India Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

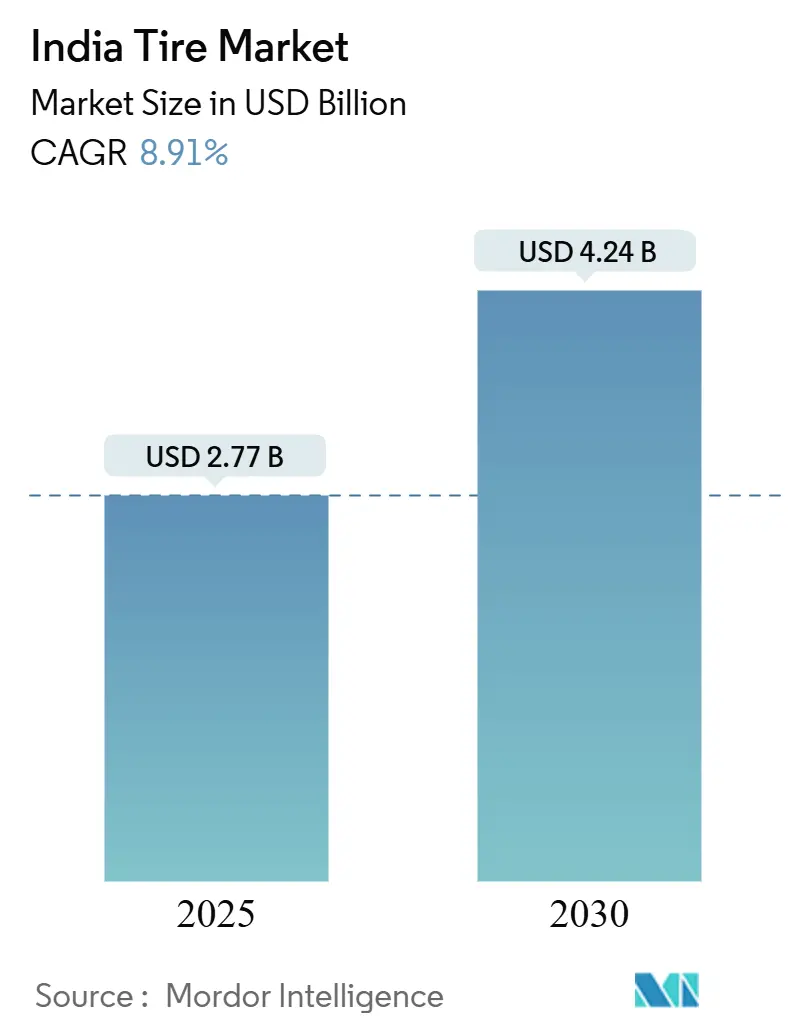

| Market Size (2025) | USD 2.77 Billion |

| Market Size (2030) | USD 4.24 Billion |

| Growth Rate (2025 - 2030) | 8.91% CAGR |

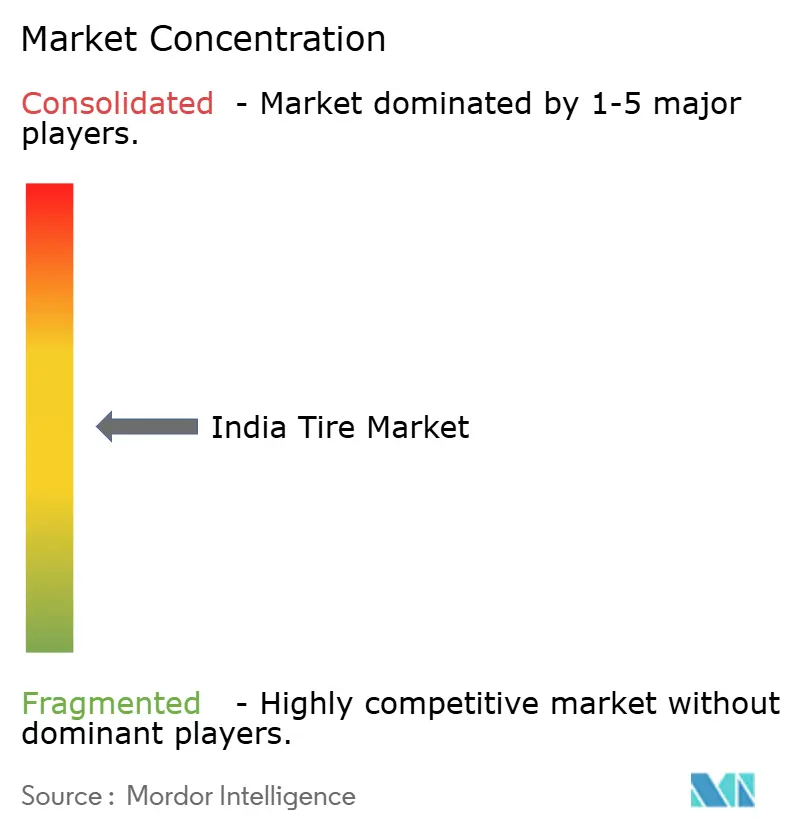

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Tire Market Analysis by Mordor Intelligence

The Indian tire market size stands at USD 2.77 billion in 2025 and is forecast to reach USD 4.24 billion by 2030, expanding at an 8.91% CAGR over 2025-2030. Accelerating infrastructure spending, two-wheeler electrification, and radial-upgrade regulations push demand upward even as natural-rubber cost swings pressure margins. Replacement activity keeps volume stable while original-equipment orders rise alongside domestic vehicle production. Government anti-dumping duties and the BIS star-labeling framework reinforce the value proposition of locally manufactured, fuel-efficient products. Competitive differentiation is shifting from price to performance, particularly toward low-rolling-resistance, sensor-enabled, and EV-optimized designs that reduce fleet operating costs and align with tightening emission rules.

Key Report Takeaways

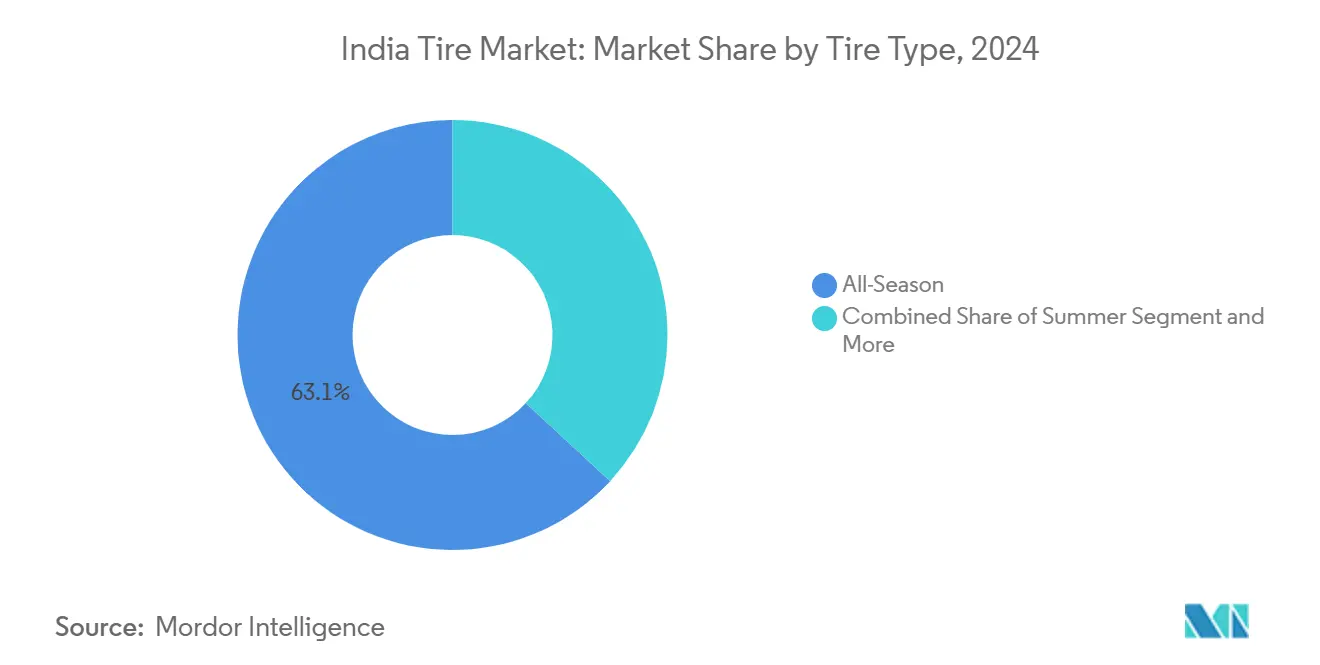

- By tire type, all-season models captured 63.12% of the Indian tire market share in 2024, whereas all-terrain offerings are forecast to advance at a 10.38% CAGR to 2030.

- By tire design, radial construction held 72.46% of the Indian tire market size in 2024; non-pneumatic formats are poised for the fastest 9.7%-plus CAGR through 2030.

- By vehicle type, the two-wheeler segment retained 45.87% revenue share in 2024, while SUVs and crossovers are projected to expand at an 11.94% CAGR over 2025-2030.

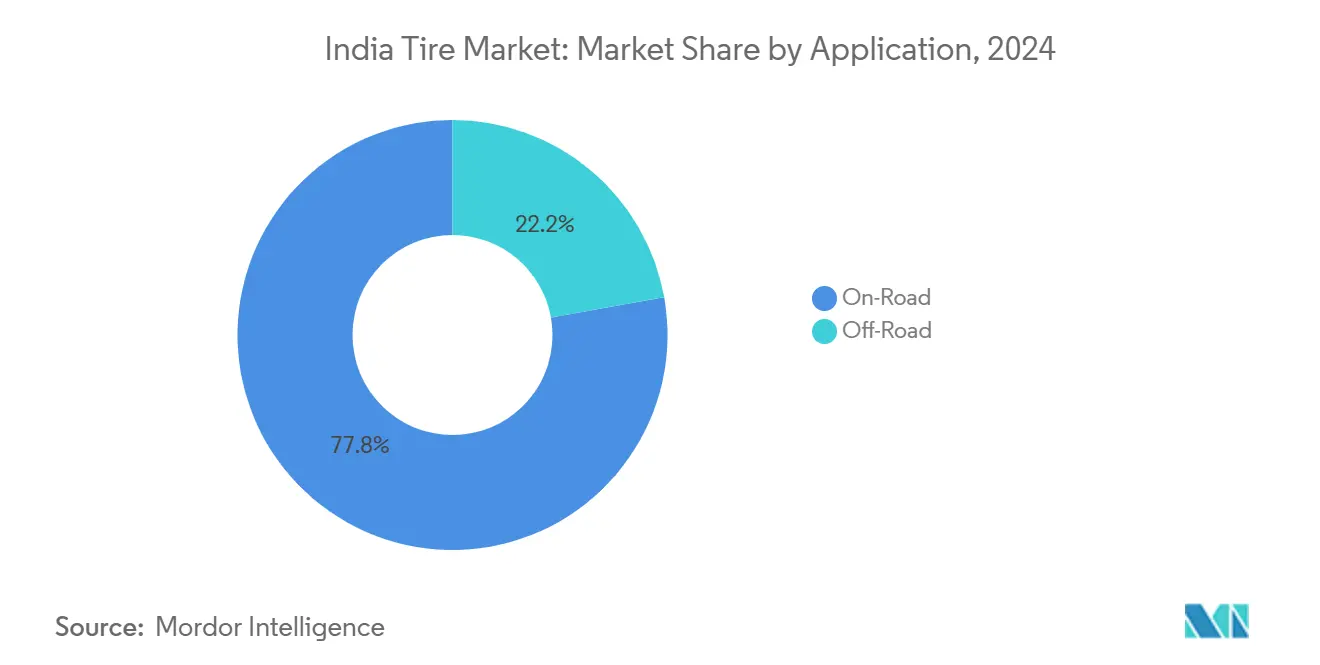

- By application, on-road demand accounted for 77.84% of the Indian tire market size in 2024; off-road demand is set to climb at a 9.71% CAGR through 2030.

- By end user, the aftermarket held a 60.92% share in 2024, whereas OEM fitments are projected to grow at an 8.64% CAGR to 2030.

- By rim size, the 15 to 20-inch category commanded 54.18% of the Indian tire market share in 2024, yet sizes above 20 inches led growth at an 11.83% CAGR to 2030.

- By propulsion, internal-combustion vehicles dominated with 88.74% share in 2024, but battery-electric vehicles represent the fastest-rising slice at a 31.27% CAGR for 2025-2030.

India Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Infrastructure Spend Fuels Commercial Tire Demand | +2.1% | Maharashtra, Gujarat, Tamil Nadu | Medium term (2–4 years) |

| Rapid Electrification of the Two-Wheeler Parc Accelerates EV-Optimised Tire Uptake | +1.8% | Urban centers and Tier-2 cities | Short term (≤ 2 years) |

| BIS Star-Labelling for Rolling Resistance Drives Radial-Upgrade Cycle | +1.4% | National | Medium term (2–4 years) |

| Government Anti-Dumping Duties Protect Domestic Producers | +0.9% | National | Long term (≥ 4 years) |

| Smart-Tire Sensor Integration Unlocks New OE Revenue Streams | +0.7% | Urban fleet corridors | Long term (≥ 4 years) |

| Fleet Telematics Contracts Incentivise Low-Rolling-Resistance Tires | +0.6% | Logistics corridors | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surging Infrastructure Spend Fuels Commercial Tire Demand

Government infrastructure allocation through the National Infrastructure Pipeline creates sustained demand for heavy commercial vehicles in construction, mining, and logistics applications. The Ministry of Heavy Industries' PLI scheme for automotive components, with an outlay of INR 25,938 crore, incentivizes domestic value addition requirements that benefit local tire manufacturers while driving commercial vehicle production scale[1]"Year End Review 2024: Ministry of Heavy Industries," Press Information Bureau, pib.gov.in.. Road construction projects under the PM Gati Shakti and Bharatmala initiatives require specialized tires for construction equipment and material transport vehicles. Commercial vehicle sales correlate with infrastructure capex deployment, creating predictable replacement cycles for fleet operators. The sector's growth momentum accelerates as state governments implement complementary infrastructure programs that expand beyond federal initiatives. Infrastructure-driven demand provides margin stability as commercial operators prioritize durability and total cost of ownership over initial price considerations.

Rapid Electrification of Two-Wheeler Parc Accelerates EV-Optimized Tire Uptake

Two-wheeler electrification targets 50-60% penetration by 2030, fundamentally altering tire performance requirements as electric motors deliver instant torque that demands enhanced grip characteristics[2]Ketan Thakkar, "India's EV Battery Plans May Run into Domestic Supply Glut," Autocar Professional, autocarpro.in. . EV-specific tire formulations optimize rolling resistance to extend battery range while managing noise reduction requirements that become critical without internal combustion engine masking. Rural two-wheeler demand recovery outpaces urban markets at 8.39% versus 6.77% growth, creating geographic expansion opportunities for EV-optimized products as charging infrastructure deployment accelerates. FAME-II incentives and state-level EV policies drive adoption velocity, particularly in delivery and ride-sharing applications where operational cost advantages justify premium tire investments. Manufacturers like CEAT are developing specialized compounds and tread patterns for electric two-wheelers, recognizing that traditional tire designs inadequately address EV performance characteristics.

BIS Star-Labelling for Rolling-Resistance Drives Radial-Upgrade Cycle

Bureau of Indian Standards' implementation of star-labeling for tire rolling resistance creates regulatory momentum that accelerates radial tire adoption across passenger and commercial segments. The certification framework, administered under the BIS Act 1986, establishes performance benchmarks that favor radial construction over bias-ply alternatives, driving technology upgrade cycles among domestic manufacturers[3]"Products under Compulsory Certification," BIS, bis.gov.in.. Fuel efficiency regulations indirectly mandate low-rolling-resistance specifications as fleet operators seek operational cost reductions amid volatile fuel prices. Star-labeling transparency enables informed purchasing decisions by commercial buyers who previously relied on brand reputation rather than performance metrics. The regulatory framework creates competitive differentiation opportunities for manufacturers investing in advanced tread compounds and construction technologies. Compliance requirements establish entry barriers for low-quality imports while rewarding domestic innovation in rolling resistance optimization.

Government Anti-Dumping Duties Protect Domestic Producers

Trade remedies implementation shields domestic manufacturers from predatory pricing by international competitors, particularly Chinese producers who previously disrupted market pricing through below-cost exports. Anti-dumping measures on steel wheels and related automotive components create upstream protection that stabilizes input costs for domestic tire manufacturers. Import restrictions on waste tires limit low-cost retreading competition while encouraging domestic recycling infrastructure development. Duty protection enables domestic capacity expansion investments as manufacturers gain pricing power and margin stability previously eroded by unfair trade practices. The policy framework supports technology transfer and joint venture formation as international players establish local manufacturing to avoid tariff barriers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural-Rubber Price Volatility Squeezes Margins | -1.7% | Kerala and Tamil Nadu Tapping Regions | Short Term (≤ 2 Years) |

| Tightening Scrappage Policy Defers Replacement Purchases | -1.2% | Urban Clusters with Older Fleets | Medium Term (2–4 Years) |

| Slow Rural Demand Recovery Curbs Two-Wheeler Sales | -1.0% | Rural and Semi-Urban Markets | Medium Term (2–4 Years) |

| Import Dependence on High-Performance Synthetic Rubber Raises Forex Risk | -0.8% | National (Ports and Industrial Hubs) | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Natural-Rubber Price Volatility Squeezes Margins

Natural rubber price increases exceeding 50% in 2024 create acute margin pressure as manufacturers struggle to pass through cost inflation to price-sensitive consumers and fleet operators. India's natural rubber deficit of 550,000 tons annually exposes domestic producers to international price volatility driven by supply disruptions in Southeast Asian producing regions. Synthetic rubber import dependence compounds forex risk as rupee depreciation amplifies input cost inflation, particularly affecting manufacturers with limited hedging capabilities. Raw material costs represent 60-65% of tire manufacturing expenses, creating operational leverage that magnifies profit volatility during commodity price cycles. Manufacturers like Apollo Tires and CEAT reported margin compression in recent quarters as selective price increases failed to fully offset input cost inflation fully, forcing operational efficiency improvements and product mix optimization strategies.

Tightening Scrappage Policy Defers Replacement Purchases

Vehicle scrappage policy implementation creates replacement demand uncertainty as the lukewarm response to incentive programs delays fleet renewal cycles that traditionally drive aftermarket tire sales. The policy's voluntary nature and limited financial incentives result in extended vehicle lifecycles that defer replacement tire purchases, particularly in commercial segments where operators maximize asset utilization. Rural demand recovery remains constrained by income pressures that prioritize essential spending over discretionary vehicle maintenance, creating geographic disparities in replacement demand patterns. Scrappage program design flaws, including inadequate compensation for end-of-life vehicles, limit participation rates and extend the average age of the vehicle parc. Extended replacement cycles compress aftermarket volumes while shifting demand toward premium, longer-lasting tire specifications that reduce replacement frequency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tire Type: All-Season Dominance Faces Terrain-Specific Challenge

All-season tires commanded 63.12% market share in 2024, reflecting consumer preference for versatile performance across India's diverse climatic conditions and road surfaces. However, all-terrain tires are accelerating at a 10.38% CAGR through 2030, driven by SUV proliferation and adventure tourism growth that demands enhanced off-road capability. Winter tires remain niche given India's tropical climate, while summer tires serve specialized applications in extreme heat conditions across the northern plains. The shift toward all-terrain specifications reflects changing consumer behavior as urban buyers seek vehicles for city commuting and weekend recreational activities.

CEAT's launch of specialized all-terrain products and Apollo Tires' Apterra AT2 range demonstrate the manufacturer's response to evolving performance requirements. All-season segment growth moderates as consumers prioritize specific performance attributes over general-purpose functionality. The segmentation evolution indicates market maturation where differentiated products capture premium pricing opportunities previously unavailable in commodity-focused segments.

By Tire Design: Radial Technology Consolidates Market Position

Radial construction captured 72.46% market share in 2024 and continues expanding at 7.62% CAGR as fuel efficiency regulations and performance requirements favor advanced construction methods over traditional bias-ply alternatives. Non-pneumatic airless tires represent emerging technology with limited commercial deployment but significant long-term potential for specific applications, including two-wheelers and low-speed vehicles. Bias construction persists in price-sensitive segments and specialized applications where radial advantages don't justify cost premiums. The technology transition reflects broader automotive industry evolution toward performance optimization and operational efficiency.

BIS star-labeling requirements effectively mandate radial adoption in regulated segments, creating regulatory momentum that accelerates market transformation. Manufacturers invest heavily in radial production capacity while phasing out bias-ply lines, indicating an irreversible technology transition. Non-pneumatic development by global manufacturers suggests potential for future disruption, though commercial viability remains limited by cost and performance constraints.

By Vehicle Type: Two-Wheeler Leadership Challenged by SUV Surge

Two-wheelers maintained a 45.87% market share in 2024, reflecting India's mobility patterns and urban transportation preferences, though growth moderates as the segment matures. SUVs and crossovers emerge as the fastest-growing segment at 11.94% CAGR, driven by rising disposable incomes, consumer preference for higher seating positions, and perceived safety benefits. Light commercial vehicles benefit from e-commerce expansion and last-mile delivery growth, while heavy commercial trucks and buses serve infrastructure development and public transportation expansion. Off-the-road and specialty applications grow with mining, agriculture, and construction activity.

Rural two-wheeler recovery outpaces urban markets, with FADA data showing 7.71% growth in FY25 as rural incomes stabilize and financing availability improves. The vehicle type evolution reflects broader economic transformation as India transitions from two-wheeler-centric mobility toward multi-modal transportation preferences. The passenger car segment remains constrained by affordability challenges, while SUV growth indicates premiumization trends that benefit tire manufacturers through a higher-value product mix

By Application: On-Road Dominance Faces Off-Road Acceleration

On-road applications commanded 77.84% market share in 2024, reflecting India's road-centric transportation infrastructure and urban mobility patterns. Off-road applications accelerate at a 9.71% CAGR through 2030, driven by construction, mining, and agricultural mechanization that demands specialized tire performance characteristics. The segmentation reflects economic diversification as India expands beyond services toward manufacturing and infrastructure development that requires heavy machinery deployment. Construction equipment demand surges with infrastructure spending, while mining activity expands to support industrial growth requirements.

Government infrastructure initiatives under PM Gati Shakti and National Infrastructure Pipeline create sustained off-road tire demand as construction projects require specialized equipment with terrain-specific tire specifications. Agricultural mechanization trends favor larger, more capable equipment that demands advanced tire technology for soil protection and operational efficiency. The application shift indicates market sophistication as end-users prioritize performance optimization over cost minimization.

By End User: Aftermarket Strength Challenged by OEM Momentum

The aftermarket segment maintained 60.92% market share in 2024, reflecting India's large installed vehicle base and replacement-driven demand patterns that favor independent distribution channels. OEM segment accelerates at 8.64% CAGR through 2030 as domestic vehicle production scales and manufacturers integrate advanced tire specifications into new vehicle designs. The segmentation evolution reflects the maturation of the automotive industry as OEMs increasingly specify performance tires rather than commodity alternatives. Replacement demand benefits from extended vehicle lifecycles and deferred replacement cycles that increase tire wear rates.

Vehicle production growth under PLI automotive schemes drives OEM demand as manufacturers establish domestic supply chains that favor local tire producers over imports. Aftermarket channel evolution includes digital platforms and organized retail expansion that improves consumer access and service quality. The end-user dynamic indicates market structure transformation as organized channels gain share from traditional unorganized distribution networks.

By Rim Size: Mid-Range Dominance Faces Premium Expansion

The 15-20-inch rim size category commanded 54.18% of the market share in 2024, reflecting mainstream passenger vehicle specifications and commercial vehicle requirements. Above 20-inch segments accelerate at 11.83% CAGR through 2030, driven by SUV premiumization and luxury vehicle adoption that demands larger wheel specifications. Below 15 inches serves entry-level segments and two-wheeler applications where cost sensitivity constrains upgrade adoption. The evolution of rim size reflects the automotive industry's trend toward larger wheels that enhance vehicle aesthetics and performance characteristics.

Premiumization trends favor larger rim sizes as consumers associate wheel size with vehicle quality and status, creating margin expansion opportunities for tire manufacturers serving high-value segments. Commercial vehicle specifications remain stable in mid-range categories where operational requirements prioritize durability over aesthetics. The segmentation shift indicates market maturation as consumer preferences evolve beyond basic transportation toward lifestyle and status considerations.

By Propulsion: ICE Dominance Faces Electric Disruption

Internal combustion engines retained 88.74% market share in 2024, reflecting the installed vehicle base and continued dominance of conventional powertrains in new vehicle sales. Battery-electric vehicles represent the fastest-growing segment at 31.27% CAGR, though from a small base that limits near-term market impact. Hybrid and fuel-cell vehicles serve niche applications with limited commercial deployment but growing manufacturer interest. The propulsion evolution reflects the automotive industry's transformation toward electrification, which fundamentally alters tire performance requirements.

EV-specific tire development focuses on rolling resistance optimization, noise reduction, and instant torque management, which conventional tires inadequately address. Government EV policies, including FAME-II and state-level incentives, accelerate adoption velocity, particularly in the two-wheeler and commercial segments, where operational cost advantages justify premium investments. The propulsion transition creates product development opportunities as manufacturers adapt formulations and construction methods for electric vehicle characteristics.

Geography Analysis

India represents the primary geographic focus for this market analysis, with regional variations reflecting economic development patterns, infrastructure quality, and vehicle adoption rates across states and territories. Maharashtra, Tamil Nadu, Gujarat, and Karnataka emerge as leading consumption centers due to concentrated automotive manufacturing, higher disposable incomes, and superior road infrastructure that supports premium tire adoption. These states benefit from established automotive clusters that create OEM demand and aftermarket replacement requirements, while their industrial development drives commercial vehicle deployment that demands specialized tire applications.

Northern states, including Uttar Pradesh, Punjab, and Haryana, show strong growth potential driven by agricultural mechanization and infrastructure development under government initiatives, though price sensitivity constrains premium product adoption. The Delhi NCR region represents a significant market due to high vehicle density and consumer purchasing power. At the same time, extreme weather conditions create specific performance requirements for tire durability and heat resistance. Eastern states, including West Bengal and Odisha, benefit from mining activity and port development that drives heavy commercial vehicle demand. However, overall market development lags in Western and Southern regions due to lower industrial activity and income levels.

Rural markets across all regions demonstrate recovery momentum as two-wheeler electrification and agricultural mechanization create new demand patterns that favor domestic manufacturers with established distribution networks. The geographic distribution reflects India's economic transformation as infrastructure development and industrial expansion create regional growth opportunities that benefit tire manufacturers with national presence and local manufacturing capabilities. State-level EV policies and infrastructure incentives create geographic variations in electric vehicle adoption, influencing tire demand composition and performance requirements across different regions.

Competitive Landscape

The Indian tire market exhibits moderate fragmentation with domestic players MRF, Apollo Tires, JK Tire, and CEAT competing against international manufacturers including Bridgestone, Michelin, Continental, and Goodyear across different segments and price points. Market concentration varies by segment, with premium categories showing higher consolidation while entry-level segments remain fragmented among numerous regional players. Strategic patterns emphasize capacity expansion, technology upgrades, and product portfolio diversification as manufacturers adapt to evolving performance requirements and regulatory mandates. White-space opportunities emerge in EV-specific formulations, smart tire integration, and specialized applications, including off-road and agricultural segments, where performance requirements exceed current product capabilities.

Technology deployment focuses on rolling resistance optimization, smart sensor integration, and advanced compounds that address electric vehicle characteristics and fuel efficiency regulations. MRF reported revenue growth with dividend distributions of INR 200 per share, while Apollo Tires invested in European R&D capabilities, and CEAT achieved double-digit growth in replacement and international segments. Emerging disruptors include specialized manufacturers targeting niche applications and technology companies developing smart tire solutions that integrate with fleet management systems. The competitive dynamics reflect market maturation as manufacturers shift from volume-based competition toward value-added products and services that command premium pricing and improve customer loyalty.

India Tire Industry Leaders

-

Apollo Tyres Ltd.

-

JK Tyre & Industries Ltd.

-

Balkrishna Industries Ltd. (BKT)

-

MRF Tyres

-

CEAT

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: India’s tire industry is set to gain a competitive edge in the UK market following the signing of the India–UK Comprehensive Economic and Trade Agreement (CETA). Under this landmark deal, all import duties on tires and rubber products exported from India to the UK have been eliminated immediately, providing a strong boost to the price competitiveness of Indian producers.

- April 2025: Goodyear Tire & Rubber Company is evaluating the potential sale of its Indian agricultural tire division as part of its broader "Goodyear Forward" restructuring initiative. The division, which commands approximately 50% market share in India’s farm tire segment, is being valued between ₹2,500 crore and ₹2,700 crore (roughly USD 300 million)

- December 2024: In December 2024, JK Tyre & Industries secured a Euro 30 million (EUR 30 million) long-term loan from Germany's development finance institution DEG. The funding is earmarked for a sustainable expansion of its passenger car radial (PCR) tire production facility in Madhya Pradesh.

India Tire Market Report Scope

| Summer |

| Winter |

| All-Season |

| All-Terrain/Mud-Terrain |

| Radial |

| Bias |

| Non-pneumatic/Airless |

| Passenger Cars |

| SUVs and Crossovers |

| Light Commercial Vehicles |

| Heavy Commercial Trucks and Buses |

| Two-Wheelers |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road (Construction, Mining, Agriculture) |

| OEM |

| Aftermarket (Replacement and Retread) |

| Below 15 inches |

| 15 to 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| By Tire Type | Summer |

| Winter | |

| All-Season | |

| All-Terrain/Mud-Terrain | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic/Airless | |

| By Vehicle Type | Passenger Cars |

| SUVs and Crossovers | |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks and Buses | |

| Two-Wheelers | |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road (Construction, Mining, Agriculture) | |

| By End User | OEM |

| Aftermarket (Replacement and Retread) | |

| By Rim Size | Below 15 inches |

| 15 to 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid and Fuel-Cell Vehicles |

Key Questions Answered in the Report

What is the forecast value of the India tyre market in 2030?

It is projected to reach USD 4.24 billion by 2030, growing at an 8.91% CAGR.

Which tyre design dominates current sales?

Radial construction led with a 72.46% share in 2024 due to fuel-efficiency mandates.

How fast is electric-vehicle tyre demand expanding?

Battery-electric fitments are advancing at a 31.27% CAGR, the fastest among propulsion classes.

Which rim-size band is growing quickest?

Tyres above 20 inches are rising at an 11.83% CAGR, driven by premium SUV adoption.

What factor most threatens manufacturer margins?

Natural-rubber volatility, with a 50% price jump in 2024, reduced profitability by 1.7 percentage points on CAGR forecasts.

Page last updated on: