Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

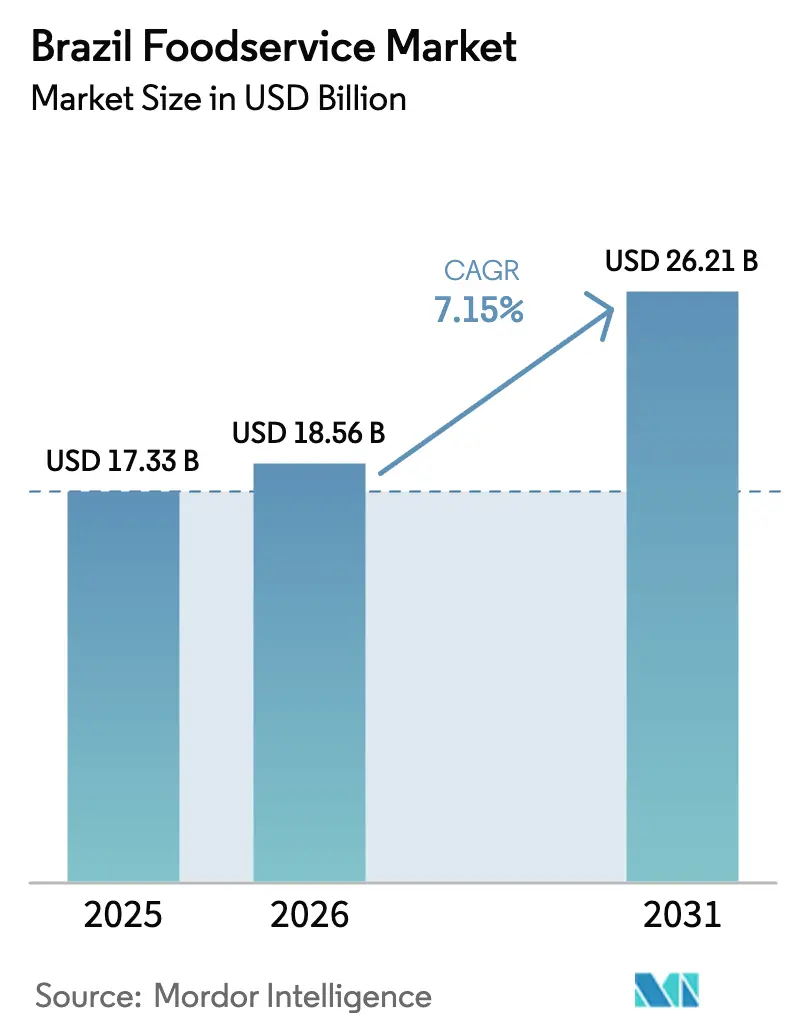

| Base Year Market Size (2025) | USD 17.33 Billion |

| Market Size (2026) | USD 18.56 Billion |

| Market Size (2031) | USD 26.21 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

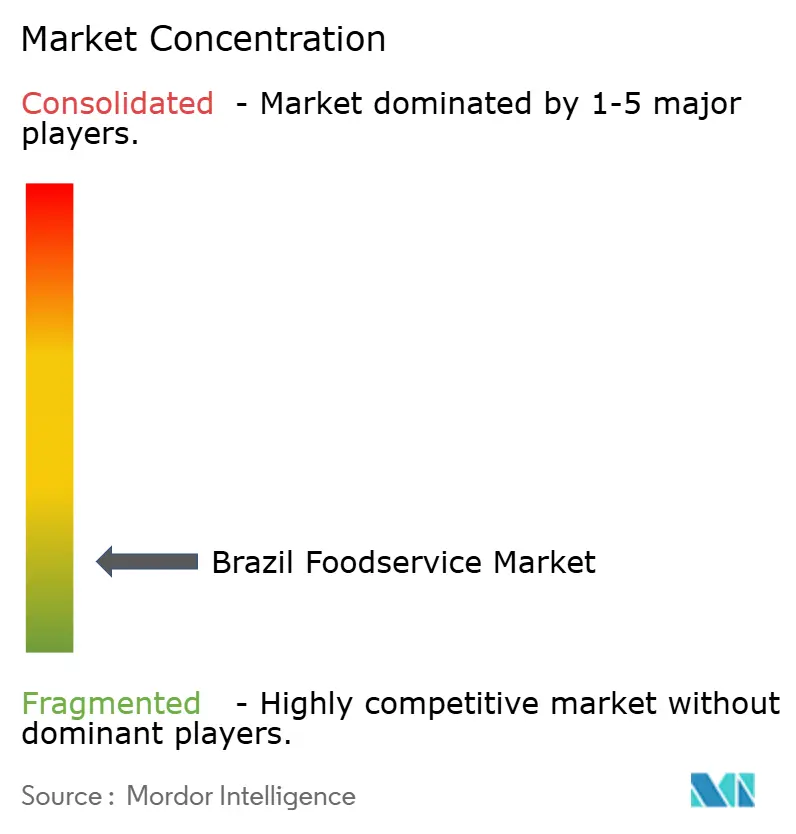

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Foodservice Market Analysis by Mordor Intelligence

The Brazil foodservice was valued at USD 17.33 billion in 2025 and estimated to grow from USD 18.56 billion in 2026 to reach USD 26.21 billion by 2031, at a CAGR of 7.15% during the forecast period (2026-2031). Urbanization, digital payment penetration that is on track to cover 76% of Brazilians by 2025, and a structural shift toward out-of-home dining are reinforcing demand. Quick-service restaurants continue to capture the largest spending, yet cloud kitchens are scaling fast as São Paulo’s 2022 ordinance lowered real-estate barriers. Delivery platforms such as iFood and Rappi are re-shaping order economics, while tourism receipts that topped BRL 36.6 billion in the first nine months of 2024 have widened opportunities for lodging and travel locations. Operators that master data-driven loyalty, menu innovation, and compliance with Agência Nacional de Vigilância Sanitária (ANVISA) traceability rules are positioned to widen margins even as raw-material inflation and labor turnover test resilience.

Key Report Takeaways

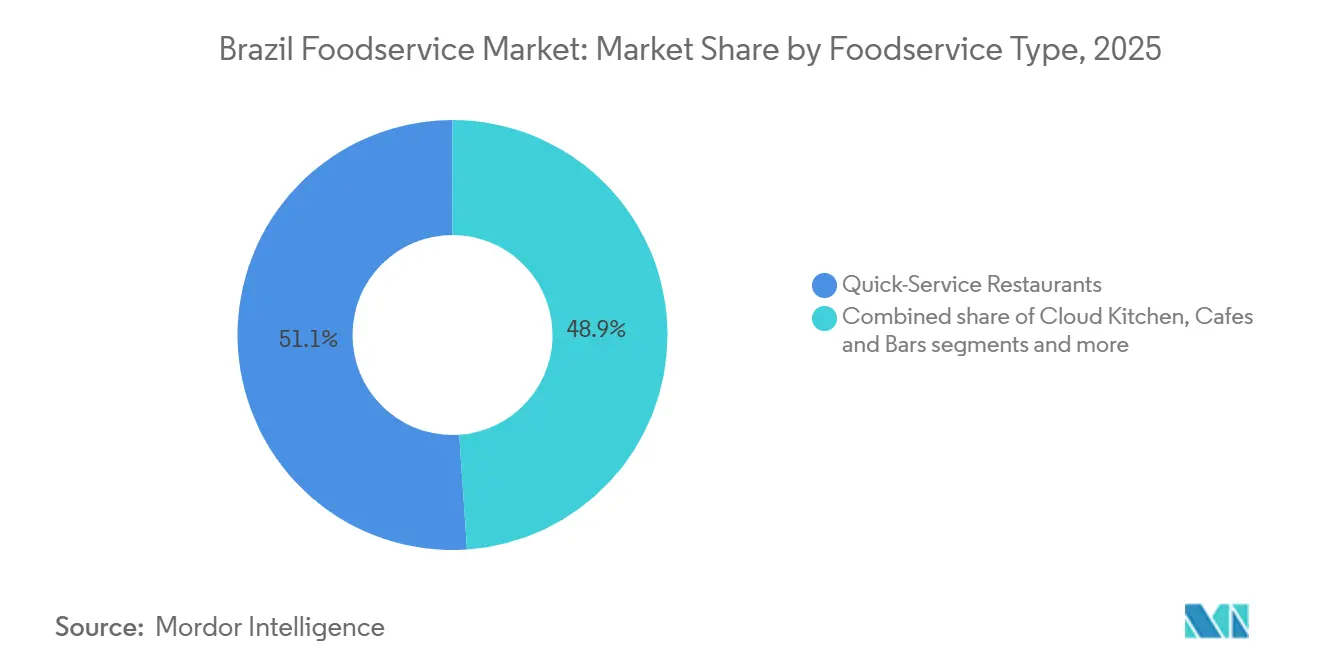

- By foodservice type, quick-service restaurants led with 51.07% revenue share in 2025, whereas cloud kitchens are projected to expand at an 11.18% CAGR through 2031.

- By outlet, independent venues held 81.17% share of the Brazil foodservice market size in 2025, while chained formats are advancing at a 7.18% CAGR to 2031.

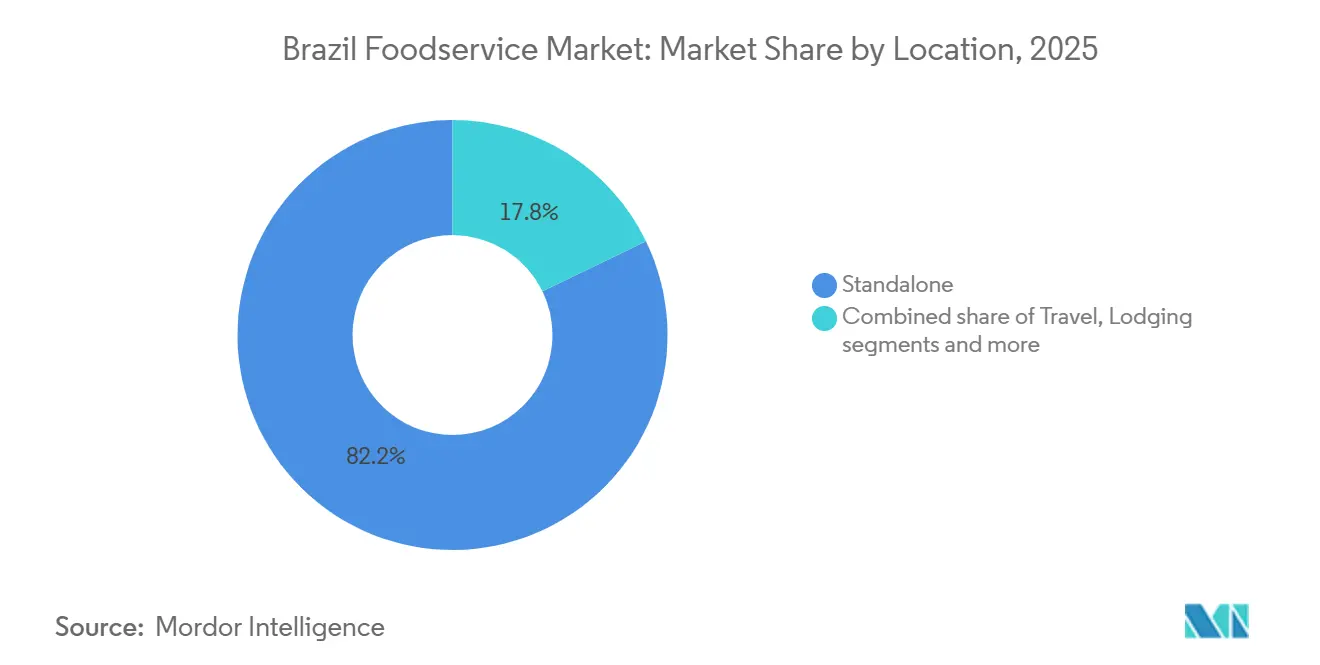

- By location, standalone sites accounted for 82.19% share in 2025, and lodging outlets are forecast to grow at an 8.89% CAGR through 2031 as tourism spending accelerates.

- By service type, dine-in generated 65.31% of revenue in 2025, but delivery is poised for a 10.07% CAGR to 2031 on the back of API-enabled integration.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for convenience and fast food | +1.2% | National, concentrated in São Paulo, Rio de Janeiro, Brasília metropolitan areas | Medium term (2-4 years) |

| Expanding café and casual dining segments | +0.8% | National, with early gains in São Paulo, Rio de Janeiro, Belo Horizonte | Medium term (2-4 years) |

| Increasing tourism driving market growth | +0.6% | Coastal cities, Rio de Janeiro, Salvador, Florianópolis; Amazon region gaining traction | Short term (≤ 2 years) |

| Influence of international cuisine trends | +0.5% | São Paulo, Rio de Janeiro, Curitiba, Porto Alegre | Long term (≥ 4 years) |

| Rising popularity of online food delivery services | +1.5% | National, led by São Paulo, Rio de Janeiro, Belo Horizonte, expanding to secondary cities | Short term (≤ 2 years) |

| Government initiatives to support foodservice industry | +0.4% | National, with emphasis on Northeast and North regions for SME support | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for convenience and fast food

The growing demand for convenience and fast food is a key driver of the Brazil foodservice market. With a highly urbanized population, approximately 88% of Brazilians lived in urban areas in 2024, according to World Bank data [1]Source: World Bank, "Urban population (% of total population) - Brazil", data.worldbank.org. This urban shift has increased the need for quick, accessible meal options, particularly in bustling cities. Fast food chains, delivery services, and ready-to-eat meals are thriving as a result, catering to the fast-paced lifestyle of urban dwellers. The convenience factor is becoming increasingly important to Brazilian consumers, who prioritize time-saving solutions in their busy daily routines. As a result, foodservice businesses are rapidly adapting to meet this demand, contributing to the overall growth of the sector. This trend is expected to continue as urbanization and the preference for quick dining experiences increase across Brazil.

Expanding café and casual dining segments

The café and casual dining layer of the Brazil foodservice market is benefiting from a consumer shift toward fewer but higher-value visits, which is helping experience-led formats justify spending. The Brazilian Specialty Coffee Association data cited in the draft indicated that the specialty coffee segment is growing 15% annually and already represents 5% to 10% of national coffee consumption. That demand profile is drawing branded entrants, and Juan Valdez opened its first Brazilian store in December 2025 with plans for 100 units by 2028 and 300 by 2032 through franchising. In parallel, spend per visit rose 28.3% year over year in Q1 2026, which shows that consumers are still willing to pay more when the format offers stronger perceived value and a better occasion experience. Grupo Madero’s combined premium and fast-casual model also performed well, with 32.3% revenue growth and 18.3% same-store sales growth in 2026, which suggests that casual dining and café formats are increasingly meeting in the middle around quality, convenience, and accessible premium positioning.

Increasing tourism driving the market growth

Increasing tourism is a key driver of growth in Brazil's foodservice market. According to the Presidência da República, the number of international tourists visiting Brazil between January and May 2025 reached a historic high of 4.8 million, a 49.7% increase over the same period in 2024, which recorded 3.2 million visitors [2]Source: Brazil welcomed 4.8 million international tourists over five months — 1 million to Rio de Janeiro, “Presidência da República”, gov.br. This influx of tourists not only boosts the economy but also drives demand for a variety of dining experiences, from local Brazilian delicacies to international cuisines. In the first nine months of 2024, tourism receipts surged to BRL 36.6 billion, reflecting a 14.5% growth over the previous year [3]Source: Brazilian Ministry of Tourism, “Tourism Data”, gov.br/turismo/pt-br. As more visitors flock to Brazil, they contribute to a growing appetite for diverse food offerings, creating new opportunities for restaurants, cafés, and foodservice chains. The rise in international tourism is expected to continue shaping the foodservice sector, as it encourages the expansion of specialized dining establishments that cater to global tastes. As a result, tourism not only supports the country's hospitality industry but also fuels the broader growth of Brazil's foodservice market.

Influence of international cuisine trends

Restaurant operators are responding by expanding international menus and introducing fusion concepts that blend Brazilian ingredients with global flavors, such as sushi featuring tropical fruits or burgers topped with local cheeses and sauces. Major domestic chains including Grupo Trigo have diversified their portfolios with concepts such as China in Box, Gendai (Japanese cuisine), and Gurumê, while premium restaurant groups such as Alife Nino continue expanding Italian-inspired dining concepts across major cities. International brands including Outback Steakhouse, Madero's American-style gourmet burgers, and authentic Asian restaurant chains have further strengthened consumer acceptance of global cuisines. This evolving preference for multicultural dining experiences is encouraging menu innovation, increasing restaurant visits, and creating new growth opportunities across Brazil's foodservice industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising costs of raw materials and inflation | -0.9% | National, acute in Northeast and North regions with longer supply chains | Short term (≤ 2 years) |

| Labor shortages impacting operations | -0.7% | National, most severe in São Paulo, Rio de Janeiro, Brasília | Medium term (2-4 years) |

| Limited consumer purchasing power in some regions | -0.5% | Northeast, North regions; rural areas across all states | Long term (≥ 4 years) |

| Stringent regulations on food safety and hygiene | -0.3% | National, with higher compliance costs in São Paulo, Rio de Janeiro due to municipal overlays | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising costs of raw materials and inflation

Rising costs of raw materials and inflation are significant restraints on Brazil's foodservice market. In recent years, the country has faced increasing prices for essential ingredients such as meat, grains, and vegetables, which has put pressure on foodservice operators. Inflationary pressures have also led to higher operational costs, from utilities to wages, further squeezing profit margins. These rising costs have forced many restaurants and cafés to adjust their pricing strategies, sometimes resulting in higher prices for consumers. For smaller foodservice businesses, these financial challenges can be especially difficult to navigate, impacting their ability to stay competitive. As inflation continues to affect the economy, many businesses are struggling to balance quality, affordability, and profitability. The situation may lead to slower market growth as consumers become more cautious about their spending on dining out.

Labor shortages impacting operations

Labor shortages are a significant restraint on the Brazil foodservice market, affecting operations across the industry. The demand for skilled workers in restaurants, cafés, and other foodservice establishments has outpaced supply, leading to staffing challenges. Many businesses are struggling to hire and retain qualified chefs, servers, and other essential staff. These labor gaps often result in longer wait times for customers, lower service quality, and even restricted operating hours. Additionally, higher labor costs due to increased demand for workers have put added pressure on foodservice businesses already facing rising operational expenses. For smaller establishments, this shortage can be particularly damaging, leading to reduced efficiency and customer satisfaction. As the labor market remains tight, the foodservice industry must find innovative solutions to attract and retain talent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Disrupt Traditional Formats

Quick-service restaurants (QSRs) dominated the Brazil foodservice market with a substantial 51.07% revenue share in 2025, establishing themselves as the leading segment through their emphasis on speed, value, and widespread accessibility. Iconic brands like McDonald's, Burger King, and local powerhouse Bob's deliver affordable combos often below BRL 25, resonating with cost-conscious urban consumers amid fluctuating inflation and busy routines. These outlets flourish in high-density areas such as São Paulo, Rio de Janeiro, and Belo Horizonte, where drive-thrus, app ordering, and under-four-minute service times capture peak-hour traffic from commuters and families alike. QSRs capitalize on localized menus blending global staples with Brazilian flavors like pão de queijo burgers or coxinha sides, ensuring mass appeal across diverse demographics.

Cloud kitchens are poised as the fastest-growing segment in Brazil's foodservice market, expected to accelerate at a strong 11.18% CAGR through 2031, propelled by digital platforms and urban delivery demand. Concentrated in megacities like São Paulo and emerging hubs such as Fortaleza, these virtual kitchens optimize for iFood and Rappi orders, slashing costs by eliminating dine-in spaces and focusing on high-margin ghost brands. The model's rise stems from hyper-targeted offerings like feijoada bowls, açaí deliveries, and vegan jackfruit tacos, catering to late-night workers, remote professionals, and health trends with minimal wait times. Cloud kitchens leverage AI analytics for demand spikes, enabling rapid menu pivots and multi-brand operations from single facilities to test viral concepts risk-free.

By Outlet: Independents Dominate but Chains Gain Ground

The independent venue segment continues to dominate Brazil’s foodservice market, capturing approximately 81.17% share of the Brazil foodservice market in 2025. This overwhelming presence reflects the country’s deep-rooted culture of localized, family-run eateries that cater to regional preferences and diverse consumer tastes. Independent operators remain vital to the market’s structure, often relying on personalized service, traditional recipes, and strong community ties to maintain customer loyalty. Their flexibility in menu adaptation and pricing strategies allows them to respond quickly to changing consumer demands. These venues also benefit from lower operational constraints compared to large chains, enabling them to sustain profitability even in periods of economic volatility.

While independent outlets lead by size, chained formats are emerging as the fastest-growing segment, projected to expand at a compound annual growth rate (CAGR) of 7.18% through 2031. Growth is being driven by rising urbanization, changing consumer lifestyles, and a growing appetite for convenience and brand consistency. Chain operators are strengthening their presence across quick-service, casual dining, and coffee segments by leveraging franchising models and digital transformation. Investments in technology such as delivery apps, loyalty programs, and data analytics are further helping chains enhance customer reach and operational efficiency. Moreover, the increasing acceptance of international and premium food concepts among younger consumers is accelerating this trend.

By Location: Standalone Sites Prevail, Lodging Segment Accelerates

Standalone outlets continue to represent the dominant format in Brazil’s foodservice landscape, accounting for around 82.19% of the total market share in 2025. Their strong position is supported by widespread distribution across urban and suburban areas, appealing to a broad customer base ranging from quick-service customers to full-service diners. Standalone sites typically offer greater flexibility in menu innovation, branding, and operational management, allowing operators to tailor their offerings to local consumer preferences. These outlets also benefit from high street visibility and accessibility, factors that significantly influence impulse dining and repeat visitation.

In contrast, lodging-based foodservice outlets represent the fastest-growing location segment, expected to expand at a CAGR of 8.89% between 2026 and 2031, supported by rising domestic and international tourism. The recovery of travel and hospitality sectors is encouraging hotels, resorts, and guest accommodations to enhance their dining offerings as key revenue drivers. Many hospitality operators are upgrading their culinary concepts, partnering with celebrity chefs, and incorporating local and experiential dining themes to attract visitors. Additionally, the growing trend of food tourism and experiential travel is increasing the contribution of in-house restaurants and bars to total foodservice revenues. The integration of technology and delivery services within lodging formats is also improving convenience and expanding access beyond hotel guests.

By Service Type: Delivery Gains Share as Dine-In Adapts

Dine-in services accounted for the majority share of Brazil’s foodservice market in 2025, generating around 65.31% of total sector revenue. This strong performance underscores Brazilians’ enduring preference for social and experiential dining, which remains central to the country’s food culture. Restaurants that offer dine-in experiences continue to thrive on ambiance, personalized service, and menu differentiation, all of which help attract repeat customers and sustain brand loyalty. The segment’s strength is particularly noticeable in casual dining, full-service restaurants, and traditional eateries, where in-person interaction is a key part of the value proposition. Moreover, as consumer spending recovers and urban areas see more foot traffic, dine-in formats are regaining pre-pandemic momentum.

Meanwhile, the delivery segment is positioned as the fastest-growing service type, projected to expand at a CAGR of 10.07% through 2031, driven by ongoing digital transformation and API-enabled integration. The growing penetration of mobile ordering platforms and seamless third-party delivery apps has revolutionized how consumers access food. Operators are increasingly leveraging automation, data analytics, and integrated APIs to synchronize kitchen operations with real-time delivery demand, ensuring efficiency and consistency. Additionally, younger consumers and working professionals are fueling the shift toward delivery due to convenience, time savings, and expanding menu availability. Partnerships between cloud kitchens, aggregators, and traditional restaurants are also accelerating this growth by expanding coverage and reducing service bottlenecks.

Geography Analysis

The Brazil foodservice market is heavily concentrated in its major urban centers, particularly in São Paulo, Rio de Janeiro, and Belo Horizonte, where a large portion of the population resides and disposable incomes are higher. These metropolitan regions have a high density of restaurants, cafes, and fast food outlets, catering to both local consumers and international tourists. São Paulo, the largest city, is a hub for food innovation, with a diverse range of international and local dining options, while Rio de Janeiro’s booming tourism industry further fuels the demand for foodservice establishments, especially in areas with heavy tourist traffic like Copacabana and Ipanema.

In contrast, smaller cities and rural regions in Brazil tend to have more traditional dining preferences, with a larger emphasis on family-run restaurants and local cuisine. The market in these areas is not as saturated with international brands, and foodservice is often more focused on affordable, home-style meals. However, the growing middle class and increased urbanization are gradually changing this, leading to a rise in demand for quick-service restaurants (QSRs) and fast-casual chains in smaller cities, especially in regions like the Northeast and Central-West, where economic growth is driving consumption.

The tourism sector plays a significant role in shaping the geography of the foodservice market in Brazil, particularly in tourist destinations like Salvador, Florianópolis, and Recife. These regions see increased demand for dining options that cater to both international visitors and local tourists. High-end restaurants, regional Brazilian food, and international fast food chains are thriving in these areas due to the influx of tourists. Coastal regions, known for their natural beauty and vacation spots, present a key opportunity for growth, as they attract a global audience eager to experience both local delicacies and global food offerings.

Competitive Landscape

The Brazil foodservice market is highly fragmented, with a mix of local independent operators and international chains competing for market share. Large multinational brands such as McDonald’s, Burger King, Pizza Hut, and Subway dominate the quick-service restaurant (QSR) segment, benefitting from their established brand recognition, economies of scale, and extensive delivery networks. These chains continue to expand their reach in both urban and suburban areas, leveraging aggressive marketing strategies and frequent menu innovations. However, local brands, such as Giraffas and Habib’s, maintain a stronghold by offering Brazilian-style cuisine, catering to regional tastes, and emphasizing customer loyalty.

Independent restaurants and small-scale operators are also crucial to the competitive landscape, with a growing number of food trucks, boutique cafes, and regional eateries entering the market. These players cater to niche consumer demands, such as health-conscious meals, sustainable practices, and authentic regional flavors, providing an attractive alternative to the mainstream chains. In addition, the rise of the delivery economy, particularly through platforms like iFood and Uber Eats, has leveled the playing field, allowing small players to reach a wider audience and compete with larger brands that traditionally dominated brick-and-mortar locations.

Another key competitive factor in the Brazil foodservice market is the growing consumer demand for diversity in dining options, including plant-based menus and international cuisines. Both large and small operators are innovating to meet these needs. Global chains are incorporating more health-conscious offerings, while local restaurants focus on traditional Brazilian dishes or modern twists on familiar foods. Moreover, sustainability concerns are shaping competition, with an increasing focus on eco-friendly packaging, locally sourced ingredients, and waste reduction.

Brazil Foodservice Industry Leaders

-

Arcos Dorados Holdings Inc.

-

Grupo Madero

-

Restaurant Brands International Inc.

-

Yum! Brands, Inc.

-

Habib's S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Yum! Brands, the U.S.-based parent company of Pizza Hut, KFC, and Taco Bell, is stepping back in as the master franchisee for a Mexican-food restaurant chain in Brazil, aiming for a target of 200 stores by 2030.

- September 2025: Firehouse Subs, building on its international expansion, announced its entry into Brazil. The brand has ambitious plans, targeting the opening of over 500 restaurants across the country within the next decade. With this move, Firehouse Subs is setting its sights on Brazil's burgeoning sandwich market.

- February 2025: Fogo de Chão, a chain renowned for its southern Brazilian cuisine, has inaugurated its ninth location in Brazil, setting up shop at Shopping Tamboré in São Paulo. This expansion not only highlights Fogo de Chão's commitment to its Brazilian heritage but also signals its ambitions for further global growth.

Brazil Foodservice Market Report Scope

Foodservice is the business of preparing, handling, and serving food to people outside of their homes. The market scope encompasses cafes & bars, cloud kitchens, full-service restaurants, and quick-service restaurants.

The Brazil foodservice market is segmented by foodservice type, outlet, location, and service type. Based on foodservice type, the market is segmented into cafes and bars, cloud kitchens, full-service restaurants and quick-service restaurants. Based on outlet, the market is segmented by chained outlets and independent outlets. Based on location, the market is segmented by leisure, lodging, retail, standalone, and travel. Based on service type, the market is segmented by dine-in, takeaway, and delivery). The market sizing has been done in value terms in USD for all the above mentioned segments.

By Foodservice Type

| Cafes and Bars | Bars and Pubs |

| Cafes | |

| Juice/Smoothie/Dessert Bars | |

| Specialist Coffee and Tea Shops | |

| Cloud Kitchens | |

| Full-Service Restaurants | Asian |

| European | |

| Latin American | |

| Middle Eastern | |

| North American | |

| Other FSR Cuisines | |

| Quick-Service Restaurants | Bakeries |

| Burger | |

| Ice-cream | |

| Meat-based Cuisines | |

| Pizza | |

| Other QSR Cuisines |

Outlet

| Chained Outlets |

| Independent Outlets |

Location

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

Service Type

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Cafes and Bars | Bars and Pubs |

| Cafes | ||

| Juice/Smoothie/Dessert Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchens | ||

| Full-Service Restaurants | Asian | |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick-Service Restaurants | Bakeries | |

| Burger | ||

| Ice-cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines | ||

| Outlet | Chained Outlets | |

| Independent Outlets | ||

| Location | Leisure | |

| Lodging | ||

| Retail | ||

| Standalone | ||

| Travel | ||

| Service Type | Dine-in | |

| Takeaway | ||

| Delivery | ||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms