Iran Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

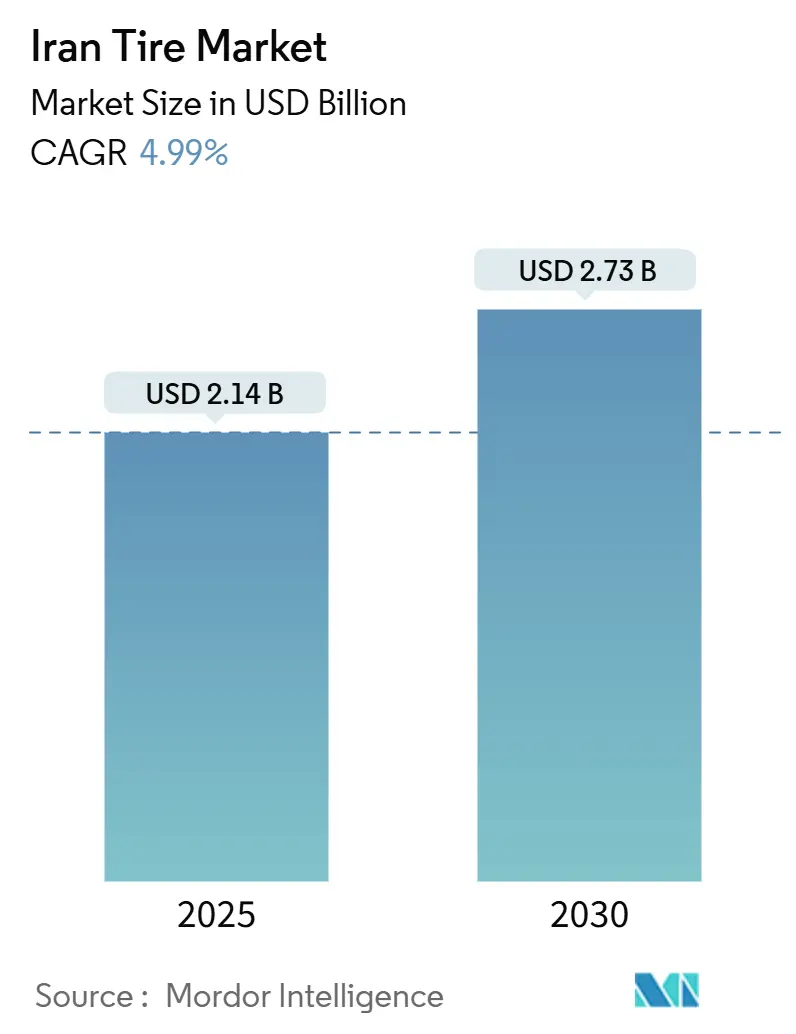

| Market Size (2025) | USD 2.14 Billion |

| Market Size (2030) | USD 2.73 Billion |

| Growth Rate (2025 - 2030) | 4.99% CAGR |

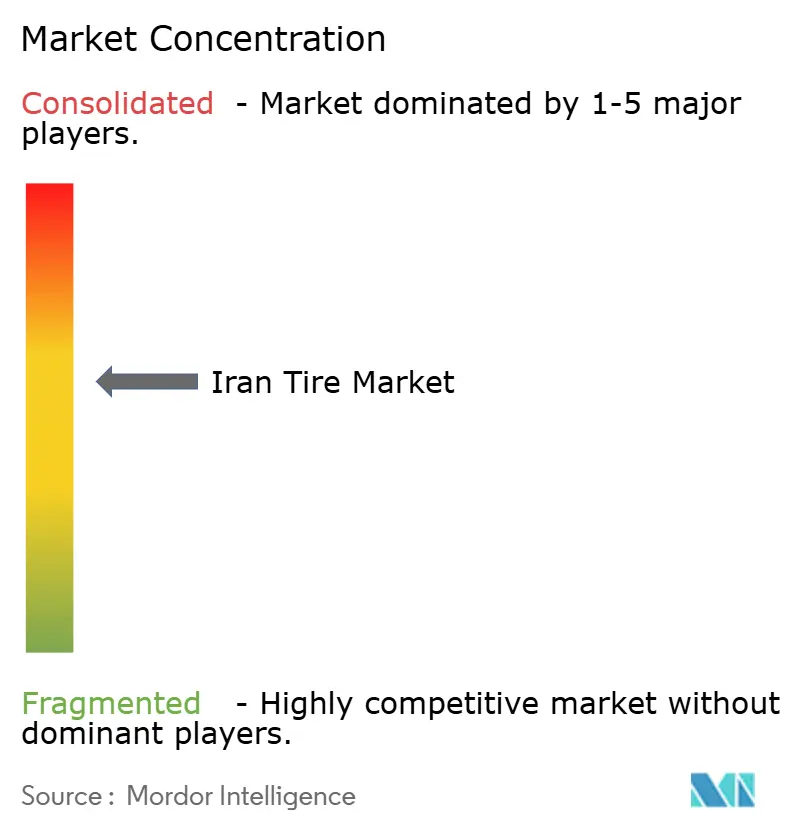

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iran Tire Market Analysis by Mordor Intelligence

The Iranian tire market stood at USD 2.14 billion in 2025 and is forecast to reach USD 2.73 billion by 2030, registering a 4.99% CAGR over 2025-2030. Domestic vehicle production, government-subsidized pricing schemes, and a dual-channel distribution structure continue to anchor replacement demand. A steady localization drive by Iran Khodro (IKCO) and SAIPA is deepening ties with domestic suppliers, while new technology-transfer deals, such as Linglong’s partnership for the Arya Hamoon plant, show the industry’s determination to modernize despite sanctions headwinds. Harsh road conditions and extreme summer heat shorten replacement cycles, keeping aftermarket volumes high, and the gradual roll-out of electric taxi fleets in Tehran is seeding demand for low-rolling-resistance (LRR) tires. Altogether, these forces position the Iranian tire market for measured but resilient expansion through the end of the decade.

Key Report Takeaways

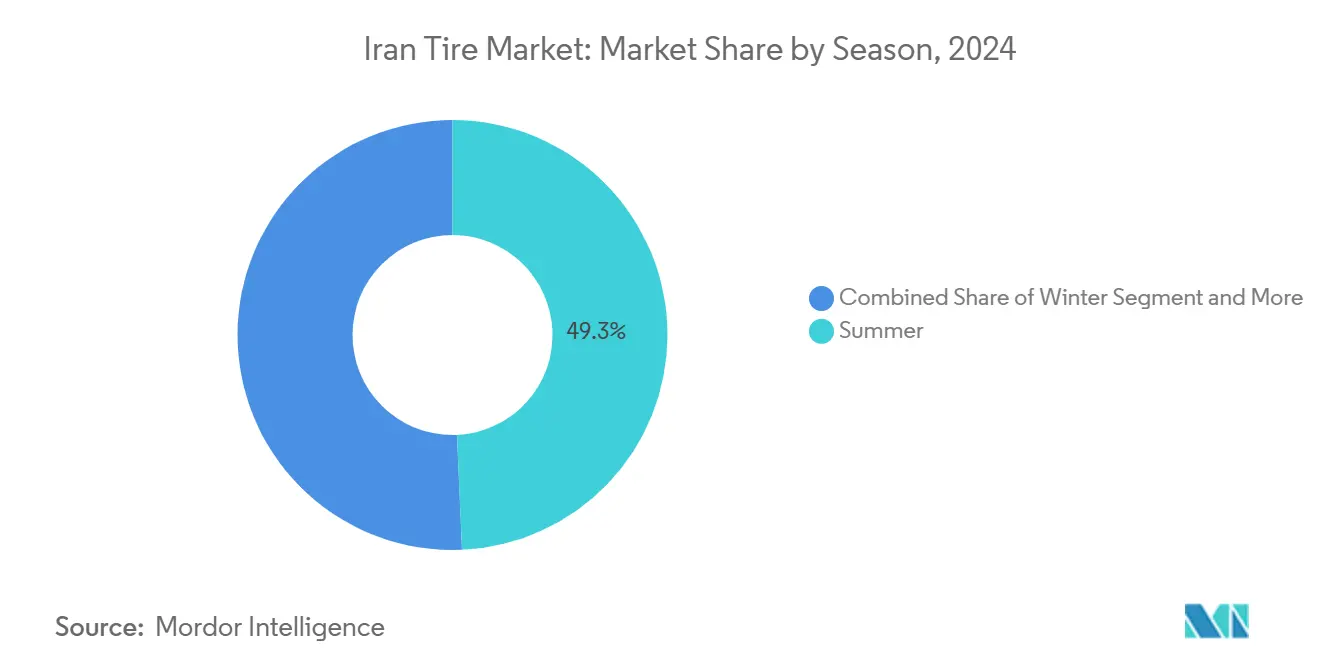

- By season, summer tires commanded 49.33% of the Iranian tire market share in 2024; winter tires are advancing at a 6.12% CAGR through 2030.

- By tire design, radial construction accounted for 70.25% of the Iranian tire market share in 2024, whereas non-pneumatic/airless tires are forecast to post the fastest 7.58% CAGR to 2030.

- By vehicle type, passenger cars led with 43.16% of the Iranian tire market share in 2024, while the same segment is projected to expand at a 5.03% CAGR through 2030.

- By application, on-road led with 68.55% of the Iranian tire market share in 2024, while the same segment is projected to expand at a 5.47% CAGR through 2030.

- By end user, the aftermarket segment held 64.15% of the Iranian tire market share in 2024 and is growing at a 6.48% CAGR to 2030.

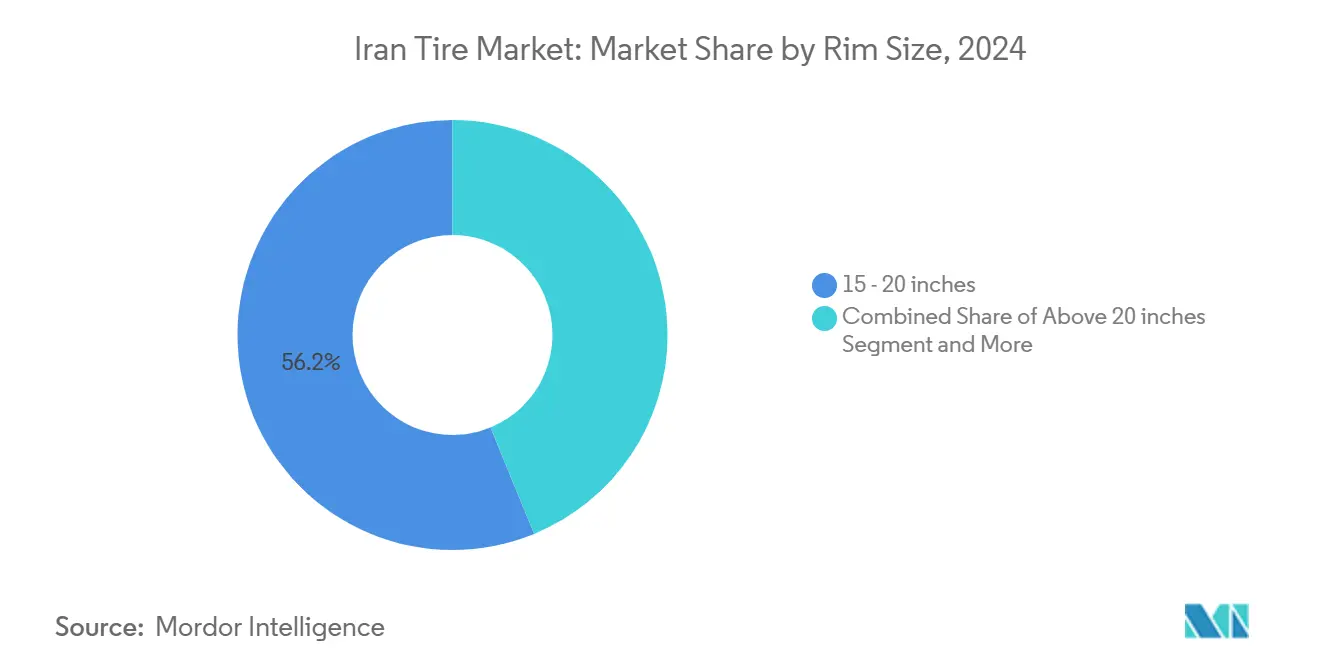

- By rim size, 15-20 inch products captured 56.17% of the Iranian tire market share in 2024, while above 20 inch offerings are projected to rise at a 7.14% CAGR through 2030.

- By propulsion, internal-combustion vehicles represented 83.18% of the Iranian tire market share in 2024, but battery-electric vehicles are set to record a 10.92% CAGR over 2025-2030.

Iran Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidized-Price Stabilizing Demand | +0.8% | National, major urban centers | Medium term (2-4 years) |

| Localization Push by IKCO and SAIPA | +0.6% | Manufacturing hubs in Tehran and Khorasan | Long term (≥ 4 years) |

| Shorter Replacement Cycles | +0.5% | Nationwide, intensified in southern provinces | Short term (≤ 2 years) |

| SUV and CUV Parc Expansion | +0.4% | Tehran, Isfahan and other urban corridors | Medium term (2-4 years) |

| Mandatory ID-Linked E-Sales | +0.3% | National digital roll-out | Short term (≤ 2 years) |

| Emerging EV-Taxi Pilots | +0.2% | Tehran metro area; roll-out to other big cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Subsidized-Price Program Stabilizing Replacement Demand

State-run allocation keeps subsidized passenger-car tires roughly 35-40% below open-market quotes, guaranteeing steady sell-through on platforms such as kala.ntsw.ir. Convergence of controlled and free prices has discouraged speculative hoarding, and quota caps of one pair per national ID every six months distribute purchases across the year. Manufacturers benefit from predictable factory gate volumes because subsidized tires must meet identical INSO quality benchmarks. Yet, as street prices narrow toward subsidized levels, some drivers are less willing to share personal data, challenging the system’s long-term traction.

OEM Localization Push by IKCO and SAIPA

IKCO and SAIPA, which command a notable share of national vehicle output, are escalating localization amid tight foreign-currency budgets, requesting a combined investment in emergency credit to shore up supply chains. Their strategy steers more volume to domestic tire firms that can deliver radial and tubeless lines that meet new model requirements in Khorasan and Tabriz. Technology-sharing deals, such as Kavir Tire’s acquisition of Matador radial know-how, underscore the Iran tire market’s commitment to homegrown competence. Localization also mitigates sanctions-related import risk, converting currency volatility into a structural tailwind for domestic contract awards.

Shorter Replacement Cycles from Harsh Roads and High Heat

Thermal cycling and rough asphalt shorten passenger-car tread life to well below global averages, especially in desert provinces where temperatures breach 50 °C. Mining and construction fleets see steeper attrition; tire specialists like BazarLastik tailor compounds to resist acidic soils and jagged quartz on open-pit haul roads. Data collected through Iran’s heavy-vehicle allocation portal confirms quicker scrappage in the south, creating a reliable aftermarket cadence that underpins factory utilization plans for domestic producers.

Rapid SUV and Crossover Parc Expansion

SUVs and CUVs already account for a significant share of local Chery output, lifting demand for 15-20 inch rims that captured the majority of 2024 volumes. Larger sidewalls and reinforced beads command premium prices, widening gross margins for producers able to scale bigger cavities and two-layer tread designs that dissipate heat under 50 °C summer road temperatures. Rising gasoline consumption confirms higher vehicle usage, accelerating wear rates for heavier SUVs [1]“Fuel Consumption Hits New Highs,” Tehran Times, tehrantimes.com. The Iranian tire market, therefore, benefits doubly from larger diameter sizes and shorter replacement cycles in this segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FX Volatility Inflating Input Costs | −1.2% | Nationwide, acute in Tehran & Isfahan clusters | Short term (≤ 2 years) |

| U.S. Sanctions Blocking Tech Inflow | −0.8% | National, especially advanced radial investments | Long term (≥ 4 years) |

| Aging Truck Slowing Radial Conversion | −0.4% | Commercial transport corridors | Medium term (2-4 years) |

| Water-Stress Limiting Rubber Projects | −0.3% | Southern and central drought-prone provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FX Volatility Inflating Imported Raw-Material Costs

Because specialty carbon black, steel cord, and synthetic rubber remain dollar-denominated, every rial swing compresses margins at local plants. DSGE modeling links sanctions shocks to sharp drops in intermediate-goods imports, reinforcing raw-material scarcity. Even with domestic carbon-black output, e.g., Carbon Simorgh’s 42,000 t line, higher-grade inputs must still be sourced abroad, raising ex-works prices whenever the free-market rate jumps. Preferential currency windows help temporarily, but unpredictable allocation schedules force conservative inventory builds that tie up cash.

Secondary U.S. Sanctions Limiting Technology Inflow

Since 2018, Western licensors have walked away from Iranian projects, stalling upgrades such as smart-tire sensor lines and fully automated curing presses. Chinese groups have partially filled the gap; Linglong’s 3.1 million-unit project is emblematic, but their equipment lacks some cutting-edge automation available from European suppliers[2]“Linglong’s Iran Expansion,” European Rubber Journal, european-rubber-journal.com. The resulting tech lag limits the Iranian tire market’s export competitiveness just as nearby Turkey and Pakistan emphasize EU-compliant quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: Summer Dominance Reflects Climate Reality

Summer patterns represented 49.33% of the Iranian tire market in 2024, underpinned by year-round high temperatures across the central plateau and coastal south. Winter tires occupy a smaller base today, yet will grow at a 6.12% CAGR as motorists in Gilan, Mazandaran, and Kurdistan respond to stricter safety checks on mountain passes. Therefore, the Iranian tire market size for winter products is set to climb faster than total demand, although absolute volume will still lag summer lines through 2030.

Consumer education campaigns and improved supply of INSO-certified snow patterns are shortening the time needed for segment adoption. Meanwhile, all-season tires remain popular with Tehran commuters who face mixed weather throughout the year. Suppliers tailor compound blends by adding higher silica content to keep tread pliable below 7 °C, ensuring uniform performance while extending mileage warranties, an important selling point in price-sensitive cities.

By Tire Design: Radial Technology Leads Modernization

Radial construction secured 70.25% of Iran's tire market share in 2024, reflecting three decades of factory upgrades funded through domestic bonds and technology deals with Matador and Linglong. Bias designs survive mainly in older agriculture and heavy-haul fleets where low unit cost outweighs performance. The Iranian tire market size for non-pneumatic/airless solutions remains niche but will gain from mining and military orders, expanding at a 7.58% CAGR to 2030.

Domestic toolmakers now supply a significant share of bead-winding and extrusion equipment, lowering capex and accelerating radial-line deployment. As OEMs shift completely to tubeless specs after 2026, the residual bias segment will shrink further, freeing capacity producers can redeploy toward emerging EV-optimized SKUs featuring low rolling-resistance tread blocks and noise-dampening foam inserts.

By Vehicle Type: Passenger Cars Drive Volume Growth

Passenger-car demand accounted for 43.16% of the Iranian tire market size in 2024 and is projected to grow at a 5.03% CAGR, thanks to a robust pipeline of IKCO and SAIPA sedans plus brisk used-vehicle trade. Light commercial vans are seeing momentum from e-commerce last-mile delivery firms, while heavy-truck replacements hinge on infrastructure freight volumes.

Two-wheelers remain indispensable in Tehran’s narrow lanes, yet their share in value terms is modest because their average rim size is less than 18 inches. Off-the-road mining and construction categories offer higher margins per kilogram, drawing specialist entrants who fabricate cut-resistant compounds for Komatsu and Caterpillar fleets operating in the Zagros range quarry belts.

By Application: On-Road Dominance Mirrors Infrastructure Focus

On-road fitments captured 68.55% of Iran tire market share in 2024 and should expand at a 5.47% CAGR on the back of improved expressways linking Mashhad, Isfahan, and the Persian Gulf ports. Off-road niches, mining, farming, and construction account for a smaller volume but command unit prices up to 3× higher because of tread depth and reinforcement layers.

Industrial tire dealers report quarry trucks in Kerman Province change sets every 1,500 hours due to abrasive sandstone, a cycle twice as quick as global norms. Domestic brands are experimenting with 3-ply carcasses and dual compound sidewalls to capture this premium. Agricultural uptake benefits from mechanization incentives in Fars, where new tractors qualified for subsidized tires in 2024.

By End User: Aftermarket Reflects Fleet Age Profile

Aftermarket volumes made up 64.15% of the Iranian tire market in 2024, and this channel is accelerating at a 6.48% CAGR as owners retain vehicles longer during economic uncertainty. OEM draw-downs mirror passenger-car output but remain below the total tire unit demand.

Retreading enjoys cost advantages that resonate with large truck fleets. The Aria Tire Complex quotes 30-50% savings versus new sets, reusing 80% of casing material, and reducing environmental load. For passenger-car owners, dealer networks now bundle wheel-alignment and nitrogen inflation packages, raising ticket sizes while anchoring brand loyalty.

By Rim Size: Mid-Range Sizes Dominate Present Demand

Rims between 15 and 20 inches represented 56.17% of the 2024 Iranian tire market share, driven by compact sedans and emerging CUVs. Above-20-inch SKUs will expand 7.14% CAGR as premium imports and domestic luxury models gain traction.

Mashhad Wheel Manufacturing’s capacity now includes flow-forming lines for lightweight 22-inch alloys. This local supply reduces dependence on Chinese wheel imports, directly supporting larger-rim tire uptake. However, Less than or equal to 14-inch rims in rural taxi fleets remain common, constraining demand for ultra-low-profile rubber outside major metros.

By Propulsion: ICE Still Rules While EV Momentum Builds

ICE platforms secured 83.18% of the Iranian tire market in 2024, yet battery-electric fitments will deliver the fastest 10.92% CAGR, propelled by generous tariff breaks and clean-air mandates. Hybrid volumes trail but could accelerate once domestic automakers localize 48-V systems.

LRR compounds and aerodynamic sidewalls are now in pilot production, with Kavir Tire benchmarking EU-label A-rated rolling resistance. As charging corridors expand along the Qom–Isfahan expressway, EV drivers will demand higher-speed rated tires, widening the premium tier and reinforcing value growth over mere unit gains.

Geography Analysis

Iran’s domestic market remains the anchor, but rising non-oil exports to Turkey show why tire manufacturers eye neighboring states for incremental sales. Plants clustered around Tehran, Isfahan, and Kerman enjoy road and rail links that keep freight costs competitive for outbound loads to Iraq, Azerbaijan, and Armenia. Meanwhile, the under-construction Arya Hamoon facility in Sistan-Baluchestan plans to earmark a notable capacity for Pakistan and Afghanistan, leveraging proximity to the border.

Domestic demand varies sharply by climate. Desert provinces such as Khuzestan order heat-resistant tread rubber year-round, whereas Gilan and Mazandaran retailers shift significant winter volumes between November and March. Tehran’s vehicle parc secures its position as the single largest urban market, bolstered by mandatory periodic technical inspections that encourage timely replacements.

Regional infrastructure spending influences off-road volumes. Kerman’s copper mines fuel heavy-truck orders, while Khuzestan’s irrigation projects drive flotation-tire demand on sugarcane farms. Government data extracted from the kala.ntsw.ir portal lets producers allocate inventory precisely, although some still sidestep full reporting requirements, causing sporadic shortages in provincial towns. Overall, geography favors suppliers with multi-plant networks able to shuttle inventory in response to these micro-market spikes.

Competitive Landscape

The Iranian tire market shows moderate concentration. Kavir Tire, Barez Industrial Group, and Iran Tire Manufacturing remain the heavyweights, each running integrated compound mixing and bead-wire lines to cap imported content. Goodyear maintains a foothold through Nikran Tire Co., relying on premium positioning and a loyal high-income customer base.

Technology partnerships form the competitive fulcrum. Linglong’s equipment supply to Arya Hamoon brings automated curing and X-ray inspection, whereas Matador’s earlier radial-wire deal helped Kavir Tire build tubeless capabilities. Domestic groups that upgrade now can meet OEM requests for EV-compatible low-RR designs, an area where imported brands previously held an edge.

Strategic moves also include capacity expansions: Barez started civil works on a 15 ktpa TBR plant in Lorestan, targeting completion in 2025 [3]“Investment in Lorestan Plant,” Barez Industrial Group, barez-tires.com. Mashhad Wheel’s upstream wheel venture positions it as a systems supplier, bundling tires and rims for CKD kits. Meanwhile, smaller players explore retreading franchises to lock in recurring revenue. With sanctions likely to persist, the race centers on local raw-material integration, cost control, and compliance with INSO labeling norms prohibiting importing tires older than two years at customs.

Iran Tire Industry Leaders

Barez Industrial Group

Kavir Tire Co.

Yazd Tire Co.

Iran Tire Manufacturing Co.

Artawheel Tire (Aptrco)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Barez Industrial Group broke ground on a greenfield plant in Aligoudarz to deliver 15 ktpa of truck, bus radial, and light-truck tires by Jul 2025.

- January 2023: Barez Industrial Group launched Iran’s first giant OTR tire project on a 220-acre site expected to go live within three years.

Iran Tire Market Report Scope

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic / Airless |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks and Buses |

| Two-Wheelers |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road (Construction, Mining, Agriculture) |

| OEM |

| Aftermarket (Replacement and Retread) |

| Below 15 inches |

| 15 - 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic / Airless | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks and Buses | |

| Two-Wheelers | |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road (Construction, Mining, Agriculture) | |

| By End User | OEM |

| Aftermarket (Replacement and Retread) | |

| By Rim Size | Below 15 inches |

| 15 - 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid and Fuel-Cell Vehicles |

Key Questions Answered in the Report

How large is the Iran tire market as of 2025?

The Iran tire market size reached USD 2.14 billion in 2025 and is projected to climb to USD 2.73 billion by 2030.

What is the expected growth rate for tires in Iran between 2025 and 2030?

Overall demand is forecast to advance at a 4.99% CAGR during the 2025-2030 period.

Which tire segment leads in market share?

Radial designs dominate with 70.25% share of 2024 shipments in the Iran tire market.

Why does the aftermarket account for most sales?

An aging vehicle parc, harsh road conditions, and government subsidy programs push replacement volumes to 64.15% of 2024 demand.

Page last updated on: