Brazil Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

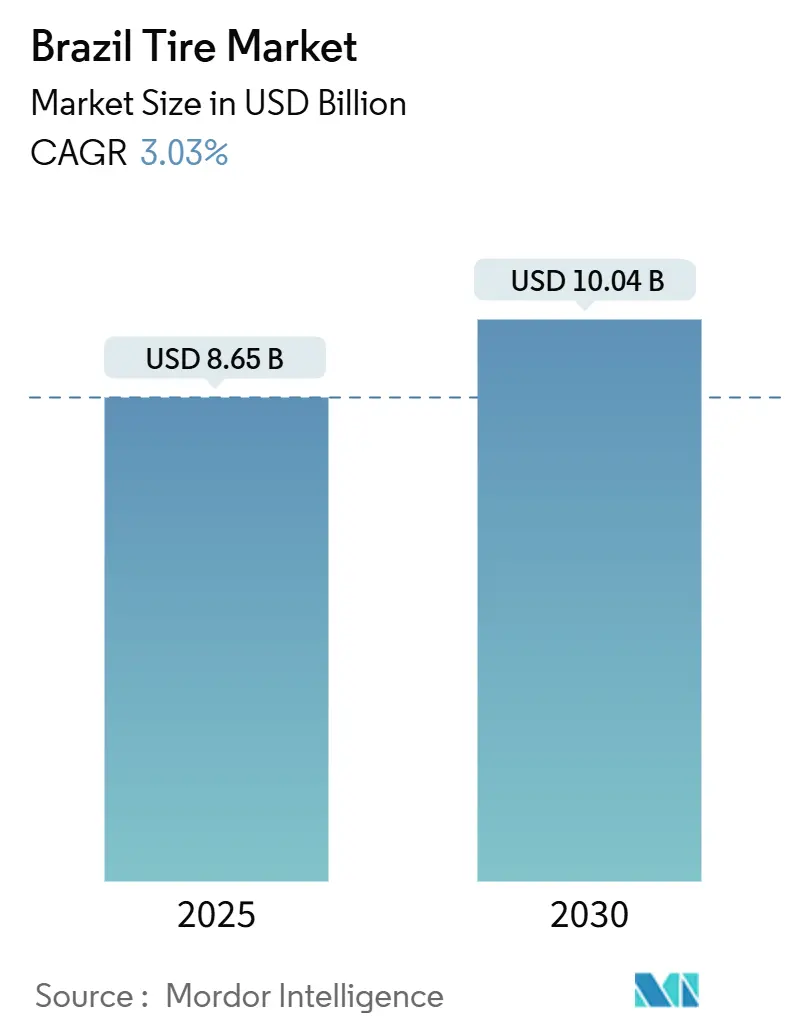

| Market Size (2025) | USD 8.65 Billion |

| Market Size (2030) | USD 10.04 Billion |

| Growth Rate (2025 - 2030) | 3.03% CAGR |

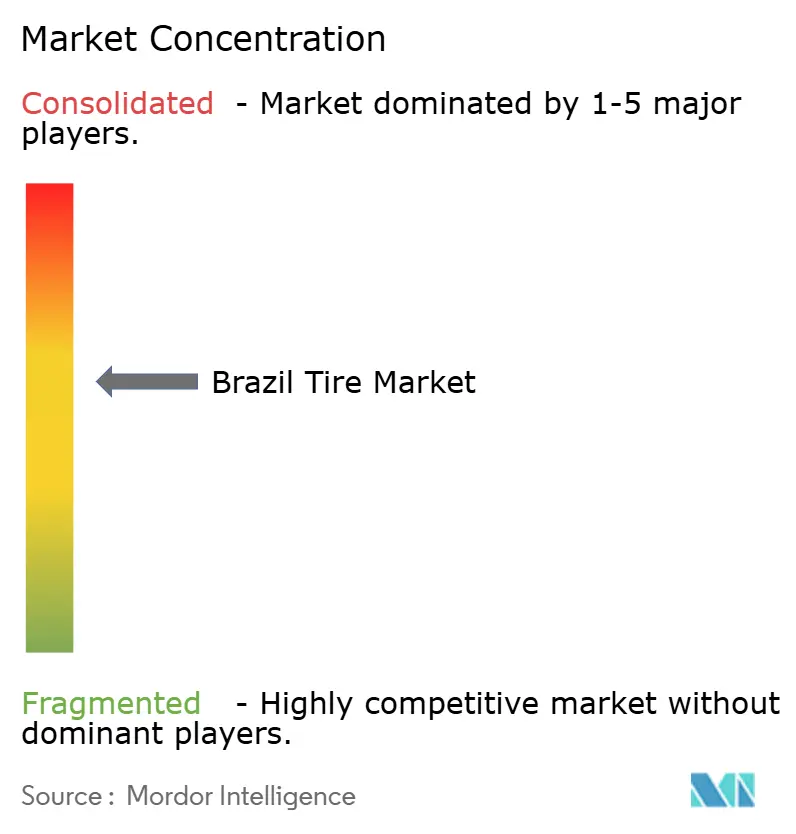

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Tire Market Analysis by Mordor Intelligence

The Brazilian tire market size reached USD 8.65 billion in 2025 and is forecast to climb to USD 10.04 billion by 2030, advancing at a 3.03% CAGR. Firm replacement-tire demand tied to an aging national vehicle fleet, a steady rebound in new-car output under the Nova Indústria Brasil incentives, and brisk freight activity linked to agribusiness exports anchor near-term growth. The Brazilian tire market benefits from SUV penetration exceeding one in two new registrations, driving a shift toward larger rim diameters and premium compounds. Digitalization of B2B sales channels boosts price transparency and inventory turns for fleet operators, while mandatory INMETRO labeling hastens product innovation around rolling-resistance and wet-grip metrics. Competitive intensity remains moderate, global incumbents preserve pricing discipline in premium tiers even as Chinese producers add local capacity to reduce antidumping exposure.

Key Report Takeaways

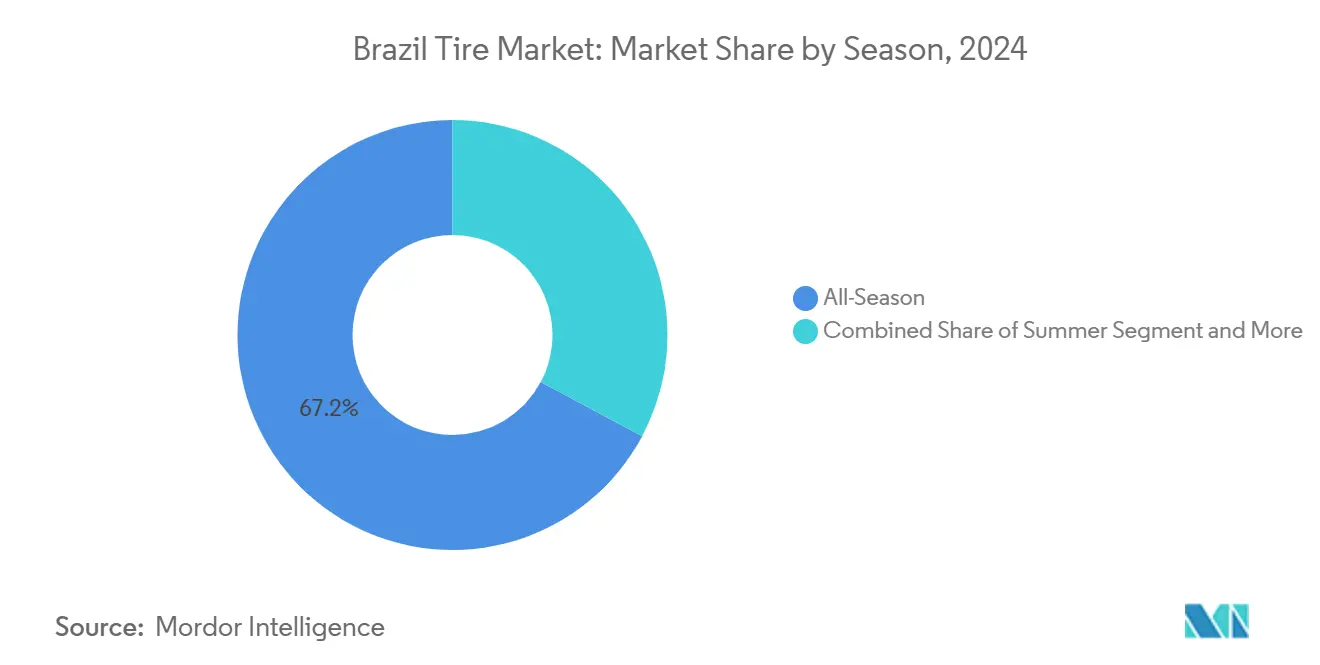

- By season, all-season tires accounted for 67.15% of the Brazilian tire market share in 2024, whereas winter tires are projected to expand the fastest at a 4.11% CAGR to 2030.

- By tire design, radial construction held 92.33% of the Brazilian tire market share in 2024, while non-pneumatic/airless formats are set to register a 5.85% CAGR through 2030.

- By vehicle type, passenger cars captured 48.14% of the Brazilian tire market size in 2024 and are poised to progress at a 3.55% CAGR to 2030.

- By application, on-road uses represented 82.46% of the Brazilian tire market in 2024; the same category is forecast to grow at a 3.94% CAGR through 2030.

- By end user, the aftermarket segment generated 74.12% of the Brazilian tire market share in 2024, yet OEM supply is predicted to post a stronger 4.73% CAGR through 2030.

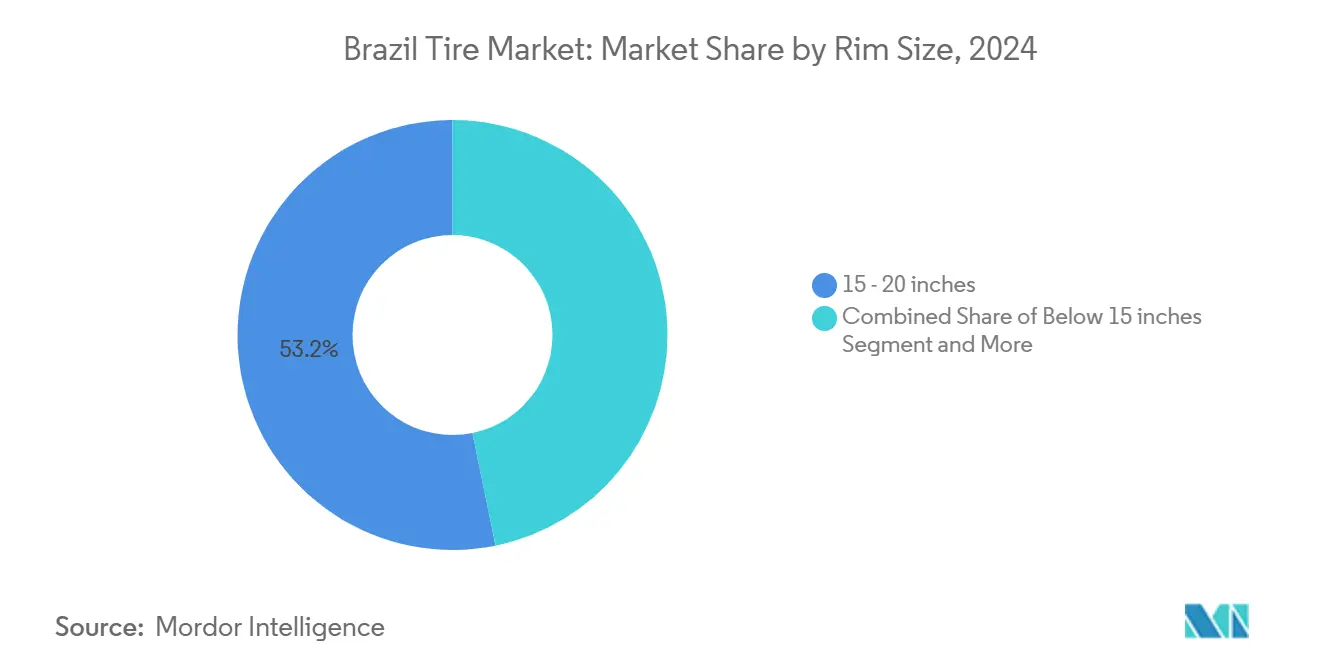

- By rim size, 15- to 20-inch products supplied 53.15% of the Brazilian tire market share in 2024, while sizes above 20 inches are likely to deliver the fastest 5.36% CAGR by 2030.

- By propulsion, Internal-combustion segments retain 90.15% of the Brazilian tire market size in 2024 and battery-electric vehicles are on track for a 9.66% CAGR to 2030.

Brazil Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Stimulus for Auto Manufacturing | +0.8% | National, with emphasis in São Paulo and Minas Gerais | Medium term (2-4 years) |

| Rising SUV Penetration In Brazil | +0.7% | National, stronger in South and Southeast | Medium term (2-4 years) |

| Growth of B2B E-Commerce | +0.6% | National, early gains in São Paulo and Rio de Janeiro | Short term (≤2 years) |

| Logistics Boom from Agribusiness | +0.5% | Central-West and Northeast corridors | Medium term (2-4 years) |

| Mandatory Tire Labeling Standards | +0.3% | National | Long term (≥4 years) |

| Emerging Off-Road Tourism | +0.2% | Interior and coastal recreation zones | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Government Stimulus for Local Auto Manufacturing 2024-2027

Fiscal incentives embedded in the Nova Indústria Brasil plan encourage tire makers to add green-field capacity, countering a significant jump in tire imports logged between 2017 and 2023. Local sourcing curbs foreign-exchange exposure and lets producers meet INMETRO test cycles without shipping delays. Radial lines attract the bulk of spending because existing Brazilian know-how shortens ramp-up times. The stimulus window extends to 2027, giving investors sufficient runway to displace low-priced Asian imports and lift the Brazilian tire market.

Rising SUV Penetration in Brazil

SUVs account for a significant share of new-car registrations, steering demand toward larger rims and reinforced sidewalls. Above-20-inch SKUs show the fastest CAGR because drivers favor curb appeal and elevated seating. OEMs specify low-rolling-resistance compounds that balance traction with fuel economy, raising average selling prices. Tire makers localize tread patterns for heavy summer rains in coastal states and pothole resistance inland. Dealer networks upsell performance upgrades that carry wider margins than standard sedan sizes.

Growth of B2B E-Commerce Tire Platforms

Fleet managers increasingly purchase tires through digital portals that quote real-time stock and dynamic discounts, streamlining procurement that was once telephone-based. Mercado Livre reported that the gross merchandise value of automotive parts will be R$2.3 billion (USD 397 million) in 2024, with tires supplying a significant share of turnover. Niche operators PneuStore and Dispetral now reach secondary cities without brick-and-mortar overhead. Commercial carriers like JSL tap platform analytics to schedule replacement cycles that cut downtime. Manufacturers glean live demand signals and allocate factory slots accordingly.

Logistics Boom from Agribusiness Exports

Record soybean and corn output scheduled for 2025 overloads freight corridors linking Mato Grosso fields to Santos and Itaqui ports. CONAB notes a surge in heavy-truck utilization accelerates wear on steer and drive axles [2]“2025 Logistics Bulletin,” National Supply Company (CONAB), conab.gov.br. Carriers seek 120,000-kilometer warranty casings and retreadable designs to contain operating costs. Producers with warehouses in Rondonópolis and Sorriso gain share because they replenish stock within 48 hours, beating coastal rivals. By enlarging the heavy-duty segment, the freight spike adds half a percentage point to CAGR for the Brazil tire market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FX-Driven Import Price Volatility | -0.9% | National | Short term (≤2 years) |

| High Cost of Natural Rubber | -0.6% | National supply chain | Long term (≥4 years) |

| Tire Recycling Disposal Bottlenecks | -0.4% | Urban centers | Medium term (2-4 years) |

| Delayed EV-Specific Tire Rules | -0.3% | Emerging EV corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

FX-Driven Import-Price Volatility

The Brazilian real swings sharply against the U.S. dollar, making the landed cost for imported tires unpredictable [3]“Tire Import Data 2023,” Secretariat for Foreign Trade (SECEX), secex.gov.br. Distributors lacking hedges must re-price weekly, eroding dealer confidence and freezing larger orders. Currency whiplash pushes fleets to delay bulk purchases until rates stabilize, depressing short-run sales. Domestic producers absorb some input shocks by blending synthetic and natural rubber, yet specialty additives remain dollar-denominated.

High Cost of Natural Rubber Amid Amazon ESG Scrutiny

NGO pressure forces tire firms to certify latex sourced from Pará and Acre against deforestation, adding chain-of-custody audits and satellite monitoring fees. Weather disruptions slash tapped volume and spur price spikes that ripple through invoice terms quarterly. Synthetic substitutes cost more energy to produce and cannot fully replace natural rubber in heavy-duty tires.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: Widespread all-season use anchors sales

All-season products generated 67.15% of the Brazilian tire market in 2024 and continue to outpace population growth because motorists seek one-set convenience in tropical climates. The winter sub-segment, though just 9% of demand, is rising at a 4.11% CAGR as southern states experience cooler winters and premium European-brand dealerships encourage seasonal swaps. OEM configuration lists now show factory-fit winter options on imported luxury models, nudging awareness in affluent consumer circles.

Seasonal diversification lets manufacturers lift margins by segmenting compounds for distinct microclimates. Winter tread in Porto Alegre ships mainly in Q3 ahead of colder months, smoothing factory utilization otherwise skewed to peak summer output. CONTRAN enforcement of “appropriate tire for conditions” standards prompts ride-sharing fleets to rotate season-specific packages to avoid fines. This multi-tier mix sustains balanced production loads and underpins incremental price premiums across the Brazilian tire market.

By Tire Design: Radial leadership meets airless disruption

Radial construction accounted for 92.33% of the Brazil tire market size in 2024, illustrating economies of scale and ride-comfort superiority. Heavy-truck fleets now demand all-steel radials with cut-chip tread for mixed highway-dirt routes in soybean corridors, which supports retread business models. Bias ply lingers under a minimal share among legacy tractor inventories, where carcass stiffness is prized over fuel savings.

Airless, non-pneumatic prototypes log a 5.85% CAGR in pilot deployments for urban delivery robots and refuse trucks. Their puncture immunity slashes downtime expenses, appealing to last-mile couriers operating tight schedules in congested city centers. Run-flat tires also win exemption from spare-wheel mandates, saving boot space in compact EVs. Tire makers test thermoplastic spokes molded at local tech parks to comply with local-content rules, signaling eventual mainstream crossover within the Brazilian tire market.

By Vehicle Type: Passenger cars at the forefront of value creation

Passenger-car fitments generated 48.14% of the Brazil tire market size in 2024 and track a 3.55% CAGR through 2030, buoyed by rising SUV trims priced above the segment average. Sedan replacement intervals shorten due to deteriorating urban road surfaces, lifting aftermarket volume.

Light commercial vans experience an uptick from e-grocery and parcel fulfilment, yet miles-per-tire cycle stretch longer because drivers adopt load-range C radials that last 30% more kilometers than decade-old designs. Heavy trucks capture agribusiness freight and new toll-road concessions, leaning on multi-life retread contracts that bundle telematics sensors. Two-wheeler share ebbs marginally as ride-sharing apps pivot to four-wheel platforms, though off-road motorcycles keep rural mobility alive. These shifts illustrate how nuanced sub-segments collectively shape the Brazil tire market size.

By Application: On-road predominance molds product architecture

In 2024, on-road demand contributed 82.46% of the Brazilian tire market's size and is advancing at a 3.94% CAGR as federal highway BR-163 upgrades reduce journey times between farms and ports. Tread longevity rises due to smoother asphalt, yet high ambient heat still accelerates shoulder cracking, pushing suppliers to tweak polymer blends.

Off-road supply remains vital for quarry, construction, and plantation work, often far from service centers. Ultra-deep lug patterns and heat-resistant carcasses carry price premiums that help offset lower unit volumes. Manufacturers position mobile service trucks on mine sites in Pará, capturing maintenance contracts that insulate revenue when civil works slow. These use cases fortify the Brazilian tire market against cyclical dips in any segment.

By End User: Aftermarket dominance spawns service innovation

The aftermarket claimed 74.12% of the Brazilian tire market size in 2024, reflecting an average fleet age of above 10.3 years. Independent retailers offer twelve-installment plans that resonate with budget-conscious drivers, especially in Northeast capitals where per-capita income trails the national mean.

OEM channel share is projected to edge by 4.73% CAGR by 2030 as assemblers localize SUV lines and roll out certified service centers. Branded outlets bundle free inspections and road-hazard warranties that retain customers beyond first replacement. Shared digital stock-locators bridge automaker and aftermarket systems, ensuring real-time parts visibility across the Brazilian tire market and trimming idle inventory days.

By Rim Size: Mainstream mid-sizes dominate while premium diameters surge

Rims between 15 and 20 inches supplied 53.15% of the Brazilian tire market size in 2024 and serve sedans, hatchbacks, and urban crossovers. Price-elastic shoppers in this band chase promotion bundles tied to fuel vouchers.

Rims above 20 inches advance at a 5.36% CAGR because luxury SUVs and pickup trucks makeovers command plus-size wheels. Import quotas once availability is squeezed, but new local forging lines shorten lead times to ten days. Below-15-inch share contracts are slowly exiting line-ups as micro-cars do. The broad rim spectrum compels producers to diversify SKU matrices while safeguarding plant efficiency, directly influencing profitability across the Brazilian tire market.

By Propulsion: EV traction signals a structural pivot

Internal-combustion segments retain 90.15% of the Brazilian tire market size in 2024, yet the battery-electric sub-set is sprinting at 9.66% CAGR as public charging points are growing nationwide.

EV tires integrate stronger bead bundles and low-noise tread blocks to offset instantaneous torque and cabin-quiet expectations. Initial pricing carries an 18% premium over ICE equivalents, but the total cost of ownership evens out through lower energy burn. Hybrid vehicles settle in the middle, usually adopting high-load indexes but standard compounds. The propulsion mix will reshape raw-material recipes and factory tooling within the Brazilian tire market over the next decade.

Geography Analysis

São Paulo commands the most significant slice of the Brazilian tire market because it hosts Pirelli, Bridgestone, and Continental plants alongside the country’s densest light-vehicle parc. Its port and highway web funnel imports and distributes finished goods nationwide, letting dealers promise next-day delivery within a 400-kilometer radius. Consumer affluence in the Southeast fuels demand for premium all-season and winter options with advanced labeling grades.

Central-West states such as Mato Grosso and Goiás generate outsized heavy-truck consumption tied to soybean and corn exports. Fleets in these corridors favor long-haul drive-axle radials with tread suitable for asphalt and unpaved access roads. Regional wholesalers stock deeper inventories around harvest windows to match seasonal cargo peaks. Despite lower population density, freight activity pushes the Brazil tire market size in the Central-West to outgrow the national average.

As new transshipment hubs emerge near Suape and Pecém ports, Northeast corridors witness accelerating demand. Tire buyers here lean toward value brands priced below the national mean, yet INMETRO enforcement ensures minimum safety standards hold. Southern states enjoy the coolest climate and the highest per-capita income, prompting early winter and performance tires adoption. Across all macro-regions, uniform federal labeling and recycling rules safeguard product consistency, while regional culture and economic makeup dictate distinct purchasing habits that producers must address to maximize Brazil's tire market penetration.

Competitive Landscape

Pirelli leads premium segments, holding a significant share of ultrahigh-performance SKU revenue in 2024. Bridgestone and Michelin trail but invest heavily in fleet solutions bundled with telematics that predict optimal rotation intervals, granting carriers 5-point fuel-efficiency gains. Goodyear exploits its Americana plant proximity to automotive OEM clusters, supplying original-fit tires for six SUV nameplates.

Chinese challengers scale fast: Linglong’s Paraná complex will output 15 million units yearly, covering PCR and TBR lines. XBRI plans a Bahia facility for export-grade passenger tires. Antidumping tariffs on low-cost imports, prolonged to 2030, spur offshore brands to “on-shore” and sidestep duties. Continental aims to triple its aftermarket footprint by expanding BestDrive franchised shop outlets.

Sustainability narratives shape brand differentiation. Michelin pilots carbon-neutral manufacturing modules in Resende, while Pirelli targets 100% renewable electricity. Domestic recyclers partner with municipal road agencies to embed crumb rubber in asphalt relays, projecting a notable compound annual tonnage growth. Digital momentum also rises: Goodyear integrates cloud-based demand sensing with São Paulo dealers, cutting backorders significantly. These moves collectively underscore a moderately concentrated but innovation-active Brazil tire market.

Brazil Tire Industry Leaders

Bridgestone Corporation

Pirelli & C. S.p.A.

Michelin Group

The Goodyear Tire & Rubber Company

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Brazil renewed anti-dumping duties on select Chinese passenger-car radials for five more years under GECEX Resolution 744.

- April 2025: Shandong Linglong Tire confirmed a USD 1.19 billion, 15-million-unit plant in Ponta Grossa alongside local distributor SUNSET S.A.

- September 2024: SUNSET Tires Corp allocated USD 256 million for a Brazilian factory to produce XBRI passenger models aimed at domestic and U.S. channels.

- July 2024: Trelleborg expanded supply via over 300 John Deere dealerships, bringing 700 tire SKUs to farmers under an Agrishow agreement.

Brazil Tire Market Report Scope

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic / Airless |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks and Buses |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road (Construction, Mining, Agriculture) |

| OEM |

| Aftermarket (Replacement and Retread) |

| Below 15 inches |

| 15 - 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic / Airless | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks and Buses | |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road (Construction, Mining, Agriculture) | |

| By End User | OEM |

| Aftermarket (Replacement and Retread) | |

| By Rim Size | Below 15 inches |

| 15 - 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid and Fuel-Cell Vehicles |

Key Questions Answered in the Report

What is the current size and growth outlook for the Brazil tire market?

The Brazil tire market size stood at USD 8.65 billion in 2025 and is projected to hit USD 10.04 billion by 2030, supported by a 3.03% CAGR.

Which tire segments are expanding the fastest in Brazil?

Winter tires, airless designs, above-20-inch rims, and battery-electric vehicle fitments each register highest CAGRs through 2030.

How are government policies influencing domestic tire production?

Tax incentives and financing under the Nova Indústria Brasil initiative motivate global and local manufacturers to build plants in Brazil, curbing reliance on imports.

What challenges does the Brazil tire market face?

Currency volatility, recycling infrastructure gaps, natural-rubber ESG scrutiny, and delayed EV tire regulations each place downward pressure on growth.

Page last updated on: