Malaysia Foodservice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

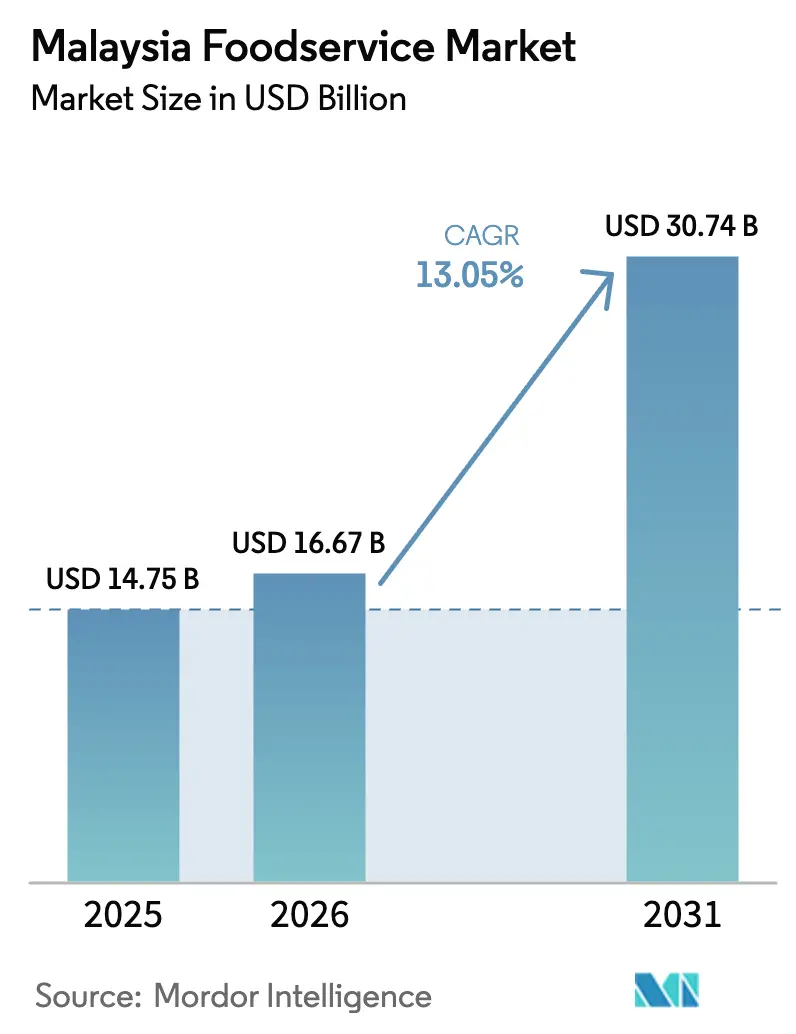

| Base Year Market Size (2025) | USD 14.75 Billion |

| Market Size (2026) | USD 16.67 Billion |

| Market Size (2031) | USD 30.74 Billion |

| Growth Rate (2026 - 2031) | 13.05% CAGR |

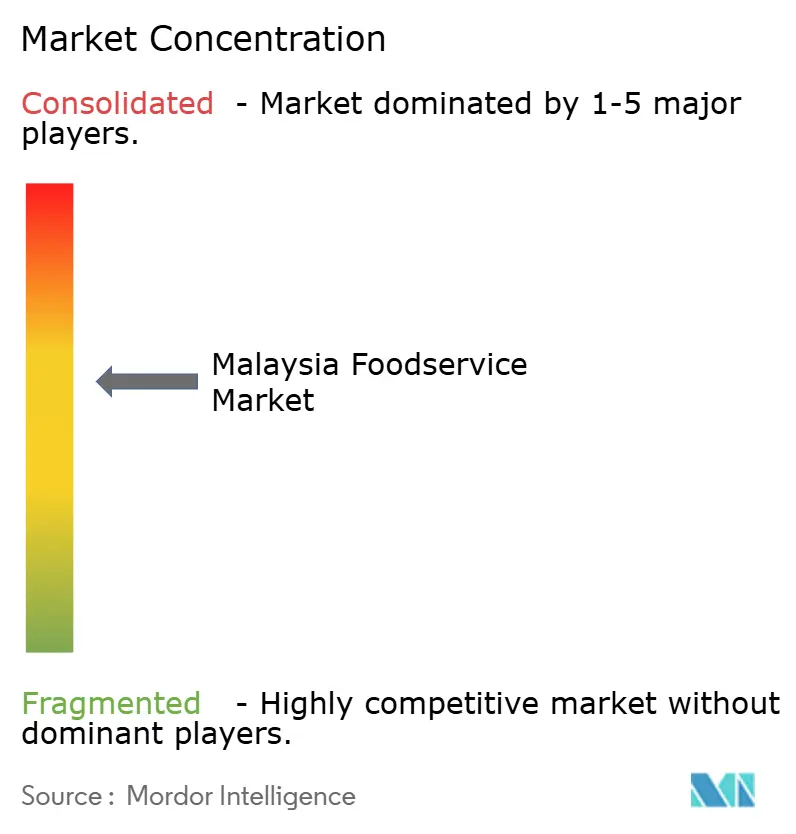

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Foodservice Market Analysis by Mordor Intelligence

The Malaysia foodservice market size was valued at USD 14.75 billion in 2025 and estimated to grow from USD 16.67 billion in 2026 to reach USD 30.74 billion by 2031, at a CAGR of 13.05% during the forecast period (2026-2031). The market expansion is primarily attributed to the rising purchasing power of Malaysian consumers, consistent economic growth reflected in the country's GDP performance in 2025, and the population's increasing adoption of digital technologies. The foodservice industry's growth trajectory is supported by the widespread integration of mobile ordering applications, continuous improvements in restaurant infrastructure, and favorable government policies that benefit both established restaurant chains and small independent food businesses. Traditional full-service restaurants continue to hold significant cultural importance in the Malaysian dining landscape. However, the market is experiencing a transformation with the introduction of cloud kitchens, virtual restaurant brands, and delivery-optimized business models. The industry's potential is further validated by substantial investment commitments exceeding USD 1 billion from international quick-service restaurant chains and prominent local operators, demonstrating strong market confidence despite existing regulatory challenges.

Key Report Takeaways

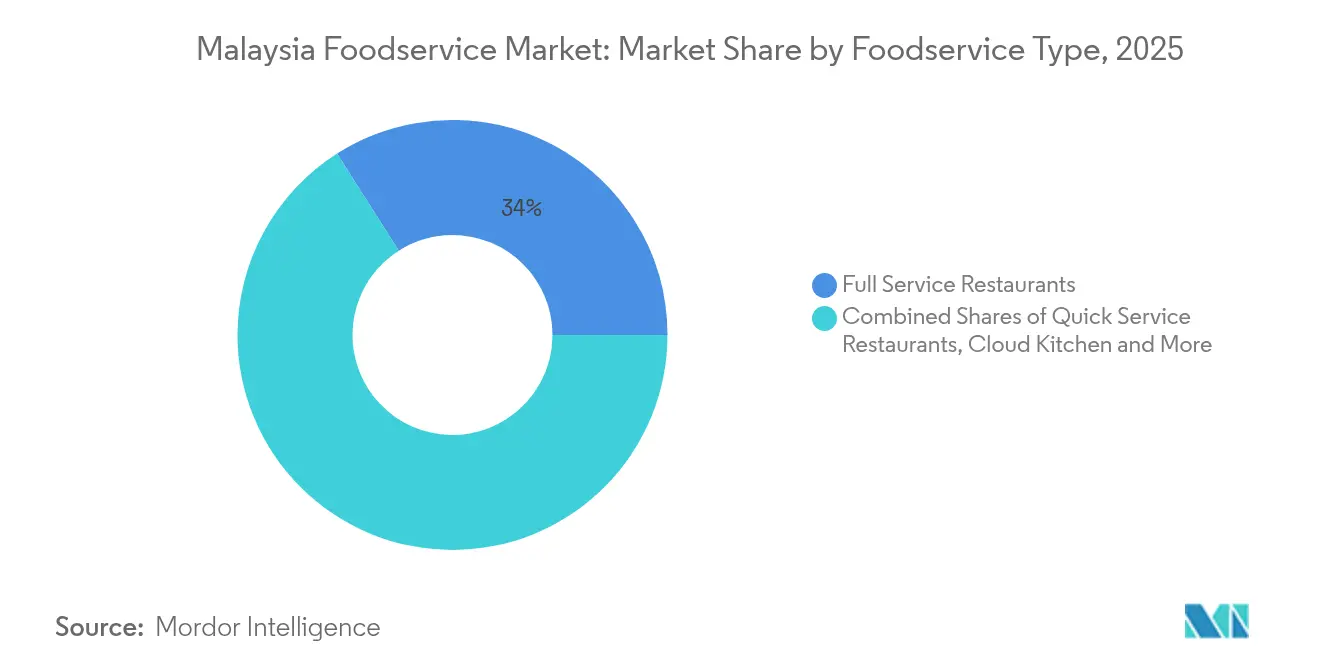

- By foodservice type, full service restaurants led with 34.02% revenue share in 2025; cloud kitchens are forecast to expand at a 15.88% CAGR through 2031.

- By outlet, independent operators held 73.52% of the Malaysia foodservice market share in 2025, while chained outlets record the highest projected CAGR at 12.98% to 2031.

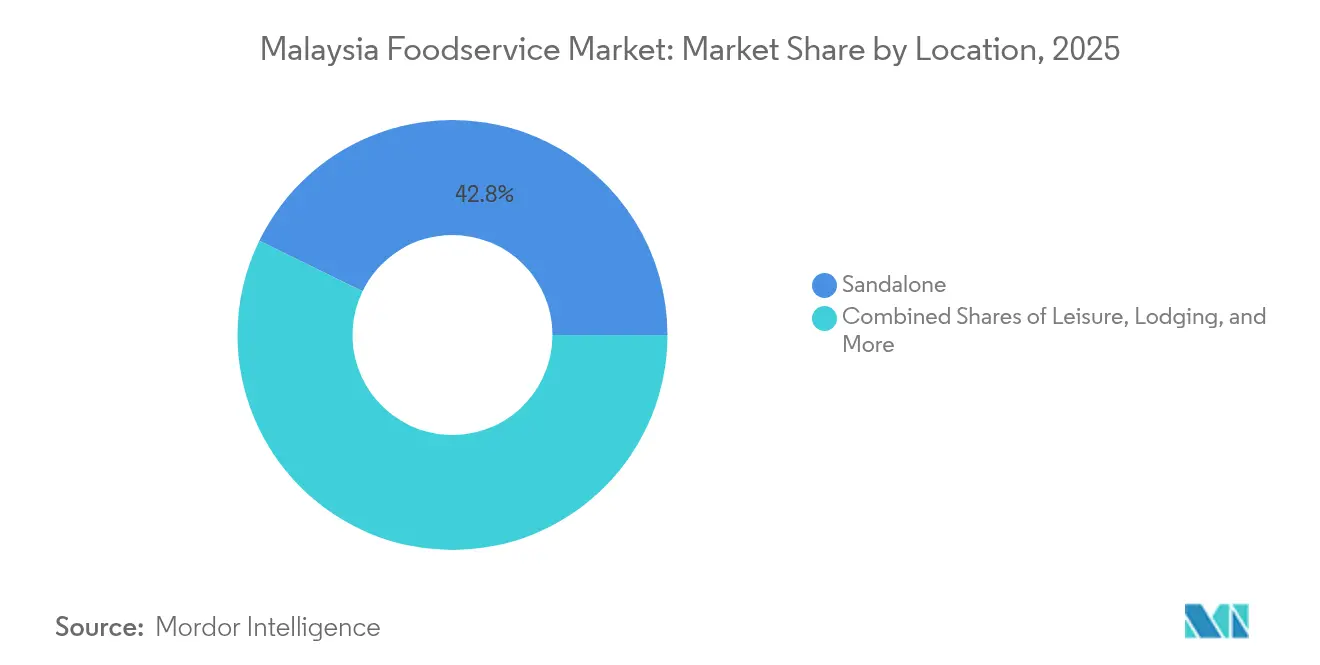

- By location, standalone venues accounted for 42.78% of the Malaysia foodservice market size in 2025; travel locations advance at a 15.97% CAGR through 2031.

- By service, dine-in commanded 63.55% share of the Malaysia foodservice market in 2025; delivery services are set to grow at a 15.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion and modernization of urban infrastructure | +2.1% | Klang Valley, Penang, Johor Bahru with spillover to secondary cities | Medium term (2-4 years) |

| Rapid digitization and mobile app adoption for ordering | +2.8% | National, with early gains in Kuala Lumpur, Selangor, Penang | Short term (≤ 2 years) |

| Rise of cloud kitchens and virtual-only brands | +2.3% | Urban centers nationally, concentrated in Klang Valley | Short term (≤ 2 years) |

| Increasing consumer preference for convenience and ready-to-eat food | +1.9% | National, stronger in urban and suburban markets | Medium term (2-4 years) |

| Strong coffee and café culture | +1.4% | National, with premium segments in major cities | Long term (≥ 4 years) |

| Expansion of quick-service and fast-casual restaurant chains | +2.2% | National, with focus on shopping malls and transport hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion and Modernization of Urban Infrastructure

Malaysia's extensive infrastructure modernization initiatives are creating significant opportunities for foodservice market expansion through the development of commercial real estate properties and improved transportation networks. The ongoing Pan Borneo Highway project and substantial data center developments in Johor have resulted in a notable 14.6% increase in construction employment during H1 2024, which has directly benefited local foodservice establishments operating near these project sites [1]Source: Asian Development Bank, “Southeast Asia (Asian Development Outlook – September 2024),” adb.org. The development of modern shopping malls and integrated commercial projects such as PMINT Square continues to provide premium locations for foodservice operators, while enhanced transportation infrastructure has significantly reduced delivery times and enabled businesses to serve broader geographical areas. The expansion of airport terminals at KLIA, Penang International Airport, and various regional facilities presents valuable concession opportunities for foodservice businesses, supported by Malaysia Airports Holdings' substantial investment of RM10 billion allocated over a five-year period for infrastructure improvements. This continuous cycle of infrastructure investment generates sustained foodservice demand through two key phases: initial consumption during the construction period and subsequent long-term commercial activities within the newly developed spaces.

Rapid Digitization and Mobile App Adoption for Ordering

Digital ordering platforms have fundamentally transformed Malaysia's foodservice consumption patterns, demonstrating significant impact on business operations and consumer behavior. QSR Brands exemplifies this transformation, recording a substantial 25% revenue growth in 2024, driven by strategic digital initiatives including customer-friendly self-ordering kiosks and mobile applications. Multi-sided platforms create valuable network effects that deliver mutual benefits to restaurants and consumers, resulting in reduced transaction costs and enhanced order accuracy. These platforms also leverage sophisticated data analytics to deliver personalized marketing campaigns and optimize inventory management systems. The Malaysian government's implementation of the e-invoicing mandate in August 2024 has accelerated digital payment adoption throughout the foodservice sector, with notable uptake among small and medium enterprises [2]Source: International Monetary Fund, “Malaysia: 2025 Article IV Consultation-Press Release; and Staff Report,” elibrary.imf.org. Modern cloud-based point-of-sale systems and integrated delivery management platforms have leveled the playing field, enabling independent operators to effectively compete with established restaurant chains. Recent consumer research reveals a strong preference for digital ordering methods among urban populations, with bubble tea and fried chicken consistently ranking as the most frequently ordered items through online delivery services.

Rise of Cloud Kitchens and Virtual-Only Brands

Cloud kitchens are transforming the foodservice industry by offering a cost-efficient operational model focused on delivery services. This innovative approach enables business operators to reach profitability 40-60% faster than conventional restaurants by significantly reducing expenses associated with dining areas and service staff. Established restaurants can leverage this model to explore diverse culinary offerings through virtual brands, creating new revenue streams without disrupting their primary business operations. The shared kitchen infrastructure presents an accessible pathway for food entrepreneurs to enter the market with minimal initial investment. ZUS Coffee illustrates the practical application of this business model by strategically combining traditional storefronts with cloud kitchen operations, enabling efficient market expansion while maintaining cost control. This operational framework has proven particularly beneficial for businesses specializing in ethnic cuisines and dietary-specific offerings, which might otherwise struggle with the economics of traditional restaurant setups. In response to this evolution in food service, local regulatory bodies are implementing tailored frameworks, including streamlined licensing processes, specifically designed to accommodate these delivery-focused operations.

Increasing Consumer Preference for Convenience and Ready-to-Eat Food

Malaysian consumers are increasingly shifting their preferences toward convenience-focused dining solutions, primarily influenced by rapid urbanization, extended working hours, and the growing prevalence of dual-income households. The ready-to-eat meal segment has experienced significant growth as convenience stores and supermarkets strategically expand their prepared food offerings to address the demand traditionally fulfilled by restaurants. This transformation is particularly evident among the younger generation of consumers, who now view food delivery services as an essential part of their daily routines rather than a luxury option, contributing to substantial growth in delivery-oriented business models. The current economic environment, characterized by increasing cost-of-living pressures, has further reinforced this trend, as consumers actively seek value-driven convenience options instead of traditional premium dining experiences. Technological advancements in packaging solutions and enhanced food safety protocols have enabled extended shelf life and superior portability of ready-to-eat products, facilitating expansion into distribution channels beyond conventional foodservice establishments. This evolving market dynamic has encouraged existing restaurants to incorporate grab-and-go formats, generating supplementary revenue streams without necessitating substantial operational modifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain fragility and ingredient sourcing challenges | -1.8% | National, with greater impact on import-dependent operators | Short term (≤ 2 years) |

| Pressure from multinational and domestic chains on smaller operators | -1.2% | Urban centers and shopping mall locations | Medium term (2-4 years) |

| Quality consistency issues and lack of standardized operating procedures among independents | -0.9% | National, concentrated among independent operators | Long term (≥ 4 years) |

| Frequent policy/tax changes on food and beverage products | -1.1% | National, with varying regional implementation | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply Chain Fragility and Ingredient Sourcing Challenges

The Malaysian foodservice sector continues to grapple with significant supply chain challenges that affect daily operations and business sustainability. Restaurant operators, cafes, and food establishments face persistent difficulties in maintaining reliable access to imported ingredients and specialized products essential for their menus. The Malaysia Competition Commission's 2024 market review revealed concerning concentration risks within food supply networks, where any disruption at major distribution centers creates a ripple effect across numerous food businesses. The heavy dependence on imported premium ingredients makes these businesses particularly vulnerable to currency market movements, as fluctuations in the ringgit's value against major currencies directly impact their operational costs and pricing strategies. The mandatory halal certification process adds another layer of complexity to procurement decisions, requiring operators to conduct thorough compliance checks throughout their supply networks, which ultimately narrows their supplier options and increases overall procurement expenses [3]Source: Department of Islamic Development Malaysia, “Halal Certification Overview,” halal.gov.my. Small restaurants and independent food operators find themselves at a particular disadvantage, lacking the necessary scale to negotiate effectively with suppliers, which results in them paying premium prices for ingredients and facing more stringent payment conditions compared to larger restaurant chains. The situation is further complicated by unpredictable climate-related disruptions and ongoing geopolitical tensions, forcing food businesses to either maintain costly higher inventory levels or accept reduced profit margins when seeking alternative supply sources.

Pressure from Multinational and Domestic Chains on Smaller Operators

Large restaurant chains consistently outperform independent establishments by maximizing their economies of scale, implementing well-defined operational processes, and utilizing comprehensive marketing resources. In the battle for prime locations, shopping mall developers naturally gravitate towards established brands with robust financial foundations, which significantly restricts expansion possibilities for independent restaurants. The algorithmic nature of food delivery platforms tends to favor establishments with substantial order volumes and positive customer ratings, creating a cycle of success for larger operators who possess the financial capability to invest in sophisticated customer acquisition and retention strategies. Independent restaurant owners face an uphill battle in achieving comparable operational efficiencies and maintaining competitive cost structures while upholding their quality standards. These intense market pressures frequently result in independent operators having to make difficult business decisions - either aligning themselves with established franchise systems or ultimately closing their operations, which contributes to the ongoing consolidation within the restaurant industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Drive Digital Transformation

The Malaysian foodservice market is experiencing a significant transformation, with cloud kitchens emerging as a key growth driver at a CAGR of 15.88% through 2031. These delivery-focused operations are changing how food businesses operate by implementing optimized processes and virtual brand strategies, while benefiting from lower costs and faster scaling abilities. Full-service restaurants continue to lead the market with a 34.02% share in 2025, building on Malaysia's rich dining culture, even as they adapt to new consumer behaviors.

Quick-service restaurants are strengthening their presence through franchise models and shopping mall locations, while cafes and bars are flourishing due to Malaysia's growing appreciation for coffee culture, particularly in specialty coffee shops and bubble tea establishments. The industry's digital evolution enables operators to launch virtual-only brands and test new concepts without traditional restaurant investments. This transformation is exemplified by TamJai International's market entry through Hextar Retail partnership, showing how international brands can successfully navigate Malaysia's market by working with local partners to meet regulatory requirements and consumer preferences.

By Outlet: Independent Operators Face Consolidation Pressure

The Malaysian foodservice landscape continues to be dominated by independent outlets, which currently command a substantial 73.52% market share in 2025. These establishments embody the entrepreneurial spirit of local food businesses and cater to Malaysia's diverse culinary preferences. However, they are experiencing heightened pressure from chain operations, which are making significant inroads with a robust 12.98% CAGR. This growth is fueled by their strong financial backing, well-established operational systems, and the ability to leverage economies of scale for competitive pricing and service consistency.

While independent operators maintain their stronghold through authentic local cuisine and deep community connections, particularly in residential areas and traditional markets, they face mounting challenges. The market is witnessing a notable shift as consumers increasingly gravitate toward standardized experiences and digital integration capabilities. This trend favors larger operators who possess the resources for technological investments. Additionally, independent operators must navigate the complexities of regulatory compliance, including halal certification and food safety standards, often with limited resources compared to their chain counterparts.

By Locations: Travel Segments Lead Recovery

Malaysia's tourism recovery and strategic airport infrastructure investments are fueling significant growth in travel location foodservice, with an expected CAGR of 15.97% through 2031. The country welcomed 11.8 million tourists in H1 2024, achieving a 28.9% year-over-year increase, while the government aims to attract 27.3 million visitors in 2024. This growth in tourism continues to strengthen travel-related foodservice demand, as demonstrated by Plaza Premium Group's expansion of Flight Club dining at KLIA Terminal 1, which effectively leverages passenger traffic and extended waiting times.

The foodservice market remains dominated by standalone locations, which account for 42.78% of the market share in 2025. This dominance reflects Malaysia's suburban growth and automobile-focused infrastructure, which makes accessible, parking-friendly locations essential. The market sees additional growth through retail locations in expanding shopping malls and lifestyle centers, while lodging locations benefit from improving hotel occupancy and renewed business travel. Leisure locations continue to thrive by serving domestic tourists and recreational consumers.

By Service Type: Delivery Transforms Consumer Behavior

The delivery services segment continues to expand at a 15.76% CAGR, as consumers increasingly rely on this channel for their food needs. This transformation is particularly evident among urban millennials and dual-income households, who have embraced delivery as their primary ordering method. The market's evolution reflects changing consumer behavior, supported by more sophisticated digital platforms, better logistics networks, and a growing acceptance of delivery fees in exchange for time savings.

Dine-in services remain the market leader, holding a 63.55% share in 2025, as Malaysian consumers value the social aspects of restaurant dining and the overall experience of ambiance and service. Meanwhile, takeaway services occupy a strategic position between delivery and dine-in, offering cost-effective convenience without delivery charges while maintaining personal restaurant interactions. This service distribution highlights how different consumer groups prioritize their needs - with delivery serving time-conscious customers, dine-in catering to experience-seekers, and takeaway appealing to value-oriented consumers.

Geography Analysis

The foodservice landscape in Malaysia shows a clear concentration in three major regions - Klang Valley, Penang, and Johor Bahru - which together make up 59.75% of the market value in 2025. These regions thrive due to their dense populations, higher consumer spending power, and strong tourism appeal. The Klang Valley stands out as the market leader, hosting numerous international restaurant chains, upscale dining venues, and innovative food concepts, thanks to its strategic location near Malaysia's primary airport and business districts. Penang's rich culinary heritage and UNESCO World Heritage status fuel its tourism-driven food scene, while Johor Bahru benefits from Singapore's spillover dining traffic and a growing expatriate community drawn by its expanding data center industry.

Beyond the main urban centers, cities such as Kota Kinabalu, Kuching, and Ipoh are experiencing notable growth in their foodservice sectors, driven by better infrastructure and ongoing regional development. In East Malaysia, Sabah and Sarawak offer unique opportunities with their focus on local food traditions and independent businesses, attracting increasing interest from international restaurant chains. While traditional eating establishments like coffee shops, hawker centers, and family restaurants remain popular in rural and semi-urban areas, they are gradually adopting modern conveniences through digital payments and food delivery services.

The government's investment in major infrastructure projects, such as the Pan Borneo Highway and various airport expansions, is creating new opportunities for both established food businesses and local entrepreneurs. This expansion mirrors Malaysia's broader economic growth strategy, where food businesses follow the path of infrastructure development and urban growth. Food operators must carefully consider local tastes, regulations, and market competition when expanding their presence while ensuring efficient management across their restaurant networks.

Competitive Landscape

The Malaysian foodservice industry features a balanced mix of established businesses and new market entrants, creating a dynamic competitive environment. Traditional businesses that relied on prime locations and brand recognition now find themselves adapting as digital-first companies and delivery-focused operators reshape market expectations. International chains, despite their operational strengths and marketing resources, are experiencing increased pressure from local brands that understand Malaysian consumers and navigate regulatory requirements more effectively.

Companies are gaining competitive advantages through strategic technology investments in digital ordering platforms, customer management systems, and data analytics tools. These investments help businesses improve their marketing precision and operational efficiency. The recent RM250 million investment in ZUS Coffee demonstrates the market's confidence in local companies that combine technological capabilities with deep market understanding to challenge established international brands.

Companies that succeed in this market consistently deliver quality food, convenient access, and competitive prices across multiple customer touchpoints. The regulatory environment, particularly regarding halal certification, provides additional competitive advantages to businesses that have established certification processes and reliable supply chain relationships.

Malaysia Foodservice Industry Leaders

Gerbang Alaf Restaurants Sdn Bhd

Berjaya Starbucks Coffee Company Sdn Bhd

Domino’s Pizza Enterprises Ltd

Marrybrown Sdn Bhd

Secret Recipe Cakes & Café Sdn Bhd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: ZUS Coffee secured RM250 million investment from consortium including KV Asia Capital, KWAP, and Indonesia's Kapal Api Group to accelerate regional expansion into Singapore, Brunei, and additional Southeast Asian markets. The funding supports the company's growth from 18 stores in 2020 to approximately 600 stores regionally by 2024, demonstrating the scalability of tech-enabled coffee chains in Malaysia's competitive market.

- September 2024: ZUS Coffee secured RM250 million investment from consortium including KV Asia Capital, KWAP, and Indonesia's Kapal Api Group to accelerate regional expansion into Singapore, Brunei, and additional Southeast Asian markets. The funding supports the company's growth from 18 stores in 2020 to approximately 600 stores regionally by 2024, demonstrating the scalability of tech-enabled coffee chains in Malaysia's competitive market.

- August 2024: TamJai International entered Malaysia through strategic partnership with Hextar Retail, planning first restaurant in Kuala Lumpur by Q1 2025. The partnership leverages Hextar's local market expertise and existing mall relationships to establish the Hong Kong-based noodle chain in Malaysia's competitive fast-casual segment.

Malaysia Foodservice Market Report Scope

| Café and Bars | By Cuisine | Bars & Pubs |

| Café | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Sandalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Café and Bars | By Cuisine | Bars & Pubs |

| Café | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Locations | Leisure | ||

| Lodging | |||

| Retail | |||

| Sandalone | |||

| Travel | |||

| By Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms