South Africa Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 1.72 Billion |

| Market Size (2030) | USD 2.38 Billion |

| Growth Rate (2025 - 2030) | 6.69% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Tire Market Analysis by Mordor Intelligence

The South African tire market size stands at USD 1.72 billion in 2025 and is projected to reach USD 2.38 billion by 2030, advancing at a 6.69% CAGR, underscoring healthy momentum in the country’s automotive supply chain. Passenger-car and commercial-vehicle radialization, infrastructure upgrades in freight corridors, and sustained fleet renewal cycles underpin demand despite margin pressures from raw-material volatility. Regulatory safeguards such as the May 2025 anti-dumping duties on Chinese tires shield local production, while rising electric-vehicle launches create a premium segment for low-rolling-resistance tires. Tire makers accelerate digital retail, including mobile fitment and e-commerce, to serve urban customers who expect same-day installation. Mining and construction projects continue to buoy off-the-road (OTR) volumes, ensuring that the South African tire market maintains balanced exposure across on-road and off-road applications.

Key Report Takeaways

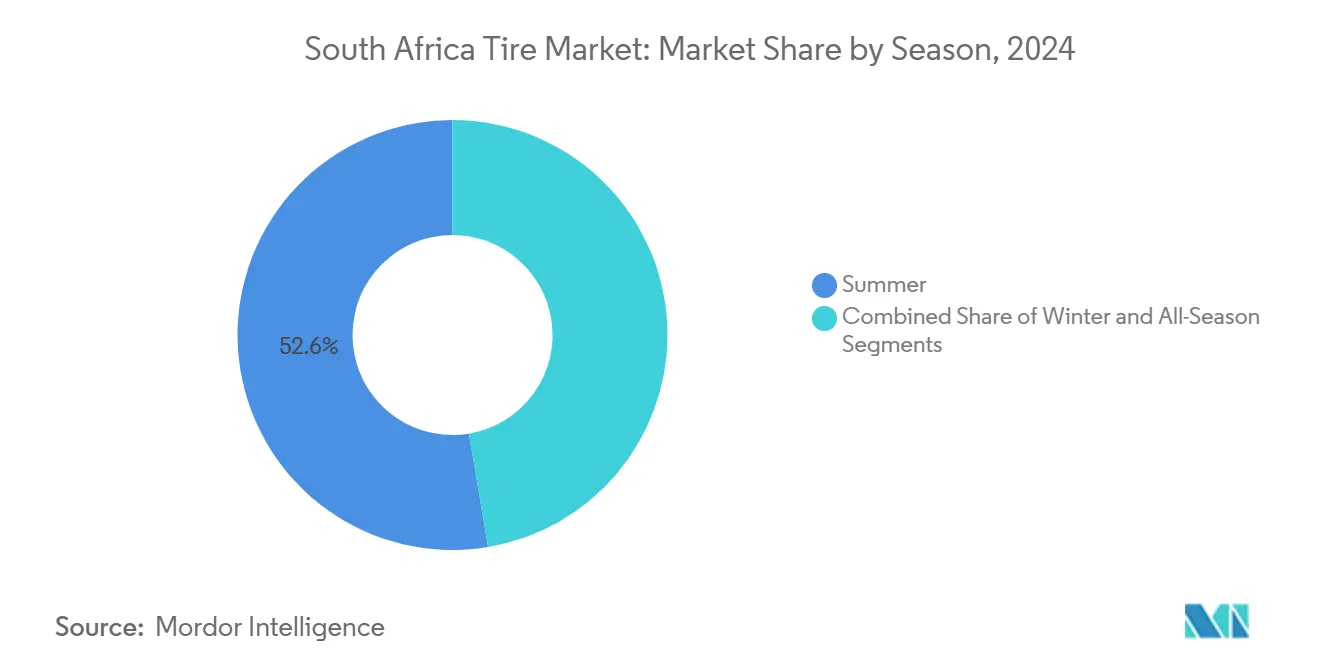

- By season, summer tires led with 52.64% revenue share of the South African tire market in 2024, while winter tires are forecasted to expand at a 7.81% CAGR through 2030.

- By tire design, radial technology captured 89.09% of the South African tire market share in 2024; non-pneumatic designs are projected to advance at a 12.15% CAGR to 2030.

- By vehicle type, passenger cars accounted for 44.54% of the South African tire market size in 2024, whereas SUV and crossover tires are growing at a 6.84% CAGR.

- By application, on-road use dominated with a 74.91% share of the South African tire market size in 2024, yet off-road demand is accelerating at a 7.33% CAGR.

- By end user, the aftermarket commanded 62.77% share of the South African tire market in 2024; retreading is set to rise at an 8.29% CAGR through 2030.

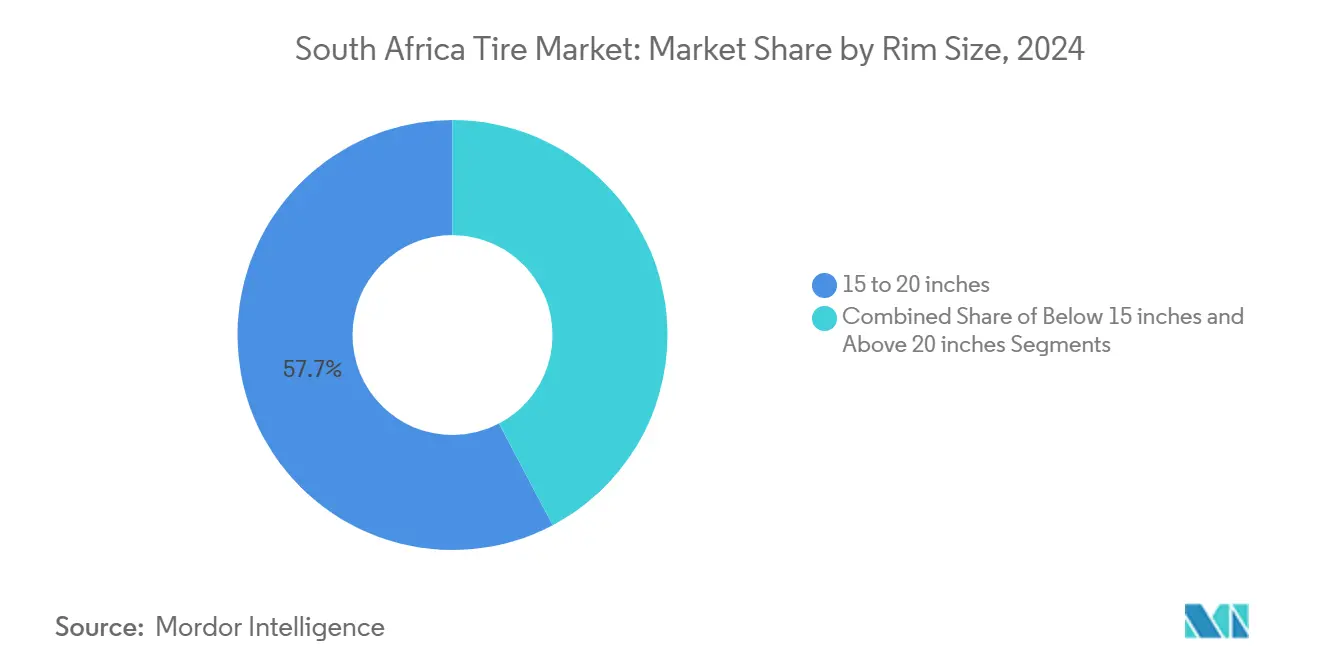

- By rim size, the 15–20 inch band held 57.71% of the South African tire market revenue in 2024, while the above 20 inch sizes are scaling at a 7.92% CAGR.

- By propulsion, internal-combustion vehicles represented 84.02% of total demand of the South African tire market in 2024; battery-electric vehicle tires are predicted to grow at an 11.39% CAGR.

South Africa Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Vehicle Parc | +1.5% | Gauteng, Western Cape, KwaZulu-Natal | Medium term (2-4 years) |

| Infrastructure and Logistics Expansion | +1.3% | Gauteng, Western Cape, Eastern Cape | Long term (≥ 4 years) |

| Radialization and Premiumization | +0.9% | Gauteng, Western Cape, Free State | Medium term (2-4 years) |

| OTR Demand | +0.7% | North West, Limpopo, Mpumalanga | Long term (≥ 4 years) |

| EV and Hybrid Model Launches | +0.5% | Gauteng, Western Cape | Long term (≥ 4 years) |

| Digitization of Tire Retail | +0.4% | Gauteng, Western Cape, KwaZulu-Natal | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Parc and Replacement Demand

Surging new-vehicle registrations expand the active fleet, shortening average replacement cycles and driving premium tire uptake. Fleet operators in Gauteng and Western Cape increasingly rely on predictive maintenance to cut unscheduled downtimes, ensuring consistent aftermarket pull-through. Higher kilometers traveled across revitalized freight corridors further elevate wear rates, bolstering volume growth in the South African tire market. Regulatory scrutiny by the South African Bureau of Standards compels adherence to safety thresholds, nudging consumers toward certified premium brands. Together, these factors sustain a dependable demand base that cushions manufacturers against macroeconomic swings.[1]“South Africa’s Strategic Adaptation to U.S. Tariffs: Advancing National Interests through Policy and Strategy,” Department of Trade, Industry and Competition, dtic.gov.za

Infrastructure and Logistics Expansion Fueling Commercial-Tire Uptake

Government-led port upgrades at Durban and Cape Town increase freight throughput, pushing heavy-duty fleets to expand and intensify tire replacement schedules. Construction tied to the National Development Plan fuels OTR demand for earthmoving equipment, with contractors specifying premium rubber to avoid costly downtime. Digital route-optimization across logistics firms trims tire wear yet raises vehicle utilization, setting a higher replacement baseline. Mining hauls from North West and Limpopo amplify demand for high-load, cut-resistant compounds. Collectively, these projects elevate commercial tire penetration and strengthen the growth trajectory of the South African tire market.

Radialization and Premiumization Across Fleets

Radial tires already hold near-ubiquity, yet incremental benefits, 8-12% fuel savings, and longer tread life, continue to sway mid-tier fleets. Financing schemes let small operators shift to premium radials without upfront strain, broadening addressable demand. Domestic producers capitalize on tariff-induced cost advantages over bias-ply imports, deepening radial penetration. Consumer education campaigns underscore safety gains, lifting radial adoption even in price-sensitive passenger categories. Policy alignment with the Department of Transport safety codes cements radial specifications in new-vehicle approvals, reinforcing long-term dominance.

Growth of Mining, Construction and Agriculture Equipment (OTR Demand)

Stable platinum and gold extraction sustains round-the-clock equipment use, making tire integrity a mission-critical cost center where premium brands prevail. Construction rebounds post-pandemic, triggering orders for puncture-proof compounds suited to rocky terrains. Large-scale farms in the Free State deploy higher-horsepower tractors, requiring broader, soil-compaction-friendly tire profiles. Limited local competition in specialized OTR segments permits superior margins, funding continuous R&D in tread pattern and casing durability. Compliance with stringent mine-safety protocols further entrenches established suppliers, augmenting the value pool of the South African tire market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-Cost Imports | -1.2% | Gauteng, Western Cape, KwaZulu-Natal | Short term (≤ 2 years) |

| Volatile Rubber and Oil Prices | -0.9% | National | Medium term (2-4 years) |

| Tire Recycling and EPR Regulations | -0.6% | Gauteng, Western Cape | Medium term (2-4 years) |

| Power-Grid Instability | -0.4% | Gauteng, KwaZulu-Natal | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge of Low-Cost Imports Intensifying Price Competition

Even after the May 2025 anti-dumping duties, certain overseas suppliers re-route shipments through third-country assembly centers, sustaining a 25–35% price edge over local budget offerings[2] “News Headlines,” International Trade Administration Commission of South Africa, itac.org.za. Price-sensitive buyers, especially in the replacement market, gravitate toward these alternatives, forcing domestic brands to trim margins. Inventory pile-ups during economic lulls exacerbate discounting, undermining profitability for small and mid-sized producers. Enforcement gaps at ports allow non-compliant products to leak into retail, challenging standardization efforts. The scenario compresses near-term earnings and forces cost-cutting across South African manufacturing lines.

Volatile Natural-Rubber and Oil Prices Squeezing Margins

Sharp input-cost swings constrain pricing power in a market where consumers resist frequent list-price revisions. Synthetic-rubber costs track crude-oil fluctuations, layering additional volatility. Medium-sized firms without sophisticated hedging tools face cash-flow strain during spikes, leading to curtailed production runs that disrupt supply reliability. Currency depreciation amplifies imported raw-material expenses, complicating long-range planning. Persistent volatility could deter capital investment in capacity upgrades, tempering growth in the South African tire market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: Summer Leadership with Winter Uptick

Summer tires captured 52.64% of the South African tire market share in 2024, underpinned by South Africa’s warm climate and high share of passenger-car travel. Seasonal demand remains especially pronounced in Gauteng’s commuter corridors, where summer compounds deliver optimal wet-grip and tread life. Winter tire sales are expanding at a 7.81% CAGR as fleet managers in high-altitude regions recognize traction and braking dividends during cold mornings. All-season products serve cost-conscious drivers seeking year-round utility without seasonal change-overs.

Fleet procurement data show that rotating between summer and winter sets can extend aggregate tire lifespan by 15% while lowering fuel consumption. Digital fleet-management dashboards quantify these savings, encouraging broader adoption. Retailers bundle rotation services with purchase contracts, further stimulating penetration. As consumer familiarity rises, winter tires are expected to account for a larger slice of the South African tire market by decade’s end.

By Tire Design: Radial Supremacy and Airless Emergence

Radial technology dominated the South African tire market in 2024, capturing 89.09% on the back of proven fuel-economy and ride-comfort gains. Local producers enjoy tariff protection against bias-ply imports, widening price parity, and reinforcing radial drift. Airless, non-pneumatic formats are projected to exhibit a 12.15% CAGR, driven by interest from materials-handling fleets and urban last-mile vehicles eyeing puncture elimination. Sumitomo Rubber South Africa’s Ladysmith plant increasingly dedicates R&D budgets to radial-casing refinements for rough asphalt conditions.

Cost remains a barrier to airless penetration, yet pilot deployments demonstrate lifecycle savings through zero blow-outs and reduced downtime. Regulatory safety approvals granted in 2024 bolster confidence, encouraging niche segments to trial the technology. Long-term, autonomous shuttles and delivery robots could unlock high-volume applications, opening a new growth frontier for the South African tire market.

By Vehicle Type: Passenger Base and SUV Momentum

Passenger cars generated 44.54% of the South African tire market's 2024 revenue, buoyed by Johannesburg’s commuter ecosystem and Pretoria’s government-employee fleets. The segment, SUVs and crossovers in particular, benefitting from lifestyle shifts toward higher-ground-clearance vehicles, outpaced overall market growth at a 6.84% CAGR. Light commercial vans underpin last-mile e-commerce logistics, maintaining steady demand. Heavy-truck tire volumes correlate with infrastructure spend and port throughput, providing cyclical upside linked to public-works budgets.

SUV tires typically command larger rim diameters, often above 18 inches, delivering higher unit revenue. Suppliers capitalize on this shift through premium-priced all-terrain SKUs. Fleet electrification trends create emerging demand for EV-specific tire designs optimized for electric vehicle characteristics, though adoption remains limited by South Africa's nascent EV infrastructure. Manufacturers also refine rolling-resistance coefficients for electric SUV applications, aiming to retain share as electrification progresses. This segmental diversification stabilizes aggregate earnings for companies serving the South African tire market.

By Application: On-Road Core with Off-Road Expansion

On-road categories comprised 74.91% of the South African tire market value in 2024, anchored by passenger sedans, city buses, and inter-provincial haulage trucks. Stringent highway safety checks drive steady replacement intervals. Off-road sales, growing at a 7.33% CAGR, benefit from steady mining capex and government road-building schemes that rely on earth-moving machinery. OTR tire manufacturers supply cut-resistant compounds and reinforced sidewalls tailored for abrasive ore-haul tracks.

Mining firms drive specialized off-road tire requirements, allocating up to 20% of equipment operating costs to tires, incentivizing premium procurement to reduce unplanned stoppages. Construction contractors increasingly adopt telematics to predict wear patterns, scheduling change-outs that minimize idle time. Both developments underpin a resilient demand stream, adding breadth to the South African tire market.

By End User: Aftermarket Dominance and Retread Acceleration

The aftermarket contributed 62.77% of the South African tire market share in 2024 since South Africa’s 12-million-unit vehicle parc demands constant replacement, and consumers value immediate availability over brand allegiance. National chains like Tiger Wheel & Tire stock multi-tier assortments, letting buyers trade up or down according to wallet and usage profile without leaving the store. Loyalty apps collect driving-behavior data and push rotation reminders, further tightening the aftermarket’s hold on drivers. Together, these innovations lock in a robust replenishment engine that powers the South African tire market share.

Retreading, moving at an 8.29% CAGR, resonates with freight firms chasing cost savings and ESG targets under mandatory extended-producer-responsibility rules. Advances in shearography inspection ensure casing integrity, cutting failure rates, and building confidence in remanufactured rubber. Government waste levies reward fleets that document multi-life casings, translating sustainability into cash-flow gains. Meanwhile, OEM volumes mirror macro auto-assembly trends—buoyant when production lines hum, muted during plant retooling phases. These three channels—aftermarket, retread, and OEM—create a portfolio effect that stabilizes overall revenue in the South African tire market.

By Rim Size: Mid-Range Strength and Large-Diameter Upswing

Rims sized 15–20 inches delivered 57.71% of 2024 revenue, mirroring the dominant footprint of compact sedans, hatchbacks, and one-ton pickups. This category offers suppliers high-volume mold utilization, enabling lean cost structures and competitive pricing that fend off grey-import rivals. Retailers keep deep inventory buffers because these sizes turn fastest and underpin service-level metrics promised in e-commerce portals. Promotions often pair mid-range tires with free rotation services, driving store traffic and ancillary sales of batteries and wiper blades. As a result, the mid-range diameter acts as both a bread-and-butter product and a customer-acquisition funnel.

Rim diameters above 20 inches climb at 7.92% CAGR, fueled by SUV and luxury-sedan sales that prize aesthetics and cornering stability. Each unit commands higher material inputs—about 2 kg more rubber—yet production still runs on the same curing presses, translating into outsized margins. Dealerships upsell chrome alloys and matching ultra-high-performance tires at vehicle delivery, bundling the cost into financing plans that diffuse price sensitivity. Lifestyle marketing on social media spotlights large-rim vehicles, reinforcing aspirational demand among younger buyers. This high-value tail lifts the blended average selling price and contributes incremental profit to the South African tire market size.

By Propulsion: ICE Dominance with EV Traction

Internal-combustion engines fueled 84.02% of the South African tire market share in 2024, mirroring the national vehicle fleet that still relies on diesel and gasoline amid limited charging infrastructure. Replacement cycles for ICE vehicles are well understood, letting distributors fine-tune stock to region-specific models and climate. Fuel-price volatility steers some operators toward low-rolling-resistance tires even for diesel fleets, hinting at a gradual convergence with EV-focused compound technology. Supply contracts with public-transport agencies lock in predictable volumes, offsetting fluctuations in retail walk-in traffic. Consequently, ICE remains the dependable baseline for the South African tire market.

Battery-electric tires, however, expand at an 11.39% CAGR under Automotive Masterplan 2035 incentives that offer tax deductions on EV manufacturing investment. Fleet pilots in last-mile delivery reveal 25% faster tread wear due to instant torque, prompting heavier-duty rubber and new tread patterns. Manufacturers collaborate with EV OEMs to co-develop foam-filled cavities that lower road noise and improve passenger comfort, absent engine masking. Tire makers position these specialized lines as premium products with connected-sensor options that feed range-prediction algorithms, carving out a growing profit pool. Hybrids and fuel-cell vehicles trail but serve as technology bridges, ensuring suppliers refine future-ready compounds without abandoning today’s core ICE customer.

Geography Analysis

Gauteng anchors the South African tire market, fueled by Johannesburg–Pretoria commuter flows, a dense logistics hub, and the country’s largest passenger-car base. Continuous freight along the N1 and N3 highways drives robust heavy-truck tire turnover, while fintech-enabled retail chains offer buy-now-pay-later plans that spur replacement purchases. Western Cape ranks second, with Cape Town’s port throughput and wine-industry distribution underpinning both passenger and commercial tire demand. Agricultural activities in the province bolster specialized tractor-tire sales, and tourism traffic elevates SUV tire volumes during holiday seasons.

KwaZulu-Natal benefits from Durban’s role as Africa’s busiest container terminal, sustaining OTR and truck-tire consumption. Local OEM hubs support steady OEM fitment volumes, while regional ride-hailing fleets maintain high passenger-car replacement rates. Mining provinces, North West, Limpopo, Mpumalanga, generate steady OTR sales aligned with platinum and coal output. Fleet operators in these areas adopt predictive analytics to pre-order tire lots ahead of rainy seasons, avoiding supply disruptions.

Secondary regions, including Eastern Cape, experience localized spikes thanks to OEM factories that generate OEM and worker-commuter demand. Free State’s farm economy creates predictable seasonal uplift in agricultural tire orders around planting and harvest. Digital marketplaces extend retailer reach into rural districts, though last-mile logistics challenges persist. Collectively, geographic diversity balances the growth profile of the South African tire market.

Competitive Landscape

The South African tire market features moderate concentration, with the top five brands controlling a majority share in 2024. Bridgestone South Africa leads, leveraging a nationwide dealer network and OEM linkages. Continental Tire SA differentiates through advanced silica compounds that improve wet grip. Goodyear South Africa focuses on fuel-efficient truck-tire lines launched in September 2025. Tariff barriers and local sourcing mandates protect incumbents, yet agile newcomers leverage e-commerce to bypass legacy wholesaling layers.

Firms ramp up investments in predictive-maintenance telematics that feed tire-condition data to fleet dashboards, fostering sticky service contracts. Local manufacturing plants grapple with load-shedding; installing solar microgrids and energy-storage systems mitigates downtime and enhances ESG scores. Partnership models emerge between tire makers and recycling startups to meet stricter EPR quotas, turning waste liabilities into brand-enhancing circular-economy narratives.

Digital experience is now a battleground: mobile fitment vans equipped with hydraulic lifts deliver on-site service within two hours of purchase, raising customer satisfaction benchmarks. Brands pilot subscription-based tire-as-a-service bundles covering rotation, balancing, and condition monitoring for a monthly fee. Anti-dumping duties reshape low-price tiers, steering cost-sensitive buyers toward domestically assembled alternatives and stabilizing margins across the South African tire market

South Africa Tire Industry Leaders

Bridgestone South Africa (Pty) Ltd

Continental Tyre South Africa (Pty) Ltd

Goodyear South Africa (Pty) Ltd

Sumitomo Rubber South Africa

Hankook Tire SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Goodyear introduced the KMAX GEN-3 truck-tire lineup, claiming up to 13% lower rolling resistance and higher mileage.

- November 2024: BFGoodrich rolled out the KO3 all-terrain tire tailored for South African bakkies and SUVs.

South Africa Tire Market Report Scope

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic / Airless |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks and Buses |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road (Construction, Mining, Agriculture) |

| OEM |

| Aftermarket (Replacement and Retread) |

| Below 15 inches |

| 15 to 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic / Airless | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks and Buses | |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road (Construction, Mining, Agriculture) | |

| By End User | OEM |

| Aftermarket (Replacement and Retread) | |

| By Rim Size | Below 15 inches |

| 15 to 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid and Fuel-Cell Vehicles |

Key Questions Answered in the Report

How large is the South African tire market in 2025?

The South African tire market size is USD 1.72 billion in 2025.

What is the projected CAGR for tire demand in South Africa to 2030?

Demand is forecast to rise at a 6.69% CAGR through 2030.

Which tire segment is growing fastest by design?

Non-pneumatic airless tires are expanding at a 12.15% CAGR.

Why are winter tires gaining attention in South Africa?

Higher-altitude regions face colder mornings, pushing winter tire sales at a 7.81% CAGR for safer traction.

How do anti-dumping duties impact local manufacturers?

Duties reduce low-cost import pressure, letting domestic producers protect margins and sustain investment.

What drives the surge in retread adoption?

Fleet operators pursue cost savings and compliance with waste-reduction mandates, spurring an 8.29% CAGR in retreading.

Page last updated on: