, and Pearl-rated towers in Abu Dhabi, keeping specification pipelines full. Larger facilities are moving toward Thread-enabled self-healing sensor networks that cut installation labor by 30%. Competitive pricing from high-volume Asian manufacturers is accelerating adoption in smart thermostats, while incumbents defend margins by offering 10-year calibration-free warranties and on-chip neural networks.

Key Report Takeaways

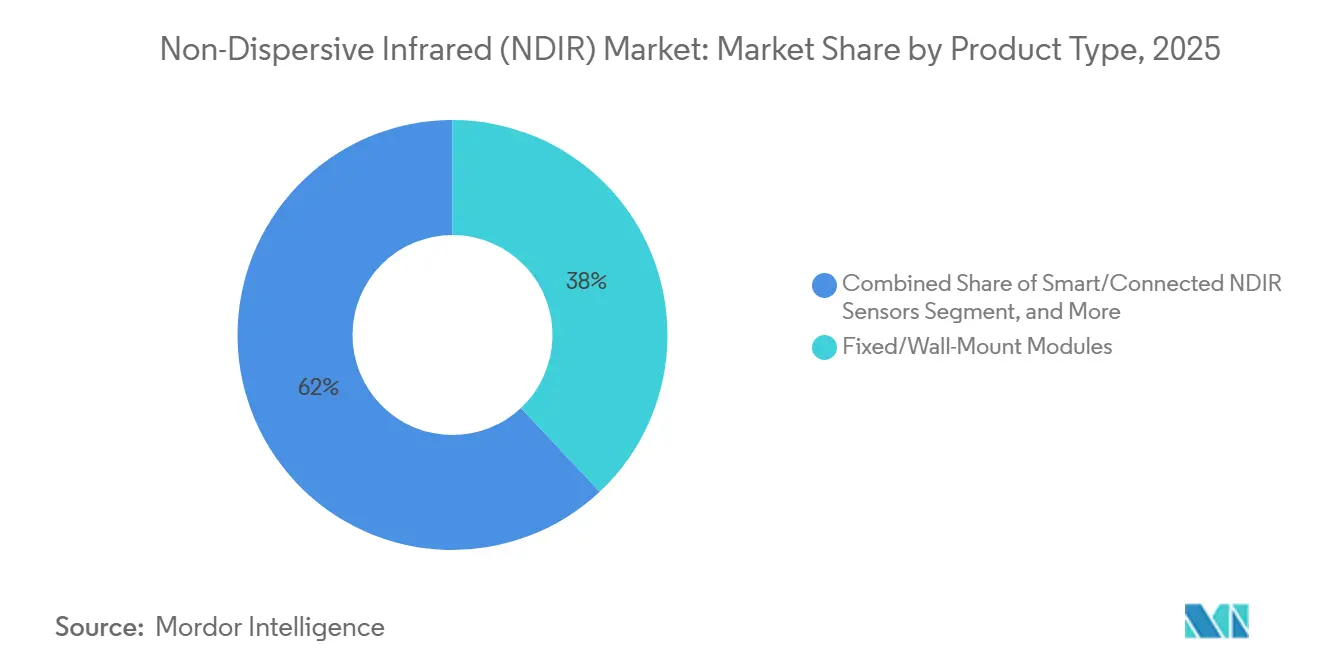

- By product type, fixed and wall-mount modules held a 38.00% share of the Non-Dispersive Infrared market in 2025, while smart and connected sensors are forecast to grow at a 7.31% CAGR to 2031.

- By gas detected, carbon dioxide accounted for 46.00% of revenue in the NDIR market in 2025, and refrigerant monitoring is advancing at a 7.78% CAGR through 2031.

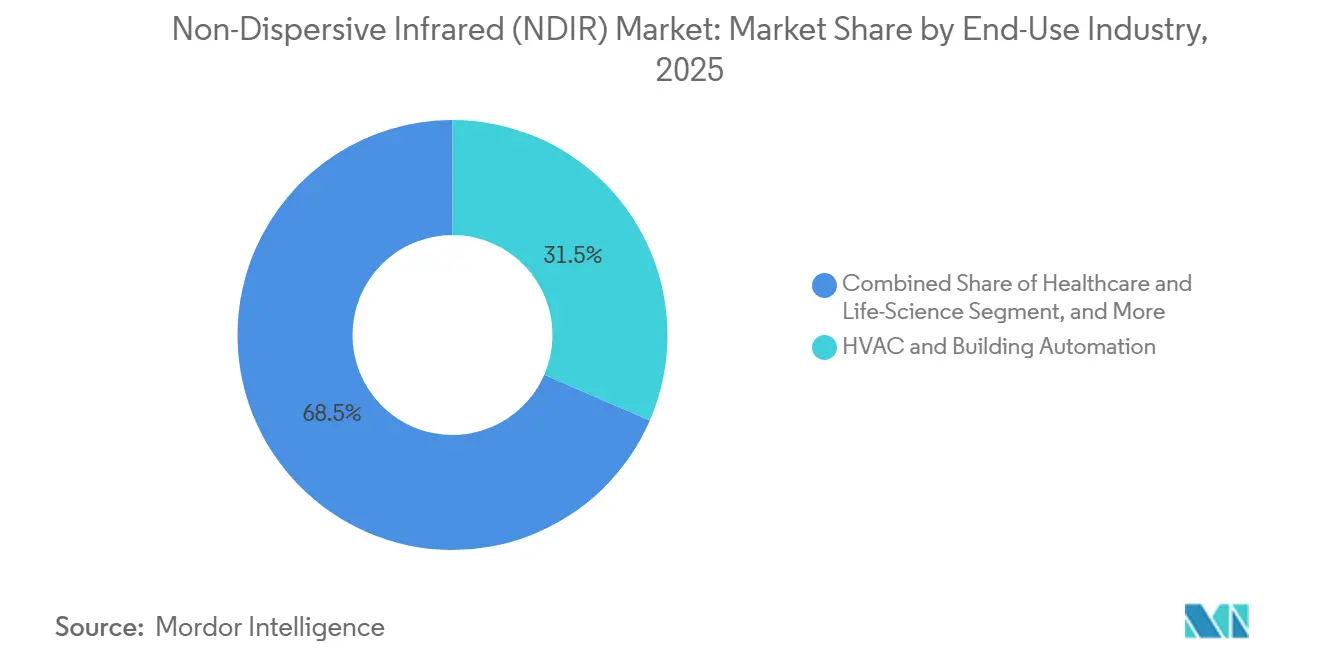

- By end-use industry, HVAC and building automation captured 31.50% share of the Non-Dispersive Infrared market in 2025, whereas healthcare and life-science applications are projected to post a 7.38% CAGR.

- By platform, module-level sensors commanded 44.20% of the market share in 2025, yet PCB-mount chips are poised for a 7.43% CAGR.

- By geography, Asia-Pacific led the Non-Dispersive Infrared market with 42.80% revenue share in 2025, and the Middle East is poised to expand at a 7.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Non-Dispersive Infrared (NDIR) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying IAQ Regulation in Commercial Buildings | +1.2% | Global with faster rollouts in North America, Europe, China | Short term (≤ 2 years) |

| Stricter Automotive and Industrial Emission Norms | +1.0% | Europe, United States, China | Medium term (2-4 years) |

| Accelerated HVAC Automation and Smart Thermostat Uptake | +0.9% | North America, Europe, Asia-Pacific urban clusters | Short term (≤ 2 years) |

| Edge-AI NDIR Modules Enabling On-Sensor Analytics | +0.7% | Early adoption in North America and the Europe | Medium term (2-4 years) |

| Carbon Pricing Driving Continuous Methane Monitoring | +0.6% | North America, Europe, Middle East oil producers | Medium term (2-4 years) |

| Bluetooth 5.3 Power Budgets for Wearables | +0.4% | Nascent penetration in the Asia-Pacific and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying IAQ Regulation in Commercial Buildings

School boards, ministries of health, and green-building councils are converging on permanent CO₂ sensing as a proxy for ventilation. California’s AB 2232 requires classrooms to use devices with ±75 ppm accuracy and requires yearly verification, and similar statutes are emerging in seven other US states.[1]California Legislative Information, “Assembly Bill 2232,” leginfo.legislature.ca.gov China lowered the permissible indoor CO₂ ceiling to 800 ppm in 2023, driving retrofits across roughly 30 billion m² of floor space. Market preference is shifting toward modules with automatic baseline correction that hold drift below ±50 ppm across five years. Vendors promoting self-healing mesh networks under the Matter standard are winning retrofit bids by avoiding proprietary gateways.

Stricter Automotive and Industrial Emission Norms

Euro 7 and EPA Tier 4 standards extend monitoring from tailpipes to cabin air and factory stacks. Automakers now embed NDIR CO₂ sensors in electric-vehicle HVAC loops to balance battery drain with occupant comfort. On the industrial side, new methane caps require quarterly leak checks at 0.40 kg h-¹ sensitivity, opening a replacement cycle for portable analyzers that previously used pellistors. Suppliers that can certify to the -40 °C to +80 °C operating range without sacrificing ±200 ppm accuracy are securing multi-year supply agreements with Tier 1 system integrators.[2]Sensirion AG, “SCD43 Datasheet,” sensirion.com

Accelerated HVAC Automation and Smart Thermostat Uptake

Demand-controlled ventilation reduces energy use by 20%-40 % by matching outside-air intake to occupancy.[3]ASHRAE, “Humidity Effects on NDIR Performance,” ashrae.org The Mass-market launch of Matter-ready thermostats in 2025 eliminated the need for vendor-specific hubs, lowering adoption barriers for small businesses. Thread mesh networks allow up to 250 sensors to auto-organize, slashing wiring costs in 1970s-era buildings rewired for LEED upgrades. Hospitals and hotels are installing 10-year-life NDIR modules that forward fault codes to building-management software, reducing truck rolls and unplanned downtime.

Edge-AI NDIR Modules Enabling On-Sensor Analytics

TinyML models running on ARM Cortex-M0+ cores now perform drift prediction, anomaly detection, and auto-calibration directly on the module. Sensirion’s 2026-bound SCD53 claims ±30 ppm stability over a decade without cloud recalibration. Offshore oil platforms value instant alarms without satellite latency, so edge processing is a selling point. Dual-wavelength designs that distinguish water-vapor interference in humid tropics are also feeding training data into embedded neural networks, further improving field accuracy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Erosion and Sensor Commoditization | -0.8% | Most acute in Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Performance Drift in Harsh Temperature and Humidity | -0.6% | Middle East, tropical Asia, Arctic field installations | Short term (≤ 2 years) |

| Helium Shortage Impacting Calibration Gas Supply | -0.4% | North America and Europe | Medium term (2-4 years) |

| Growing Adoption of Long-Wave TDLAS and Photoacoustic Techniques | -0.5% | High-precision plants in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Erosion and Sensor Commoditization

Average selling prices for basic 5 000 ppm CO₂ modules dropped below USD 20 in 2025, led by large-scale producers in Shenzhen.[4]Winsen Electronics, “MH-Z19C Product Sheet,” winsen-sensor.comGross margins for Western firms tightened to low-20% territory, encouraging them to bundle firmware analytics and calibration services as subscription offerings. RESET and Title 24 certifications remain differentiators in enterprise bids, allowing premium models to keep double-digit price deltas, yet consumer IoT buyers overwhelmingly select the least-cost-compliant option.

Performance Drift in Harsh Temperature and Humidity

Relative humidity above 90% and ambient swings beyond -20 °C to +60 °C accelerate baseline drift to ±50 ppm per year or worse. Condensation inside optical cavities skews readings, shortening calibration cycles in cold storage, tropical farms, and desert stadiums. Advanced modules add hydrophobic membranes and active heaters, but these features increase the bill of materials by USD 15 per unit, limiting adoption in price-sensitive markets. Self-calibrating algorithms help, but accuracy degrades at sites where CO₂ remains elevated for long periods, such as fermentation tanks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Connectivity Reshapes Installation Economics

Smart and connected units gained momentum, with a CAGR of 7.31% over the forecast period, as facility managers pursued predictive maintenance capabilities. Although fixed and wall-mount modules dominated the Non-Dispersive Infrared market share at 38.00% in 2025, cloud-ready models are the only category consistently outselling the baseline growth rate. Their wireless firmware updates curb technician visits, and Thread networking lets contractors install 30% fewer repeaters. Portable analyzers retain relevance for occupational safety audits, especially models certified to SIL2 that meet refinery turnaround schedules. Industrial rack analyzers benefit from explosion-proof enclosures that meet ISO 14064 compliance requirements, making them a staple of petrochemical megasites.

Vendors are pivoting toward sensor-as-a-service agreements that bundle hardware, calibration, and dashboards for one monthly fee. Sensirion’s Wi-Fi-enabled SCD43 illustrates how automatic compliance reports reduce paperwork under WELL and Title 24 rules. Matter interoperability has ended vendor lock-in, opening retrofit work to local electricians rather than proprietary installers. Portable devices now ship with rechargeable lithium-ion packs that last a full workweek, solving past runtime complaints. Industrial analyzers leverage edge AI to detect fouling early and prevent unplanned shutdowns that cost millions in lost throughput.

By Gas Detected: Refrigerant Monitoring Gains Urgency

Carbon dioxide held the revenue anchor at 46.00% in 2025, yet growth stalled near the overall Non-Dispersive Infrared market average. Refrigerant sensing, growing at 7.78% CAGR, now captures capital allocated to comply with F-Gas and Kigali deadlines. The segment requires narrow-bandpass optics to separate R-1234yf from water vapor, adding design complexity but opening premium pricing. Hydrocarbon modules are moving from catalytic pellistors to NDIR, a safer option in high-H₂S fields where sparks are unacceptable. Medical-gas monitors meet ISO 80601 mandates in operating rooms, a small but margin-rich niche that requires ±0.3 vol-% accuracy.

Honeywell’s dual-wavelength hydrocarbon sensor compensates for humidity error in real time, achieving ±5% precision across 5 000 ppm. Greenhouse operators are buying 20 000 ppm-range modules that keep readings within ±50 ppm despite 95% relative humidity. Oil producers accept higher list prices if a device negates the need for quarterly calibration gas, because logistics dominate total cost offshore. Anesthetic-gas instruments are drifting away from sidestream sampling toward mainstream sensors mounted directly in the airway, eliminating lag that complicates pediatric procedures.

By End-Use Industry: Healthcare Emerges As Growth Leader

HVAC and building automation accounted for 31.50% of 2025 revenue, yet healthcare and life-science deployments posted the fastest 7.38% CAGR through 2031. Hospital administrators now require real-time capnography in every emergency bay, a leap from the prior one per operating room. Schools, hotels, and coworking spaces still form the backbone of the installation, partly financed by US Inflation Reduction Act tax credits that refund up to 30% of sensor retrofit costs. Industrial users integrate NDIR into leak-detection systems that alert crews before CO₂ crosses the 5 000 ppm permissible exposure limit.

Electric-vehicle makers embed cabin CO₂ sensors to pre-empt driver drowsiness and manage battery load, an example of the NDIR market spilling into transportation comfort rather than focusing solely on emissions. Vertical farms pump CO₂ to 1 500 ppm to boost yields, mandating drift-free modules tolerant of constant humidity. Pharmaceutical fermentation and controlled-atmosphere packaging extend the application set, where 30% CO₂ can slow microbial growth on fresh cuts. Carbon-capture plants need sensors graded for 40-bar pressure lines, a niche where Vaisala’s 10-year probe undercuts costly laser analyzers.

By Platform and Form-Factor: Miniaturization Drives PCB-Mount Adoption

Module-level products maintained a 44.20% share of the Non-Dispersive Infrared market in 2025, but PCB-mount chips, growing at a 7.43% CAGR, are the stars in consumer devices and automotive dashboards. Photoacoustic architectures shrink optical paths, allowing 14 mm packages that fit smartwatches. Bluetooth 5.3 supports 100 mW of transmit power, enough to stream multi-gas data without draining coin cells. Industrial retrofit kits still favor swappable modules with IP65 housings and Modbus ports, preserving field-service routines refined over decades.

Photoacoustic chips also sidestep condensation problems by sealing cavities and adding active heaters. Edge-AI routines in these chips flag lens fouling before accuracy drifts past ±50 ppm, feeding maintenance alerts into mobile apps. Meanwhile, complete analyzer racks and incorporate pumps, filters, and data loggers to comply with stack-testing regulations that a bare sensor cannot meet. Vendors now offer hybrid designs, a tiny PCB-mount core surrounded by a configurable shell that scales from desktop QA tools to field-swap modules.

Geography Analysis

Asia-Pacific delivered 42.80% of 2025 revenue after China cut indoor CO₂ limits to 800 ppm, triggering retrofits across 30 billion m² of offices and malls. India’s Smart Cities Mission and Japan’s updated school codes both hard-wire NDIR into ventilation controllers, guaranteeing baseline demand. South Korea and Australia align with ASHRAE 62.1, easing foreign sensor approvals and unifying tender processes for multinational property managers.

The Middle East, forecast to grow at a 7.88% CAGR, benefits from Vision 2030 green-building decrees and the ESTIDAMA Pearl system, which classifies indoor CO₂ levels above 800 ppm as a compliance breach. Stadiums built for the 2022 World Cup in Qatar embedded more than 10 000 sensors, demonstrating their viability in 50 °C climates and spurring airports and malls to follow suit. Saudi Arabia’s industrial methane inventory program now mandates NDIR on refinery stacks, stitching a recurring revenue stream for calibration services. Egypt’s New Administrative Capital orders LEED Gold across 1.8 million m² of downtown core, each tower specifying CO₂ sensors on every air-handling unit.

North America and Europe together represented roughly 40% of the NDIR market in 2025. California’s classroom law and the EU Energy Performance of Buildings recast both stipulate continuous monitoring, creating retrofit waves in schools, hotels, and care homes. US federal tax incentives can rebate one-third of sensor project costs, lifting payback models for mid-tier hotels. Germany lowered workplace CO₂ limits to 3 000 ppm, nudging factories to upgrade. The UK recommended sub-1 500 ppm classrooms after winter tests showed 60% non-compliance, adding an estimated 300 000-unit opportunity. South America and Africa are early-stage, yet Brazil is drafting calibration norms, while South Africa weighs mandatory CO₂ sensing in deep mines, hinting at future upside.

Competitive Landscape

The Non-Dispersive Infrared market shows moderate concentration, with the top five firms (Sensirion, Honeywell, Vaisala, Senseair, Amphenol) accounting for roughly 55%-60% of worldwide revenue. Chinese vendors Winsen and Cubic leverage cost advantages to price basic CO₂ modules at USD 18, forcing incumbents to differentiate through 10-year warranties, on-chip AI, and multi-gas portfolios. Vertical integration matters; Sensirion fabricates its own MEMS heaters and humidity stacks that calibrate alongside CO₂ channels, shortening design cycles for combo sensors.

Edge-AI is emerging as a pivotal arena, driving innovation and competition among key players. Sensirion’s SCD53, set to debut in Q4 2026, offers a calibration-free lifespan, potentially significantly reducing maintenance requirements and operational costs for end users. Infineon’s PAS design adeptly filters out vibration noise, making it particularly suitable for factory environments where precision and reliability are critical. For oil sands operators, breaking seals every winter poses logistical and financial challenges, making Vaisala’s 15-year IR source life a new procurement standard that effectively addresses these pain points. Additionally, patent filings are increasingly focusing on dual-wavelength compensation and acoustic driver algorithms, raising the technical bar and creating entry barriers for low-cost competitors aiming to enter the NDIR market.

In the realm of Agricultural IoT and carbon-capture sites, there's untapped potential, especially in environments where humidity and pressure levels surpass traditional specifications. These extreme conditions present opportunities for innovation and market growth. Senseair’s S88 GH is specifically designed for greenhouses operating at 95% relative humidity, addressing a critical need for reliable performance in such challenging settings. Similarly, Vaisala’s CCS probe offers a cost-effective alternative to traditional laser systems, reducing installed costs by two-thirds and making advanced technology more accessible to a broader range of users. However, NevadaNano is positioning itself to leapfrog competitors with its molecular-property spectrometers, which promise zero cross-sensitivity, a significant advantage in applications requiring high accuracy. Despite this promise, the company faces challenges in scaling up to commercial volumes, which could impact its ability to capitalize on this technological edge in the near term.

Non-Dispersive Infrared (NDIR) Industry Leaders

Sensirion AG

Honeywell International Inc.

Cubic Sensor and Instrument Co., Ltd.

Amphenol Advanced Sensors (Telaire)

Senseair AB (Asahi Kasei Microdevices)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Honeywell International rolled out the 4-Series NDIR Hydrocarbon Gas Sensor, a dual-wavelength module delivering ±5% accuracy over 0-5 000 ppm and cutting condensation drift by 40%, aligning with EPA methane survey rules.

- January 2026: Sensirion AG unveiled the SCD53 CO₂ module, slated for Q4 2026 release, featuring on-chip neural networks that maintain ±30 ppm stability for 10 years without baseline correction.

- December 2025: Amphenol Advanced Sensors updated Telaire T6793 firmware for Matter compatibility, enabling gateway-free integration into major smart-home ecosystems.

- September 2025: Gas Sensing Solutions secured ISO 9001:2015 for its Cumbernauld plant, paving the way into the ISO 13485 medical markets.

Global Non-Dispersive Infrared (NDIR) Market Report Scope

The Non-Dispersive Infrared (NDIR) Market comprises gas sensing technologies that measure gas concentrations using infrared light absorption without dispersing light through prisms or gratings. NDIR sensors detect specific gases (CO₂, CO, CH₄, hydrocarbons, refrigerants, VOCs) by comparing infrared absorption at target wavelengths against reference bands, offering high accuracy, selectivity, and long-term stability for industrial, HVAC, safety, and environmental monitoring applications.

The Non-Dispersive Infrared Market Report is Segmented by Product Type (Fixed/Wall-Mount Modules, Portable/Handheld Devices, Smart/Connected NDIR Sensors, and Industrial Process Analyzers), Gas Detected (Carbon Dioxide (CO2), Hydrocarbons (CH4, C3H8), Refrigerants (HFCs, HFOs), and Anesthetic and Medical Gases), End-Use Industry (HVAC and Building Automation, Industrial Safety and Process, Automotive and Transportation, Healthcare and Life-Science, and Food and Agriculture), Platform (PCB-Mount Chip Sensors, Module-Level Sensors, and Complete Analyzer Systems), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Fixed/Wall-Mount Modules |

| Portable/Handheld Devices |

| Smart/Connected NDIR Sensors |

| Industrial Process Analyzers |

| Carbon Dioxide (CO2) |

| Hydrocarbons (CH4, C3H8) |

| Refrigerants (HFCs, HFOs) |

| Anesthetic and Medical Gases |

| HVAC and Building Automation |

| Industrial Safety and Process |

| Automotive and Transportation |

| Healthcare and Life-Science |

| Food and Agriculture |

| PCB-Mount Chip Sensors |

| Module-Level Sensors |

| Complete Analyzer Systems |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Fixed/Wall-Mount Modules | |

| Portable/Handheld Devices | ||

| Smart/Connected NDIR Sensors | ||

| Industrial Process Analyzers | ||

| By Gas Detected | Carbon Dioxide (CO2) | |

| Hydrocarbons (CH4, C3H8) | ||

| Refrigerants (HFCs, HFOs) | ||

| Anesthetic and Medical Gases | ||

| By End-Use Industry | HVAC and Building Automation | |

| Industrial Safety and Process | ||

| Automotive and Transportation | ||

| Healthcare and Life-Science | ||

| Food and Agriculture | ||

| By Platform | PCB-Mount Chip Sensors | |

| Module-Level Sensors | ||

| Complete Analyzer Systems | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value outlook for the Non-Dispersive Infrared market?

The market stands at USD 0.80 billion in 2026 and is on track to reach USD 1.12 billion by 2031.

Which end-use segment is expected to grow fastest through 2031?

Healthcare and life-science applications are projected to expand at a 7.38% CAGR as capnography becomes mainstream in emergency and post-anesthesia care.

Why are refrigerant NDIR sensors attracting investor interest?

Stricter F-Gas and Kigali phase-downs require continuous monitoring of hydrofluorocarbon leaks, making refrigerant detection the quickest-growing gas segment at 7.78% CAGR.

How are new connectivity standards influencing sensor selection?

Matter and Thread allow vendor-agnostic mesh networks, reducing installation labor by around 30% and accelerating smart-sensor adoption in retrofits.

What differentiates next-generation NDIR modules from legacy designs?

Embedded edge-AI eliminates frequent recalibration, while photoacoustic architectures shrink packages to under 15 mm without sacrificing ±50 ppm accuracy.

Page last updated on: