Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

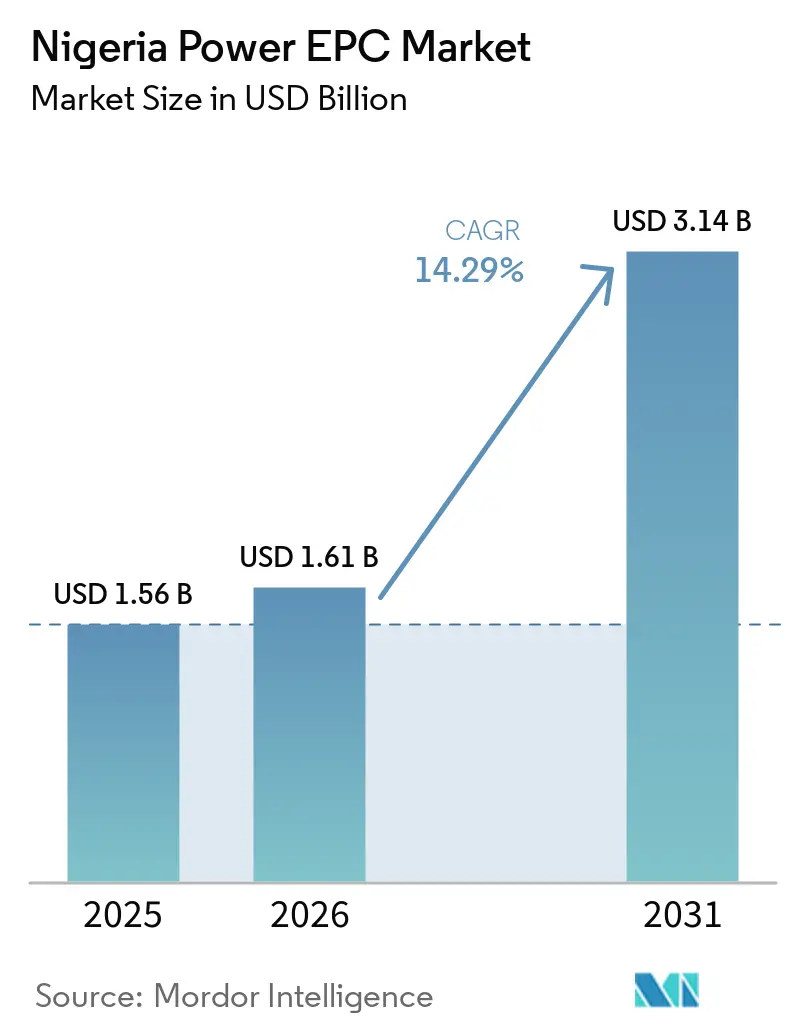

| Base Year Market Size (2025) | USD 1.56 Billion |

| Market Size (2026) | USD 1.61 Billion |

| Market Size (2031) | USD 3.14 Billion |

| Growth Rate (2026 - 2031) | 14.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Power EPC Market Analysis by Mordor Intelligence

The Nigeria Power EPC Market size is projected to expand from USD 1.56 billion in 2025 and USD 1.61 billion in 2026 to USD 3.14 billion by 2031, registering a CAGR of 14.29% between 2026 to 2031.

Transmission & Distribution EPC is expected to expand faster than generation, rising from USD 0.63 billion in 2025 to USD 1.32 billion in 2031 on a 15.94% growth, as regulators prioritize evacuation and grid‐loss reduction over raw generation additions.[1]Nigerian Electricity Regulatory Commission, “Order on Performance Improvement Plan for the Transmission Company of Nigeria Plc and the Nigerian Independent System Operator,” nerc.gov.ng Renewables already command the majority of generation EPC value, aided by concessional climate finance that trims project discount rates by up to 400 basis points.[2]World Bank Group, “DARES Program for Nigeria,” worldbank.org At the same time, 28 newly licensed gas-flare commercialization ventures promise 3 GW of captive capacity that will deepen the project pipeline for mid-sized EPC contracts.[3]Federal Republic of Nigeria, “Presidential Directive on Local Content Compliance Requirements,” nuprc.gov.ng Execution risk persists, however, as the Naira’s cumulative devaluation in 2024-2025 inflated imported switchgear and turbine costs by as much as 50%, while militant disruptions in the Niger Delta briefly cut gas feedstock to Nigeria LNG by 80% in March 2025.

Key Report Takeaways

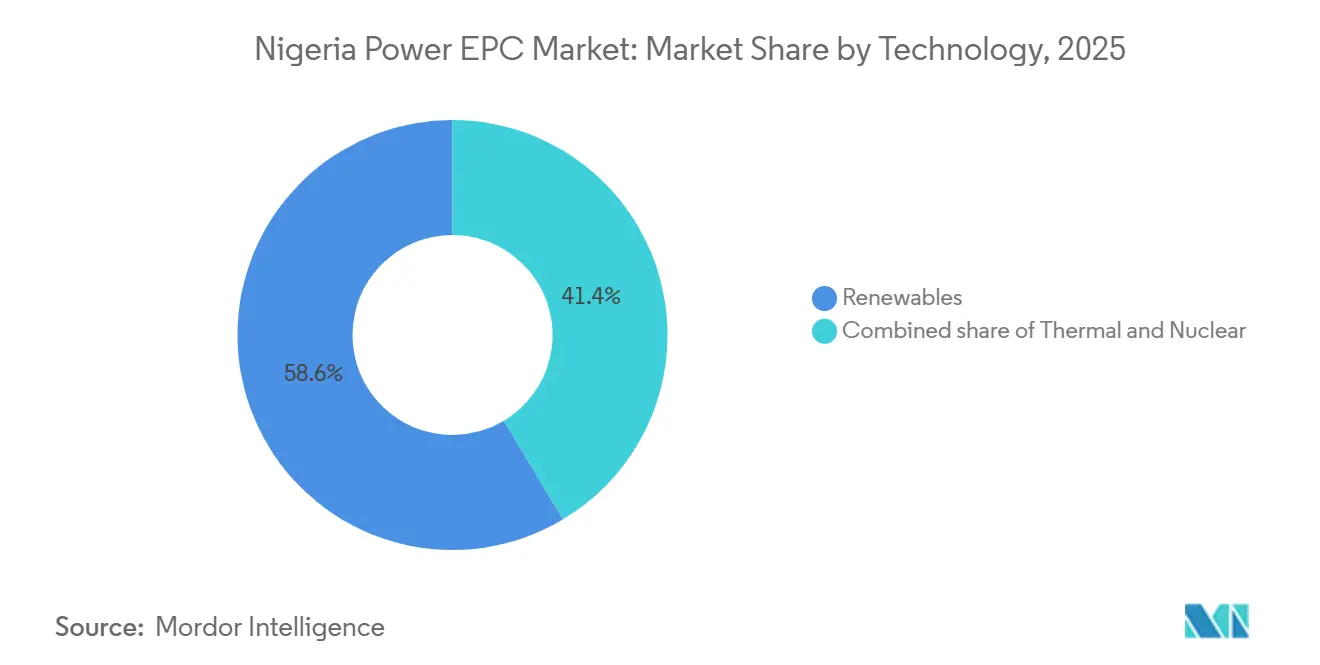

- Nigeria's power EPC market is segmented into power generation EPC and power transmission and distribution (T&D) EPC. Power generation EPC accounted for 60.9% of the market in 2025, while power transmission and distribution (T&D) EPC is projected to grow at a 15.94% CAGR through 2031.

- By technology, renewables led with 58.6% revenue share in 2025; thermal posted the slowest growth, while renewable EPC is tracking a 22.5% CAGR to 2031.

- By capacity band, the 100 MW–499 MW segment accounted for 51.5% of the Nigerian power generation EPC market share in 2025, whereas sub-100 MW projects are forecast to expand at an 18.1% CAGR through 2031.

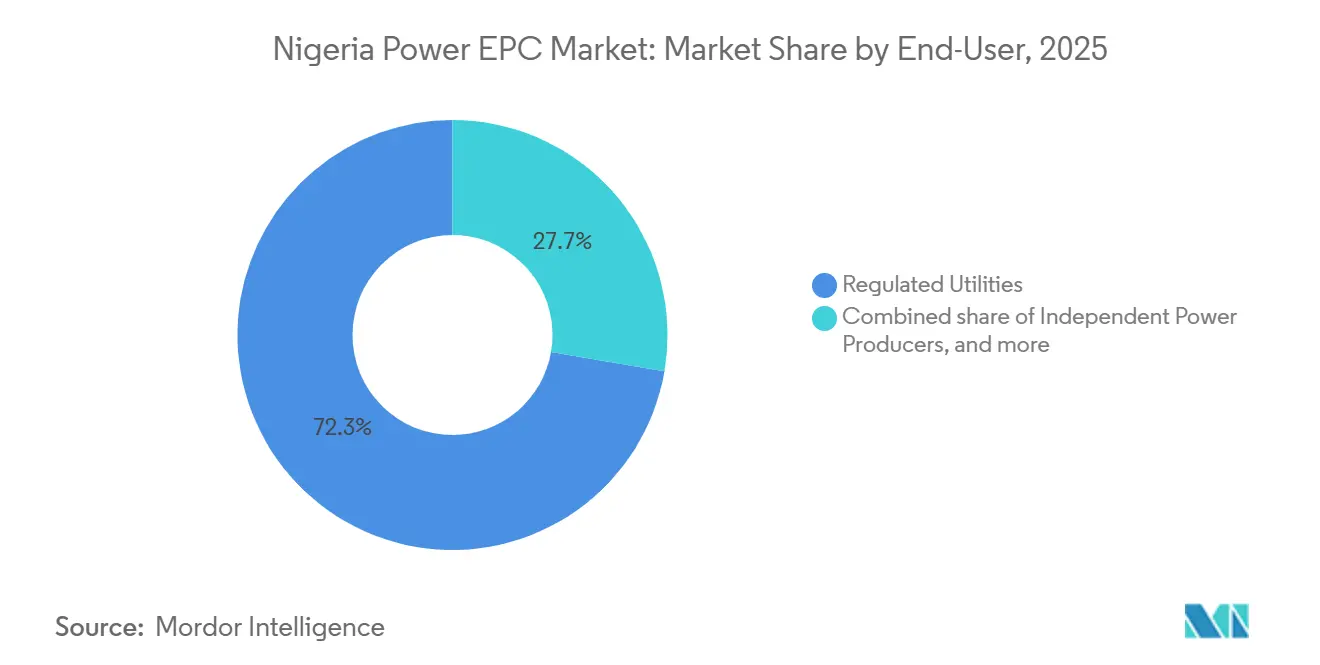

- By end user, regulated utilities held 72.3% of the 2025 value, and the same is advancing at a 16.7% CAGR to 2031.

- Sinohydro, CCECC, and PowerChina together captured about 45% of 2025 turnkey utility-scale awards, underpinned by vendor financing from China Exim Bank.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nigeria Power EPC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in NIPP Phase-II project pipeline | +3.2% | Lagos, Rivers, Kano, Kaduna | Medium term (2-4 years) |

| National Electrification Project mini-grid roll-outs | +2.8% | Rural and peri-urban zones | Medium term (2-4 years) |

| Multilateral climate-finance inflows | +2.5% | Nationwide | Long term (≥ 4 years) |

| Gas-flare commercialization enabling captive IPPs | +1.9% | Niger Delta, industrial hubs | Short term (≤ 2 years) |

| Digital sub-station retrofits | +1.4% | Urban distribution networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in NIPP Phase-II Project Pipeline

The second phase of the National Integrated Power Project is steering capital toward 100 MW–499 MW gas-fired and hybrid solar assets, the same band that already holds 51.5% of 2025 EPC value. State co-financing trims sovereign risk and accelerates financial close, while the regulator’s May 2025 approval of NGN 82.66 billion for matching transmission lines reduces the chances of stranded generation.[4]Nigerian Electricity Regulatory Commission, “First-Quarter 2024 Report,” nerc.gov.ng Large turnkey contractors benefit because integrated engineering, procurement, and construction slots compress timelines and shift cost-overrun risk to the contractor.

National Electrification Project Mini-Grid Roll-Outs

Performance-based grants funded by the USD 750 million DARES facility pay out against metered connections and uptime, shifting incentives from asset delivery to system reliability. The model favors experienced mini-grid integrators bundling solar PV, lithium-ion storage, and smart metering. Because most hardware can now be sourced in Naira, developers avoid the foreign-exchange exposure that plagues grid-scale imports.

Multilateral Climate-Finance Inflows

Concessional debt from the World Bank, AfDB, and British International Investment lowers the weighted average cost of capital by 200-400 basis points, spurring solar and wind EPC even in Nigeria’s high-discount-rate environment. The same lenders also back distribution automation and metering programs that improve collections and free up revenues for further EPC work. State governments are starting to tap these facilities directly, leveraging new autonomy under the 2023 Electricity Act.

Gas-Flare Commercialization Enabling Captive IPPs

Licenses issued to 28 firms turn what used to be a penalty into a feedstock advantage, unlocking about 3 GW of new captive power. Industrial offtakers such as Dangote can now lock in low-cost gas priced in Naira, insulating projects against currency slides. Local-content rules embedded in the February 2024 Presidential Directive further tilt awards toward Nigerian-owned fabricators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Naira depreciation & FX liquidity crunch | −2.1% | Nationwide | Short term (≤ 2 years) |

| Militant activity in Niger Delta | −1.3% | Niger Delta | Short term (≤ 2 years) |

| Local-content rules inflating BoQ costs | −0.9% | Nationwide | Medium term (2-4 years) |

| Grid evacuation limits capping PPAs | −1.6% | Lagos, Kano, Port Harcourt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Naira Depreciation & FX Liquidity Crunch

The local currency’s 2024-2025 slide inflated imported turbine and transformer costs by as much as 50% and delayed letters of credit, pushing many EPC contractors to demand USD-denominated mobilization fees. Distribution companies’ collection rate of 79.11% still leaves cash gaps, compelling greater reliance on donor-funded projects that lengthen procurement cycles.

Grid Evacuation Limits Capping PPAs

Despite a nominal 6,000 MW wheeling capacity, the grid suffered 12 collapses in 2024, curbing purchase agreements for new generation. Phase 1 of the Siemens-led Presidential Power Initiative will add 7,140 MW of capacity only by 2027, prolonging the underutilization of existing plants and constraining renewable curtailment risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Renewables Gain Ground on Thermal

Renewables comprised 58.6% of power generation EPC value in 2025, and the segment is forecast to widen on a 22.5% CAGR as multilateral funds cheapen project finance and industrial offtakers chase carbon targets. The Nigeria Power Generation EPC market size attributable to renewables will therefore more than double by 2031, while thermal contracts grow modestly on grid-services demand. Solar-plus-storage hybrid mini-grids now offer 95%-plus uptime, a reliability level the national grid still cannot match.

Gas remains the lowest-cost dispatchable fuel, so thermal EPC still underpins baseload needs, but Niger Delta pipeline sabotage weighed heavily in 2025. Turbine OEMs mitigate that risk by embedding long-term service agreements into bids, cushioning revenue even when capacity factors falter. Meanwhile, nuclear remains aspirational; feasibility studies have yet to secure lender interest for the twenty-year payback horizon.

By Capacity Band: Distributed Assets Accelerate

Projects in the 100 MW–499 MW band captured 51.5% of the Nigerian Power Generation EPC market share in 2025, supported by NIPP Phase-II and IPP gas projects. Yet sub-100 MW assets, especially solar-hybrid mini-grids, will be the fastest-growing slice at an 18.1% CAGR through 2031. Larger than 500 MW builds, such as the 700 MW Zungeru hydro plant, remain pivotal for grid inertia but face decade-long timelines and heavy FX exposure.

Distributed generation is democratizing capacity additions; over 250 enterprises now operate a combined 6,500 MW of captive plants, surpassing average grid dispatch. The Electricity Act 2023 eased licensing, and Q1 2024 alone saw nine new captive permits totaling 52.57 MW. As the grid struggles, more factories and campuses will defect into this tier.

By End User: Utilities Dominate but Captive Demand Surges

Regulated utilities absorbed 72.3% of 2025 EPC spend, sustained by statutory procurement obligations and state backing. They are projected to maintain a 16.7% CAGR, yet the Nigeria Power Generation EPC market share commanded by utilities will erode mildly as private offtakers self-generate.

Industrial captive owners already exceed grid output, led by Dangote’s 1,500 MW fleet. Gas-flare IPPs further boost this class by securing low-cost, Naira-priced fuel. Independent power producers leverage bilateral contracts with creditworthy factories, bypassing cash-strapped distribution companies. Public institutions are experimenting with energy-as-a-service micro-grids to avoid upfront capital.

Geography Analysis

Lagos consumes roughly 40% of national electricity and therefore attracts the bulk of T&D EPC, with high-profile projects like Eko Atlantic demanding 99% supply reliability. Rivers and Akwa Ibom draw gas-flare IPP investment yet remain vulnerable to pipeline sabotage, a risk that elevates insurance and security costs. Northern corridors such as Abuja-Kaduna benefit from the Siemens initiative’s 7,140 MW wheeling upgrade budget.

Mini-grid roll-outs under the National Electrification Project concentrate on low-access states such as Benue and Taraba, spurring rural EPC clusters. States now hold licensing power, and early movers Lagos and Kaduna have created power agencies that speed approvals. Meanwhile, 129 federal transmission projects worth NGN 1.7 trillion target Lagos-Ibadan, Port Harcourt-Aba, and Abuja-Kaduna corridors to relieve congestion.

Execution risk is asymmetric: Lagos and Abuja offer superior logistics and skilled labor, while remote northern and southeastern states face longer mobilization times. Contractors price that differential into bids, making geographic diversification a balancing act between revenue potential and cost overruns.

Competitive Landscape

Chinese SOEs hold a pricing edge, bundling 15%-25% cheaper vendor financing; Sinohydro’s USD 1.3 billion Zungeru hydro win exemplifies the model. European OEMs such as Siemens Energy and GE Vernova prioritize equipment supply and multiyear service revenue. Siemens’s Presidential Power Initiative, already 90% complete in its pilot, underpins a USD 328.8 million Phase 1 contract for 544 km of new lines.

Local champion Julius Berger proved competitive by finishing the 459 MW Azura-Edo IPP ahead of schedule, a feat that meets the February 2024 local-content directive requiring “genuine, substantial and tangible” in-country capacity. Schneider Electric’s 2024 Lagos hub, with 250 staff positions, is for SCADA and micro-grid integration work.

White-space persists below 100 MW. Sterling & Wilson has an MoU for 961 MWp of solar plus 455 MWh storage, but still hunts for finance. Energy-as-a-service providers are emerging, targeting factories and campuses that lack balance-sheet capacity yet demand grid-independent power. As local-content enforcement tightens, foreign EPCs increasingly form joint ventures with Nigerian fabricators, raising near-term costs but deepening domestic capability.

Nigeria Power EPC Industry Leaders

Energo Nigeria Ltd.

Sterling and Wilson Nigeria Limited

Gentec EPC Ltd.

Sinohydro Corp.

Siemens Energy Nigeria

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: In April 2026, the International Finance Corporation (IFC) and Norfund announced expanded financing support for renewable mini-grid deployment in Nigeria. The initiative includes approximately 315 solar-hybrid mini-grid sites with an estimated capital expenditure of USD 271 million, offering significant EPC opportunities in rural electrification and distributed energy infrastructure.

- May 2025: NERC created a Transmission Infrastructure Fund financed by an NGN 2.17/kWh levy that will channel NGN 212.04 billion into 50 priority projects across Lagos, Kano, Kaduna, and Port Harcourt.

- April 2025: Siemens Energy reached 90% completion of its pilot phase, adding 821.6 MW of capacity and signing a USD 328.8 million Phase 1 construction contract.

- March 2025: Gas supply to Nigeria LNG fell 80% after sabotage shut three pipelines, underscoring upstream security risk.

- March 2025: Schneider Electric sealed a deal guaranteeing 99% power at Lagos’ Eko Atlantic smart city via an integrated substation and battery storage.

Nigeria Power EPC Market Report Scope

The power EPC market encompasses the global industry of companies that provide comprehensive execution of power generation, transmission, and distribution projects on a turnkey basis. EPC contractors handle engineering design, equipment procurement, construction, installation, testing, and commissioning of power infrastructure, ensuring project delivery aligns with agreed cost, time, and performance requirements.

The Nigeria power EPC market is segmented into power generation EPC and power transmission & distribution EPC. By power generation EPC, the market is segmented into technology, capacity band, and end-user. These segments are further divided as technology- thermal, nuclear, and renewables; capacity band- Up to 100 MW, 100-499 MW, Above 500 MW; end-user- regulated utilities, IPPs, industrial captive power, and public sector/SOE. For each segment, the market sizing and forecasts have been done based on revenue (USD Billion) for all the above segments.

Power Generation EPC

| By Technology | Thermal |

| Nuclear | |

| Renewables | |

| By Capacity Band | Up to 100 MW (DER, micro-grid) |

| 100 to 499 MW | |

| Above 500 MW | |

| By End-User | Regulated Utilities |

| Independent Power Producers | |

| Industrial Captive Power | |

| Public Sector and SOE |

| Power Generation EPC | By Technology | Thermal |

| Nuclear | ||

| Renewables | ||

| By Capacity Band | Up to 100 MW (DER, micro-grid) | |

| 100 to 499 MW | ||

| Above 500 MW | ||

| By End-User | Regulated Utilities | |

| Independent Power Producers | ||

| Industrial Captive Power | ||

| Public Sector and SOE | ||

Key Questions Answered in the Report

What is the current value of the Nigeria Power EPC market?

The market stands at USD 1.61 billion for 2026 and is forecast to reach USD 3.14 billion by 2031.

Which segment is growing fastest within Nigeria's EPC space?

Sub-100 MW distributed generation, especially solar-hybrid mini-grids, is expanding at an 18.1% CAGR through 2031.

How are foreign-exchange swings affecting EPC contracts?

The Naira's depreciation raised imported equipment costs up to 50%, prompting contractors to price bids in USD and demand hard-currency mobilization fees.

Which companies dominate utility-scale projects?

Chinese SOEs such as Sinohydro, CCECC and PowerChina jointly capture roughly 45% of large turnkey contracts, leveraging concessional vendor finance.

Why is renewable EPC outpacing thermal?

Concessional climate finance, falling solar costs and industrial buyers' grid defection are driving renewables at a 22.5% CAGR versus slower growth for gas-fired plants.

What policy is most influential for mini-grid expansion?

The National Electrification Project's performance-based grants, supported by the USD 750 million DARES facility, directly subsidize reliable rural mini-grids.

Page last updated on: