Egypt Foodservice Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

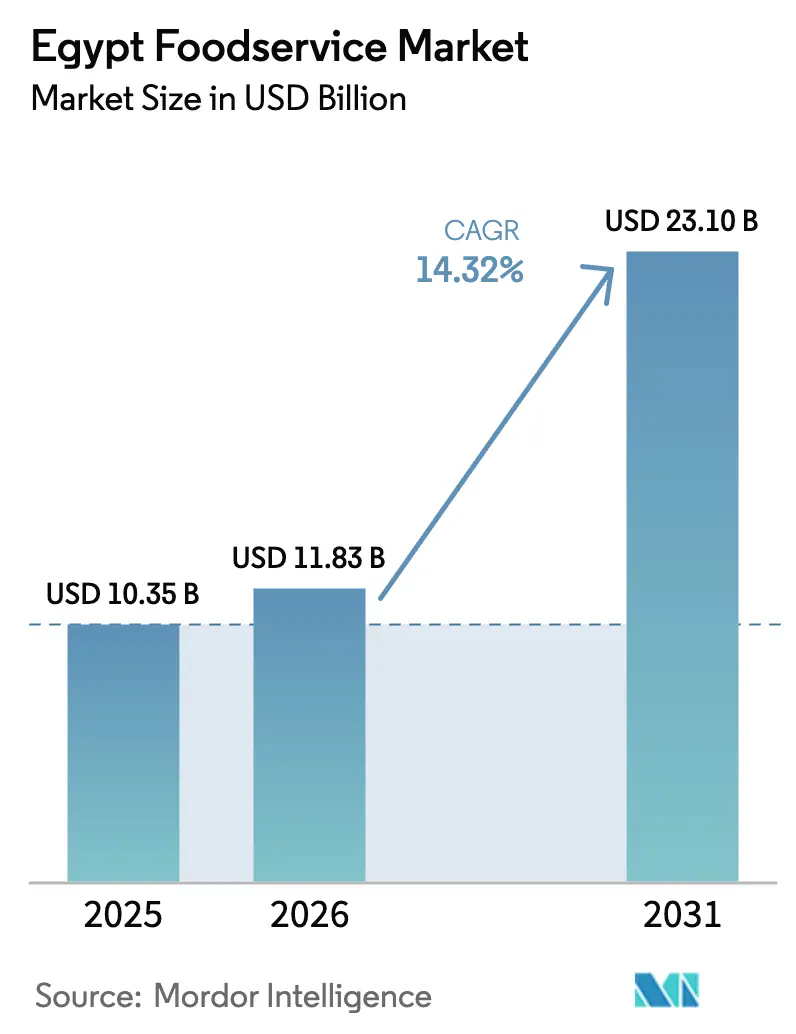

| Base Year Market Size (2025) | USD 10.35 Billion |

| Market Size (2026) | USD 11.83 Billion |

| Market Size (2031) | USD 23.1 Billion |

| Growth Rate (2026 - 2031) | 14.32% CAGR |

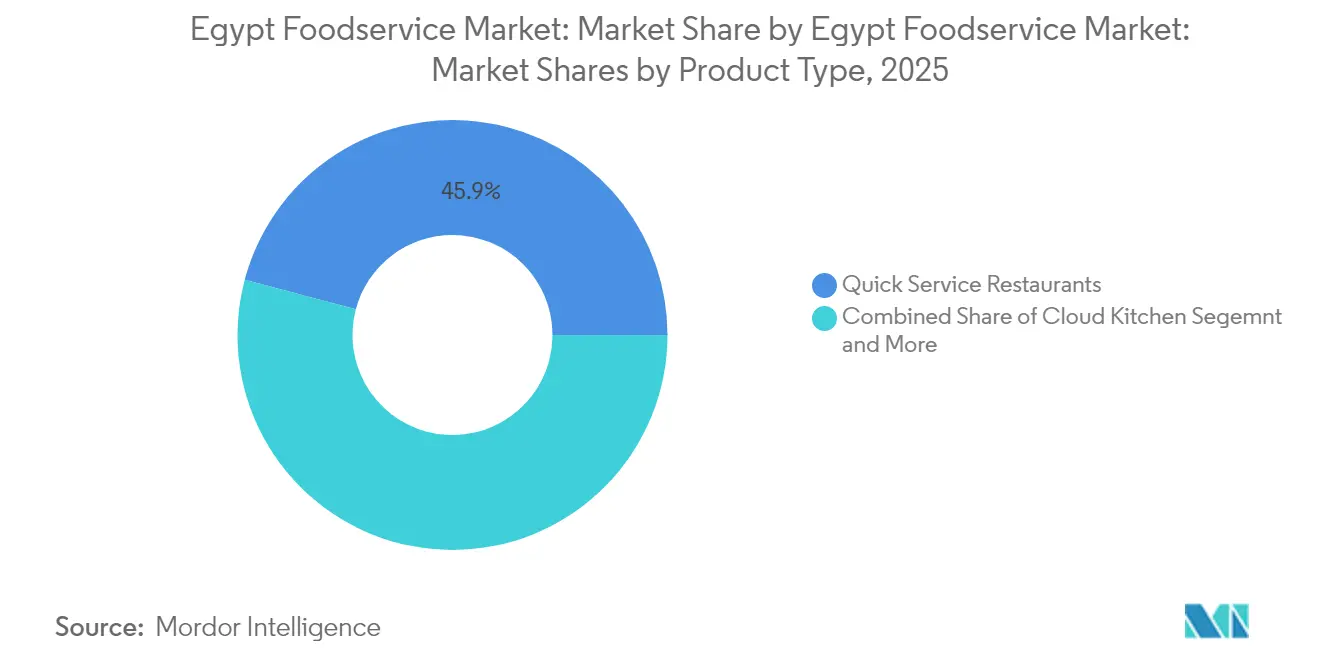

| Fastest Growing Market | Quick Service Restaurants |

| Largest Market | Cloud Kitchen |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Egypt Foodservice Market Analysis by Mordor Intelligence

Egypt foodservice market size in 2026 is estimated at USD 11.83 billion, growing from 2025 value of USD 10.35 billion with 2031 projections showing USD 23.1 billion, growing at 14.32% CAGR over 2026-2031. Robust digital infrastructure, recovering tourism, and rising disposable incomes are propelling demand even as food inflation and currency pressures test sector resilience. Quick service restaurants keep their cost-focused edge, while delivery-led models pull new investment toward cloud kitchens and dark-store networks. Government formalization of street vendors, combined with GCC franchisors’ accelerated entry after the 2024 devaluation, widens participation in the Egypt foodservice market. Ongoing IMF-backed reforms, most visibly the USD 35 billion Ras El-Hekma development, amplify hospitality flows that ripple directly into restaurant traffic[1]International Monetary Fund. "Arab Republic of Egypt: First and Second Reviews Under the Extended Arrangement Under the Extended Fund Facility, Monetary Policy Consultation, and Requests for Waiver of Nonobservance of a Performance Criterion, and Augmentation and Rephasing of Access—Press Release; and Staff Report; IMF Country Report No. 24/98." March 19, 2024. https://www.elibrary.imf.org/downloadpdf/view/journals/002/2024/098/002.2024.issue-098-en.pdf.

Key Report Takeaways

- By foodservice type, Quick Service Restaurants led with 45.86% of Egypt foodservice market share in 2025; Cloud Kitchens are forecast to expand at a 13.21% CAGR through 2031.

- By outlet format, Independent outlets commanded 70.88% share of the Egypt foodservice market size in 2025, whereas Chained outlets are projected to grow at 8.05% CAGR to 2031.

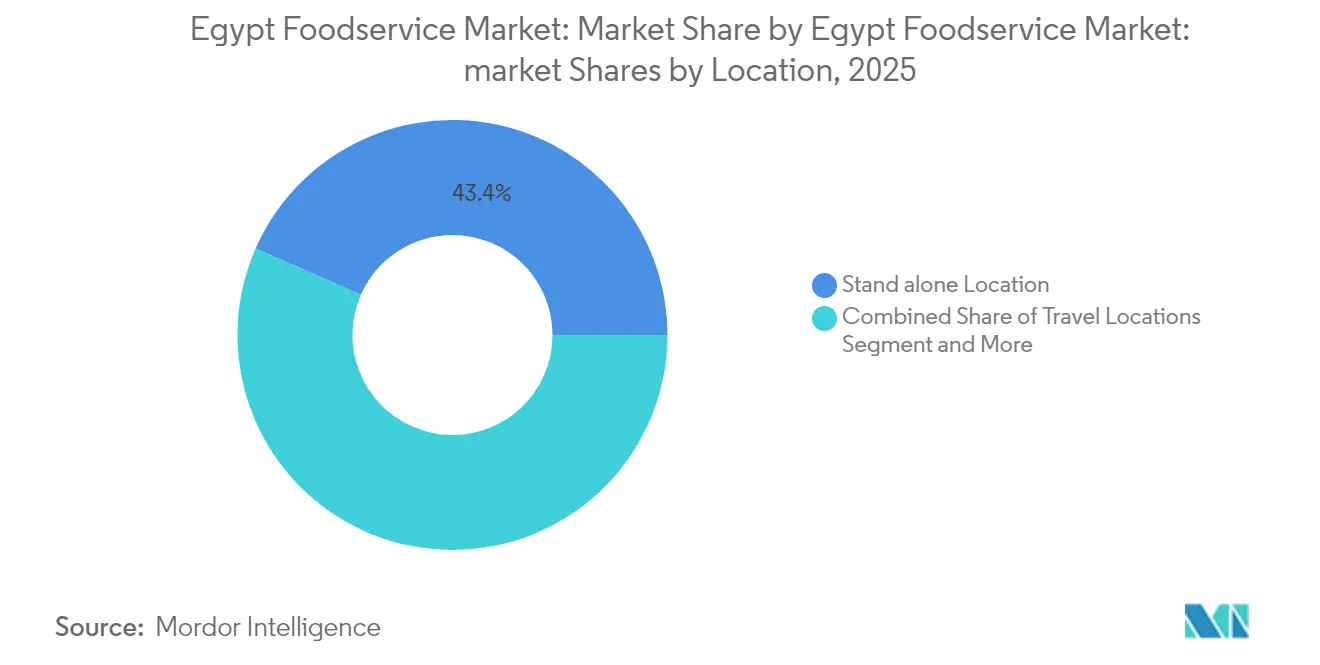

- By location, Standalone venues captured 43.42% share in 2025, while Travel-based outlets are advancing at an 11.44% CAGR to 2031.

- By service type, Dine-in accounted for 58.76% revenue share in 2025; Delivery services hold the fastest trajectory at a 14.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing disposable income & urban middle-class expansion | +2.8% | National, concentrated in Greater Cairo, Alexandria, Giza | Medium term (2-4 years) |

| Proliferation of third-party delivery platforms | +3.1% | Urban centers, expanding to secondary cities | Short term (≤ 2 years) |

| Post-COVID tourism rebound & "Egypt, Safe & Ready" campaign | +2.2% | Red Sea, South Sinai, Luxor, Aswan, Cairo | Medium term (2-4 years) |

| Government formalization of street-food vendors | +1.9% | National, priority in Cairo, Alexandria, Giza | Long term (≥ 4 years) |

| Surge in ghost-kitchen capacity linked to dark-store networks | +2.7% | Greater Cairo, Alexandria, emerging in secondary cities | Short term (≤ 2 years) |

| GCC franchisors' accelerated entry after 2023 currency devaluations | +2.4% | National, initial focus on major urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Disposable Income & Urban Middle-Class Expansion

Egypt's urban middle-class expansion creates sustained demand for foodservice experiences beyond traditional home cooking, particularly as government wage increases and social protection measures partially offset inflation pressures. The government raised public-sector minimum wages from EGP 3,500 to EGP 4,000 and announced an additional EGP 180 billion social package for FY2024/25, including pension top-ups and expanded Takaful and Karama coverage to over 5 million households. This income support, while modest relative to inflation rates, sustains discretionary spending on dining experiences among lower-middle-income segments. Urban centers like Greater Cairo and Alexandria benefit most significantly, as these regions concentrate formal employment opportunities and government salary adjustments[2]Refaat, Taarek. "World Employment Confederation: Egypt 'Attractive' for Investment ... Ingredients for Success 'Available'." SEE News, May 14, 2024. https://see.news/world-employment-confederation-egypt-attractive-for-investment-ingredients-for-success-available. The trend accelerates as Egypt's projected GDP recovery to 4.4-4.5% in FY2024/25 and 5.5% over the medium term creates employment opportunities and wage growth across service sectors. However, the sustainability of this driver depends on successful inflation control, with headline inflation expected to decline from 35.7% to 15.3% by FY2024/25 as monetary tightening measures take effect.

Proliferation of Third-Party Delivery Platforms

Digital delivery platforms fundamentally reshape foodservice accessibility and operational models, with companies like Talabat, Akelni, and Mrsool expanding infrastructure and service coverage across Egyptian urban centers. Talabat's acquisition of Instashop for USD 360 million in 2024 demonstrates the sector's consolidation and expansion into grocery delivery, creating integrated dark-store networks that support both restaurant delivery and quick-commerce operations. This integration enables restaurants to access broader distribution channels while reducing last-mile delivery costs through shared logistics infrastructure. The platforms benefit from Egypt's young demographic profile and increasing smartphone penetration, particularly as mobile payment solutions gain acceptance among urban consumers. OneOrder's USD 3 million Series A funding in 2024 specifically targets restaurant supply chain digitization, indicating investor confidence in the sector's technology adoption potential[3]Wamda. "OneOrder raises $3 million in Series A funding." January 2024. https://www.wamda.com/2024/01/oneorder-raises-3-million-series-funding. The proliferation creates network effects where increased restaurant participation attracts more consumers, while higher order volumes justify platform investments in logistics infrastructure and technology capabilities.

Post-COVID Tourism Rebound & "Egypt, Safe & Ready" Campaign

Egypt's tourism recovery directly translates into foodservice demand across key destinations, with the sector benefiting from both international visitor spending and domestic tourism growth. The "Egypt, Safe & Ready" campaign, launched in coordination with international health protocols, helped restore confidence in Egypt's tourism infrastructure and safety measures. Tourism performance showed strength pre-regional conflicts, though the Gaza-Israel war and Red Sea disruptions affected visitor arrivals in late 2023 and early 2024. Suez Canal receipts fell approximately 50% year-over-year in January 2024, indicating broader regional disruption impacts on tourism flows. However, the Ras El-Hekma development deal provides a significant catalyst for tourism infrastructure expansion, with USD 35 billion in committed investment expected to create new hospitality and foodservice demand along Egypt's North Coast. The project's scale suggests potential for integrated resort developments that could transform regional foodservice markets through both direct hotel-restaurant demand and ancillary dining opportunities serving construction and operational workforces. Recovery sustainability depends on regional stability and successful execution of tourism infrastructure investments.

Government Formalization of Street-Food Vendors

The government's systematic approach to formalizing street food vendors creates pathways for informal operators to access formal supply chains, financing, and regulatory compliance frameworks. This initiative addresses Egypt's high informality rate in the accommodation and food services sector, where overall economic informality reaches 67% according to ILO analysis. Formalization programs provide vendors with commercial registration, tax facilitation packages, and access to digital payment systems through partnerships with the National Food Safety Authority (NFSA) and other regulatory bodies. The process enables street vendors to participate in third-party delivery platforms, expanding their customer reach beyond immediate geographic locations. Digital commercial register initiatives and simplified licensing procedures reduce bureaucratic barriers that previously deterred formalization. However, the transition requires vendors to absorb formal taxation and regulatory compliance costs, creating short-term financial pressures that may slow adoption rates. Success depends on government provision of adequate support services, including access to microfinance, business training, and gradual implementation of tax obligations to ensure vendor viability during the transition period.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High food inflation & EGP depreciation | -3.8% | National, acute in import-dependent urban centers | Short term (≤ 2 years) |

| Volatile import supply chains & ingredient cost spikes | -2.9% | National, severe in Red Sea trade routes | Short term (≤ 2 years) |

| Intermittent power outages raising generator OPEX | -1.7% | National, concentrated in industrial zones | Medium term (2-4 years) |

| Chef talent drain to GCC pushing wage inflation | -2.1% | National, acute in Cairo, Alexandria hospitality hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Food Inflation & EGP Depreciation

Egypt's food inflation crisis severely constrains consumer purchasing power and restaurant profitability, with food and beverage prices rising 71.9% year-over-year and restaurant services inflation reaching 49.5% annually. The March 2024 exchange rate unification resulted in a 38% devaluation of the Egyptian pound against the USD, creating immediate cost pressures for restaurants dependent on imported ingredients, equipment, and packaging materials. Vegetable prices demonstrated extreme volatility, with month-on-month increases of 24.4% in August 2023, forcing restaurants to adjust menu pricing and portion sizes frequently. The inflationary environment disproportionately affects middle and lower-income consumers, who reduce dining frequency and shift toward lower-priced food options. Restaurant operators face margin compression as they balance cost pass-through with consumer price sensitivity, often resulting in reduced service quality or operational hours. The Central Bank of Egypt's aggressive monetary tightening, with policy rates reaching 27.75%, aims to anchor inflation expectations but simultaneously increases borrowing costs for restaurant expansion and working capital financing. Recovery depends on successful inflation control, with IMF projections indicating headline inflation declining to 15.3% by FY2024/25 as exchange rate stability and monetary policy measures take effect.

Volatile Import Supply chains & Ingredient Cost Spikes

Supply chain disruptions create operational uncertainty and cost volatility for foodservice operators, particularly those dependent on imported ingredients and specialized equipment. Red Sea shipping disruptions reduced Suez Canal receipts by approximately 50% year-over-year in January 2024, indicating broader logistics challenges affecting food import reliability and costs The government's fuel price indexation mechanism, implemented in March 2024 with diesel prices rising 21.2% and fuel oil increasing 25%, directly impacts food transportation and cold chain logistics costs. Restaurants face inventory management challenges as they balance carrying costs against stockout risks, often leading to menu simplification or increased reliance on locally-sourced ingredients. The volatility particularly affects international franchise operations and upscale restaurants that maintain standardized ingredient specifications and cannot easily substitute local alternatives. Foreign exchange shortages, which created USD 7-8 billion in FX backlogs at banks before the March 2024 unification, previously delayed essential imports and forced restaurants to seek alternative suppliers at premium prices. While FX liberalization has cleared these backlogs, ongoing regional conflicts and global supply chain pressures maintain elevated risk levels for import-dependent operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Segment 1

Quick Service Restaurants command 45.86% market share in 2025, reflecting Egyptian consumers' preference for affordable, convenient dining options amid economic pressures and time constraints in urban environments. The segment's dominance stems from its ability to offer standardized quality at accessible price points, with major players like KFC operating 169 branches across Egypt and McDonald's maintaining a strong presence through Mansour Group's franchise operations. QSR operators benefit from economies of scale in procurement, standardized operations that reduce labor training costs, and established supply chain relationships that provide some insulation from ingredient cost volatility. The segment's resilience during inflationary periods reflects its value proposition for price-sensitive consumers seeking consistent dining experiences. International franchisors like Arby's, which signed agreements for 50 restaurant locations in 2024, view Egypt's QSR market as an attractive expansion opportunity despite economic headwinds.

Cloud Kitchens represent the fastest-growing foodservice segment at 13.21% CAGR through 2031, driven by digital delivery platform expansion and changing consumer preferences for home dining experiences. This segment benefits from significantly lower capital requirements compared to traditional restaurants, eliminating front-of-house real estate costs and enabling operators to focus resources on food production and delivery optimization. Talabat's acquisition of Instashop for USD 360 million demonstrates the integration between delivery platforms and dark-store networks, creating infrastructure that supports both restaurant delivery and quick-commerce operations. Cloud kitchens enable restaurant brands to test new markets and menu concepts with minimal upfront investment, while providing flexibility to adjust operations based on demand patterns and delivery zone performance. The segment's growth accelerates as third-party delivery platforms expand coverage beyond major urban centers, creating market access for cloud kitchen operators in secondary cities where traditional restaurant economics may not support physical locations.

By Outlet: Independent Resilience Versus Chain Expansion

Independent outlets maintain market leadership with 70.88% share in 2025, demonstrating the resilience of family-owned and small-scale foodservice operations that dominate Egypt's traditional dining landscape. These establishments benefit from lower overhead costs, flexible menu adaptation, and deep local market knowledge that enables them to adjust quickly to consumer preferences and economic conditions. Independent operators often source ingredients from local suppliers, providing some protection against import cost volatility while supporting regional food systems. Their success reflects Egyptian consumers' preference for authentic, locally-adapted cuisine and personalized service experiences that larger chains struggle to replicate.

Chained outlets emerge as the fastest-growing segment at 8.05% CAGR through 2031, reflecting the gradual formalization and consolidation trends within Egypt's foodservice market. Chain expansion benefits from standardized operations, centralized procurement systems, and established brand recognition that attracts consumers seeking consistent quality and service standards. International franchisors accelerated their Egypt entry following the 2023-2024 currency devaluations, which improved investment attractiveness and reduced dollar-denominated franchise fees relative to local revenue potential. Pickl's expansion into Egypt and Arby's 50-restaurant development agreement exemplify this trend, as GCC-based franchisors view Egypt as an attractive growth market despite economic volatility.

By Location: Standalone Prevalence Meets Travel Opportunity

Standalone locations dominate with 43.42% market share in 2025, reflecting the prevalence of neighborhood restaurants, street food vendors, and independent establishments that serve local communities without integration into larger commercial developments. These locations benefit from lower rental costs compared to mall or hotel-integrated spaces, enabling operators to offer competitive pricing while maintaining acceptable profit margins. Standalone establishments often develop strong local customer loyalty through personalized service and menu customization that responds to immediate community preferences. The segment includes both formal restaurants and semi-formal establishments that serve workplace clusters, residential neighborhoods, and transportation hubs.

Travel locations represent the fastest-growing segment at 11.44% CAGR through 2031, directly linked to Egypt's tourism recovery and infrastructure development initiatives. This segment benefits from the government's "Egypt, Safe & Ready" campaign and major tourism investments, including the USD 35 billion Ras El-Hekma development project that will create significant hospitality and foodservice demand. Airport foodservice operations, exemplified by SSP Group's contract wins at Egyptian airports, demonstrate the segment's expansion potential as international travel recovers SSP Group.

By Service Type: Dine-In Tradition Meets Delivery Transformation

Dine-in service maintains dominance with 58.76% market share in 2025, reflecting Egyptian cultural preferences for social dining experiences and the continued importance of restaurants as community gathering spaces. This preference persists despite economic pressures, indicating that dining out serves social and cultural functions beyond mere food consumption. Dine-in establishments benefit from higher average order values compared to delivery orders, as customers typically order beverages, appetizers, and desserts when dining in restaurant environments. The segment includes both formal restaurants and traditional establishments like ahwas (coffee houses) that serve as social hubs for business meetings, family gatherings, and community interactions.

Delivery services emerge as the fastest-growing segment at 14.52% CAGR through 2031, transforming foodservice accessibility and operational models across Egyptian urban centers. This growth reflects changing consumer behavior accelerated by digital platform proliferation, with companies like Talabat, Akelni, and Mrsool expanding coverage and service capabilities. The segment benefits from lower overhead costs compared to dine-in operations, as restaurants can optimize kitchen space and eliminate front-of-house expenses while reaching broader geographic markets. Delivery growth enables restaurants to serve customers during extended hours and weather conditions that might otherwise limit foot traffic to physical locations. Integration with dark-store networks, demonstrated by Talabat's Instashop acquisition, creates operational synergies that reduce delivery costs while expanding product offerings beyond traditional restaurant menus.

Geography Analysis

Egypt's foodservice market is heavily concentrated in major urban centers, including Greater Cairo, Alexandria, and Giza. This concentration is driven by high population density, elevated disposable incomes, and well-developed tourism infrastructure. These cities benefit from established supply chains, diverse consumer bases, and proximity to import facilities, ensuring ingredient availability despite broader supply chain challenges. The urban development patterns in Egypt, characterized by economic opportunities and formal employment clustering in metropolitan areas, have created consumer segments with regular income and dining-out habits. Additionally, government infrastructure projects, such as the New Administrative Capital and urban expansion initiatives, are generating new foodservice demand in emerging urban zones. However, this geographic concentration increases vulnerability to localized economic shocks and limits market access for operators aiming to expand beyond these cities.

Tourism destinations along the Red Sea, including Sharm El-Sheikh, Hurghada, and emerging developments on the North Coast, present significant growth opportunities. These regions are benefiting from the recovery of international tourism and substantial hospitality investments. The USD 35 billion Ras El-Hekma project is a key driver of foodservice demand, catering to both hotel-restaurant requirements and workforce dining needs. These destinations command premium pricing due to tourist spending patterns and limited competition, enabling operators to achieve higher profit margins despite elevated operational costs. Foreign currency revenues in these regions provide some insulation from domestic inflation, although they remain vulnerable to regional conflicts and global travel disruptions. The "Egypt, Safe & Ready" campaign is supporting recovery by addressing safety concerns that previously deterred international visitors.

Secondary cities and rural areas are emerging as potential markets due to the expansion of digital delivery platforms and government formalization initiatives. These regions offer lower operational costs, including reduced rent and labor expenses, while serving populations with increasing purchasing power supported by government social protection programs and agricultural income. Platforms like Talabat and Akelni are facilitating market access for local operators and national chains seeking geographic diversification. However, infrastructure challenges, such as unreliable power supply and limited cold chain logistics, increase operational complexity. Success in these markets requires business models tailored to local preferences, price sensitivity, and infrastructure constraints, while leveraging digital platforms to overcome traditional market access barriers.

Competitive Landscape

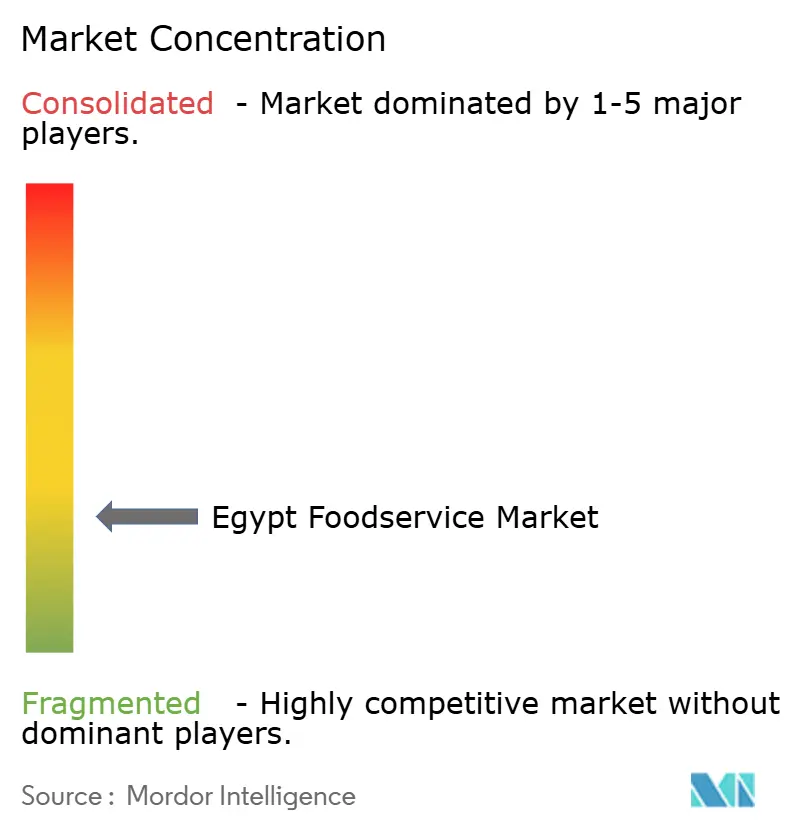

The Egypt Foodservice Market, with a concentration score of 3 out of 10, showcases moderate fragmentation. This score highlights substantial opportunities for both market consolidation and the success of new entrants, provided they adopt strategic positioning and operational excellence. Market leaders like Americana Restaurants International PLC, Alamar Foods Company, and Mansour Group harness established supply chain networks, brand recognition, and diverse portfolios to secure their competitive edge. However, the market's low concentration signals that newcomers can carve out significant market shares through unique positioning or by embracing technology. The competitive landscape rewards operators adept at navigating economic fluctuations while upholding consistent quality and value. Successful players showcase adaptability, tweaking menu prices, portion sizes, and service models in response to shifts in consumer spending power.

Strategic trends highlight a push towards digital transformation and enhanced delivery capabilities. Traditional operators are increasingly collaborating with third-party platforms and pouring investments into cloud kitchen formats, all to tap into the surging demand for deliveries. But technology adoption isn't limited to just delivery; it's also permeating areas like inventory management, customer engagement, and operational optimization. Such advancements empower smaller operators to rival the scale advantages of larger chains.

Untapped opportunities abound in secondary cities with limited delivery platform coverage, in tourism hotspots undergoing infrastructure upgrades, and in niche cuisine segments catering to Egypt's rich cultural tapestry. The regulatory landscape is shifting in favor of formal operators. Government initiatives are not only offering compliance benefits but also easier access to financing. This positions licensed establishments for swift growth, while their informal counterparts grapple with pressures to formalize or risk exiting the market.

Egypt Foodservice Industry Leaders

-

Alamar Foods Company

-

Americana Restaurants International PLC

-

Mansour Group

-

Mo'men Group

-

The Olayan Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Nobu has officially launched its first restaurant in Egypt, at OGAMI, a prestigious coastal development by SODIC on Egypt’s North Coast. The debut brings Nobu's signature Japanese-Peruvian fusion cuisine to one of the region’s key summer destinations, blending understated elegance with vibrant Mediterranean energy.

- June 2025: Pizza Inn, the pizza buffet concept, opened its first restaurant in Egypt as part of a seven-store master franchise agreement with Al Ruwad Hospitality Services & Restaurants Management Group

- October 2024: Dubai’s popular burger joint Pickl has launched its flagship store in Cairo in 2024, marking a major milestone in its regional expansion. Located at Park Street West in Sheikh Zayed, this venue offers dine-in, delivery services, and an open kitchen experience for burger lovers.

Egypt Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.| Cafes & Bars | By Cuisine | Bars & Pubs |

| Cafes | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee & Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| Foodservice Type | Cafes & Bars | By Cuisine | Bars & Pubs |

| Cafes | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee & Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| Outlet | Chained Outlets | ||

| Independent Outlets | |||

| Location | Leisure | ||

| Lodging | |||

| Retail | |||

| Standalone | |||

| Travel | |||

| Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms