Nigeria Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

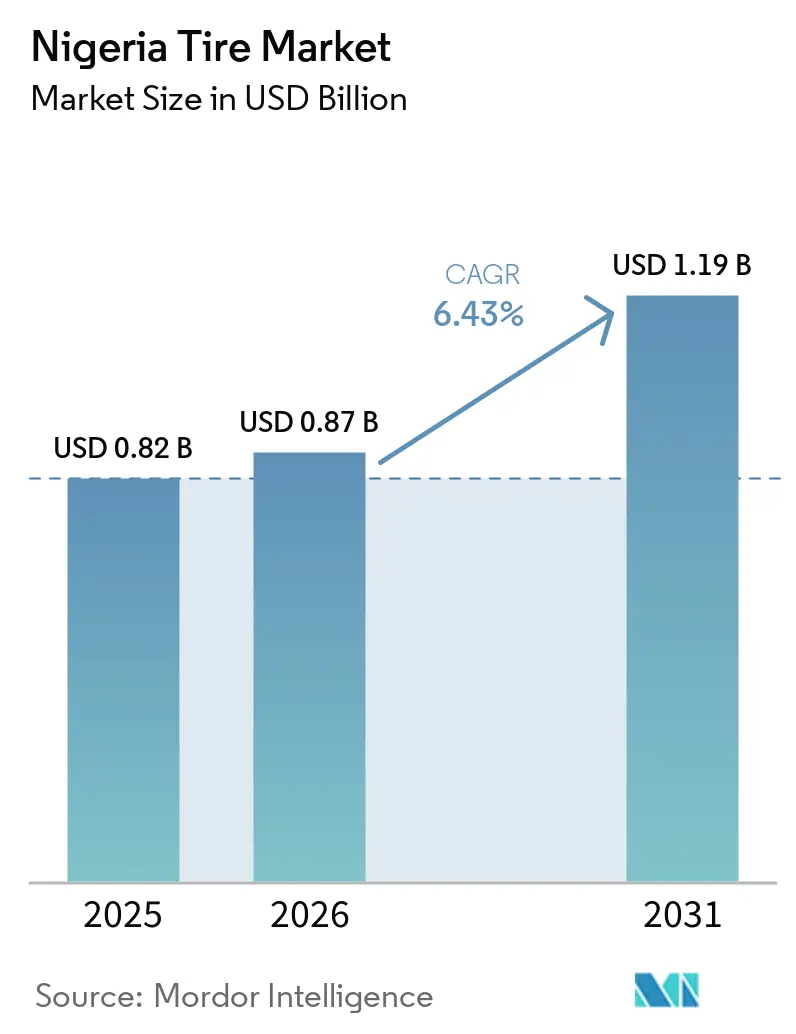

| Base Year Market Size (2025) | USD 0.82 Billion |

| Market Size (2026) | USD 0.87 Billion |

| Market Size (2031) | USD 1.19 Billion |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

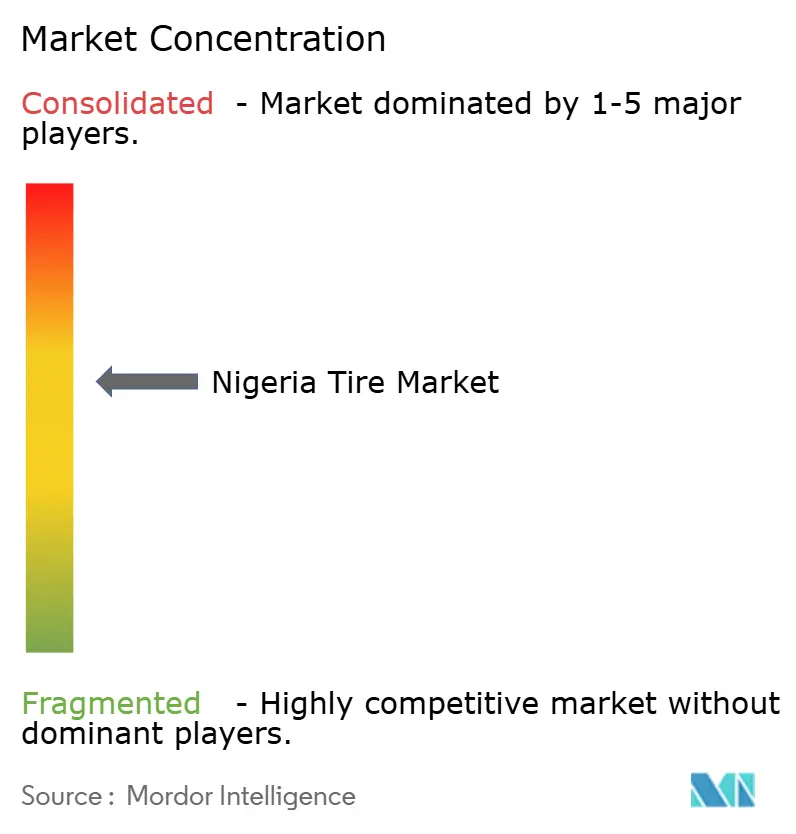

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Tire Market Analysis by Mordor Intelligence

The Nigerian tire market size is projected to grow from USD 0.82 billion in 2025 to USD 0.87 billion in 2026 and is forecast to reach USD 1.19 billion by 2031, registering a CAGR of 6.43% between 2026 and 2031. Nigeria's expansive population, along with the African Continental Free Trade Area (AfCFTA) framework and a government-imposed ban on most used tire imports, is driving this trend. The demand momentum is further supported by the rapid expansion of the light-duty fleet, vehicle financing programs introduced by ride-hailing platforms, and significant investments in the Lagos-Ogun industrial corridor. However, while foreign exchange shortages and fluctuations in power supply present challenges to the sector's immediate growth, they are also encouraging domestic assembly initiatives, which have the potential to enhance local value addition over time. Additionally, stricter enforcement against counterfeit products is shifting replacement purchases toward established brands, contributing to revenue growth in Nigeria's formal tire market.

Key Report Takeaways

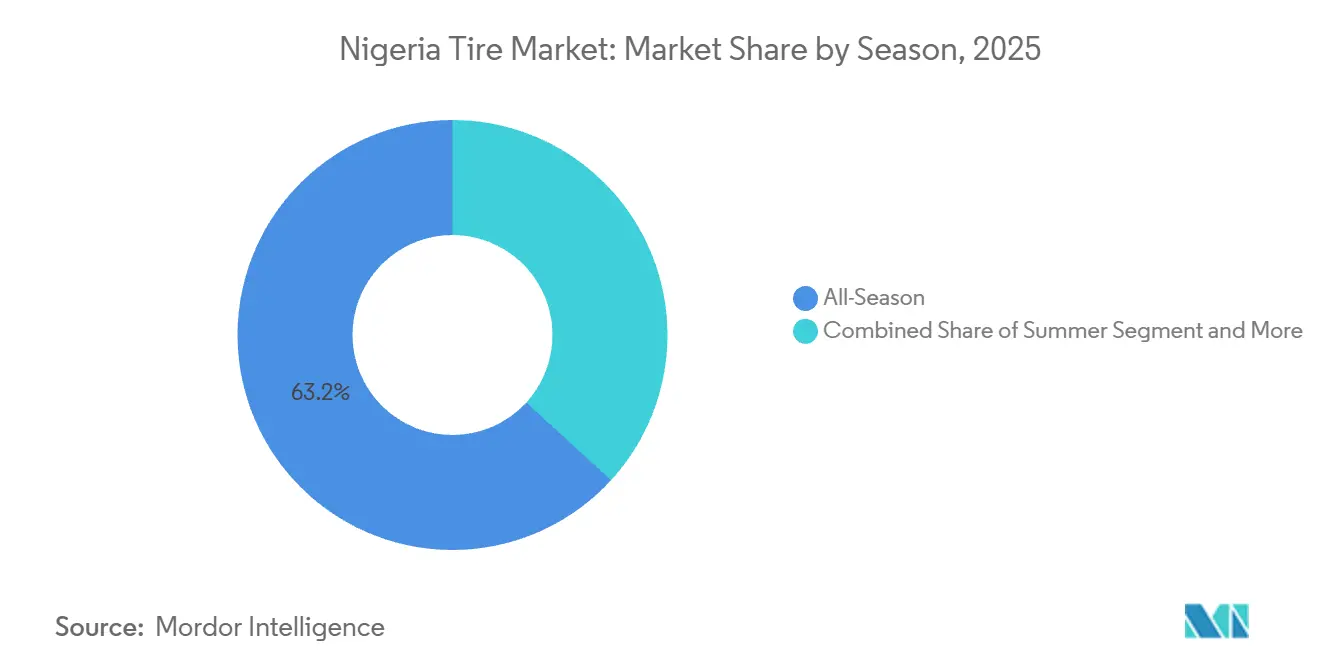

- By season, all-season captured 63.15% of Nigeria's tire market share in 2025, and the segment is projected to grow at a 6.84% CAGR to 2031.

- By tire design, radial tires represented 79.33% share of the Nigerian tire market size in 2025; non-pneumatic/airless technology is advancing at a 9.07% CAGR over the same horizon.

- By vehicle type, passenger cars led with 39.14% revenue share of Nigeria's tire market size in 2025, and the segment is projected to grow at a 7.01% CAGR to 2031.

- By application, on-road led with 85.46% revenue share of Nigeria's tire market size in 2025, and the segment is projected to grow at a 7.33% CAGR to 2031.

- By end user, the aftermarket commanded 73.11% of Nigeria's tire market share in 2025, whereas the OEM segment is forecast to achieve an 8.15% CAGR through 2031.

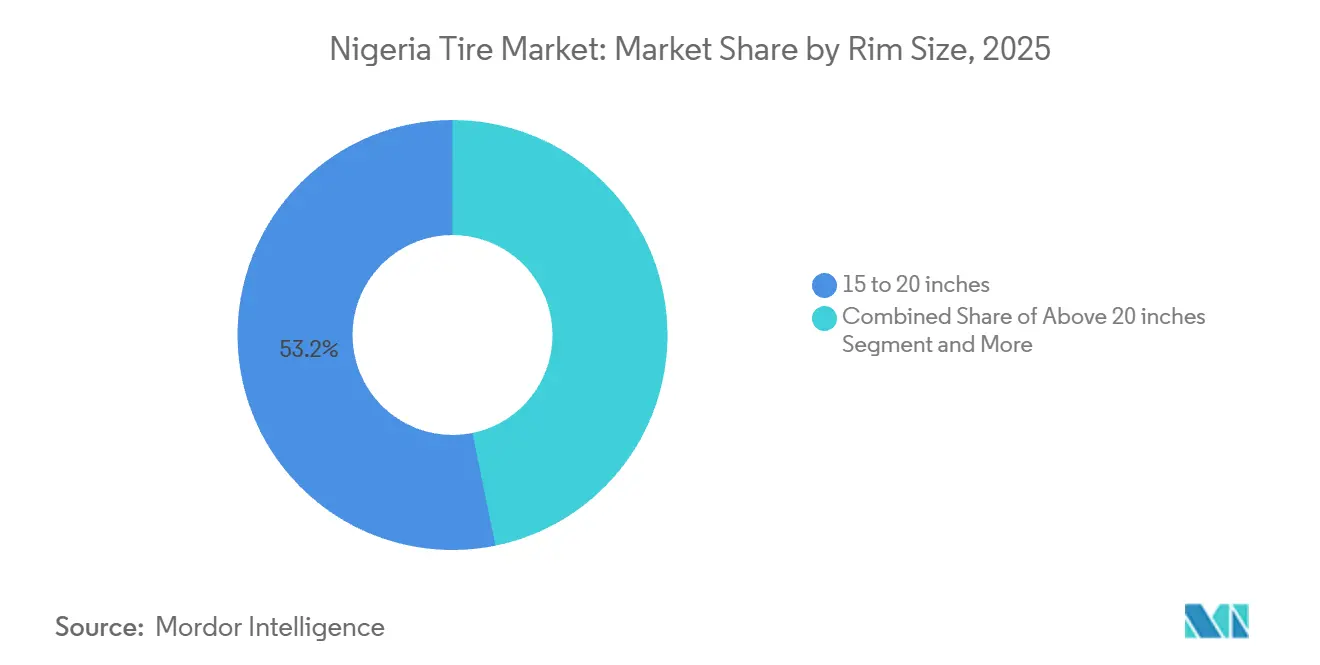

- By rim size, the 15-20 inch category accounted for 53.22% of Nigeria's tire market share in 2025, while sizes above 20 inches are positioned for an 8.36% CAGR to 2031.

- By propulsion, internal-combustion vehicles accounted for 90.55% of Nigeria's tire market share in 2025, while battery-electric vehicles are positioned for an 11.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nigeria Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ban on Used-Tire Imports | +1.8% | Nationwide; intensive in border states | Short term (≤ 2 years) |

| Rapid Light-Duty Fleet Expansion | +1.2% | National; strongest in Lagos, Ogun, Rivers | Medium term (2-4 years) |

| OEM Localization Incentives | +1.1% | Lagos, Ogun, Kaduna | Long term (≥ 4 years) |

| Ride-Hailing Financing Programs | +0.9% | Lagos, Abuja, Port Harcourt | Short term (≤ 2 years) |

| Ogun-Lagos Corridor Trucking Demand | +0.7% | Southwest corridor | Medium term (2-4 years) |

| E-Commerce Last-Mile Growth | +0.6% | Major urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Ban on Used-Tire Imports Boosts Demand for New Units

In 2024, Nigeria tightened its grip on the tire market, banning imports of used and retreaded tires, with the exception of truck tires sized 11.00 × 20 inches and above. This move effectively wiped out around 80% of the low-cost tire segment, nudging consumers towards purchasing new tires[1]“Implementation of Quality Tire Regulations,” Standards Organisation of Nigeria, son.gov.ng. Customs officials, showcasing their enforcement commitment, seized 167 tires in the Oyo and Osun regions. This policy aligns with the Central Bank's foreign-exchange restrictions on rubber and plastic products, aiming to boost local value addition and secure revenue from the replacement cycle for distributors who play by the rules.

Rapid Light-Duty Fleet Expansion After AfCFTA Implementation

Following the operational phase of the African Continental Free Trade Area (AfCFTA), which eased regional trade barriers, Nigeria has positioned itself as a significant hub for distribution networks across West Africa. This development has led to a notable increase in light-duty vehicle registrations. The reduction in tariffs on components has made local assembly more cost-effective, thereby boosting the demand for tires used in passenger cars and light commercial vehicles. The Standards Organization of Nigeria (SON) has implemented stricter compliance checks, enabling high-quality brands to capture additional market volumes. Furthermore, regional assemblers such as CIG Motors have expanded their product lines, including GAC and Wuling vehicles, to cater to cross-border markets. This expansion has further reinforced the growing demand for tires in the region.

OEM Localization Incentives for CKD Assembly Plants

Nigeria's Automotive Industry Development Plan provides seven-year tax holidays and eliminates duties on equipment to encourage the growth of component manufacturing. The Kaduna plant operated by Dangote Peugeot has increased its assembly capacity to produce up to 120 vehicles per day. Additionally, Coscharis-Renault has announced plans to introduce three new vehicle models in 2025, which is expected to generate significant demand for original equipment manufacturer (OEM) tires. Furthermore, government-supported automotive industrial parks located in Nnewi and Lekki are designed to establish integrated supply chains that include tire production. These developments indicate a strong potential for long-term growth and opportunities for domestic manufacturers in the automotive sector.

Financing Programs from Ride-Hailing Platforms Drive Passenger-Car Tire Sales

Ride-hailing operators, in collaboration with banks such as Stanbic IBTC, are providing five-year auto loans with minimal equity requirements. This initiative significantly reduces entry barriers for drivers and facilitates the expansion of passenger-car fleets. Due to the high utilization rates of ride-hailing vehicles, these cars experience accelerated tread wear, resulting in more frequent tire replacements compared to privately owned vehicles. The concentration of operations in cities such as Lagos, Abuja, and Port Harcourt creates predictable geographic demand clusters. Tire dealers who offer on-site fitting services and maintenance plans are well-positioned to capitalize on this demand and cater to the specific needs of ride-hailing operators in these regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic FX Shortages | −1.4% | Nationwide | Short term (≤ 2 years) |

| Counterfeit-tire Influx | −0.8% | Oyo, Osun, Kebbi, Borno | Medium term (2-4 years) |

| Power-supply Volatility | −0.7% | Lagos, Ogun, Kaduna | Medium term (2-4 years) |

| Under-developed Natural-Rubber Chain | −0.5% | Edo, Delta, Ogun, Cross River | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic FX Shortages Inflate Import Costs

The naira depreciated from approximately NGN 362.6/USD in 2019 to around NGN 900/USD by the end of 2023, before weakening further to about NGN 1,500/USD levels in 2025.[2]“FX Window Exclusions,” Central Bank of Nigeria, cbn.gov.ngImporters forced into parallel markets face unfavorable rates that erode margins and retail affordability. Elevated diesel prices compound input costs for domestic assemblers, slowing progress on local production initiatives. Importers operating in parallel markets encounter unfavorable exchange rates, which compress profit margins and reduce retail affordability. Additionally, rising diesel prices have escalated input costs for domestic assemblers, further impeding progress on local production initiatives and affecting the overall market dynamics.

Persistent Counterfeit Tire Influx Through Porous Borders

Illegal tires, which sell at 40% to 60% below the prices of genuine products, significantly erode brand equity and pose serious risks to road safety, according to the Standards Organization of Nigeria (SON). The smuggling routes used for these illegal tires are often shared with traffickers of fuel and rice, highlighting critical enforcement gaps along Nigeria’s extensive 4,000-kilometer land frontier. These gaps in enforcement have a detrimental impact on the volumes handled by legitimate distributors, further exacerbating the challenges faced by the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: All-Season Dominance Reflects Climate Realities

In 2025, all-season products dominated the Nigerian tire market, accounting for 63.15% of the market share, and are projected to grow at a CAGR of 6.84% through 2031. Considering Nigeria's unique dual rainy dry cycle and its lack of sub-zero temperatures, year-round tire compounds have emerged as the preferred and economical choice for both private motorists and ride-hailing services. Demand for summer tires is driven by performance-focused drivers and specific logistics applications that necessitate heat-rated tread compounds. Meanwhile, winter tires see minimal uptake. Tire manufacturers are now innovating by blending silica with carbon black formulations, achieving a balance of wet grip and heat resistance, which serves as a key differentiator in Nigeria's price-sensitive retail market. To address concerns over counterfeit imports, distributors are prominently showcasing SON quality seals, thereby bolstering customer confidence.

Consumer education initiatives are actively promoting best practices in tire rotation and inflation, aiming to extend tread life and resonate with the cost-conscious nature of the Nigerian market. With 60% of roads being unpaved, there is a heightened demand for puncture-resistant tread patterns and reinforced sidewalls. In an effort to challenge premium brands, tier-two brands are now offering mileage warranties, striking a balance between competitiveness and affordability. The Nigerian tire market continues to evolve, driven by these factors and the increasing focus on cost efficiency and product reliability.

By Tire Design: Radial Technology Leads Market Evolution

In 2025, Nigeria's tire market observed radials commanding a dominant 79.33% share, driven by their fuel efficiency and extended tread life, which justified the higher initial cost. Bias construction continues to remain prevalent in agricultural machinery and off-road segments, where challenges such as overloading and uneven road surfaces are routine. Furthermore, non-pneumatic or airless designs, which are experiencing a robust 9.07% CAGR, are increasingly favored by mining and security fleets that prioritize uptime. In a significant development, the Standards Organization of Nigeria (SON) has initiated the drafting of technical standards for airless tires, signaling a push towards broader commercialization.

Original equipment manufacturer assemblers are increasingly adopting radial specifications for new passenger cars and light-commercial vehicles, further strengthening their market dominance. Additionally, ride-hailing cooperatives are entering bulk purchase contracts that not only include tire acquisitions but also scheduled rotation and balancing services, ensuring consistent radial replacement cycles. On another front, parallel importers are leveraging foreign exchange fluctuations by sourcing surplus inventory from Asian hubs. However, they are facing challenges as increasing compliance checks are narrowing this arbitrage opportunity.

By Vehicle Type: Passenger Cars Drive Market Growth

In 2025, passenger car tires accounted for 39.14% of Nigeria's tire market, with a projected CAGR of 7.01% through 2031. As Nigeria's middle class expands and gains better access to financing, first-time car purchases are on the rise. E-commerce's last-mile delivery boosts demand for light commercial vehicles (LCVs), while heavy trucks see sustained demand through interstate freight corridors, notably linking Apapa port to northern markets. While motorcycles play a crucial role in rural mobility, their growth is stagnating due to urban authorities limiting two-wheeler taxis in central business districts.

Ride-hailing fleets drive 3 to 4 times the weekly mileage of privately owned cars, leading to tire replacements in under nine months. To capitalize on this rapid turnover, tire retailers strategically position themselves near major ride-hailing inspection centers. Meanwhile, trucking fleets are increasingly partnering with retread services, achieving lower per-kilometer costs and aligning with sustainability goals.

By Application: On-Road Usage Dominates Demand

In 2025, on-road tires dominated Nigeria's tire market, capturing 85.46% of the share and projected to grow at a 7.33% CAGR through 2031, driven by highways accommodating the bulk of passenger and freight traffic. Meanwhile, off-road segments, particularly in construction, mining, and agriculture, demand specialized carcass structures and command premium pricing. Government initiatives, like the Lagos Badagry expressway expansion, bolster on-road mileage, and while rail network upgrades are on the horizon, they aren't expected to impact road freight demand before 2030.

As container volumes surge, port-linked logistics corridors boost on-road tire consumption. This uptick prompts fleet operators to embrace predictive maintenance and telematics, monitoring tread depth and temperature to mitigate blowouts. In mechanized agriculture, off-road users are gravitating towards imported low-pressure radial designs, which effectively reduce soil compaction.

By End User: Aftermarket Dominance Signals Replacement Focus

In 2025, Nigeria's tire market saw the aftermarket dominate, accounting for 73.11% of the total size. This trend underscores the country's aging vehicle fleet and its long-standing history of importing used vehicles. On Nigeria's rough roadways, replacement cycles have become more frequent. Meanwhile, smaller trucking firms are opting for retreads, extending tire life at just a third of the cost of new units. Notably, demand from original equipment manufacturers (OEMs) is surging, with an impressive 8.15% CAGR, driven by the expansion of local assembly under knockdown kit (CKD) regimes.

Regionally assembled tire ranges now feature prominently in OEM-approved fitment programs, including brands like Dunlop, Michelin, and Bridgestone. Furthermore, distributors are enhancing their offerings by integrating fleet management software with tire sales, leading to lucrative service contracts that encompass installation, alignment, and telemetry-based condition monitoring.

By Rim Size: Mid-Range Sizes Lead Preferences

In 2025, rims measuring 15 to 20 inches accounted for 53.22% of Nigeria's tire market share, catering primarily to mainstream sedans, crossovers, and light commercial vehicles (LCVs). Rims exceeding 20 inches, witnessing a CAGR of 8.36%, are favored by premium SUVs and performance cars, especially among the affluent in Lagos and Abuja. While rims under 15 inches still find their place in sub-compact models and older fleets, their market share is slowly diminishing as consumers increasingly opt for larger wheels, prioritizing aesthetics and ride comfort.

As tire prices surge with increasing diameter, the demand for premium rims boosts unit revenue. To alleviate the strain on working capital, retailers are adopting a j inventory approach, seamlessly integrated with digital order portals. This strategy not only minimizes the risk of dead stock but also ensures consistent service levels.

By Propulsion: Internal Combustion Still Dominates, EVs Emerge

In 2025, Nigeria's tire market was dominated by internal combustion vehicles (ICVs), commanding a substantial 90.55% share, due to well-established fuel distribution networks and competitive purchase prices. Meanwhile, battery electric vehicles (BEVs), though still a niche player, are on the rise with an impressive CAGR of 11.15%. This growth is primarily driven by corporate fleets, drawn by the allure of reduced operating costs and enhanced ESG credentials. In the premium segments, hybrid volumes are gaining traction, bolstered by brand importers who offer bundled maintenance services and access to charging stations.

BEV tires are specially designed with low rolling resistance compounds and reinforced sidewalls, catering to the added weight of their battery packs. Tire assemblers, eyeing partnerships with Chinese firms, are optimistic about establishing localized EV fitting lines. However, they await improvements in the national grid's reliability and the expansion of the charging infrastructure.

Geography Analysis

Lagos State, home to the majority of Nigeria’s registered vehicles, remains the dominant hub for the nation's tire market. The city's high traffic density and active port operations result in frequent tire replacements, which support a complex distribution network stretching from Apapa to Alimosho. Wholesalers, utilizing cross-docking hubs along the Lagos Ogun corridor, are able to replenish retail stock within 24 hours, effectively mitigating delays caused by foreign exchange fluctuations.

In contrast to the southern region, northern trade centers such as Kaduna, Kano, and Abuja place greater emphasis on heavy-duty and agricultural tires. CKD plants in Kaduna anchor original equipment manufacturer demand, while freight connections in Kano drive higher turnover of truck tires. Additionally, government fleets headquartered in Abuja represent a reliable institutional customer base, frequently engaging in open tenders that require compliance with SON standards.

In the Niger Delta, the oil and gas logistics in Rivers and Bayelsa create specific requirements for specialized tires. These tires, designed to resist heat and punctures, are critical for navigating rough terrains and withstanding bitumen spills. Meanwhile, in the eastern commercial centers of Onitsha and Aba, dynamic trading networks accelerate tire shipments into Cameroon and Niger, positioning the region as an informal re-export hub. Furthermore, while Cross River’s rubber plantations remain undercapitalized, they offer significant long-term potential as a raw material source for any future domestic tire manufacturing plant.

Competitive Landscape

In the competitive landscape of Nigeria's tire industry, the top five players command significant influence, supported by extensive dealer networks and certifications from the Standards Organization of Nigeria (SON). While Michelin and Dunlop closed their local factories in 2006 and 2008, respectively, the market has since been dominated by imports, leaving retailers vulnerable to currency fluctuations. Operating under the Dunlop license, DN Tyre & Rubber Plc maintains a limited domestic presence, sourcing output from Pamol rubber estates.

Digital platforms such as Tyreman.ng are transforming the market, offering over 10,000 SKUs and providing mobile fitting services across Nigeria, which alleviates the burden of traffic for Lagos drivers. Meanwhile, Chinese manufacturers, including Linglong and Sailun, are expanding the market with their cost-effective offerings, facilitated by direct-import agreements. This influx not only increases consumer choices but also complicates the dynamics of brand loyalty.

Industry participants are focusing on an omnichannel approach, securing fleet-service contracts, and introducing innovations such as airless tires and low rolling resistance technologies, all designed for Nigeria's unique road conditions. In alignment with sustainability goals, startups like FREEE Recycle are converting end-of-life tires into rubber tiles and alternative fuels, indicating a growing revenue stream within the circular economy.

Nigeria Tire Industry Leaders

Bridgestone Corporation

Michelin

The Goodyear Tire & Rubber Company

Continental AG

Pirelli & C. S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: French tire major Michelin is making a strategic comeback to Nigeria in 2025, nearly two decades after exiting local production. The company has shifted to a direct local operating model with a Lagos-based office. Focus is on rebuilding OEM and premium vehicle fitment relationships.

- May 2025: Stallion Group launched a new vehicle assembly plant in Enugu State. The initial plan includes assembling approximately 2,000 hybrid vehicles, with expansion into buses.

Nigeria Tire Market Report Scope

The scope includes segmentation by season (summer, winter, and all-season), tire design (radial, bias, and non-pneumatic/airless), vehicle type (two-wheelers, passenger cars, light commercial vehicles, heavy commercial trucks and buses, and off-the-road and specialty vehicles including agriculture, mining, and racing), application (on-road and off-road across construction, mining, and agriculture), end user (OEM and aftermarket including replacement and retread), rim size (below 15 inches, 15 to 20 inches, and above 20 inches), and propulsion (internal-combustion vehicles, battery-electric vehicles, and hybrid and fuel-cell vehicles).

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic/Airless |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks and Buses |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road (Construction, Mining, Agriculture) |

| OEM |

| Aftermarket (Replacement and Retread) |

| Below 15 inches |

| 15 to 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic/Airless | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks and Buses | |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road (Construction, Mining, Agriculture) | |

| By End User | OEM |

| Aftermarket (Replacement and Retread) | |

| By Rim Size | Below 15 inches |

| 15 to 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid and Fuel-Cell Vehicles |

Key Questions Answered in the Report

What is the current value of the Nigeria tire market?

As of 2025, the market is valued at USD 0.82 billion and is expected to reach USD 1.19 billion by 2031.

How fast is the passenger-car tire segment growing?

Passenger-car tires are projected to expand at a 7.01% CAGR between 2026 and 2031, outpacing all other vehicle categories.

Why do aftermarket sales dominate Nigeria’s tire landscape?

An aging fleet, rough road conditions, and a historical reliance on used-vehicle imports drive frequent replacement, giving the aftermarket 73.11% share in 2025.

Which rim sizes are most popular?

Mid-range 15 to 20 inch rim sizes account for 53.22% of 2025 sales, though above-20-inch sizes are the fastest-growing due to premium-SUV adoption.

Page last updated on: