Nigeria Foodservice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

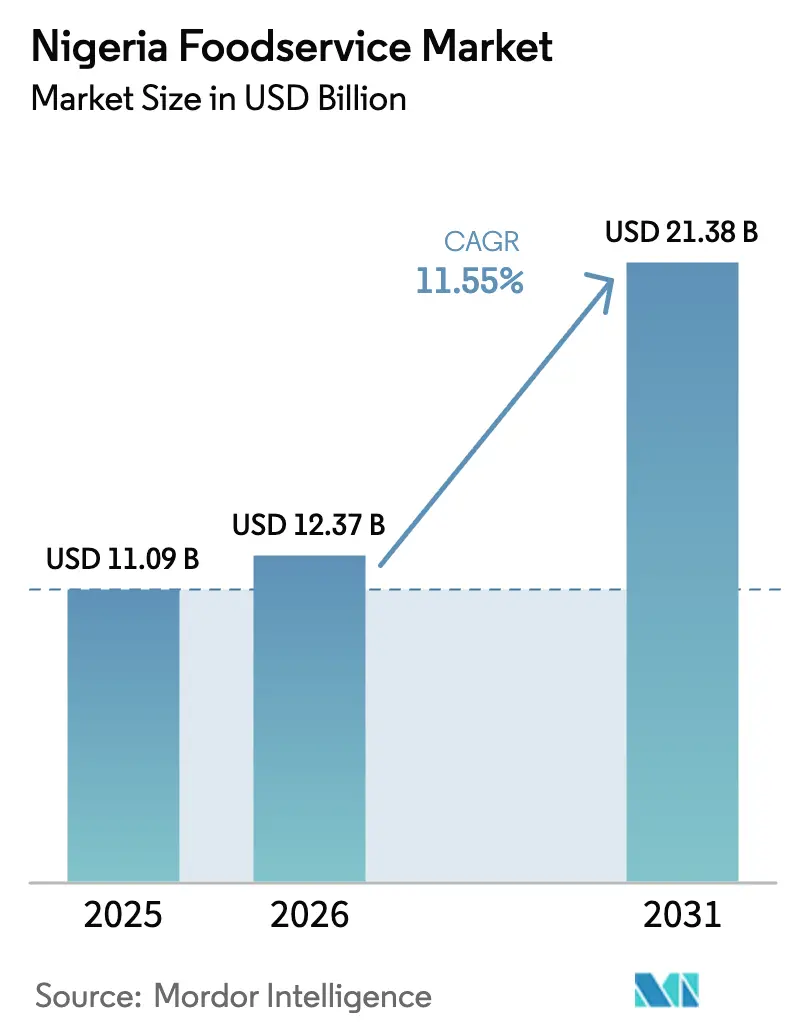

| Base Year Market Size (2025) | USD 11.09 Billion |

| Market Size (2026) | USD 12.37 Billion |

| Market Size (2031) | USD 21.38 Billion |

| Growth Rate (2026 - 2031) | 11.55% CAGR |

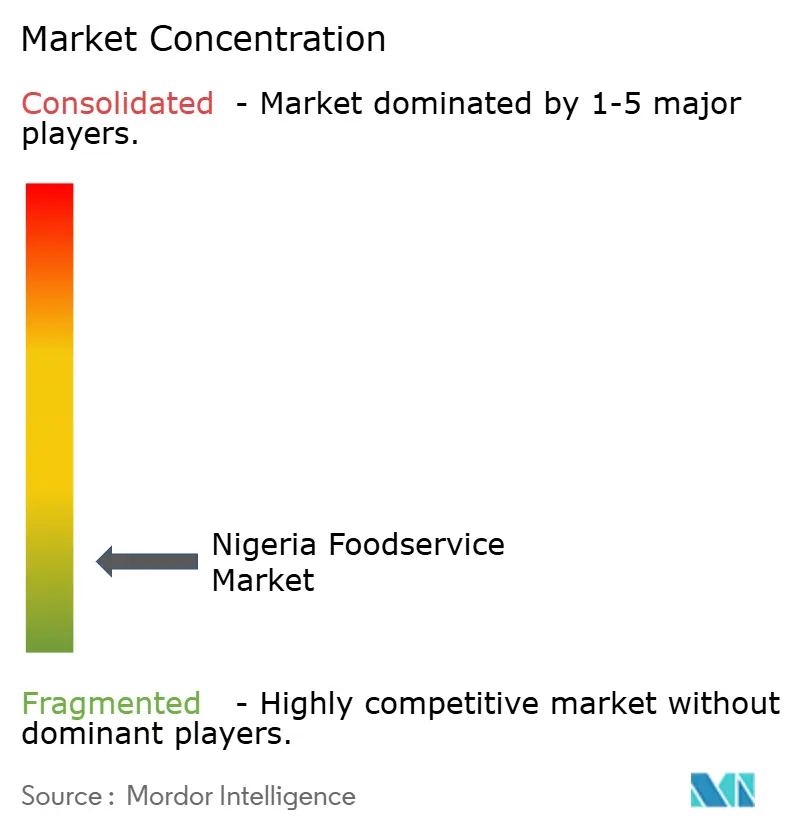

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nigeria Foodservice Market Analysis by Mordor Intelligence

The Nigerian foodservice market size is expected to grow from USD 11.09 billion in 2025 to USD 12.37 billion in 2026 and is forecast to reach USD 21.38 billion by 2031 at 11.55% CAGR over 2026-2031. The expansion is underpinned by a youthful population, a widening urban middle class, and rapid digital payment adoption that lowers transaction frictions. Quick Service Restaurants (QSRs) continue to drive volume growth, while cloud-kitchen formats leverage asset-light operations to tap into new demand opportunities. Retail mall openings in Lagos and Abuja supply premium real estate that drives higher ticket values, whereas airport modernizations multiply growth opportunities in travel hubs. Consolidation moves by well-capitalized chains hint at future efficiency gains, yet persistent double-digit food inflation and infrastructure gaps keep margins under pressure. Furthermore, Nigeria's foodservice industry is marked by a significant presence of independent outlets, alongside the regional growth of emerging chains such as Food Concepts PLC, Eat & Go Limited, and Sundry Foods Limited, which are utilizing digital platforms and delivery models.

Key Report Takeaways

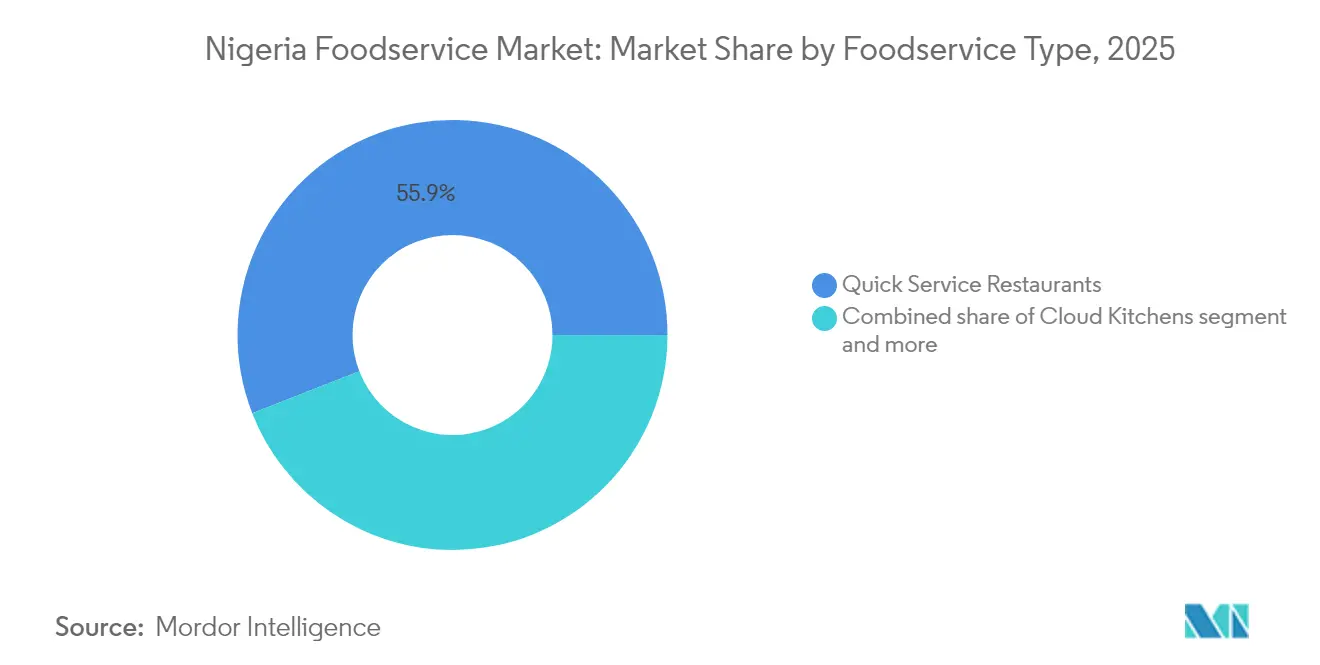

- By foodservice type, quick service restaurants led with 55.92% of the Nigerian foodservice market share in 2025; cloud kitchens are forecast to expand at a 12.05% CAGR through 2031.

- By outlet, independent outlets commanded a 70.62% share of the Nigerian foodservice market size in 2025; chained outlets are set to grow at a 12.96% CAGR through 2031.

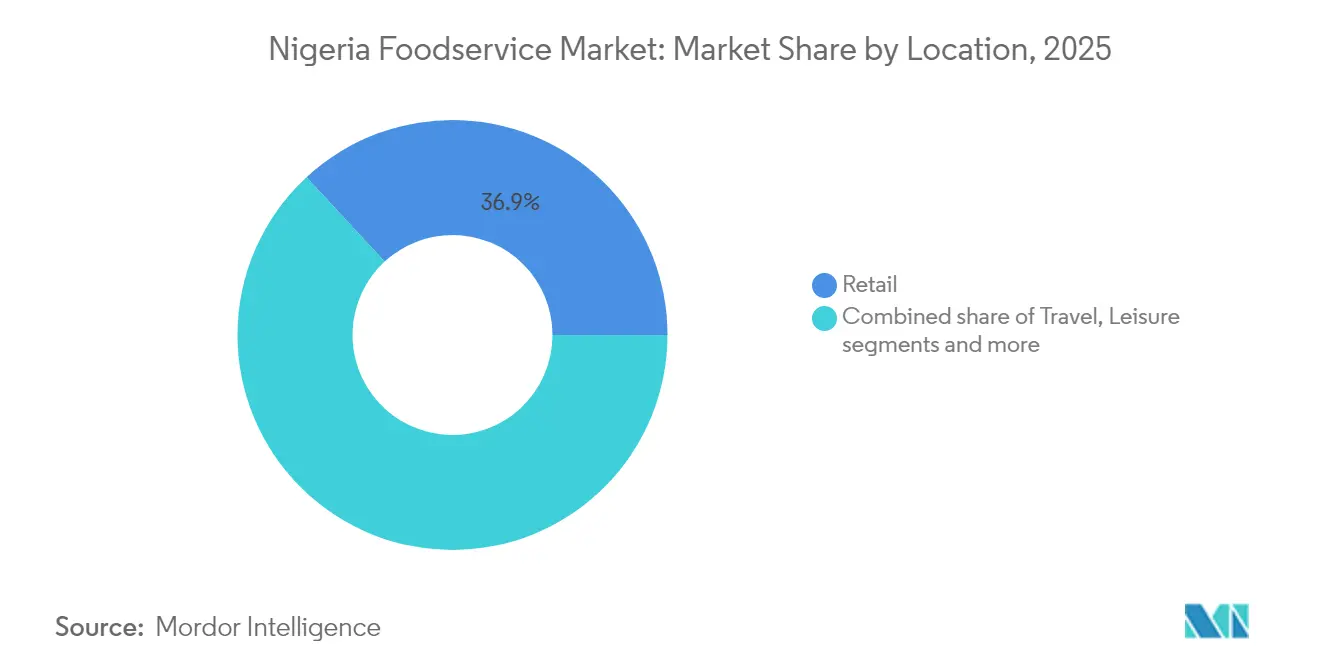

- By location, retail settings accounted for 36.88% of the Nigerian foodservice market size in 2025; travel locations are projected to post a 11.88% CAGR through 2031.

- By service type, dine-in represented 64.02% of the Nigerian foodservice market size in 2025; delivery services are expected to climb at a 12.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban middle-class expansion and rising discretionary spend | +1.8% | Lagos, Abuja, Port Harcourt, Kano metropolitan areas | Medium term (2-4 years) |

| Explosive growth of online delivery and cloud-kitchen models | +2.1% | National, concentrated in Lagos-Abuja corridor | Short term (≤ 2 years) |

| Rapid mall and retail-real-estate development in Lagos/Abuja | +1.4% | Lagos State, FCT Abuja, emerging in Port Harcourt | Medium term (2-4 years) |

| Government push for local food processing and backward integration | +1.2% | National, with early gains in SAPZ program states | Long term (≥ 4 years) |

| Power-as-a-service micro-grids lowering outlet OPEX | +0.9% | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Growing diaspora tourism driving premium dining formats | +0.8% | Lagos, Abuja, tourism destinations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban middle-class expansion and rising discretionary spend

Nigeria's urban middle class expansion accelerates foodservice demand as disposable income growth outpaces inflation in key metropolitan areas. Lagos State generated NGN 111.5 billion (USD 73 million) from tourism and hospitality activities during December 2024 alone, with hotels earning NGN 54 billion from over 15,000 bookings and achieving 90% occupancy rates during the Detty December phenomenon [1]Source: The "Good Tourism" Blog, "Detty December: The Rise of Diaspora Tourism in Nigeria", goodtourismblog.com. This seasonal surge demonstrates the purchasing power concentration among Nigeria's estimated 15 million middle-class consumers, who increasingly prioritize experiential spending over traditional goods consumption. The demographic shift toward urbanization creates sustainable demand pools, as Nigeria's urban population grows at 4.3% annually, significantly above the global average of 1.8%. Digital payment adoption among small and medium enterprises correlates with higher sales growth, indicating that middle-class consumers drive both volume and value expansion across foodservice categories. NAFDAC's food safety regulations increasingly influence consumer preferences, with middle-class segments demonstrating willingness to pay premiums for certified establishments that meet international hygiene standards.

Explosive growth of online delivery and cloud-kitchen models

Online food delivery platforms transform Nigeria's foodservice landscape through asset-light business models that bypass traditional real estate constraints. Mano expanded from grocery delivery into food delivery in July 2024, targeting a market segment valued at USD 936.5 million, while leveraging existing dark store infrastructure in Lagos and Abuja to achieve 40-minute fulfillment times. Chowdeck secured USD 2.5 million in seed funding to address Nigeria's notoriously challenging delivery market, focusing on supply-side restaurant onboarding and last-mile logistics optimization. The cloud kitchen model gains traction through companies like Chow Central by utilizing underused commercial kitchens across African cities. This approach reduces capital requirements compared to traditional restaurant formats while enabling rapid geographic expansion. Moreover, key cities such as Lagos, Abuja, and Port Harcourt are experiencing significant adoption of app-based ordering platforms integrated with digital payment systems. Cloud kitchens are transforming operations by allowing multiple brands to operate delivery-only outlets from shared facilities, reducing rental and service expenses. Local operators are adapting by offering multi-cuisine menus and forming rapid delivery partnerships to address changing consumer preferences.

Rapid mall and retail-real-estate development in Lagos/Abuja

Shopping mall proliferation in Nigeria's primary commercial centers creates premium foodservice real estate opportunities that command higher average order values and extended operating hours. Lagos and Abuja metropolitan areas account for over 70% of modern retail space development, with new shopping complexes integrating food courts as anchor tenants to drive foot traffic and extend visitor dwell times. For instance, in July 2024, Avolta secured a 10-year duty-free concession at Lagos Airport's new Terminal 2, opening a 400 square meter store that includes food and beverage offerings alongside beauty and liquor categories. The Federal Airports Authority's plan to develop 5 new terminals across Nigeria positions airport retail as a high-growth foodservice channel, particularly for international brands seeking to establish market presence. British Airways invested in a fully renovated 360 square meter lounge at Lagos Airport, featuring self-service dining areas with Nigerian classics and British-inspired dishes that rotate regularly. Retail location advantages include higher security levels, reliable power supply, and concentrated consumer traffic, factors that justify premium rental costs while delivering superior unit economics for foodservice operators.

Government push for local food processing and backward integration

Nigeria's government implements comprehensive policies to strengthen domestic food value chains, creating opportunities for foodservice operators to secure cost-effective, locally-sourced ingredients. The Special Agro-Industrial Processing Zones (SAPZ) program received USD 538.5 million in funding for Phase 1 implementation across 7 states plus the Federal Capital Territory, targeting 1.5 million households and 400,000 direct jobs in agricultural processing activities. The Nigeria First Policy prioritizes local manufacturing through zero duty rates on basic food items, including husked brown rice, grain sorghum, millet, maize, wheat, and beans, reducing input costs for foodservice operators who integrate backward into supply chain management. JBS signed a memorandum of understanding with the Nigerian government in November 2024 to invest USD 2.5 billion in 6 meat-processing plants, enhancing domestic protein supply capacity and reducing import dependency. The National Policy on Food Safety and Quality, launched on World Food Safety Day (June 7, 2024), establishes standardized frameworks that benefit larger foodservice chains capable of implementing compliance systems while creating barriers for informal operators. Regulatory influence from NAFDAC and the Standards Organisation of Nigeria increasingly shapes procurement decisions as foodservice operators seek certified suppliers to meet evolving consumer expectations for food safety and quality assurance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent double-digit food inflation compressing margins | -1.4% | National, most severe in northern states | Short term (≤ 2 years) |

| Chronic power and cold-chain gaps outside Tier-1 cities | -1.2% | Secondary cities, rural areas nationwide | Long term (≥ 4 years) |

| Foreign-exchange volatility hiking import-dependent input costs | -0.9% | National, affecting import-reliant operators | Medium term (2-4 years) |

| Rising insecurity in North-West disrupting supply chains | -0.7% | North-West states, spillover to Middle Belt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent double-digit food inflation compressing margins

Food inflation pressures create operational challenges for foodservice operators as input costs rise faster than menu price adjustments, compressing profit margins across all segments. Nigeria's food inflation reached 40.9% in 2024 (National Bureau of Statistics (NBS)), forcing operators to implement dynamic pricing strategies while managing consumer price sensitivity in a market [2]Source: The Nigerian Economic Summit Group, "Nigeria’s Inflation Rate Rose to a 28-year High in June 2024", nesgroup.org. Chicken Republic, Nigeria's largest fast-food chain with NGN 66.2 billion in sales during 2023, demonstrates how established players counter inflation through promotional campaigns and supply chain optimization. The poultry sector faces particular pressure from maize price volatility, with industry associations lobbying for import license approvals to stabilize feed costs that directly impact protein-based menu pricing. Fragmented market structure amplifies inflation impacts, as independent operators lack purchasing power to negotiate favorable supplier terms compared to chained outlets that leverage economies of scale. Consumer spending patterns shift toward value-oriented offerings, with quick service restaurants maintaining market share while full-service establishments experience traffic declines in price-sensitive demographic segments.

Chronic power and cold-chain gaps outside tier-1 cities

Chronic power shortages and insufficient cold-chain infrastructure continue to impede the growth of Nigeria’s foodservice market beyond tier-1 cities such as Lagos and Abuja. The lack of reliable electricity and refrigeration limits restaurant operations, food storage, and safe handling practices. ICE Commercial Power’s microgrid systems provide up to 35% energy savings for hospitality and retail businesses, enhancing cost efficiency in urban areas. Similarly, Alfen’s cacao factory microgrid has demonstrated a reduction in diesel consumption by over a million liters annually, showcasing scalable renewable energy models. ColdHubs has contributed to strengthening the cold chain with 58 solar-powered cold rooms and 10 refrigerated trucks, serving over 11,000 farmers and retailers while significantly reducing food spoilage. However, these innovations are largely concentrated in major cities, leaving secondary regions dependent on expensive diesel generators. This disparity increases operational costs for small foodservice operators and limits menu diversification that requires refrigeration. While the West Africa Centre for Crop Improvement and CGIAR are working on cold transport initiatives, a nationwide rollout is still years away. This infrastructural gap particularly impacts cold-dependent food categories such as dairy, frozen desserts, and fresh produce. As a result, power and logistics challenges remain critical structural barriers to the inclusive growth of Nigeria’s foodservice market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: QSR Dominance Meets Cloud Kitchen Innovation

Quick Service Restaurants command 55.92% market share in 2025, reflecting Nigerian consumers' preference for affordable, convenient dining options amid economic pressures and time constraints in urban environments. The segment's resilience stems from standardized operations that enable consistent quality and pricing, while local adaptations like Chicken Republic's Nigerian-inspired menu items create competitive differentiation against international franchises. Food Concepts PLC operates stores across West Africa, demonstrating the scalability potential for well-managed QSR chains that leverage technology for operational efficiency. The company's online delivery growth exceeded 140% year-over-year, indicating successful digital transformation initiatives that capture changing consumer behavior patterns. Full-service restaurants face margin compression from inflation and labor cost increases, while cafes and bars benefit from Nigeria's growing coffee culture and social dining trends among urban millennials and Gen Z consumers.

Cloud kitchens emerge as the fastest-growing segment at 12.05% CAGR through 2031, capitalizing on delivery platform proliferation and reduced real estate requirements that enable rapid market entry and geographic expansion. Technology integration becomes critical for cloud kitchen success, with real-time order tracking, inventory management, and coordination between central kitchens and fulfillment centers driving operational efficiency. The segment benefits from Nigeria's digital payment infrastructure improvements, including eNaira adoption and mobile wallet penetration exceeding 60% among informal enterprises, facilitating seamless transaction processing for delivery-only business models.

By Outlet: Independent Resilience Versus Chain Standardization

Independent outlets maintain 70.62% market share in 2025, reflecting Nigeria's entrepreneurial culture and consumers' preference for locally-adapted menu offerings that cater to regional taste preferences and cultural dining traditions. These establishments benefit from operational flexibility, enabling rapid menu adjustments based on ingredient availability and seasonal price fluctuations that larger chains struggle to implement across standardized operations. Independent operators often integrate vertically into food preparation and sourcing, reducing dependency on formal supply chains while building direct relationships with local farmers and suppliers. However, they face challenges in accessing formal financing, implementing technology solutions, and achieving economies of scale in procurement and marketing activities. The segment's resilience demonstrates that, during economic downturns, independent operators adjust pricing and portion sizes more dynamically than franchise-bound competitors constrained by corporate guidelines.

Chained outlets accelerate at 12.96% CAGR through 2031, driven by superior access to capital, technology infrastructure, and standardized operational processes that deliver consistent customer experiences across multiple locations. Food Concepts PLC's partnership with ACA Private Equity, which acquired a 31% stake, exemplifies how chains leverage external investment to fund expansion and technology upgrades. Burger King's opening of its 16th Nigerian outlet at Murtala Muhammed Airport 2 demonstrates international chains' strategic focus on high-traffic locations that justify premium rental costs through superior customer throughput. Chained outlets increasingly adopt digital ordering systems, loyalty programs, and data analytics capabilities that enable personalized marketing and operational optimization. The segment benefits from brand recognition and marketing scale economies, while standardized training programs ensure service quality consistency that builds consumer trust and repeat business patterns across diverse geographic markets.

By Location: Retail Concentration Drives Travel Segment Growth

Retail locations capture 36.88% market share in 2025, benefiting from concentrated foot traffic, extended operating hours, and integrated shopping experiences that encourage impulse dining decisions and higher average order values. Shopping malls provide controlled environments with reliable power supply, security systems, and parking facilities that address key infrastructure challenges facing standalone foodservice establishments in Nigeria's urban centers. The location type particularly suits international franchise concepts that require standardized store formats and operational consistency, while food courts enable smaller operators to access premium real estate through shared facilities and reduced individual rental costs. Retail integration creates cross-selling opportunities, with foodservice operators partnering with retailers for promotional campaigns and customer loyalty programs that drive mutual traffic generation. However, retail locations face higher rental costs and revenue-sharing arrangements that pressure profit margins, requiring operators to achieve superior sales performance to justify location premiums.

Travel locations are projected to be the fastest-growing segment, with a CAGR of 11.88% through 2031. This growth is attributed to the recovery of Nigeria's tourism and aviation sectors, along with infrastructure modernization initiatives aimed at improving passenger experience and reducing dwell times. The Federal Airports Authority's plan to develop new terminals across Nigeria creates expansion opportunities for foodservice operators seeking to establish a presence in high-value customer segments with limited competitive intensity. Travel locations command higher menu pricing due to captive customer bases and limited competitive alternatives, while international passenger traffic drives demand for diverse cuisine options and extended service hours. The resumption of in-flight catering services on domestic and international flights, announced by the Minister of Aviation, creates additional revenue streams for travel-based foodservice operators. Regulatory compliance requirements from the Nigerian Civil Aviation Authority ensure operational standards that benefit established operators while creating entry barriers for informal competitors.

By Service Type: Dine-in Tradition Meets Delivery Innovation

Dine-in service maintains 64.02% market share in 2025, reflecting Nigerian cultural preferences for communal dining experiences and social interaction that remain central to food consumption patterns across urban and rural markets. The service type benefits from higher average order values through beverage sales, appetizer additions, and extended meal durations that increase per-customer revenue compared to takeaway alternatives. Nigerian consumers particularly value dine-in experiences for special occasions, business meetings, and family gatherings, creating predictable demand patterns that enable operators to optimize staffing and inventory management. However, dine-in operations require higher labor costs, larger physical footprints, and extended service hours that increase operational complexity and fixed cost structures. The segment faces pressure from inflation-conscious consumers who increasingly seek value-oriented offerings and shorter meal durations to manage discretionary spending.

Nigeria's urban population, which reached 55% in 2024 according to the World Bank, is driving the growing adoption of delivery services . Urban congestion and demanding lifestyles are increasing the appeal of home-delivered meals among city residents. This trend underpins the segment's projected compound annual growth rate (CAGR) of 12.34% through 2031, highlighting the impact of urbanization and digital convenience on Nigeria's foodservice market. Delivery platforms like Chowdeck raised USD 2.5 million in 2024 to address Nigeria's challenging logistics environment through localized solutions that solve last-mile delivery constraints and merchant onboarding difficulties. The service type particularly benefits cloud kitchen operators who optimize operations for delivery efficiency without maintaining customer-facing spaces or dine-in service capabilities. Mobile wallet penetration among informal enterprises creates a payment infrastructure that supports delivery service expansion beyond traditional banking customer segments, enabling operators to access previously underserved market demographics through digital payment solutions.

Geography Analysis

Nigeria's foodservice market is heavily concentrated in the Lagos-Abuja corridor. Lagos State generated NGN 111.5 billion (USD 73 million) from tourism and hospitality in December 2024, driven by events like Detty December that attract diaspora visitors. Superior infrastructure, higher disposable incomes, and robust supply chain networks support this concentration, while Abuja's role as the federal capital fuels demand from government officials, diplomatic missions, and business travelers. However, this geographic focus exposes the market to localized economic shocks and limits expansion opportunities in other states, where infrastructure and purchasing power remain challenges.

Port Harcourt ranks as the third-largest foodservice market, benefiting from its oil industry base and international business activities that drive demand for diverse cuisines and extended service hours. The city's affluent customer base, supported by the presence of international oil companies, creates opportunities for Western-style dining and corporate catering services. Secondary cities like Kano, Ibadan, and Kaduna show growth potential due to urbanization and an expanding middle class, but infrastructure issues, including unreliable power supply and limited cold-chain logistics, hinder operational efficiency. The Federal Airports Authority's plan to develop new terminals across Nigeria offers prospects for travel-based foodservice growth, particularly in cities with increasing aviation traffic.

Northern Nigeria faces significant challenges from security issues, with banditry incidents rising, disrupting supply chains and agricultural production. This instability impacts the availability and cost of protein-based ingredients, posing challenges for foodservice operators. Despite these issues, the region's large population and growing urban centers present long-term opportunities as security improves and infrastructure develops. The USD 538.5 million Special Agro-Industrial Processing Zones (SAPZ) program, spanning seven states and the Federal Capital Territory, aims to strengthen agricultural value chains, potentially reducing transportation costs and improving ingredient sourcing for foodservice operators.

Competitive Landscape

Nigeria's foodservice market is highly fragmented, offering significant acquisition opportunities for well-capitalized players. This fragmentation reflects the country's entrepreneurial culture and low entry barriers for small-scale operators, but also highlights inefficiencies that technology-driven chains are addressing through advanced supply chain management and customer data analytics. Recent consolidation efforts, such as Tantalizers' acquisition by former banking executives in 2024 and Food Concepts PLC's partnership with ACA Private Equity, demonstrate how financial expertise and external capital are being leveraged for operational optimization and technological upgrades. Key players like Food Concepts PLC, Eat & Go Limited, and United Africa Company PLC focus on brand recognition, standardized operations, and technology adoption to deliver consistent customer experiences across multiple locations.

Adopting technology is becoming a critical factor for competitiveness in Nigeria's foodservice industry, enabling efficient transactions and improved customer engagement. The introduction of eNaira, Africa's first Central Bank Digital Currency, represents a shift toward a cashless economy, facilitating faster and more transparent payment processes. Foodservice operators who implement digital payment solutions early can attract technology-focused consumers and enhance delivery operations. The increasing use of mobile wallets, adopted by over 60% of informal enterprises, expands digital access for unbanked populations. This development allows small eateries and street vendors to participate in online ordering and delivery platforms. As payment systems advance, technology integration will increasingly influence operational efficiency and customer loyalty in Nigeria's foodservice market.

White-space opportunities are emerging in secondary cities, driven by infrastructure improvements and a growing middle class, which increases demand for standardized foodservice offerings. Regulatory compliance requirements from NAFDAC are also reshaping the competitive landscape, favoring operators with formal business structures and quality management systems over informal competitors. These trends indicate that players who adopt technology, ensure regulatory compliance, and expand into underserved regions are well-positioned to capitalize on the market's growth potential.

Nigeria Foodservice Industry Leaders

-

Eat & Go Limited

-

Food Concepts PLC

-

Sundry Foods Limited

-

United Africa Company PLC

-

Tantalizers PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Burger King Nigeria has made a historic leap in the fast-food sector by inaugurating Africa’s first shipping container drive-thru restaurant. This innovative establishment, situated on Toyin Street, marks a significant milestone for the brand, becoming its 21st outlet in Nigeria and providing customers with a unique and convenient dining experience.

- September 2024: Burger King opened its 16th Nigerian outlet at Murtala Muhammed Airport 2 (MMA2) in Lagos, strategically targeting travelers and expanding its presence in high-traffic transportation hubs

- April 2024: Sundry Foods Limited (SFL), a leading food services company in Nigeria, has announced the expansion of its flagship Kilimanjaro Restaurant with the launch of six new restaurants across Nigeria.

Nigeria Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.| Cafes and Bars | Bars and Pubs |

| Cafes | |

| Juice/Smoothie/Desserts Bars | |

| Specialist Coffee and Tea Shops | |

| Cloud Kitchen | |

| Full Service Restaurants | Asian |

| European | |

| Latin American | |

| Middle Eastern | |

| North American | |

| Other FSR Cuisines | |

| Quick Service Restaurants | Bakeries |

| Burger | |

| Ice Cream | |

| Meat-based Cuisines | |

| Pizza | |

| Other QSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Cafes and Bars | Bars and Pubs |

| Cafes | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | Asian | |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | Bakeries | |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines | ||

| By Outlet | Chained Outlets | |

| Independent Outlets | ||

| By Location | Leisure | |

| Lodging | ||

| Retail | ||

| Standalone | ||

| Travel | ||

| By Service Type | Dine-in | |

| Takeaway | ||

| Delivery | ||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms