Optocouplers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

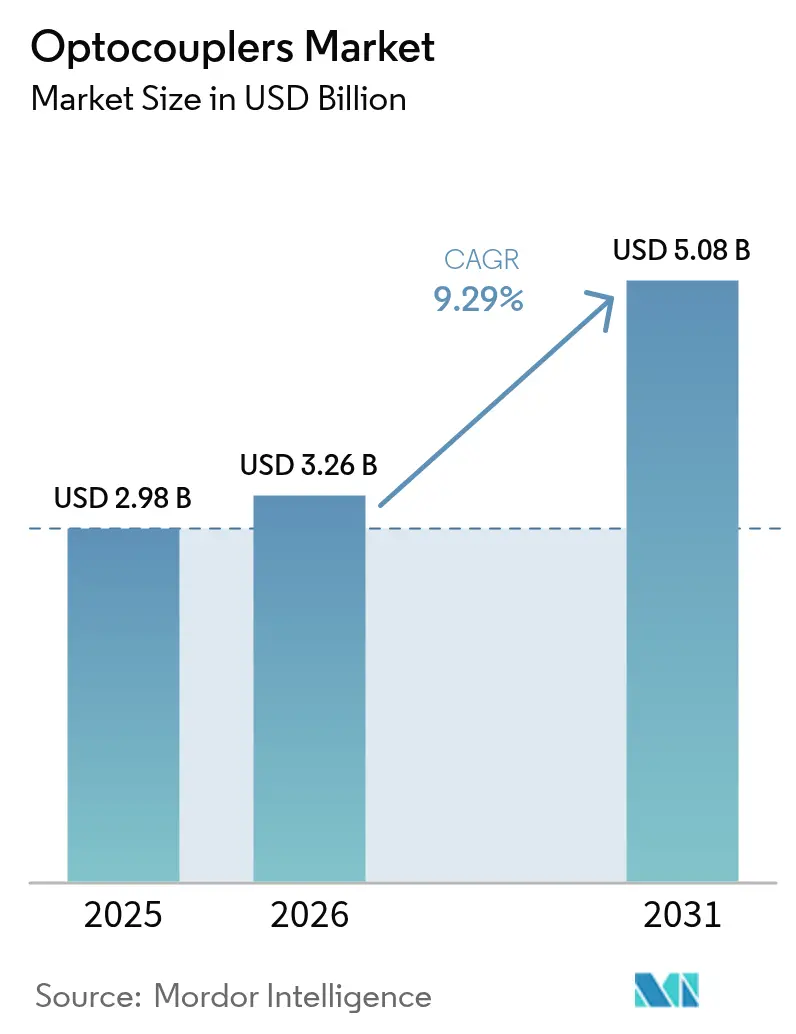

| Market Size (2026) | USD 3.26 Billion |

| Market Size (2031) | USD 5.08 Billion |

| Growth Rate (2026 - 2031) | 9.29% CAGR |

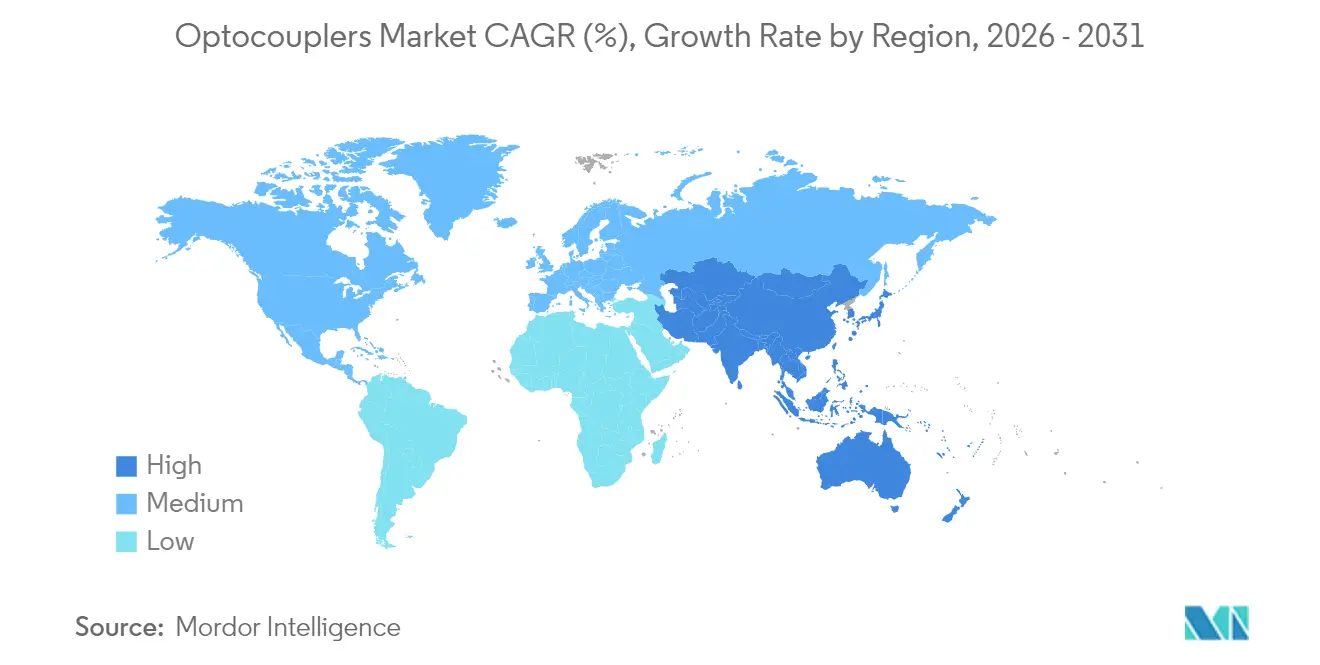

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Optocouplers Market Analysis by Mordor Intelligence

The optocouplers market size was valued at USD 2.98 billion in 2025 and estimated to grow from USD 3.26 billion in 2026 to reach USD 5.08 billion by 2031, at a CAGR of 9.29% during the forecast period (2026-2031). Growing electrification of vehicles, escalating automation retrofits, and stricter functional-safety regulations collectively keep demand resilient even as digital isolators press for design wins. Suppliers are refining LED materials and package designs, so devices tolerate 150°C junction temperatures, a threshold increasingly common in SiC-based traction inverters. High-speed logic-gate variants are now pivotal where GaN and SiC devices switch above 100 kHz, while traditional phototransistor parts continue supporting cost-sensitive industrial maintenance cycles. Regionally, North America sustains replacement demand, whereas Asia-Pacific manufacturers are scaling new lines to serve consumer electronics, EV power modules, and 5G infrastructure buildouts.

Key Report Takeaways

- By product type, phototransistor devices led with 31.85% revenue share in 2025; high-speed logic-gate optocouplers are forecast to advance at a 10.31% CAGR through 2031.

- By channel count, single-channel parts held 41.05% of the optocouplers market share in 2025, while 4-channel configurations are projected to grow at a 10.52% CAGR to 2031.

- By isolation rating, the 2.5 - 5 kVrms class accounted for 49.45% of the optocouplers market size in 2025; parts rated above 5 kVrms will expand at a 11.86% CAGR during the forecast window.

- By end-user, industrial automation captured 28.05% revenue share in 2025; automotive and e-mobility are set to compound fastest at 11.48% CAGR by 2031.

- By geography, North America led with 44.25% share of the optocouplers market size in 2025, whereas Asia-Pacific is positioned for the quickest growth at 12.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Optocouplers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging adoption in hybrid and battery-electric drivetrains | +2.10% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Rising factory automation and Industry 4.0 retrofits | +1.80% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| 5G-enabled base-station roll-outs driving power isolation demand | +1.40% | Global, led by China, South Korea, United States | Short term (≤ 2 years) |

| Proliferation of GaN/SiC power devices boosting high-speed optocouplers | +1.20% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Regulatory push for functional safety (ISO 26262, IEC 60747-5-5) | +0.90% | Global, strongest in Europe and North America | Long term (≥ 4 years) |

| Emerging solid-state circuit-breaker architectures | +0.80% | Industrial markets globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging adoption in hybrid and battery-electric drivetrains

Electric vehicles require galvanic isolation between 800 V battery packs and 12 V control domains, so EV architectures pull in larger numbers of high-voltage optocouplers certified to IEC 60747-5-5.[1]onsemi, “SiC MOSFET and Gate Driver Solutions for High-Voltage Electric Vehicles,” onsemi.com Battery-disconnect units increasingly pair SiC JFETs with logic-gate optocouplers to shorten fault-clearing times, and fast-charging stations need several isolated gate-drive channels per power module. Automotive OEM sourcing guidelines now stipulate minimum common-mode transient immunity above 20 kV/µs, a performance band that favors optocouplers with optimized internal shield structures. As global BEV sales climb toward 20 million units by 2030, the optocouplers market is expected to ship higher volumes of devices rated above 5 kVrms.

Rising factory automation and Industry 4.0 retrofits

Legacy programmable-logic controllers and motor drives stay with optocouplers because LED-phototransistor pairs exhibit excellent noise rejection in facilities packed with inverters and servos. Upgrades to smart sensors and cloud-connected edge controllers often retain the original isolation topology, so modernization activity layers new channels on top of the installed base. Suppliers now offer multi-channel surface-mount packages that reduce PCB area by 40%, an essential feature for densely packed control cabinets. Asian manufacturers spearhead this retrofitting wave as government incentives prioritize productivity improvements across textiles, metals, and discrete manufacturing.[2]Renesas Electronics, “Optocoupler LED Aging and CTR Degradation Application Note,” renesas.com

5G-enabled base-station roll-outs driving power isolation demand

Radio-access networks deploying massive-MIMO arrays escalate the need for isolated DC-bias supplies sandwiched next to RF power amplifiers. Optocouplers withstand the strong electromagnetic fields generated by 3.5 GHz and 26 GHz transmitters better than some capacitive isolators because their optical channel is immune to E-field coupling. Chinese operators alone installed over 700,000 new 5G macro sites during 2024, each containing multiple isolated fly-back converter rails that typically use logic-gate optocouplers for primary-side regulation.[3]Fibre Systems, “China 5G Infrastructure Roll-Out Accelerates Optical Component Demand,” fibre-systems.com The short deployment cycle means volume demand will remain elevated through 2027.

Proliferation of GaN/SiC power devices boosting high-speed optocouplers

Wide-bandgap switches trigger hard-switching transitions above 600 V/ns, stressing isolation devices. High-speed optocouplers with 50 ns maximum propagation delay align more naturally with these semiconductors than slower phototransistor types. Infineon’s reference designs for solid-state circuit breakers illustrate gate-drive stages that rely on 10 MBd optocouplers to achieve microsecond fault isolation.[4]Infineon Technologies, “Solid-State Circuit Breaker Reference Designs,” infineon.com Temperature-gradient testing shows LED-lifetime acceleration, so suppliers are trialing AlGaInP-based emitters to slow luminous decay at 175 °C.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LED wear-out and CTR degradation over lifetime | -1.30% | Global | Long term (≥ 4 years) |

| Thermal-management challenges above 150°C junction | -0.90% | Industrial and automotive applications globally | Medium term (2-4 years) |

| Competition from digital isolators (capacitive and magnetic) | -1.10% | North America & Europe primarily | Short term (≤ 2 years) |

| Supply-chain concentration in Asia for LED die | -0.70% | Global, with highest impact on Western OEMs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

LED wear-out and CTR degradation over lifetime

Photonic transfer relies on emitter efficiency; as LEDs age, current transfer ratio falls below datasheet minima, forcing derating or scheduled replacement. Accelerated-aging studies show 25% CTR loss after 10,000 operating hours at 125 °C, which in automotive traction inverters equates to roughly four years of service. Designers therefore oversize LEDs or increase drive current, both raising power dissipation and reducing overall system efficiency.

Competition from digital isolators (capacitive and magnetic)

Capacitive and magnetic isolators from Analog Devices and Silicon Labs support 150 MBd data rates while consuming less than 5 mW per channel during idle, features attractive in battery-powered medical and consumer products.[5]Analog Devices, “Digital Isolators vs. Optocouplers: Performance Comparison,” analog.com In many motor-control inverters, however, common-mode transient exposure above 25 kV/µs still tips the balance toward optocouplers because digital isolators require guard rings and elaborate PCB stack-ups to achieve similar robustness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: High-Speed Variants Drive Innovation

The phototransistor class controlled 31.85% of 2025 revenue within the optocouplers market. Although volume remains high for industrial logic inputs and power-supply feedback loops, its growth is modest. High-speed logic-gate types are tracking a 10.31% CAGR and, by 2031, will account for a markedly larger slice of the optocouplers market size as 5G, electric-vehicle, and renewable-inverter OEMs pivot toward sub-100 ns propagation delays. IGBT and MOSFET gate-drive optocouplers now integrate Miller-clamp circuits and desaturation detection, displacing discrete comparators and reducing BOM count.

Emerging photo-SCR and photo-TRIAC options address solid-state relays in appliance and HVAC markets, while photovoltaic optocouplers produce gate-drive voltages without ancillary bias supplies, a compelling feature for isolated high-side switches in solar micro-inverters. Toshiba’s TLP3640A, certified to EN IEC 60747-5-5, demonstrates how compliance credentials buttress adoption in functional-safety landscapes. Suppliers continue to invest in proprietary LED chemistries that double luminous output for the same drive current, prolonging lifespan and mitigating CTR degradation.

By Channel Count: Integration Density Climbs

Single-channel units kept 41.05% share of the optocouplers market in 2025 as legacy PLC I/O cards and off-line power-supply flyback controllers rely heavily on one-for-one isolation. Nevertheless, 4-channel devices are predicted to grow 10.52% annually through 2031, reflecting designers’ push to shrink board footprints in multi-axis servo drives and battery-management modules. Dual-channel packages facilitate bidirectional communication links in RS-485 transceivers, while six- and eight-channel arrays serve three-phase motor inverters, enabling simultaneous high-side and low-side gating per phase.

Density gains do not come without trade-offs; thermal coupling between channels elevates internal LED junction temperature, so package designers employ copper lead-frames and molded cavities to dissipate heat. The optocouplers industry increasingly offers pin-compatible multi-channel options featuring independent enable pins plus open-collector fault outputs, making migration straightforward. System integrators leveraging higher channel densities often achieve up to 18% PCB area savings, crucial in high-power EV on-board chargers.

By Isolation Voltage: Need for Higher Ratings Accelerates

Devices rated 2.5 - 5 kVrms represented 49.45% revenue in 2025 within the optocouplers market, reflecting mainstream industrial and automotive voltage tiers. Yet applications surpassing 800 V battery buses or 1,200 V solar string inverters now demand parts tested to 8 kVrms or higher. This over-5 kVrms slice is growing 11.86% annually and will represent a double-digit portion of the optocouplers market size by 2031.

Suppliers validate packages to survive 10 kV impulse surges and provide 20 mm creepage spacing on wide-body SO packages. Scientific Reports detailed LTCC-substrate optocouplers that sustained isolation across 250 °C cycles at 7 kVrms, illustrating research trending toward ceramic substrates with minimal thermal expansion mismatch. Conversely, consumer electronics such as smartphone chargers continue choosing ≤ 2.5 kVrms parts to minimize cost and z-direction board height.

By End-User: Electrified Mobility Gains Momentum

Industrial automation and motion control held 28.05% revenue share in 2025, reinforcing the optocouplers market’s stable core constituted by PLCs, inverter drives, and robot controllers. Growth in this segment tracks factory investments in predictive maintenance and servo motor upgrades, but its CAGR lags the market average. Automotive and e-mobility, on the other hand, is forecast for 11.48% CAGR, buoyed by battery-electric and plug-in hybrid volumes and the auxiliary demand spill-over into fast chargers, e-axle inverters, and DC-DC converters.

Energy and power applications, including solar string inverters, wind-turbine converters, and HVDC links, are adopting logic-gate optocouplers with active Miller clamps to support SiC modules operating at 1.7 kV. Telecom/datacom deployments feature high-speed parts for synchronous buck regulators inside 400 G optical transceivers, while medical imaging equipment continues to demand radiation-tolerant devices with guaranteed leakage currents below 1 µA. These diverse requirements reinforce the optocouplers market’s broad scope across industrial, automotive, energy, communications, and healthcare verticals.

Geography Analysis

North America dominated 2025 revenue with a 44.25% stake in the optocouplers market share as vehicle electrification programs, aerospace upgrades, and semiconductor equipment builds kept demand vibrant. OEMs benefit from a local ecosystem spanning LED wafer growth in Arizona through to assembly in Mexico’s Baja corridor. Economic incentives such as the U.S. CHIPS Act will further bolster domestic optoelectronics capacity, potentially tightening lead times for regional customers.

Europe follows, propelled by stringent functional-safety mandates and a strong concentration of industrial-automation firms in Germany, Italy, and France. EU climate targets incentivize 800 V EV platforms and renewable-energy storage systems, each requiring multi-kVrms isolation. The region’s commitment to carbon-neutral manufacturing supports the replacement of electromechanical relays with optically isolated solid-state alternatives. However, moderate GDP growth tempers total unit expansion.

Asia-Pacific is on a 12.25% CAGR trajectory and will close the share gap quickly. China’s aggressive 5G rollout, sprawling consumer-electronics supply chains, and surging EV output drive huge volume requirements, while Japanese incumbents leverage their process know-how to supply high-reliability optocouplers for factory-automation exports. South Korea’s memory fabs execute stringent equipment upgrade cycles, each new EUV stepper containing dozens of isolation channels. India’s production-linked incentive programs have begun to lure LED wafer slicing and backend assembly lines, diversifying the region’s supply base.

Regulatory Landscape

Optocouplers sold into automotive, industrial, power, and telecom equipment are shaped by mandatory insulation and safety standards, notably IEC 60747-5-5 (optoisolators) and insulation-coordination requirements under IEC 60664-1, alongside end-equipment safety regimes such as IEC 62368-1. In functional-safety-driven designs, compliance evidence is often supported through third-party certifications (for example, VDE, UL, and CSA listings on reinforced-isolation components) that gate qualification for traction inverters, on-board chargers, and industrial drives where common-mode transients are high.

Trade and localization policies also affect sourcing and cost. India formally notified the Electronics Component Manufacturing Scheme (ECMS) on April 8, 2025, and the Union Budget 2026-27 increased its outlay to INR 40,000 crore, reinforcing incentives to localize components and backend assembly while requiring adherence to scheme conditions and audits. In Europe, a June 25, 2026 Council of the European Union implementing action converted tariff commitments linked to the 2025 EU-U.S. Trade Framework into binding measures, creating a more structured backdrop for cross-border electronics component flows during a period of prior tariff volatility.

Value Chain Analysis

The optocouplers value chain starts with compound semiconductor and optical materials (LED epi-wafers/die, leadframes, mold compounds, and optical encapsulants), then moves into device fabrication and backend processes that drive optocoupler differentiation: die attach, wire bonding, optical alignment, molding, and high-voltage testing to standards such as IEC 60747-5-5. IDMs and specialized suppliers distribute through direct OEM engagement for automotive and industrial programs, and through broadline distributors for industrial maintenance and power-supply designs. Qualification cycles, including AEC-Q102 for automotive-grade parts, act as a gating step before volume ramps.

Bottlenecks tend to show up where single components or qualified alternates are scarce, and where downstream products require long validation windows. Sensata Technologies highlighted this fragility when it disclosed a February 2025 supply disruption in Crydom DC output solid state relays due to an optocoupler component becoming obsolete, forcing replacement validation; by March 2025, production restarted for several families after completing validations. The episode reflects the broader semiconductor supply-chain reality also noted by the OECD (June 2025) around bottlenecks and volatility, leading OEMs to dual-source at the component level, lock qualified alternates early, and improve part-level traceability for safety-critical builds.

Competitive Landscape

Incumbents such as Broadcom, ON Semiconductor, Texas Instruments, Vishay, Renesas, and Toshiba collectively own the majority of back-end assembly capacity, while niche players like Isocom, CT Micro, and Standex Electronics specialize in radiation-hardened or custom package variants. Competitive pressure stems mainly from digital-isolator suppliers, Analog Devices, Silicon Labs, and Skyworks, whose capacitive and magnetic products promise higher data rates and lower power draw. The trend forces optocoupler vendors to accelerate development of high-speed logic-gate families that bridge the performance gap without sacrificing inherent optical immunity.

Strategic moves underscore this pivot. ON Semiconductor’s 2025 acquisition of Qorvo’s SiC JFET assets for USD 115 million expands its gate-driver portfolio, enabling tightly coupled optocoupler-plus-SiC solutions for EV battery disconnects. Vishay introduced its VOIH72A 25 MBd duplex optocoupler featuring digital IO and guaranteed 60 kV/µs CMTI, addressing traction inverter designs. Toshiba rolled out automotive-qualified SO16-W packages that meet 8 mm creepage under IEC 60664, cementing its reputation among Japanese OEMs.

Intellectual-property filings reveal focus areas: high-temperature LED chemistries, optical waveguide structures reducing propagation delay, and integration of over-current detection circuits inside optocoupler gate drivers. Supply-chain vulnerability remains a concern because epi-wafer growth for AlGaAs LEDs is still concentrated in China and Taiwan. Nevertheless, Western IDMs are repatriating limited volumes to mitigate geopolitical risk, investing in compound-semi pilot lines in Texas and Saxony.

Optocouplers Industry Leaders

Broadcom Inc.

ON Semiconductor Corporation

Texas Instruments Incorporated

Vishay Intertechnology Inc.

Renesas Electronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Design whitespace is expanding where higher-voltage platforms and tighter creepage/clearance requirements collide with space-constrained power electronics, particularly in 800 V electric vehicle architectures and high-voltage solar inverters. Recent product activity points to this direction: Vishay introduced AEC-Q102 qualified VOWA617A and VOWA618A devices in May 2026 with 11 mm creepage and clearance for EV and solar applications, and followed with VOLA617A in June 2026 to support galvanic isolation needs in 800 V battery architectures. These releases align with a broader shift toward higher isolation classes (above 5 kVrms) and reinforced insulation credentials that help suppliers defend optocoupler selection against capacitive and magnetic digital isolators in noisy switching environments.

A second opportunity area is high-speed and high-CMTI interfaces for wide-bandgap power stages and fast-switching control loops, where optocouplers are being engineered for higher transient immunity and smaller surface-mount footprints. The use case is most visible in traction inverters, on-board chargers, industrial servo drives, and emerging solid-state circuit breaker designs that prioritize robust common-mode performance and safety certification artifacts for qualification. On the supply side, incentives that deepen electronics manufacturing, such as India’s ECMS framework (notified April 2025 and expanded in the 2026-27 budget), support additional backend assembly, test capacity, and qualification services for optocouplers and adjacent isolation components in Asia-focused supply chains.

Recent Industry Developments

- July 2026: Vishay Intertechnology introduced the VOMHA43A automotive 1 MBd high-speed optocoupler in a 3.6 mm wide SOP-5 package, targeting space-constrained automotive electronics. The combination of high common-mode transient immunity and a compact footprint supports denser isolation channel placement in battery management and power conversion designs.

- May 2026: Vishay Intertechnology launched the AEC-Q102 qualified VOWA617A and VOWA618A optocouplers with 11 mm creepage and clearance distances for electric vehicles and solar inverters. The release addresses reinforced-insulation needs tied to higher-voltage platforms and helps optocouplers retain roles where certification and insulation geometry are decisive selection criteria.

- December 2024: Toshiba announced the TLP3640A MOSFET-output optocoupler certified to EN IEC 60747-5-5 for functional-safety-centric EV and factory-automation designs. Certification-aligned offerings such as this improve design-in confidence for safety-regulated programs and shorten qualification cycles for OEMs that require documented isolation performance.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers optocouplers used to pass electrical signals across an isolation barrier, typically through an LED input and a photo-sensitive output stage, and it is sized in revenue terms across major end-use demand.

Scope exclusions: We exclude adjacent isolation solutions that are not optocouplers (such as capacitive or magnetic digital isolators) and we also exclude discrete LEDs or photodiodes sold outside an optocoupler package.

Segmentation Overview

- By Product Type

- Phototransistor

- Photodarlington

- Photo-SCR

- Photo-TRIAC

- High-speed Logic-gate Optocoupler

- IGBT/Power MOSFET Gate-drive Optocoupler

- Other Product Types (Photovoltaic, Analog, etc.)

- By Channel Count

- 1-Channel

- 2-Channel

- 4-Channel

- 6-Channel and 8-Channel

- By Isolation Voltage Rating

- Less than or Equal to 2.5 kVrms

- 2.5 - 5 kVrms

- Greater than 5 kVrms

- By End-user Industry

- Automotive and E-Mobility

- Industrial Automation and Motion Control

- Power and Energy (Renewables, Grid)

- Consumer Electronics and Home Appliances

- Telecom and Datacom

- Healthcare Equipment

- Other End-user Industries (Aerospace, Defense, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work is used to build the fact base and sanity checks before any modeling starts, so we begin with public statistics that describe electronics output and trade patterns. Sources we relied on include, for example, UN Comtrade for cross-border semiconductor and electronic component flows, World Semiconductor Trade Statistics for category level demand direction, and national statistical agencies such as the US Census Bureau for industrial and electronics indicators.

To connect demand with real applications, we also reviewed technical and regulatory references that shape usage and qualification, such as IEC and UL safety standards coverage for isolation, along with IEEE and other peer-reviewed publications that discuss optocoupler performance trends. Company annual reports, earnings decks, and product literature were used to understand portfolio mix and end-market exposure. We also used paid subscriptions for company financials and patent databases to cross-check timelines for new device introductions. These are illustrative examples, and many other public sources were also referenced for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary discussions were used to pressure test the demand drivers behind isolation components, and then to translate those drivers into realistic adoption and pricing assumptions. We spoke with a mix of component suppliers, distributors, and engineers and buyers from industrial, automotive, consumer electronics, and communications value chains, and coverage was balanced across APAC, EMEA, and the Americas to reflect where optocouplers are made and consumed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 21% | APAC: 49% |

| Mid tier: 49% | Functional/Unit leaders: 23% | EMEA: 33% |

| Smaller Players: 21% | Managers: 56% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where electronics production, application level demand pools, and trade movements are used to reconstruct the addressable spend on optocouplers by region, and then split by common device families and end-use intensity. The model is then corroborated with selective bottom-up approximations, such as sampled ASP times estimated unit demand by application, distributor channel checks, and a limited supplier revenue roll up to spot overcounts or missing pockets.

A few practical inputs drive most of the math, including isolation voltage rating mix, average channel count per design, typical replacement cycles in industrial and automotive systems, and the share of designs that still choose optocouplers versus newer isolation approaches. We also track pricing movement by package class (for example, standard phototransistor types versus faster logic output variants), since small ASP shifts can move the total market. For the forecast, scenario analysis is applied around end-market output growth, electrification intensity, and industrial automation spend, and those scenarios are filtered through what interviewees expect for design-in pipelines and qualification timelines. When bottom-up visibility is weak in smaller regions or niche applications, the gap is handled through ratio based allocation using end-use production indicators and import dependence signals, and then reconciled back to the global total.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals, such as regional electronics shipment direction, trade value movements, and whether the implied pricing sits within realistic ranges discussed by practitioners. If a region shows an unusual spike, we recheck currency timing, segment weights, and whether one end-use is being double counted before the numbers move forward.

A multi-step review is followed where assumptions, formulas, and intermediate totals are checked by another analyst, and then the final view is reviewed for consistency across chapters. Reports are refreshed annually, and interim updates are made when material events occur, such as major supply disruptions, regulation shifts tied to isolation standards, or notable demand shocks in automotive and industrial. Before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Optocouplers Market Estimate Compared With Other Published Estimates

Published market numbers for optocouplers can look far apart even when everyone is referencing signal isolation, because small scope choices and timing choices quickly change the total. Differences usually come from what gets counted as an optocoupler, which year is treated as the current market, and how prices are carried forward when product mix is shifting.

The main gap comes from mixing optocouplers with other isolation technologies, where Mordor Intelligence counts revenue only for optocoupler devices and keeps digital isolators outside the scope, and this is then paired with a current-year reset of ASP and mix using recent end-use build indicators rather than a single historical price curve.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.26 B (2026) | |

| Global Consultancy A | USD 4.41 B (2025) | Uses an earlier current-year point and appears to include broader product groupings by application and technology, which can pull in adjacent isolation components and inflate the spend pool when summed at a high level. |

| Industry Data Publisher B | USD 2.72 B (2024) | Anchors on an older base year and is often built from reported shipment and output splits, which can understate value when mix shifts toward higher speed or higher isolation variants and when pricing is updated less frequently. |

Looking at the spread, the higher figure aligns with a broader definition and earlier timing, while the lower figure is consistent with an older base and slower value uplift from mix. By keeping the scope tight, updating key pricing and mix assumptions, and checking totals against independent demand signals, the estimate stays traceable to clear inputs and repeatable steps for decision-making.

Key Questions Answered in the Report

How large is the optocouplers market in 2026?

The optocouplers market size reached USD 3.26 billion in 2026 and is forecast at USD 5.08 billion by 2031.

Which product type is expanding fastest?

High-speed logic-gate optocouplers show the highest growth, advancing at a 10.31% CAGR through 2031.

Why are optocouplers still preferred over digital isolators in many industrial drives?

Optocouplers provide superior immunity to common-mode transients and proven reliability in electromagnetically noisy factory environments.

Which region is forecast to grow the quickest?

Asia-Pacific is set to register the fastest CAGR of 12.25% as it scales EV, 5G, and electronics manufacturing.

What isolation voltage class is gaining the most traction?

Devices rated above 5 kVrms are expanding at 11.86% CAGR due to 800 V EV batteries and high-power renewable inverters.

How is LED CTR degradation addressed?

Vendors are introducing new AlGaInP emitter chemistries and derating guidelines to slow CTR decline over long service lives.

Page last updated on: