Africa Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

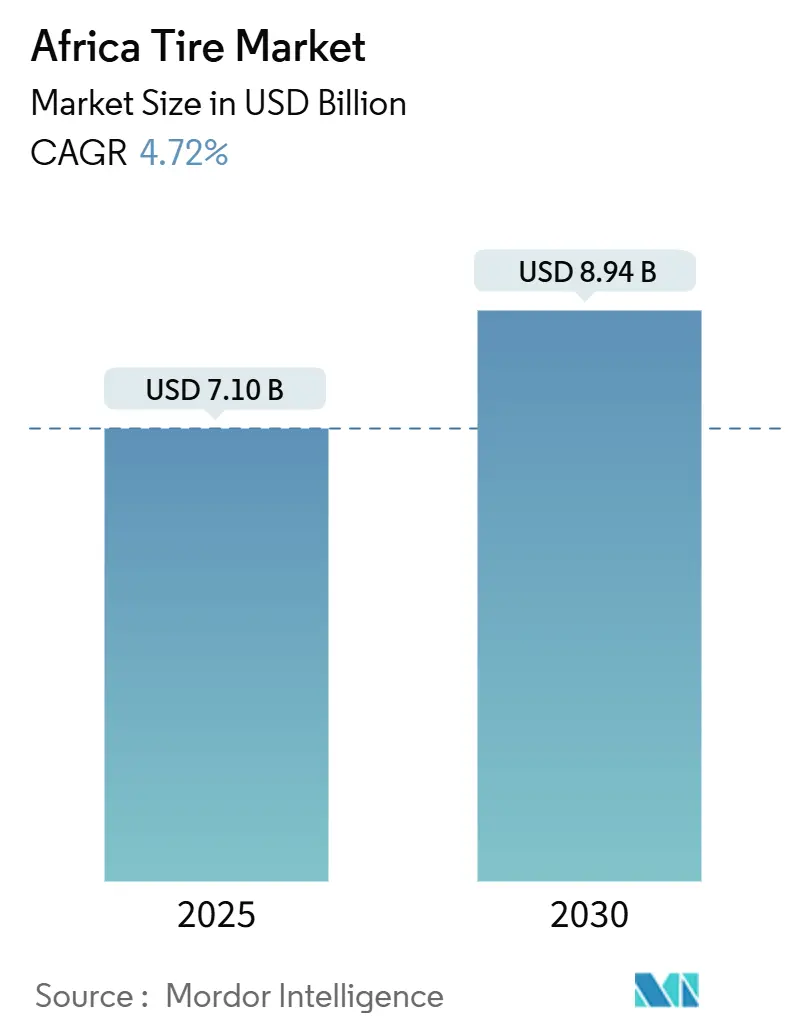

| Market Size (2025) | USD 7.10 Billion |

| Market Size (2030) | USD 8.94 Billion |

| Growth Rate (2025 - 2030) | 4.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Tire Market Analysis by Mordor Intelligence

The African tire market size is valued at USD 7.10 billion in 2025 and is projected to reach USD 8.94 billion by 2030, reflecting a 4.72% CAGR over the period. This moderate expansion hides a deeper realignment driven by infrastructure modernization, the African Continental Free Trade Agreement’s transport-corridor build-out, and the price-led advance of Chinese manufacturers. Chinese brands are securing footholds through localized plants and aggressive pricing, steadily displacing European suppliers. Rapid motorization in resource-rich economies is broadening replacement demand, while digital fleet-management tools are steering commercial fleets toward premium radial products. Currency volatility and regulatory limits on used-tire imports are simultaneously nurturing local manufacturing ambitions in Nigeria, Egypt, and Kenya, signaling fresh opportunities for players who can combine cost efficiency with compliance strength.

Key Report Takeaways

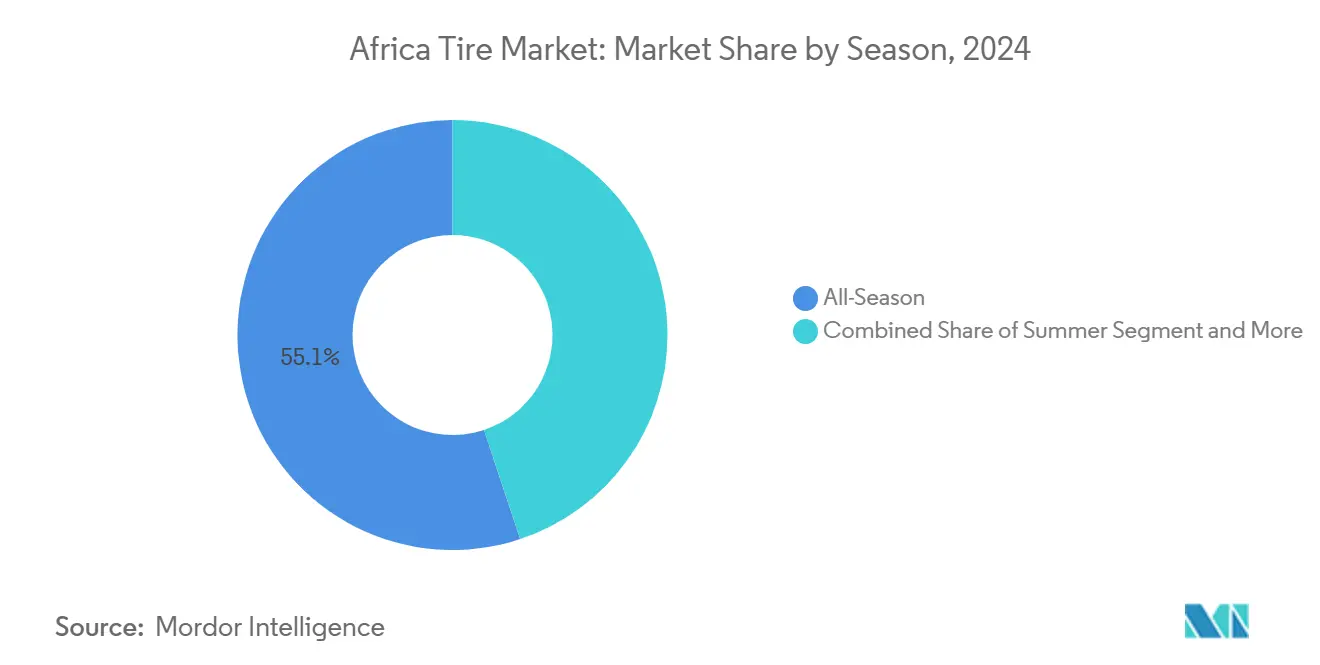

- By season, all-season lines captured 55.13% of the African tire market share in 2024; summer designs registered the fastest 5.64% CAGR through 2030.

- By tire design, radial construction commanded 91.25% share of the African tire market size in 2024; non-pneumatic airless formats are advancing at a 6.71% CAGR to 2030.

- By vehicle type, passenger cars commanded a 39.44% share of the African tire market size in 2024, and will advance at a 4.97% CAGR to 2030.

- By application, on-road commanded a 73.15% share of the African tire market size in 2024, and will continue to expand at a 5.15% CAGR to 2030.

- By end user, the aftermarket held 78.66% of the African tire market size in 2024, while OEM demand records a 6.04% CAGR through 2030.

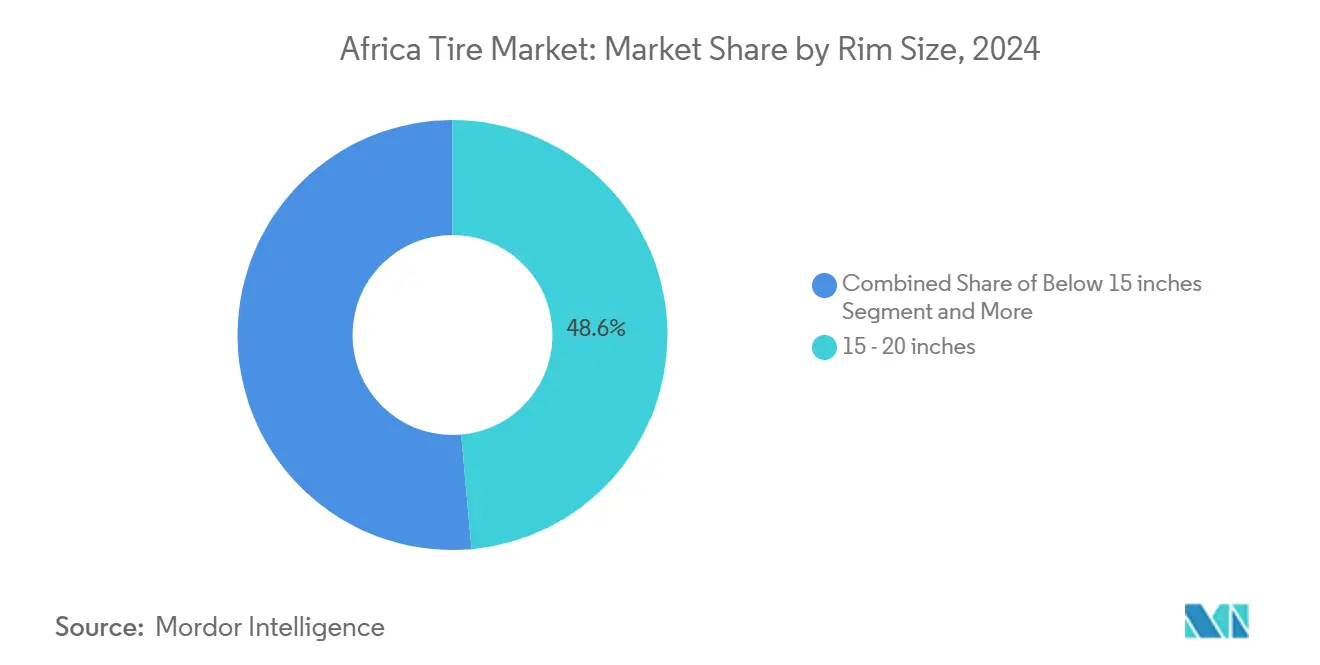

- By rim size, tires of 15-20 inches held 48.55% of the African tire market size in 2024, while the above 20 inches segment is projected to record a 5.87% CAGR through 2030.

- By propulsion, internal-combustion vehicles dominated with 90.24% of the African tire market size in 2024, while battery-electric vehicles' demand will grow at a 9.49% CAGR through 2030.

- By country, Algeria led with 26.75% of the African tire market share in 2024; the Democratic Republic of Congo posts the strongest 6.21% CAGR to 2030.

Africa Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Vehicle Parc and Motorization | +1.2% | Nigeria, South Africa, Algeria | Medium term (2-4 years) |

| Expansion of Chinese Tire-Maker | +1.1% | Morocco, Kenya, Nigeria, Egypt | Medium term (2-4 years) |

| AfCFTA Road-Infrastructure Build-Out | +0.9% | Continental, West Africa focus | Long term (≥ 4 years) |

| Demand for Affordable Replacement Tires | +0.8% | Nigeria, Kenya, Tanzania, Ghana | Short term (≤ 2 years) |

| Government Incentives for Local Capacity | +0.4% | Nigeria, Egypt, South Africa | Long term (≥ 4 years) |

| Digital Fleet-Management Adoption | +0.3% | South Africa, DRC, Ghana, Botswana | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Vehicle Parc and Motorization Rate Across Africa

Nigeria imported automobiles valued at NGN 1.47 trillion in 2023, signaling a gap that replacement tire suppliers are rushing to fill [1]“Foreign Trade Report Q4 2024,” National Bureau of Statistics Nigeria, nigerianstat.gov.ng. Rising incomes in oil-exporting states such as Algeria and Angola have lifted passenger-car ownership, spawning robust demand for budget and mid-tier tires. Fleet growth in ride-hailing and informal taxi services widens the daily replacement pool, while two-wheeler penetration in congested cities multiplies small-rim volumes. Seasonality is becoming less pronounced as urban mobility matures, keeping warehouses stocked year-round. Distributors with agile inventory policies gain an edge amid these fluctuations.

Expansion of Chinese Tire Makers’ Distribution Networks (Price Competitiveness)

Qingdao Sentury Tire Co., Ltd., Moroccan facility, and Linglong’s Kenya plant illustrate a strategic pivot from export-only to regional manufacture, cutting shipping costs and mitigating currency-risk exposure. Local production grants duty relief under regional trade agreements, making Chinese offerings cheaper than European lines. Once established, these factories can feed adjacent markets such as Senegal or Uganda within days, compressing lead times and enabling customized tread patterns for local road conditions.

Rapid Road-Infrastructure Development Programs (e.g., AfCFTA Corridors)

Projects such as the Abidjan–Lagos Highway unlock long-haul freight lanes requiring durable truck and bus radials [2]“AfCFTA Corridor Projects,” United Nations Economic Commission for Africa, uneca.org. Better pavement shifts preference from bias toward fuel-efficient radials, increasing price points. Construction equipment running on-site consumes extra off-road tires, enlarging heavy-duty niches. Improved connectivity also shortens delivery lead times, enabling hub-and-spoke warehousing models. Suppliers capable of field-service support along these corridors gain retention and upsell opportunities.

Growing Demand for Affordable Replacement Tires Through Informal Channels

In Nigeria, informal dealerships account for a major share of retail turnover, favoring brands that can supply smaller batches and offer cash-friendly terms. Chinese manufacturers leverage cost leadership and flexible packaging to meet this requirement, often bypassing formal importers. Rural penetration depends on motorbike and minibus operators whose purchase cycles are short yet volume-intensive. Quality perception remains secondary to price sensitivity, but recurring safety campaigns could gradually elevate standards, rewarding compliant producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency Depreciation and Import-Duty | –0.9% | Nigeria, Egypt, Ghana, Kenya | Short term (≤ 2 years) |

| Volatile Natural-Rubber and Synthetic Prices | –0.7% | Import-dependent states | Short term (≤ 2 years) |

| Fragmented Rubber Supply Chain | –0.4% | West and Central Africa | Long term (≥ 4 years) |

| Regulatory Clamp-Down on Imports | –0.3% | Kenya, South Africa, Nigeria | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency Depreciation and Import-Duty Fluctuations

The Nigerian naira and Egyptian pound have each lost more than 50% of value since 2024, inflating landed tire costs and curbing consumer purchasing power [3]“Regional Economic Outlook Sub-Saharan Africa,” International Monetary Fund, imf.org. Distributors must hold higher working capital just to maintain stock, adding financing strain. In response, several importers are committing to partial local assembly, signaling a gradual but irreversible supply-chain reconfiguration.

Volatile Natural-Rubber and Synthetic-Rubber Prices

Global rubber shortages have pushed input costs to decade highs, squeezing African producers that rely on overseas supply despite Côte d’Ivoire’s rising latex exports. Price spikes create budgeting headaches for budget-focused distributors, forcing either margin erosion or retail hikes that dampen demand. Hedging tools are scarce in emerging markets, leaving mid-tier players especially vulnerable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: Growing Summer-Tire Adoption in Northern Markets

All-season products still dominate the African tire market, with 55.13% market share, yet Algerian and Moroccan fleet managers now specify heat-resistant compounds to withstand desert highways. Suppliers calibrated to temperature extremes command premiums that offset higher rubber-mix costs. Summer tires are projected to expand at a 5.64% CAGR, outpacing the broader African tire market.

Elsewhere, tropical climates prefer flexible all-season rubbers that withstand intermittent rainfall. Multinational distributors, therefore, stock dual assortments: high-silica summer lines for the Maghreb and multi-purpose treads for sub-Saharan roads. Seasonal segmentation thus mirrors climatic zones more than economic tiers, rewarding companies with regionalized R&D.

By Tire Design: Radial Stronghold Faces Airless Experiments

Radials generated 91.25% of the African tire market size in 2024, a testament to their lower rolling resistance and longer tread life. Mining conglomerates in South Africa and the DRC are, however, piloting non-pneumatic/airless formats growing at 6.71% through 2030. These airless models eliminate puncture downtime, a key cost factor where equipment rents significantly exceed per hour.

Due to established service networks and retreading infrastructure, mainstream passenger and truck operators remain committed to radials. Still, OEM partnerships for quarry trucks indicate airless technology could spill into other utility vehicles once economies of scale improve. Players investing now in polymer-link architectures may capture early adopters and thought-leadership prestige.

By Vehicle Type: Passenger Cars Dominate, but Commercial Fleets Accelerate

Passenger-car fitments represented 39.44% of the African tire market share in 2024 and will grow 4.97% annually, underpinned by rising personal mobility. However, e-commerce and construction are swelling light-commercial and heavy-duty truck volumes. Greater axle loads translate into more frequent replacements, enlarging value pools for suppliers in this segment.

Two-wheeler demand thrived in Lagos, Nairobi, and Kampala as ride-hailing firms expanded motorcycle taxi fleets. Off-the-road lines servicing excavators and loaders are niche in volume but lucrative in margin. Manufacturers diversifying across these verticals hedge against slowing passenger-car turnover while tapping higher-frequency commercial cycles.

By Application: On-Road Supremacy with Off-Road Momentum

In 2024, on-road categories controlled 73.15% of the African tire market, reflecting the continent’s enlarging paved road network. The segment is also projected to expand with a CAGR of 5.15% by 2030. New asphalt supports higher speeds and necessitates stronger tread compounds, encouraging premiumization.

Off-road segments are climbing thanks to mining concessions in copper-rich Katanga and gold belts in Ghana. Specialized tread designs deliver superior traction on loose ground, commanding price premiums up to 35%. Brands offering application-specific engineering grab wallet share among fleet maintenance chiefs focused on uptime.

By End User: Aftermarket Bulk Meets OEM Growth Spurts

The aftermarket captured 78.66% of the African tire market share in 2024, anchored by used-vehicle inflows and a vast informal retail web. Tier-3 cities rely on small-scale dealers who prize immediate availability over brand pedigree, steering bulk orders toward cost-focused Asian suppliers.

OEM sales will expand 6.04% during 2025-2030, as financing schemes make new cars attainable for middle-income households. Local assembly hubs in South Africa and Morocco specify global Tier-1 brands, rewarding suppliers that can meet stringent homologation and just-in-time delivery requirements. Balancing both channels is essential to optimizing volume and margin.

By Rim Size: Mid-Sized Rims Lead, Larger Diameters Surge

The 15-20-inch bracket generated 48.55% of the African tire market share in 2024, buoyed by compact sedans and light trucks. Yet sizes above 20 inches will post a 5.87% CAGR as SUV popularity rises and construction fleets grow. Larger diameters yield higher average selling prices, improving manufacturers' gross margins.

Below-15-inch demand is tapering as minicars lose favor in metropolitan centers where ride comfort and status signaling motivate bigger wheels. Producers reducing SKU complexity in this shrinking slice can redeploy capacity toward fast-growing large formats.

By Propulsion: ICE Dominance, EV Tailwinds

Internal combustion units held 90.24% of the African tire market share in 2024, but electric vehicles will accelerate at 9.49% annually, spearheaded by South Africa’s tax-rebate scheme and Morocco’s charging corridors. EV tires require lower rolling resistance and sound-absorbing tread blocks, prompting premium brands to invest in R&D.

Hybrid uptake is modest yet signals future diversification. Suppliers that pilot EV-centric compounds now will capture first-mover goodwill as grid expansion and battery price declines push electrification deeper into taxi and delivery fleets.

Geography Analysis

Algeria contributed 26.75% of the African tire market share in 2024, sustained by hydrocarbon revenues that keep import lines open and consumer liquidity stable. Tariff-free access to European ports shortens lead times, benefiting distributors offering mid-range radials. Inflation remained contained in 2025, preserving spending power for private car owners and taxi cooperatives.

The Democratic Republic of Congo is forecast to post a 6.21% CAGR to 2030, the largest across the African tire market. Chinese-backed infrastructure projects and copper-cobalt mining are proliferating heavy-truck purchases. Though logistics hurdles persist, suppliers that partner with local wholesalers can bypass port bottlenecks by routing via Angola’s Atlantic hubs.

The Rest-of-Africa cluster paints a diverse picture. Nigeria’s sizable but currency-strained market pivots toward domestically assembled tires as naira weakness inflates import bills. South Africa’s mature OEM sector sustains baseline demand and enforces strict quality audits that favor global Tier-1 brands. Kenya is emerging as an East African manufacturing gateway, enhanced by Linglong’s plant that will ship to Uganda, Tanzania, and Rwanda within 24 hours. Exchange-rate stability and improving road density give these states a predictable consumption outlook.

Competitive Landscape

Global majors such as Michelin, Bridgestone, and Continental maintain reputations for durability and technological depth, capturing premium urban consumers and OEM fitments. Chinese challengers, Zhongce Rubber, Triangle Tyre, Sailun, and Linglong are gaining share via local factories that trim landed costs significantly.

Vertical integration is intensifying. The Qingdao Sentury Tire Co., Ltd., Morocco plant sources rubber additives locally while leveraging Tangier Med port for rapid distribution. Michelin is trialing recycled-material treads in South Africa to align with circular economy mandates, targeting fleet clients keen on ESG metrics. Linglong signed a memorandum with Kenyan authorities to train technicians, embedding the brand within the service ecosystem.

Technology is the next battleground. Bridgestone’s web-connected “Tirematics” platform and Continental’s ContiConnect Live target mining fleets demanding predictive maintenance. Chinese firms counter with lower-cost sensor kits bundled into premium SKUs, narrowing the differential. As governments toughen homologation checks, compliance capacity will increasingly sort contenders from pretenders.

Africa Tire Industry Leaders

Michelin

Bridgestone Corporation

The Goodyear Tire & Rubber Company

Continental AG

Zhongce Rubber Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CFAO Mobility Kenya has taken a significant step by acquiring Tyre Distribution Africa (TYDIA). With this acquisition, CFAO Mobility Kenya becomes the official distributor for Michelin and BF Goodrich tires in East Africa. This strategic move emphasizes CFAO Mobility Kenya's dedication to enhancing its automotive portfolio and providing superior customer solutions across the region.

- January 2025: Linglong Tire, a leading tire manufacturer hailing from China, is poised to establish a factory in Kenya, with eyes set on the expansive African market. This initiative aligns seamlessly with government efforts to attract global enterprises, further cementing Kenya's reputation as a prime hub for foreign investments.

- October 2024: Sentury's factory in Morocco marked a significant milestone as it rolled out its inaugural 17-inch and 18-inch tires, officially kicking off its operations.

- July 2024: Tiger Wheel & Tyre, a prominent South African retailer, unveiled six new stores across South Africa and Namibia in just six weeks. This swift expansion underscores the brand's 57-year heritage and its influential role in South Africa's automotive service landscape.

Africa Tire Market Report Scope

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic / Airless |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks and Buses |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road (Construction, Mining, Agriculture) |

| OEM |

| Aftermarket (Replacement and Retread) |

| Below 15 inches |

| 15 - 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| Algeria |

| Democratic Republic of the Congo |

| Sudan |

| Libya |

| Chad |

| Rest of Africa |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic / Airless | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks and Buses | |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road (Construction, Mining, Agriculture) | |

| By End User | OEM |

| Aftermarket (Replacement and Retread) | |

| By Rim Size | Below 15 inches |

| 15 - 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid and Fuel-Cell Vehicles | |

| By Country | Algeria |

| Democratic Republic of the Congo | |

| Sudan | |

| Libya | |

| Chad | |

| Rest of Africa |

Key Questions Answered in the Report

How large is the Africa tire market in 2025?

The Africa tire market size stands at USD 7.10 billion in 2025 and is projected to reach USD 8.94 billion by 2030.

What is the expected growth rate for Africa’s tire demand?

Overall demand is forecast to expand at a 4.72% CAGR between 2025 and 2030.

Which country currently leads sales across the continent?

Algeria holds 26.75% of 2024 revenue, benefiting from hydrocarbon income that keeps import channels liquid.

Which tire segment is growing fastest by design?

Non-pneumatic/airless formats show the highest 6.71% CAGR thanks to mining and heavy-equipment use cases.

Page last updated on: