Malaysia Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

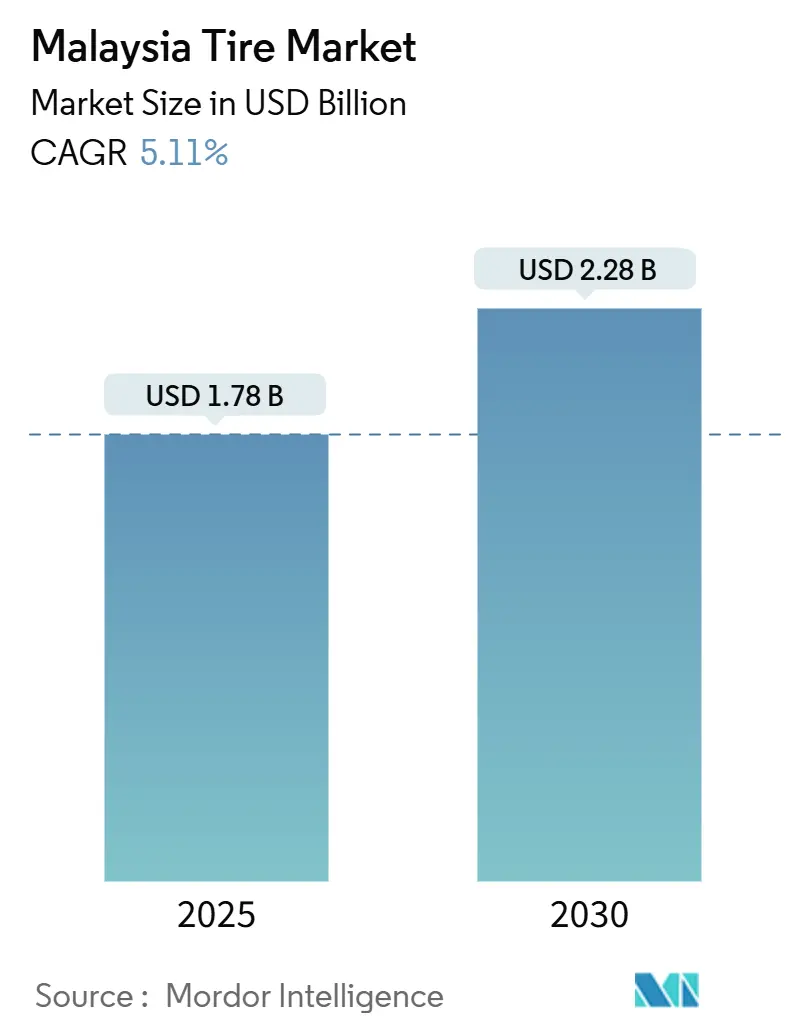

| Market Size (2025) | USD 1.78 Billion |

| Market Size (2030) | USD 2.28 Billion |

| Growth Rate (2025 - 2030) | 5.11% CAGR |

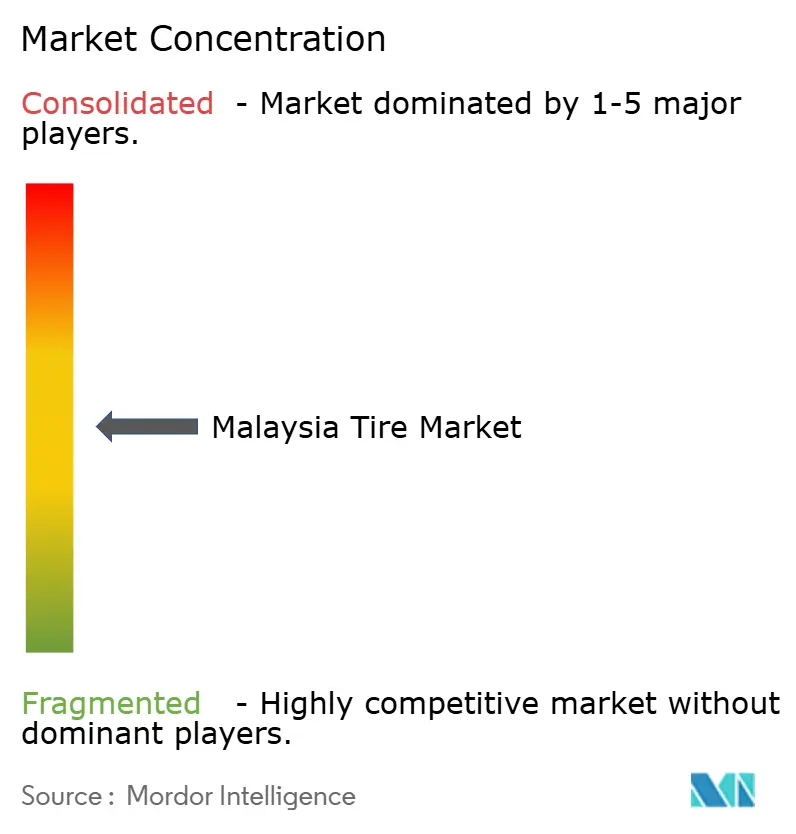

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Tire Market Analysis by Mordor Intelligence

The Malaysian Tire Market size is estimated at USD 1.78 billion in 2025, and is expected to reach USD 2.28 billion by 2030, at a CAGR of 5.11% during the forecast period (2025-2030). Domestic capacity reductions by Goodyear and Continental have tightened supply and increased pricing leverage for the remaining producers, while expanded output from plants such as Toyo’s Taiping facility keeps overall availability stable. Rapid growth in the national vehicle parc, especially within SUVs, crossovers, and an extensive motorcycle base, underpins steady replacement demand. Input-cost advantages created by weaker natural rubber prices and intensified government infrastructure spending reinforce profitability prospects for local manufacturers. At the same time, digital retail platforms and multi-brand service chains are reshaping distribution economics and customer reach.

Key Report Takeaways

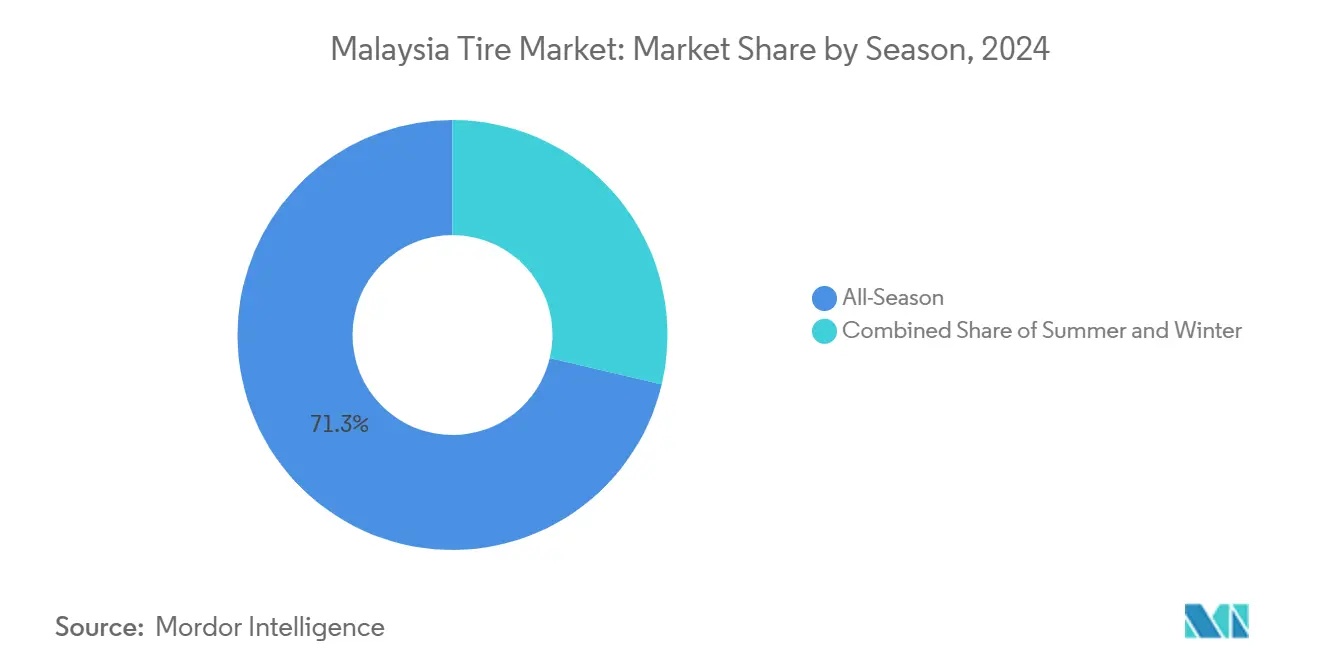

- By season, all-season tires captured 71.28% of the Malaysian market share in 2024; summer tires are forecast to expand at a 5.13% CAGR through 2030.

- By tire design, radial products accounted for 87.27% of the Malaysian tire market size in 2024; non-pneumatic airless formats are projected to grow at a 5.25% CAGR to 2030.

- By vehicle type, passenger cars held 54.52% of Malaysia's tire market share in 2024, as well as advancing at a 5.17% CAGR.

- By application, on-road fitments commanded an 82.36% share of the Malaysian tire market size in 2024; off-road uses are set to increase at a 5.16% CAGR through 2030.

- By end user, the aftermarket represented 67.73% of Malaysia's tire market share in 2024 and is growing at a 5.22% CAGR, outpacing OEM channels.

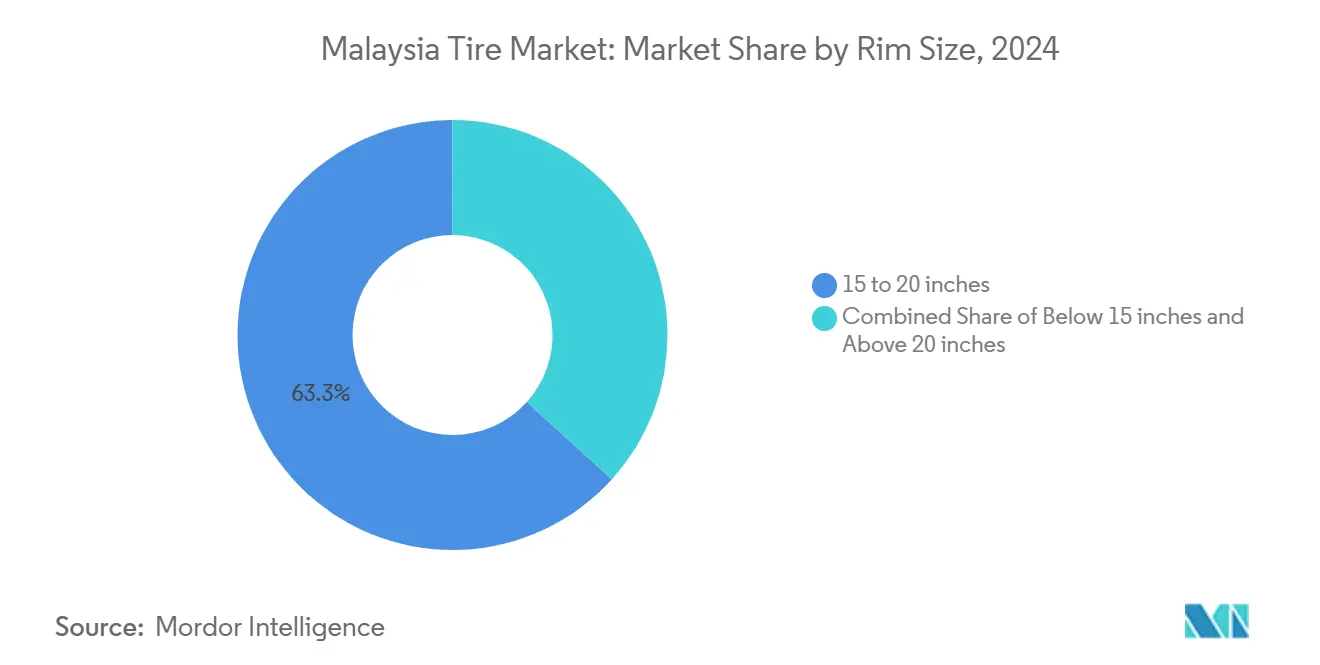

- By rim size, the 15–20-inch segment commanded 63.25% of the Malaysian tire market share in 2024, while above-20-inch rims are projected to expand at a 5.17% CAGR through 2030.

- By propulsion, internal-combustion cars dominate with 88.81% share, yet battery-electric vehicles are the fastest-rising sub-segment with a 5.21% CAGR foreseen to 2030.

Malaysia Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Vehicle PARC & High Car | +1.2% | National, concentrated in Klang Valley and Penang | Medium term (2-4 years) |

| Government Infrastructure Spend | +0.8% | National, with early gains in East Coast, Penang | Long term (≥ 4 years) |

| OEM Production Shift | +0.7% | National, centered in Perak and Selangor production hubs | Short term (≤ 2 years) |

| Capacity Freed By Overseas Expansions | +0.6% | National, with spillover to ASEAN markets | Medium term (2-4 years) |

| Local EV-Tire Testing Labs | +0.4% | National, with concentration in technology corridors | Long term (≥ 4 years) |

| Digitalised Multi-Brand Distribution/Retail Expansion | +0.3% | National, with urban concentration initially | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle PARC & High Car + Motorcycle Ownership

Malaysia’s combined fleet of motorcycles and a rising passenger-car base fuels predictable replacement cycles every 12–18 months for two-wheelers and 3–5 years for cars[1]“Vehicle Sales Data 2024–2025,” Malaysian Automotive Association, malaysianautomotive.org.my . The total volume of the national vehicle industry moderated to an estimated around eight lakh units in 2025, yet replacement demand remains insulated from new-sales swings. Higher motorcycle prices after open-market-value formula revisions are extending ownership durations, which intensifies tire replacement frequency. These patterns reinforce the aftermarket’s two-thirds dominance and support steady cash flows for retailers and service chains across the Malaysian tire market.

Government Infrastructure Spend Spurring CV Tire Demand

Flagship projects such as the RM 55 billion East Coast Rail Link, scheduled for operations in January 2027, stimulate heavy-duty tire demand during construction and logistics phases[2]“East Coast Rail Link Progress Update,” Ministry of Transport Malaysia, mot.gov.my. Concurrent RM 10 billion Light Rail Transit work in Penang, where rubber-tired train technologies are under review, broadens specialized tire use cases. Retreaded tires, priced roughly three-fifths below new units, already cover four-fifths of Malaysia’s commercial vehicle segment and stand to benefit from cost-focused fleet operators.

OEM Production Shift Toward SUVs & Crossovers

Model lineups centered on SUVs like the Proton X70 are changing rim size and compound requirements. Larger diameters (17–22 inches) and higher load indexes raise average selling prices and enhance manufacturers' value per unit. Continental’s UltraContact UX7 launch for Malaysia’s SUV sizes indicates the supplier's focus on this pivot. Proton’s move to its 1,280-acre Tanjung Malim hub by 2027 strengthens local OEM tire-sourcing opportunities, while 35 newly imported Chinese models in 2024 add aftermarket demand for specialty fitments.

Capacity Freed By Overseas Expansions

Toyo Tire’s Phase II boost lifted its Taiping plant to a huge annual capacity, serving Southeast Asia, Europe, Japan, and North America. Economies of scale lower unit costs and release supply for the Malaysian tire market, particularly in large-diameter SUV and pickup categories where Toyo claims technical strength. Conversely, shutdowns of unprofitable lines—including Toyo’s Silverstone plant in 2021—show how selective investment steers market positioning. Overall, imported capacity offsets domestic closures and keeps competition fluid.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural-Rubber & Input-Cost Volatility | -0.9% | National, with upstream supply chain exposure | Short term (≤ 2 years) |

| Influx Of Low-Priced Imports | -0.7% | National, concentrated in commercial vehicle segments | Medium term (2-4 years) |

| Local Plant Closures | -0.5% | National, with concentrated impact in Selangor and surrounding regions | Short term (≤ 2 years) |

| Slow Roll-Out Of Advanced Safety | -0.3% | National, with delayed implementation across regulatory framework | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Natural-Rubber & Input-Cost Volatility

Farm-gate support schemes create artificial price floors, while weather-driven supply shocks from smallholder-dominated tapping push volatility into tire makers’ margins. Currency swings amplify uncertainty because a stronger ringgit trims export competitiveness while a weaker currency inflates synthetic-rubber and additive imports. Imminent extended-producer-responsibility regulations will add compliance costs but may open new revenue through recycled tire materials.

Influx Of Low-Priced Imports & Retreads

Retreaded and used-tire imports grew exponentially in 2023, with Thailand supplying two-fifths of shipments. Prices three-fifths below new units squeeze margins for local producers and heighten quality-control concerns, evidenced by tires ranking as the second-largest cause of heavy-vehicle failures at inspection centers. The spread of “tire rental” practices, where compliant treads are swapped only for inspections, distorts legitimate demand. Despite MS 224:2019 and ECE R108/109 standards, enforcement gaps keep inferior products circulating.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: All-Season Dominance Drives Market Stability

All-season tires accounted for 71.28% of the Malaysia tire market share in 2024, reflecting the country’s tropical climate that negates seasonal changeovers. Consistent year-round demand enables producers to optimize manufacturing runs and distributors to hold streamlined inventories. Summer tires, though smaller, are set to post a 5.13% CAGR through 2030 as motorsports enthusiasm and performance-oriented buyers increase. The regulatory framework under NSC 12/TC 11 assures safety uniformity across all seasonal offerings, cementing consumer trust.

Consumer buying patterns prioritize convenience and total-cost-of-ownership over specialized performance traits. Consequently, all-season compounds remain the dominant revenue stream within the Malaysian tire market. Manufacturers emphasize wet-grip and heat-dissipation features tailored to high humidity and temperature conditions, maintaining relevance across diverse urban and rural driving environments.

By Tire Design: Radial Technology Maintains Supremacy

Radial construction captured 87.27% of the Malaysia tire market share in 2024, driven by superior fuel economy and heat resistance. Large-scale production secures cost advantages, discouraging bias-ply substitution beyond niche agricultural and off-road uses. Airless designs, led by Michelin’s Uptis demonstrations, are projected to rise 5.25% annually. Interest from fleet managers centers on puncture elimination and reduced downtime.

Research by Universiti Sains Malaysia on self-healing natural rubber compounds illustrates the country's capacity to push innovation and potentially accelerate airless adoption. As commercial delivery volumes grow alongside e-commerce, operators will increasingly weigh the operational savings versus up-front premiums of non-pneumatic options within the Malaysian tire market.

By Vehicle Type: Passenger Cars Lead Amid SUV Transition

Passenger cars held 54.52% of the Malaysia tire market share in 2024 and are forecast to grow at a 5.17% CAGR through 2030, buoyed by middle-class expansion and sustained affordability of A-segment models. Yet SUV and crossover production is reshaping sizing demands, lifting average rim diameters and unit values. Light commercial vehicles also benefit from last-mile delivery growth, whereas heavy-duty trucks gain traction from infrastructure projects.

Malaysia’s vast two-wheeler fleet, which replaces tires every 12–18 months, provides a stable aftermarket revenue engine. Meanwhile, electric-vehicle uptake, still at 2.5% of new registrations, is creating a specialized sub-segment that needs low-rolling-resistance, high-load tires. Suppliers adept at serving mature ICE fleets and emerging EV needs will capture incremental value as the Malaysian tire market evolves.

By Application: On-Road Applications Dominate Usage Patterns

In 2024, on-road tires represented 82.36% of the Malaysian tire market, matching the country’s extensive expressway network and urban commuting habits. Design optimization focuses on tread pattern noise reduction and wet-grip capabilities for monsoon conditions. Off-road demand is expanding at a 5.16% CAGR, propelled by palm-oil plantations, mining, and construction.

Distribution diverges along application lines: mass-market retailers stock primarily on-road SKUs, while specialist dealers manage off-road inventories requiring higher technical support. Certification by SIRIM QAS ensures both categories meet stringent safety standards, reinforcing confidence across purchase channels.

By End User: Aftermarket Channels Capture Replacement Demand

Aftermarket channels accounted for 67.73% of Malaysia's tire market share in 2024 and are charting at a 5.22% CAGR, reflecting the mature vehicle fleet’s steady replacement rhythm. Independent retailers, service centers, and digital platforms exploit this recurring demand by offering rapid service and multi-brand choice. OEM fitments remain necessary for volume consistency, especially as local assembly lines pivot to larger SUVs requiring specific homologated tires.

Digital transformation equips retailers with data analytics to refine pricing and inventory. Platforms like Klinikar.com illustrate how transparent cost structures and home-installation services can differentiate offerings in a crowded field. For manufacturers, balancing OEM relationships and an expanding, tech-enabled aftermarket will be key to defending share in the Malaysian tire market.

By Rim Size: Larger Diameters Reflect Premium Trends

Rim sizes between 15 and 20 inches held 63.25% of Malaysia's tire market share in 2024 by marrying affordability with comfort. The below 15-inch products serve price-sensitive drivers of compact cars and motorcycles. Above-20-inch tires are poised for the fastest 5.17% CAGR through 2030, mirroring higher disposable incomes and aspirational styling preferences.

Larger rims require low-profile constructions that require advanced manufacturing controls and higher-grade materials, pushing average selling prices. Suppliers that deliver performance and cost discipline will gain an advantage as style-conscious buyers widen the premium tier within the Malaysian tire market.

By Propulsion: ICE Dominance with EV Emergence

Internal-combustion vehicles retained 88.81% of the Malaysian tire market in 2024, ensuring ongoing demand for conventional compounds. Battery-electric cars, though still niche, will grow 5.21% annually as incentives and charging infrastructure accelerate adoption. Tires for EVs must combine low rolling resistance, enhanced load capacity, and reduced noise levels, pressuring suppliers to develop specialized SKUs.

Hybrid and fuel-cell vehicles occupy a middle ground, benefiting from government policy extensions encouraging lower-emission technologies. Regulation by the Ministry of Transport and JPJ mandates rigorous safety and performance validation for all propulsion-specific tires, reinforcing quality baselines across the Malaysian tire market.

Geography Analysis

Malaysia’s tire sector capitalizes on its proximity to ASEAN supply chains. Domestic plants, most notably Toyo’s Taiping site, export to Asia, Europe, and North America. Despite Goodyear and Continental closures, retained capacity remains significant.

Malaysia sits between Thailand’s large-scale production and Indonesia’s expansive domestic consumption. Thai retread imports valued highly in 2023 highlight cost-driven rivalry, prompting Malaysia to focus on higher-value segments such as airless and self-healing technologies incubated at Universiti Sains Malaysia. Government goals to rank among the global top-25 for innovation and secure two-fifths of knowledge-intensive employment further encourage R&D-heavy investments.

Cross-border deals such as EG Industries’ stake in Thailand’s ND Rubber illustrate Malaysia’s role as a regional financial hub, facilitating tire-industry consolidation and technology transfer. Participation in Belt-and-Road infrastructure links, including the East Coast Rail Link, extends market access for Chinese tire makers while unlocking logistics collabs. These dynamics underpin a resilient and globally connected Malaysia tire market.

Competitive Landscape

Global suppliers retain strong positions despite local capacity consolidation. Goodyear’s Shah Alam and Continental’s pending Alor Setar shutdowns reduced headcount but opened share opportunities for Bridgestone, Michelin, and Toyo. Michelin’s Uptis airless demos and Continental’s UltraContact UX7 SUV launch showcase technology-led differentiation in the Malaysian tire market.

Digital platforms are redefining distribution economics. Klinikar.com leverages nationwide mobile fitment, whereas multi-brand chains like B-Quik illustrate scalable storefront networks. These formats pressure traditional dealers on pricing transparency and service convenience.

Regulatory harmonization via NSC 12/TC 11 ensures safety standards and levels the playing field for incumbents and new entrants. Local retreaders, meeting MS 224:2019 rules, offer three-fifths cost savings that appeal to fleet operators. Future success will hinge on technology alliances with OEMs to cater to larger rims, EV-specific compounds, and premium SUV segments.

Malaysia Tire Industry Leaders

Continental Tyre PJ Malaysia Sdn Bhd

Goodyear Malaysia Berhad

Bridgestone Tyre Sales (Malaysia) Sdn Bhd

Michelin Malaysia Sdn Bhd

Yokohama Tyre Sales Malaysia Sdn Bhd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: In Malaysia, Continental unveiled its UltraContact UX7 tire range, tailored for SUVs and designed to deliver enhanced performance, safety, and durability. The range is available in sizes from 15 to 22 inches, catering to a wide variety of SUV models.

- January 2025: Ramssol launched Rider Gate, marking the debut of an online marketplace exclusively for used motorbikes. This platform offers comprehensive services, including motorbike inspections and warranty options, aiming to provide a seamless and reliable experience for buyers and sellers.

- October 2024: EG Industries acquired 24.08% of Thai motorcycle-tire maker ND Rubber for RM 26.05 million, highlighting cross-border consolidation.

Malaysia Tire Market Report Scope

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-Pneumatic / Airless |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks & Buses |

| Off-the-Road & Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road |

| OEM |

| Aftermarket |

| Below 15 inches |

| 15 – 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid & Fuel-Cell Vehicles |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-Pneumatic / Airless | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks & Buses | |

| Off-the-Road & Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road | |

| By End User | OEM |

| Aftermarket | |

| By Rim Size | Below 15 inches |

| 15 – 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid & Fuel-Cell Vehicles |

Key Questions Answered in the Report

How large is the Malaysian tire market 2025, and what is its growth trajectory?

The Malaysian tire market was USD 1.78 billion in 2025 and is projected to expand to USD 2.28 billion by 2030 at a 5.11% CAGR.

Which tire segment commands the highest market share in Malaysia?

Due to the country's tropical climate, all-season tires hold the top spot with a 71.28% share of 2024 revenue.

Why are aftermarket channels more prominent than OEM channels in Malaysia?

A mature vehicle parc and replacement cycles every 12–18 months for motorcycles and 3–5 years for cars give the aftermarket a 67.73% share.

What impact do infrastructure projects have on tire demand?

Projects like the East Coast Rail Link raise heavy-duty construction and logistics tire demand, especially for retreads.

How is the shift toward SUVs affecting tire specifications?

Larger rims (above 20 inches) and performance compounds are gaining popularity, supporting a 5.17% CAGR in that rim category through 2030.

What are the main challenges facing local tire manufacturers?

Volatile natural-rubber prices and an influx of low-priced retread imports tighten margins and intensify competitive pressure.

Page last updated on: