Nigeria Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

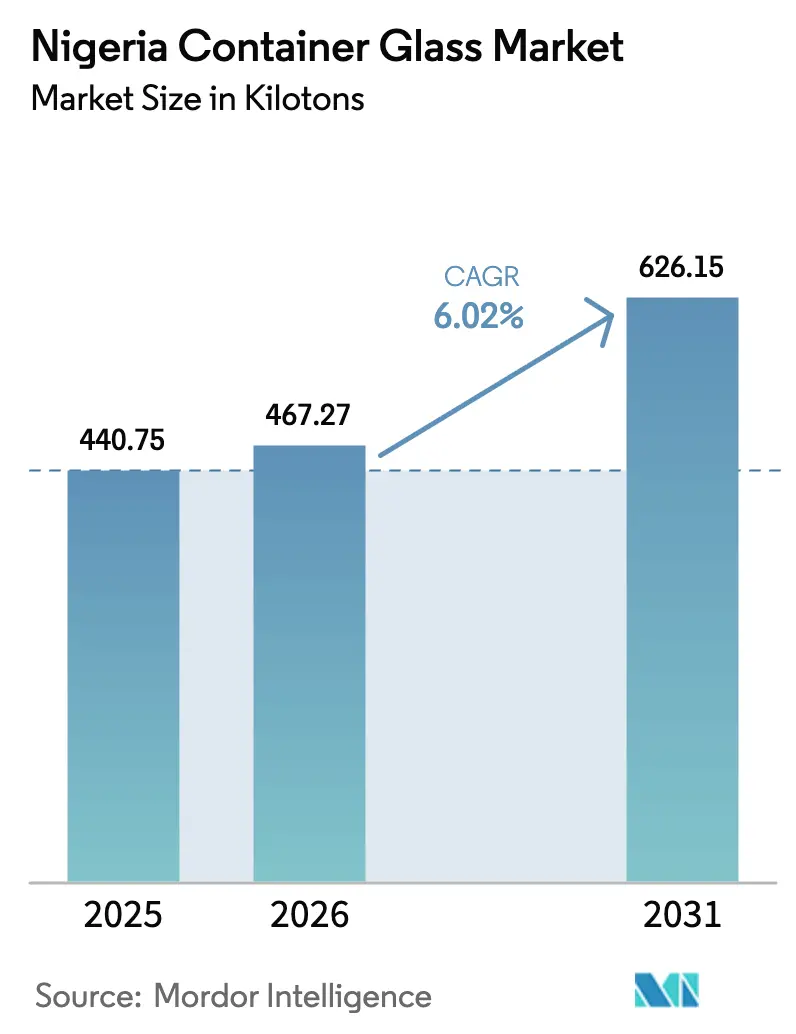

| Base Year Market Size (2025) | 440.75 kilotons |

| Market Volume (2026) | 467.27 kilotons |

| Market Volume (2031) | 626.15 kilotons |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

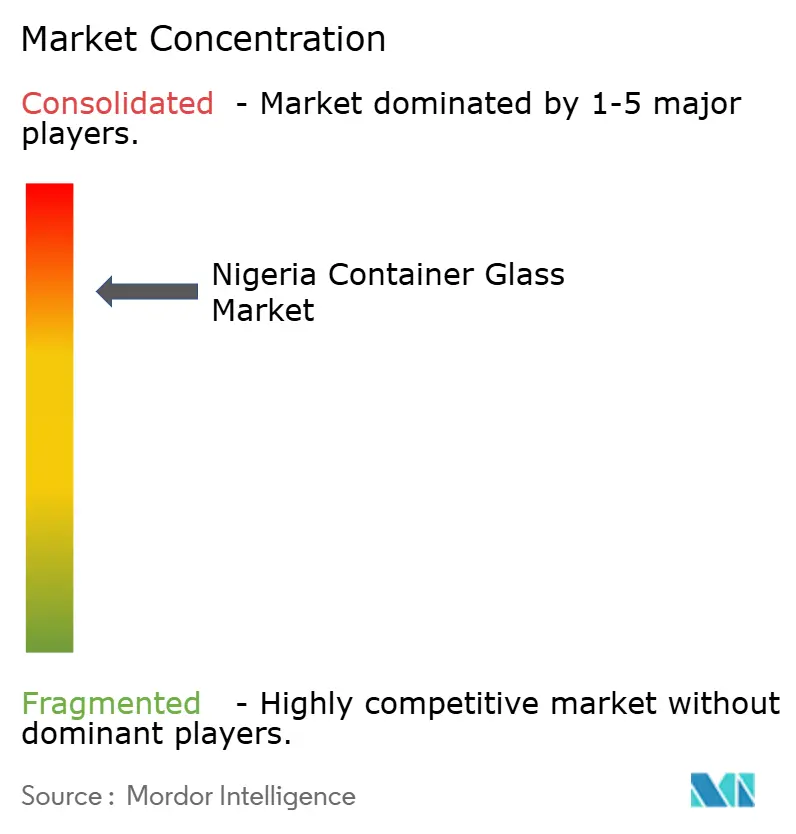

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Container Glass Market Analysis by Mordor Intelligence

The Nigeria container glass market size was valued at 440.75 kilotons in 2025 and estimated to grow from 467.27 kilotons in 2026 to reach 626.15 kilotons by 2031, at a CAGR of 6.02% during the forecast period (2026-2031). Robust consumer spending on beverages, regulatory incentives that favor local sourcing, and capacity additions by leading manufacturers keep the growth curve firmly positive. Rising premiumization in beer and spirits encourages brand owners to trade up from PET to glass, while NAFDAC’s ban on alcohol sachets and bottles below 200 ml concentrates volume in larger, returnable formats that domestic producers can supply efficiently. Tax holidays of up to five years for glassmaking and priority treatment in government procurement lower the effective cost of new furnaces, further anchoring local investment. Currency-driven inflation in plastic and aluminum has strengthened glass’s relative price competitiveness, and corporate environmental targets linked to reuse and recyclability amplify demand for returnable bottles across mainstream and premium beverage lines.

Key Report Takeaways

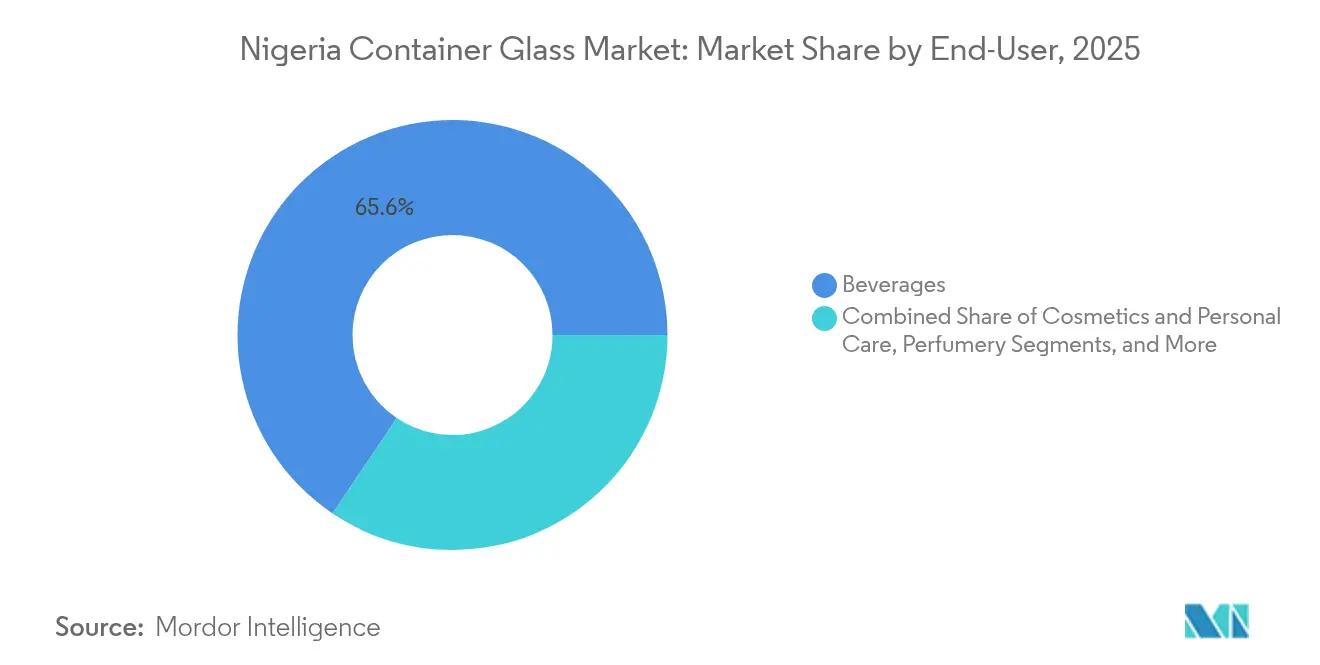

- By end-user, beverages captured 65.58% of the Nigeria container glass market share in 2025.

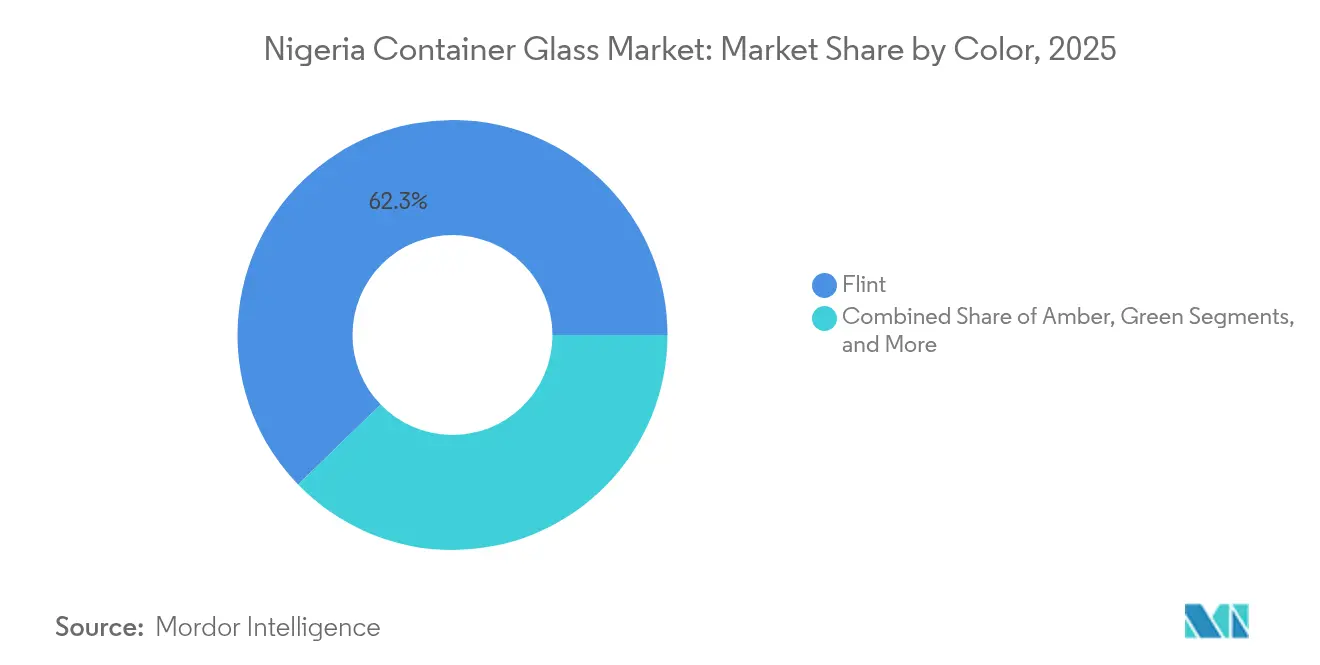

- By color, the Nigeria container glass market for amber glass is projected to grow at a 7.74% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing food-and-beverage consumption boom | +1.8% | Nationwide, especially Lagos, Kano, Port Harcourt | Medium term (2-4 years) |

| Expansion of premium and mainstream beer volumes | +1.2% | Urban hubs Lagos, Abuja, Ibadan | Short term (≤ 2 years) |

| Government incentives for local manufacturing | +0.9% | Industrial zones Agbara, Onne | Long term (≥ 4 years) |

| AfCFTA-driven export upside within ECOWAS | +0.7% | Ghana, Côte d’Ivoire gateway markets | Long term (≥ 4 years) |

| Shift to returnable glass to offset packaging inflation | +0.6% | Beverage distribution networks country-wide | Medium term (2-4 years) |

| Commissioning of energy-efficient electric furnaces | +0.4% | Existing factory clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Food-and-Beverage Consumption Boom

Household spending on branded beverages continues to outpace population growth as urban consumers shift toward bottled water, functional drinks, and ready-to-drink coffee lines that rely on glass for both shelf appeal and product integrity. Bottled water alone logged a 46% year-over-year volume increase in 2025, and brand owners cite glass’s inert barrier and premium feel as key conversion triggers from PET in the middle-income segment. Clean-label claims, transparent ingredient lists, and a desire for visible product quality further encourage formulators to opt for clear flint bottles that showcase color and purity. The Nigerian container glass market, therefore, gains from both trading up within existing categories and from entirely new beverage launches targeting health-conscious shoppers in megacities.

Expansion of Premium and Mainstream Beer Volumes

Nigeria is Africa’s second-largest beer market by value, and the Heineken-backed Nigerian Breweries, coupled with Tolaram’s newly acquired Guinness Nigeria, now run multi-site networks that collectively bottle over 17 million hl per year, nearly all in returnable glass.[1]Heineken N.V., “2024 Annual Report,” theheinekencompany.com Premium SKUs, such as Heineken Silver, utilize distinctive, thicker flint bottles for brand differentiation, whereas mainstream lagers maintain high glass reuse ratios to keep unit costs low amid inflation. Newly inked renewable-energy power purchase agreements at two off-grid breweries underscore long-term confidence in glass packaging, as bottle return loops remain viable only when production remains local and continuous.

Government Incentives for Local Manufacturing and Backward Integration

The Nigeria First Policy mandates procurement preference for domestically manufactured containers in all publicly funded beverage and pharmaceutical contracts, effectively reserving a baseline of institutional demand for local bottle makers. Pioneer-status tax holidays slash headline corporate tax to zero for up to five years, while Export Expansion Grants refund as much as 15% of invoiced export value, cushioning the capital burden of new melting tanks. Obligations to source inputs locally wherever feasible bolster domestic silica sand quarrying, and technology-transfer clauses in supply agreements accelerate skill development among Nigerian furnace operators.

AfCFTA and ECOWAS Export-Led Growth Potential

Nigeria already represents 77% of ECOWAS exports by value, and the elimination of tariffs under the African Continental Free Trade Area widens the addressable pool for glass containers used by Nigerian beverage brands expanding into Ghana, Côte d’Ivoire, and Senegal. Even with logistics bottlenecks in border regions, guided-trader corridors reduce documentary compliance time, making the inter-country movement of filled beverages and empty flint bottles easier. Early adopters among craft-beer start-ups in Accra have begun placing mid-sized orders with Nigerian container suppliers for amber bottles designed for UV-sensitive recipes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs and infrastructure deficits | −1.4% | Nationwide, pronounced outside industrial hubs | Medium term (2-4 years) |

| Extreme currency volatility and FX scarcity | −1.1% | Import-dependent operations country-wide | Short term (≤ 2 years) |

| Variable cullet quality disrupting furnace yields | −0.8% | Major recycling catchment areas | Medium term (2-4 years) |

| Import reliance for soda ash and specialty inputs | −0.9% | All glass plants | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production Costs and Infrastructure Deficits

Continuous furnaces cannot afford unscheduled shutdowns, yet chronic grid outages oblige plant owners to run diesel or LNG gensets, raising energy spend to as much as 25% of cash operating cost versus 10-12% in peer markets. Congested ports and multi-agency checkpoints along the Lagos-Calabar road inflate inbound freight for soda ash and outbound trucking of finished bottles. Consequently, the Nigerian container glass market sacrifices margins that could otherwise be reinvested in furnace rebuilds, thereby tempering the pace of capacity additions.

Extreme Currency Volatility and FX Scarcity

A 56% slide in the naira’s official rate between 2024 and 2025, compounded by sporadic Central Bank intervention, leaves glassmakers scrambling for hard currency at parallel-market premiums to pay for soda ash, cullet, and refractory bricks. The mismatch between import costs and naira-denominated selling prices squeezes working capital cycles; some converters now negotiate quarterly price resets with beverage clients to hedge their risk. Simultaneously, the higher tariffs on glassware imports announced by the Nigeria Customs Service aim to protect local furnaces, but also raise the landed cost of spare parts, thereby tightening the operational vice.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverages Sustain Volume; Cosmetics Accelerate Upside

The beverages category retained a 65.58% share of the Nigerian container glass market in 2025, underpinned by strong demand for beer, flavored malt, and bottled water. Within the segment, NAFDAC’s prohibition on containers below 200 ml redirected demand to 325 ml and 600 ml returnable bottles, thereby increasing the Nigerian container glass market size for beverages to 289.1 kilotons in 2025. The pivot also unlocked economies of scale that cushioned producers against FX-linked soda-ash price spikes. Over the forecast horizon, bottled water and functional beverages are expected to expand their market share, driven by health cues and the sensory premium associated with clear flint glass.

Cosmetics and personal care advance at an 8.02% CAGR, the highest among end-users, albeit from a modest base of 18.4 kilotons in 2025. Rising middle-class incomes are catalyzing demand for serums, fragrances, and skin-lightening creams, whose formulations require inert, non-leaching packaging. Global beauty brands entering Nigeria often harmonize their SKUs with Pan-African rollouts, resulting in long-term orders for high-clarity vials and specialty blue or frosted jars. The trend supports the incremental diversification of Nigeria's container glass industry beyond its beverage backbone.

By Color: Flint Dominates; Amber Outpaces

Flint bottles accounted for 62.25% of Nigeria's container glass market share in 2025, equivalent to 274.4 kilotons that year. Clear containers are ideal for water, spirits, and premium soft drinks, where shelf visibility reinforces trust and supports brand storytelling. Their high throughput on existing lines sustains operational efficiency, making Flint the default for any new beverage line extension.

Amber bottles, however, are forecast to clock an 7.74% CAGR through 2031 as pharmaceutical fillers, craft brewers, and cold-brew coffee makers prefer the UV shielding they provide. This upswing is expected to increase Amber’s share of the Nigerian container glass market size to 168.2 kilotons by 2031, which will tighten furnace scheduling, as Amber glass typically operates on dedicated tank days to prevent color seeding issues.

Geography Analysis

Southern industrial corridors anchor manufacturing, with Agbara in Ogun State and the Lagos Free Zone hosting two of the nation’s four large furnaces. Lagos alone accounted for 40.62% of nationwide bottle sales in 2025, reflecting its dense concentration of beverage, cosmetic, and pharmaceutical manufacturers. The Nigerian container glass market, therefore, benefits from the state’s port facilities, skilled labor pool, and proximity to recycling aggregators that supply cullet to plants.

Northern demand clusters around Kano, Kaduna, and Abuja, where rising disposable income boosts bottled-water and mainstream-beer consumption. Logistics costs remain an issue for flint bottles moving northbound; however, brewers offset freight through returnable pools that are transported back by rail and road. Consequently, the north is on track to expand the Nigeria container glass market size by 6.88% CAGR through 2031.

Regional export prospects hinge on ECOWAS protocols that waive duties for goods of community origin. Ghana and Côte d’Ivoire together imported an estimated 22 kilotons of Nigerian glass in 2025, a 9% increase year-over-year, despite border-post delays. Ongoing upgrades to the Lagos-Badagry expressway and the forthcoming Lekki Deep-Sea Port are expected to reduce transit time, thereby improving the competitiveness of the Nigerian container glass market in Francophone West Africa.

Competitive Landscape

The field is moderately fragmented, with Beta Glass, Frigoglass Nigeria, and Ardagh Glass Nigeria collectively holding roughly 48% of the rated melting capacity, leaving ample room for niche specialists and imports. Each of the top three players now operates proprietary returnable-bottle pools for anchor clients, such as Nigerian Breweries and Coca-Cola HBC, creating stable demand pipelines. Capacity expansion favors electric-boosted furnaces that curb CO₂ emissions by up to 60%, mirroring Verallia’s 100% electric unit in France, a technology Nigerian operators are currently evaluating for future rebuilds.

Sustainability credentials form a fast-emerging competitive lever. Coca-Cola HBC has opened a dedicated collection hub capable of processing 13,000 tonnes of PET annually, signaling to glass suppliers that circularity metrics will soon extend to returnable glass loops. In response, Beta Glass rolled out a pilot cullet-buyback scheme in Lagos mid-2025, targeting a 20% cullet ratio in its clear-glass tank by 2027.

Disruptors such as Igo Glass Recyclers focus exclusively on 100% recycled, small-volume tableware lines, but their proof-of-concept furnaces demonstrate the feasibility of closed-loop supply in Nigeria. Long-standing cost headwinds from imported soda ash have prompted larger players to explore joint ventures with East African producers, aiming to localize at least part of the supply chain by 2028.

Nigeria Container Glass Industry Leaders

Frigoglass Industries (Nigeria) Limited

Ardagh Glass Packaging Nigeria Limited

The Chagoury Group

Beta Glass Nigeria Plc.

Technoglass Industries Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Federal Executive Council approved the Nigeria First Policy, which locks in procurement preferences for locally made glass containers across all ministries.

- January 2025: Coca-Cola HBC opened Nigeria’s first company-run packaging collection hub and invested EUR 9.5 million (USD 10.2 million) in returnable-glass lines at its Ikeja plant.

- August 2024: Heineken Nigeria signed renewable-energy PPAs covering two breweries, improving Scope 2 performance for returnable bottle loops.

- June 2024: Tolaram purchased Diageo’s 58.02% stake in Guinness Nigeria for NGN 103 billion (USD 69 million), cementing long-term supply contracts with domestic bottle makers.

Nigeria Container Glass Market Report Scope

Container glass is designed for manufacturing glass containers, including bottles, jars, drinkware, and bowls. Its key attributes include chemical inertness, sterility, and non-permeability, rendering it especially sought after in the beverage, food, pharmaceutical, and cosmetic sectors. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

Nigeria container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the current volume of the Nigeria container glass market?

It totaled 467.27 kilotons in 2026 and is on course for 626.15 kilotons by 2031.

How fast is demand for cosmetic and personal-care glass packaging growing in Nigeria?

The segment is projected to expand at an 8.02% CAGR through 2031, the highest among all end-users.

Why are amber bottles gaining share in Nigeria?

Amber containers protect light-sensitive formulations in pharmaceuticals and craft beverages, driving an 7.74% CAGR for this color variant.

How does the Nigeria First Policy affect local glass manufacturers?

It grants procurement preference and tax holidays of up to five years, lowering the cost of new capacity and ensuring baseline domestic demand.

What are the main cost challenges for glass producers in Nigeria?

High energy costs due to unreliable grids and FX-driven price swings for imported soda ash increase operating expenses.

Which regions beyond Nigeria import Nigerian glass bottles?

Ghana and Côte d’Ivoire are the primary destinations, together absorbing roughly 22 kilotons of Nigerian bottles in 2025.

Page last updated on: