Indonesia Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

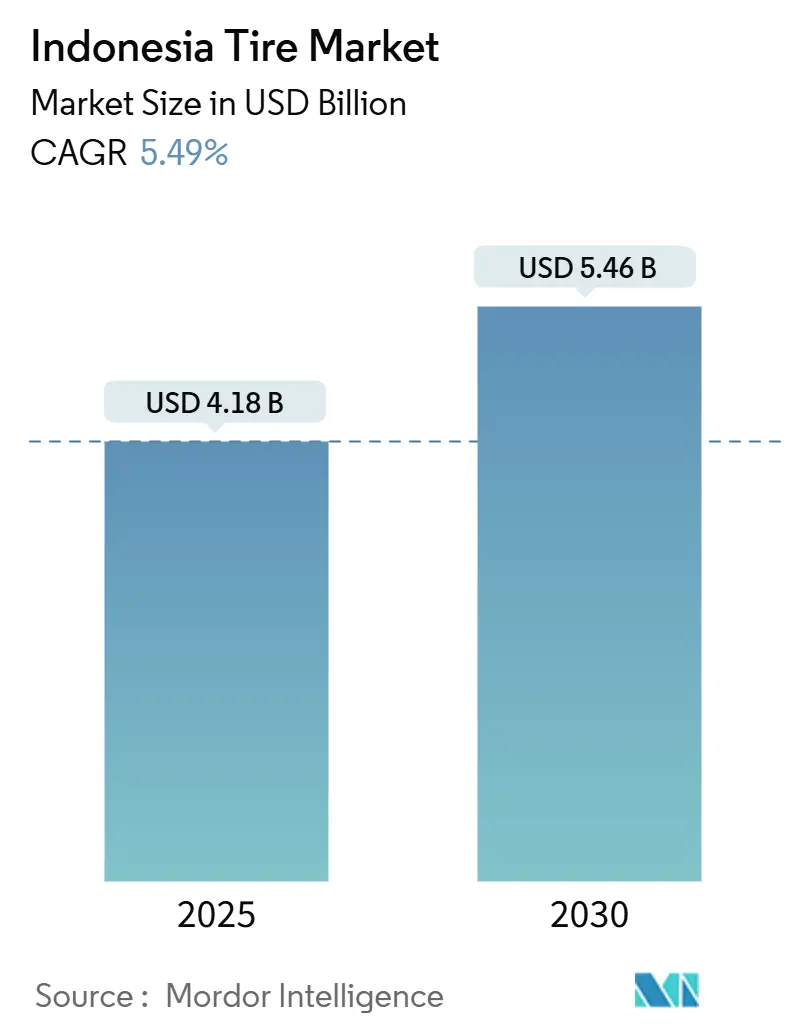

| Market Size (2025) | USD 4.18 Billion |

| Market Size (2030) | USD 5.46 Billion |

| Growth Rate (2025 - 2030) | 5.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Tire Market Analysis by Mordor Intelligence

The Indonesian tire market size reached USD 4.18 billion in 2025 and is forecast to expand at a 5.49% CAGR to reach USD 5.46 billion by 2030. This outlook reflects the Indonesian tire market benefiting from the country’s position as Southeast Asia’s largest automotive base, where motorcycles dominate daily mobility and commercial fleets underpin national freight flows. Demand is reinforced by post-pandemic travel recovery, government road-building programs, and the reality that road transport carries a major share of Indonesia’s freight volume. The Indonesian tire market also gains from rising electrification incentives that encourage EV-specific tire adoption, while regulatory barriers such as mandatory SNI certification protect compliant producers. Competitive intensity is climbing as Chinese entrants add capacity, but established local and global manufacturers retain advantages in distribution, brand strength, and technology alignment with Indonesia’s diverse operating conditions.

Key Report Takeaways

- By season, all-season products dominated with 47.33% of the Indonesian tire market share in 2024, whereas summer tires registered the highest 7.13% CAGR due to growing performance preferences.

- By tire design, radial construction captured 91.46% of the Indonesian tire market share in 2024, and non-pneumatic/airless alternatives are expected to rise at a 7.58% CAGR during the forecast horizon.

- By vehicle type, two-wheelers led with 36.21% of the Indonesian tire market share in 2024, while passenger cars are projected to grow at a 6.11% CAGR to 2030.

- By application, on-road usage represented 63.08% of the Indonesian tire market size in 2024 and is forecast to maintain the fastest 5.82% CAGR as paved-road networks expand.

- By end user, the aftermarket accounted for 72.13% of the Indonesian tire market size in 2024, whereas OEM demand is advancing at a 6.46% CAGR through 2030.

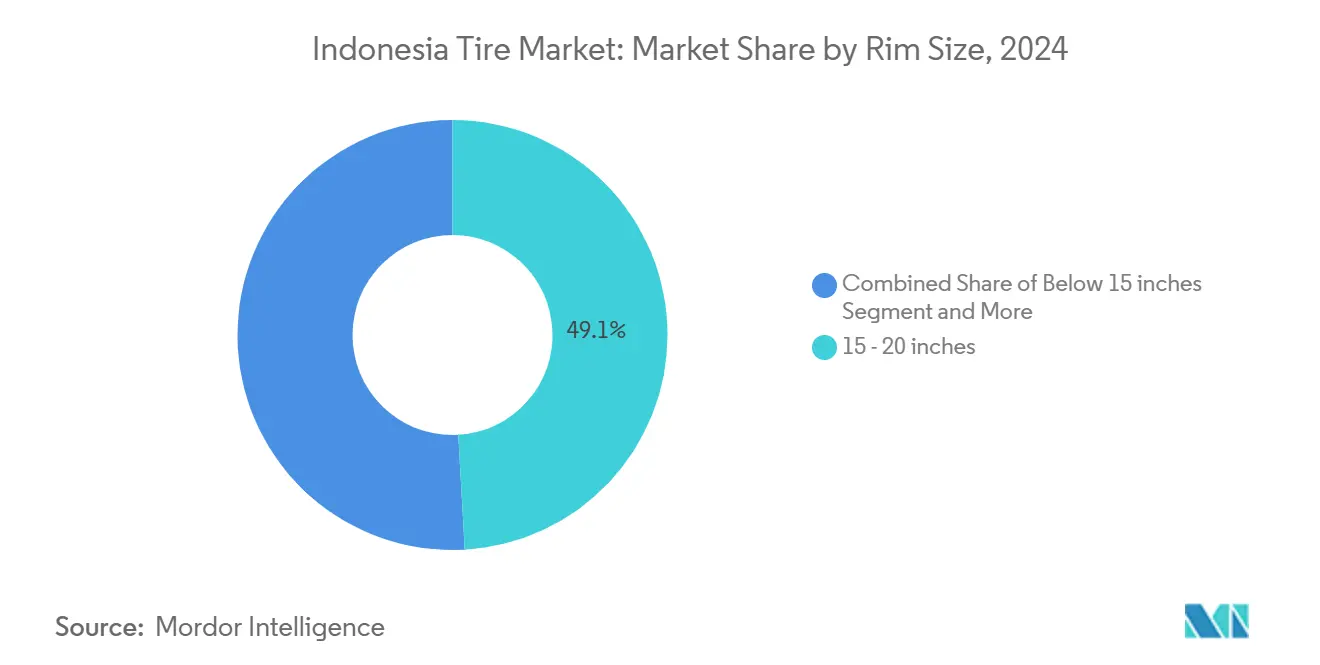

- By rim size, 15-20-inch products commanded 49.06% of the Indonesian tire market share in 2024, with above-20-inch categories expanding at a 7.81% CAGR as larger wheels gain popularity.

- By propulsion, internal combustion vehicles controlled 89.11% of the Indonesian tire market size in 2024, and battery EV fitments are projected to climb at a 10.13% CAGR to 2030.

Indonesia Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Surge in Two-Wheeler Ownership | +1.2% | Java and Sumatra | Short term (≤ 2 years) |

| Government Road-Infrastructure Boom | +0.9% | National | Medium term (2-4 years) |

| EV-Specific Tire Incentives | +0.8% | Major urban hubs | Medium term (2-4 years) |

| OEM Shift to Larger Rims | +0.7% | Urban markets | Medium term (2-4 years) |

| Fleet Digitalization and Predictive Buying | +0.6% | Java core cities | Long term (≥ 4 years) |

| Micro-Warehouse E-Commerce Logistics | +0.5% | Sumatra, Kalimantan, Sulawesi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Surge in Two-Wheeler Ownership Post-Pandemic

Motorcycle sales rebounded strongly in 2024 as commuters sought personal mobility that reduced public-transit exposure. Higher-displacement models used for intercity travel accelerated tread wear, lifting replacement frequency to 12–18 months for active riders. Digital financing platforms widened access for ride-hailing drivers, expanding the active fleet that fuels the Indonesian tire market. Infrastructure upgrades across secondary cities improved road links, encouraging longer motorcycle journeys that require premium tires. Manufacturers with broad two-wheeler portfolios, therefore, secure resilient volumes despite rising passenger-car penetration.

Government Road-Infrastructure Boom Unlocking Radial-Tire Demand

Annual public spending is rebuilding highways and port access roads, permitting heavier trucks and sustained speeds that benefit radial technology. Completed corridors in Java and Sumatra stimulate freight movement, raising replacement cycles for commercial tires that dominate the Indonesian tire market demand. Construction fleets consume significant volumes during the build phase, then shift to maintenance purchases that support long-term radial uptake. Regional projects in Kalimantan and Sulawesi replicate this pattern as outer-island logistics modernize. Local manufacturers with integrated rubber sourcing capture early contracts by meeting SNI quality rules [1]“Indonesia National Road Improvement Program,” Japan International Cooperation Agency, jica.go.jp.

EV-Specific Tire Incentives in 2026 Green Tax Reform

The forthcoming fiscal package will cut value-added tax on locally produced EV-optimized tires, spurring investments in low rolling resistance compounds and reinforced sidewalls. Early movers gain price advantages that accelerate Indonesia's tire market penetration among electric motorcycles and compact cars. The policy aligns with government targets for 2 million EV units by 2030, generating steady demand growth. Manufacturers leveraging in-house R&D and Indonesian rubber supplies can meet cost and performance criteria, positioning for export opportunities to other ASEAN EV hubs.

OEM Shift to ≥15-Inch Rims for Low-Cost SUVs/MPVs

Domestic automakers now specify 16- to 18-inch wheels on popular family models, reflecting middle-class preferences for premium styling and improved handling. The change requires tire makers to scale to larger capacities while containing costs for mass-market vehicles. Larger rim fitments carry higher unit values, lifting average selling prices in the Indonesian tire market. Consumers face steeper replacement expenses, which can lengthen aftermarket cycles or redirect demand to budget imports. Suppliers that lock multi-year OEM contracts secure baseline volumes and strategic production visibility [2]“Indonesia Operations Fact Sheet 2025,” Bridgestone Corporation, bridgestone.co.id.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retread Proliferation among Heavy Trucks | –0.8% | Java freight corridors | Short term (≤ 2 years) |

| Imported Budget Tires Squeezing Margins | –0.6% | Nationwide | Medium term (2-4 years) |

| Natural Rubber Price Volatility | –0.4% | All manufacturing hubs | Short term (≤ 2 years) |

| Skilled Labor Gap for Production | –0.3% | Java and Sumatra plants | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Retread Proliferation Across Heavy-Truck Segment

Long-haul operators extend casing life by up to 60% through professional retreading that costs roughly one-third of a new tire. Improved highway surfaces in the Indonesian tire market support multiple retread cycles, lessening premium replacement demand. Organized retreaders comply with SNI rules, legitimizing the practice and attracting large fleets. Premium brands counter by offering casing buyback programs and warranty extensions to retain loyalty. New entrants integrating retreading expand service portfolios that accommodate cost-focused customers.

Imported Budget Tires Pressuring Margins of Local Makers

Chinese producers exploit scale economies and localized factories to undercut domestic brands significantly at retail. Value-driven motorists and fleet owners gravitate toward these lower prices, diluting premium share within the Indonesian tire market. Domestic companies respond with lean manufacturing, product line simplification, and value sub-brands. SNI certification acts as a gatekeeper, yet established Chinese facilities already meet these standards, sustaining price rivalry. Profit retention thus depends on technology differentiation, channel partnerships, and after-sales support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: All-Season Dominance Reflects Climate Consistency

All-season products accounted for 47.33% of the Indonesian tire market size in 2024, mirroring a tropical climate that eliminates seasonal changeovers. The segment benefits from formulations tuned for heat resistance and monsoon traction, ensuring reliable year-round performance. Summer tires are gaining traction at a 7.13% CAGR among performance-oriented urban drivers seeking sharper handling on improved roads. Manufacturers promote silica-rich compounds and asymmetric tread patterns that deliver grip without compromising wear life. Winter tires remain niche imports for expatriate vehicles, contributing negligible revenue within the Indonesian tire market.

The expected persistence of warm weather supports ongoing R&D investments in all-season compound stability under high pavement temperatures. Summer tire growth parallels rising premium passenger-car sales and motorsport events that elevate consumer interest in responsive handling. Suppliers differentiate through UTQG ratings, wet-brake tests, and aquaplaning resistance messaging that resonates during monsoon seasons. Retailers position summer products alongside alloy-wheel upgrades that accompany the shift to larger rim sizes. Although winter products lack scale, they provide technology spillovers that enhance wet-grip features in tropical-tuned lines.

By Tire Design: Radial Technology Maintains Overwhelming Leadership

Radial construction held 91.46% of the Indonesian tire market share in 2024, supported by superior tread life and fuel efficiency across diverse terrains. Bias-ply designs survive in low-speed agriculture and legacy off-road vehicles but face continual cannibalization. Airless non-pneumatic formats will post a 7.58% CAGR as logistics firms pilot puncture-proof solutions for remote operations. Key manufacturers leverage Indonesian production bases to localize advanced steel-belt technology while minimizing import costs.

Scaling airless capacity requires new elastomer architectures and specialized molding equipment, prompting joint ventures with global innovators. Early deployments focus on forklifts, mining utility vehicles, and last-mile delivery fleets seeking zero-downtime operations. Radial technology continues upgrading through nanocomposite belts and low-rolling-resistance silica blends that support OEM emissions targets. The Indonesian tire market thus balances entrenched radial volumes with emerging design niches that secure high margins and technology branding.

By Vehicle Type: Two-Wheeler Dominance Faces Passenger-Car Momentum

Two-wheelers generated 36.21% of the Indonesian tire market share in 2024, underscoring motorcycles’ ubiquity for urban commuting and intercity travel. Passenger-car demand, however, is accelerating at a 6.11% CAGR thanks to income gains, affordable financing, and domestic vehicle assembly incentives. Light commercial vehicles expand alongside e-commerce logistics, while heavy trucks remain fundamental to plantation and mining supply chains that underpin the Indonesian tire market size.

Motorcycle tire evolution now centers on EV-specific models with reinforced sidewalls and low-noise tread blocks. Passenger-car growth creates opportunities for run-flat and self-sealing technologies suited to congested city travel, where roadside assistance may be delayed. Truck-segment suppliers broaden retread-compatible casings that satisfy cost-conscious fleet managers. Together, these shifts diversify revenue streams while preserving the Indonesian tire market's resilience, rooted in multi-segment exposure.

By Application: On-Road Usage Drives Market Growth

In 2024, on-road applications represented 63.08% of Indonesia's tire market size and will see the fastest 5.82% CAGR as highway density grows. Improved asphalt quality invites higher cruising speeds that raise heat build-up and accelerate tread wear, boosting replacement frequency. Off-road tires serve mining, plantation, and construction sites where puncture resistance and load capacity outweigh rolling efficiency. Cross-application designs emerge for mixed-service trucks traversing paved highways and plantation tracks within a single route.

Urbanization concentrates vehicle kilometers within metropolitan rings, incentivizing OEMs to source tires capable of low noise and strong wet-grip to satisfy safety regulations. Off-road markets continue upgrading to radial technology with cut-resistant compounds, increasing average selling prices. Manufacturers provide split service networks that place on-road focused centers in cities and off-road specialists near mining zones, ensuring nationwide coverage in the Indonesian tire market.

By End User: Aftermarket Dominance Reflects Replacement Patterns

The aftermarket secured 72.13% of the Indonesian tire market share in 2024, reflecting an aging vehicle parc and frequent motorcycle tire changes. OEM channels, though smaller, will grow at a 6.46% CAGR as Indonesia deepens local vehicle manufacturing and enforces rising local content thresholds. OEM contracts deliver volume stability and innovation alignment, but compress margins; aftermarket sales allow brand differentiation and channel diversity across retail outlets nationwide.

Digital marketplaces expand tire visibility and price transparency, forcing traditional dealers to add value through installation services and warranty extensions. OEM growth fuels standardization in tire specifications, especially for EVs that require certified low-rolling-resistance products. The Indonesian tire market, therefore, hinges on synchronized strategies that secure OEM pipelines while sustaining aftermarket brand loyalty.

By Rim Size: Mid-Range Sizes Dominate Current Demand

Products between 15 and 20 inches captured 49.06% of the Indonesian tire market share in 2024 due to their fitment on mainstay SUVs, MPVs, and pickup trucks. Above-20-inch variants will climb at 7.81% CAGR as premium vehicles popularize 21- to 24-inch alloys for road presence and handling. Sub-15-inch sizes continue servicing economy cars and commercial vans priced for fuel efficiency, yet their share contracts as fleet buyers upgrade vehicle classes.

Manufacturers enlarge curing presses and mold inventories to accommodate the broader diameter range while optimizing inventory turnover. Retailers bundle alloy-wheel packages with larger-size tires, incentivizing consumer upgrades at the point of sale. In rural areas, the high price of large rims restrains adoption, retaining demand for 15-inch bias-ply tires on legacy pickups. Balanced production planning mitigates the risk of overstocking uncommon sizes while fulfilling the Indonesian tire market's appetite for style-driven wheel trends.

By Propulsion: ICE Dominance Faces EV Transition

Internal-combustion vehicles still accounted for 89.11% of the Indonesian tire market share in 2024, yet battery electric vehicles will record a 10.13% CAGR through 2030. Hybrid models establish a transitional niche, appealing to commuters seeking lower fuel bills without charging constraints. EV tire requirements include low rolling resistance, reinforced bead structures for instant torque, and acoustic foam layers that damp cabin noise.

Suppliers qualifying for 2026 tax incentives gain pricing leverage and early specification access with OEMs launching Indonesian-built EV models. ICE tires continue evolving toward fuel-efficient tread compounds to meet future emissions standards. Recycling regulations under draft consideration could mandate recovery targets, influencing compound design for EV and ICE segments and adding complexity to the Indonesian tire market supply chain.

Geography Analysis

Java remains the epicenter of the Indonesian tire market, hosting a significant share of paved roads and housing major production hubs in Tangerang and Bekasi. Jakarta’s dense traffic sustains high two-wheeler and passenger-car replacement cycles, while the port of Tanjung Priok anchors distribution to outer islands. Sumatra ranks second in demand as the plantation and mining sectors generate heavy-truck volumes that depend on durable radial casings suited to mixed terrain. Manufacturers leverage Medan and Palembang warehouses to shorten delivery times and cut inventory costs.

Kalimantan and Sulawesi emerge as growth corridors where expanded highways and resource extraction projects raise vehicle counts per capita. Government incentives encouraging eastern industrialization draw tire makers to establish satellite logistics centers that feed onsite service trucks. These islands, once underserved, now contribute incremental sales of large-rim SUV tires favored by company executives and all-steel truck radials required for mining haul roads. The Indonesian tire market thus diversifies beyond Java while still depending on its manufacturing backbone.

Logistics challenges inherent to an archipelago persist. Inter-island shipping adds lead time and cost, prompting distributors to hold buffer stocks in bonded zones near secondary ports. E-commerce fulfillment centers adopt micro-warehouse models with predictive inventory algorithms to maintain service levels despite maritime delays. SNI certification enforces consistent quality across regions, protecting consumers in remote provinces from substandard imports. Companies with national service footprints use mobile installation units and retread pickup programs to build loyalty, strengthening geographic coverage for the Indonesian tire market.

Competitive Landscape

PT Gajah Tunggal Tbk leads the Indonesian tire market by combining integrated rubber plantations, diversified product lines, and nearly 1,400 nationwide TireZone outlets that secure aftermarket reach. Bridgestone Indonesia, Hankook, and Michelin operate modern plants that export to ASEAN and OECD markets, leveraging Indonesia’s labor cost advantage while meeting global quality benchmarks. Chinese entrant ZC Rubber invested USD 280 million in its Kendal Industrial Park facility, completing construction in just 233 days and signaling accelerated competitive timelines [3]“Kendal Industrial Park Facility Overview,” ZC Rubber, zcrubber.com.

Strategic actions emphasize capacity expansions and technology upgrades rather than price wars alone. PT Gajah Tunggal introduced Zeneos Ionity, an electric-motorcycle tire with low rolling resistance and reinforced sidewalls targeting ride-hailing fleets. Hankook partners with Indonesian EV start-ups to co-develop graphene-enhanced compounds that cut rolling resistance. These moves showcase a pivot toward specialized niches that command margin premiums within the Indonesian tire market.

Regulatory compliance shapes competition through mandatory SNI standards that demand consistent performance and traceability. Established manufacturers integrate in-house laboratories and TÜV-accredited audits to streamline certification renewals, while newcomers often partner with local distributors to navigate bureaucratic processes. The competitive field, therefore, balances cost-driven entrants with innovation-centric incumbents, each leveraging Indonesia’s market scale and strategic export location to pursue regional leadership.

Indonesia Tire Industry Leaders

PT Gajah Tunggal Tbk

Bridgestone Tire Indonesia

Hankook Indonesia

Michelin Indonesia

Goodyear Indonesia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sailun Group began commercial output at its new Demak City plant, marking the company’s fourth offshore facility and reinforcing its Southeast Asia growth strategy.

- January 2025: PT Gajah Tunggal Tbk and Mitra Agung opened TireZone Mitra Agung Cibodas, extending premium retail coverage in Tangerang.

- October 2024: ZC Rubber produced its first all-steel radial tire at PT Matahari Tire Indonesia in Kendal Industrial Park, accelerating Indonesian localization.

- July 2024: PT Gajah Tunggal Tbk unveiled the Giti passenger-car line at GIIAS 2024 to broaden premium offerings beyond truck and bus radials.

Indonesia Tire Market Report Scope

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic / Airless |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks and Buses |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road (Construction, Mining, Agriculture) |

| OEM |

| Aftermarket (Replacement and Retread) |

| Below 15 inches |

| 15 - 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic / Airless | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks and Buses | |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road (Construction, Mining, Agriculture) | |

| By End User | OEM |

| Aftermarket (Replacement and Retread) | |

| By Rim Size | Below 15 inches |

| 15 - 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid and Fuel-Cell Vehicles |

Key Questions Answered in the Report

How large is the Indonesia tire market in 2025 and what is its growth rate to 2030?

The Indonesia tire market size stands at USD 4.18 billion in 2025 and is projected to climb to USD 5.46 billion by 2030 at a 5.49% CAGR.

Which vehicle category currently drives the greatest replacement demand?

Two-wheelers generate the highest share at 36.21% thanks to Indonesia’s motorcycle-centric mobility patterns and frequent replacement cycles.

What rim sizes are rising fastest in sales?

Tires above 20 inches will expand at a 7.81% CAGR as consumers favor larger wheels on premium SUVs and MPVs.

Which distribution channel captures the bulk of tire sales today?

The aftermarket holds 72.13% share because Indonesia’s large in-use vehicle fleet requires frequent replacement independent of new vehicle sales.

Page last updated on: