Multi Cancer Early Detection Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

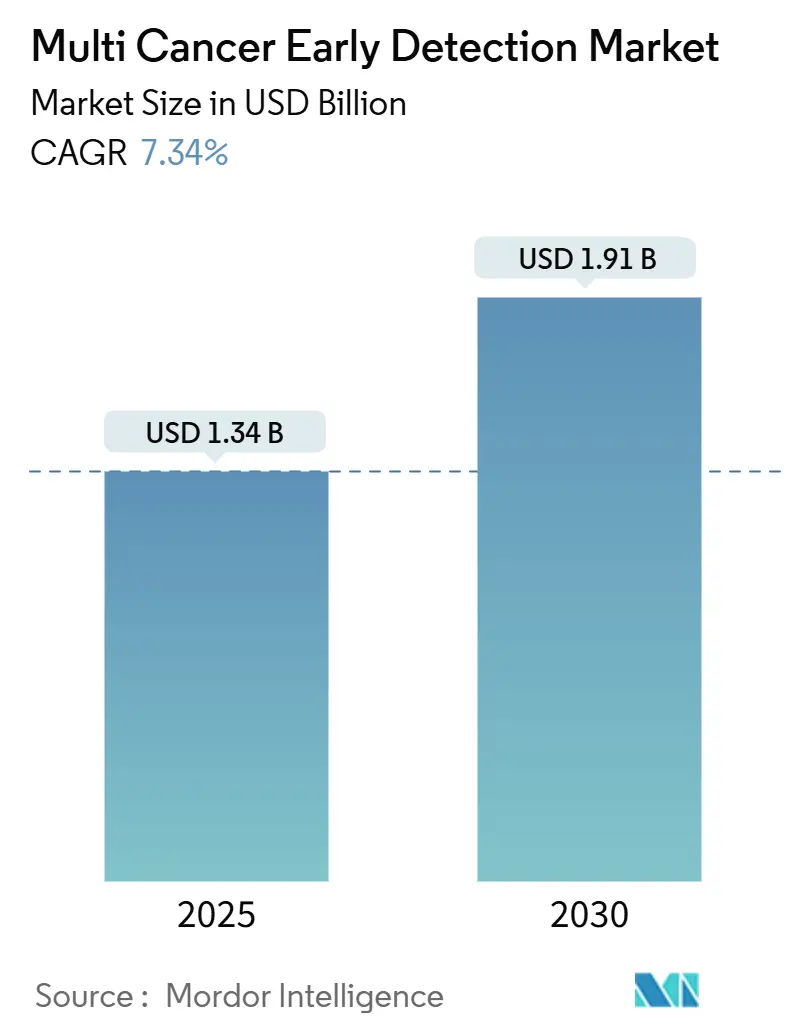

| Market Size (2025) | USD 1.34 Billion |

| Market Size (2030) | USD 1.91 Billion |

| Growth Rate (2025 - 2030) | 7.34% CAGR |

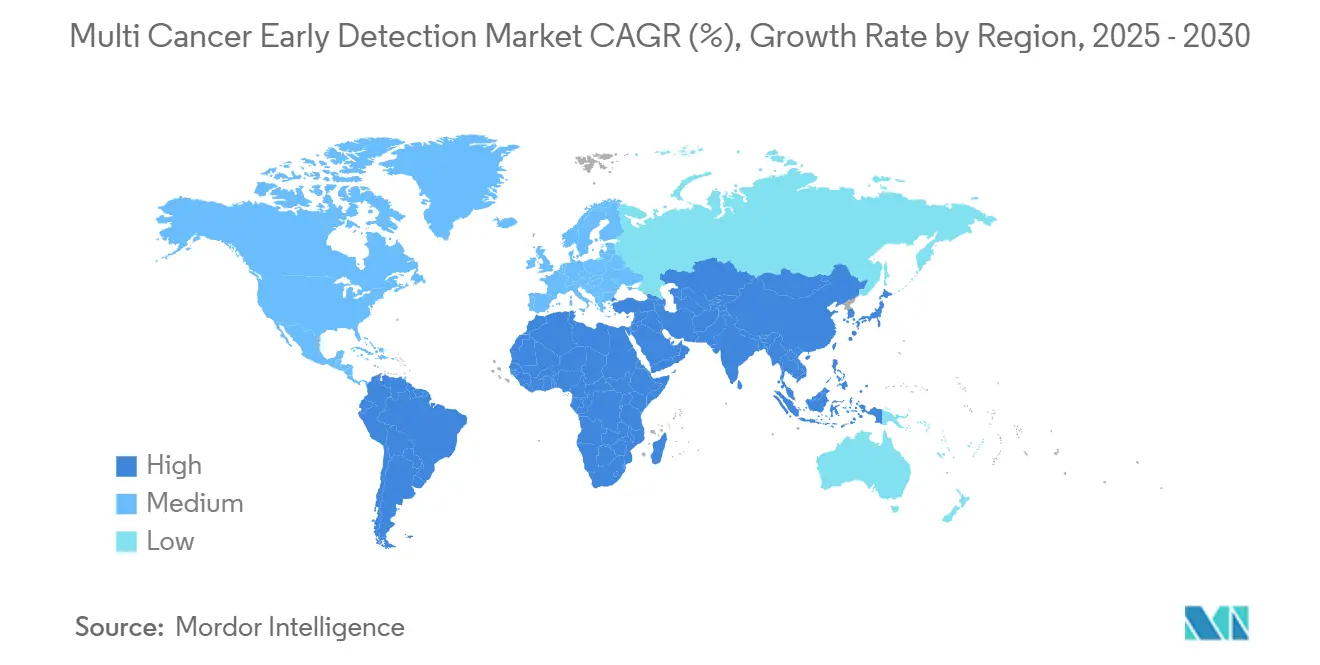

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi Cancer Early Detection Market Analysis by Mordor Intelligence

The multi-cancer early detection market size stood at USD 1.34 billion in 2025 and is forecast to reach USD 1.91 billion by 2030, advancing at a 7.34% CAGR. Rapid cost declines in circulating cell-free DNA sequencing, a wave of U.S. FDA breakthrough device designations, and value-based care incentives that reward intervention at stage I rather than stage IV collectively underpin this growth. Health-economics models show that single-cancer screening protocols overlook 86% of malignancies, so providers view comprehensive blood-based panels as a direct response to that diagnostic blind spot. Gene-panel laboratory-developed tests dominate current ordering volumes, yet methylation-based next-generation sequencing workflows now achieve clinical sensitivity that satisfies payer evidence thresholds. Employers that self-fund health benefits are emerging as key early adopters because they capture every avoided chemotherapy dollar over an employee’s tenure.

Key Report Takeaways

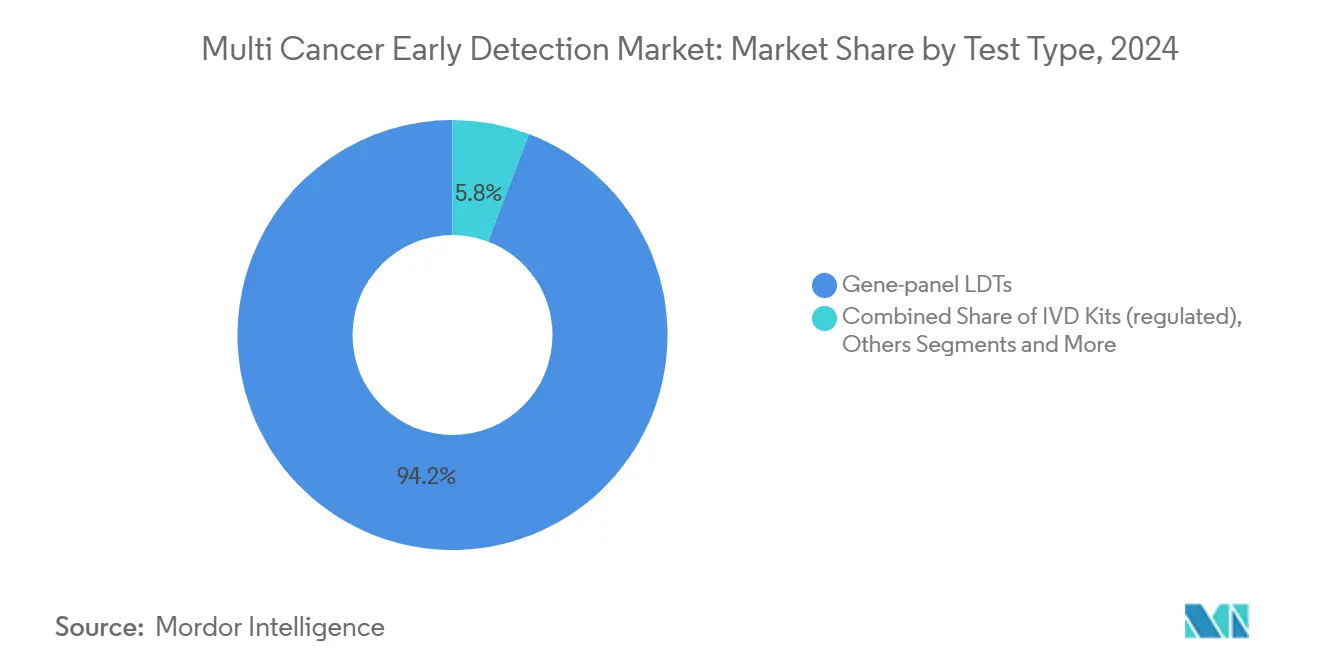

- By test type, gene-panel laboratory-developed tests led with 94.21% of multi-cancer early detection market share in 2024.

- By biomarker class, cfDNA methylation captured 63.24% share of the multi-cancer early detection market size in 2024 and is forecast to expand at a 9.32% CAGR through 2030.

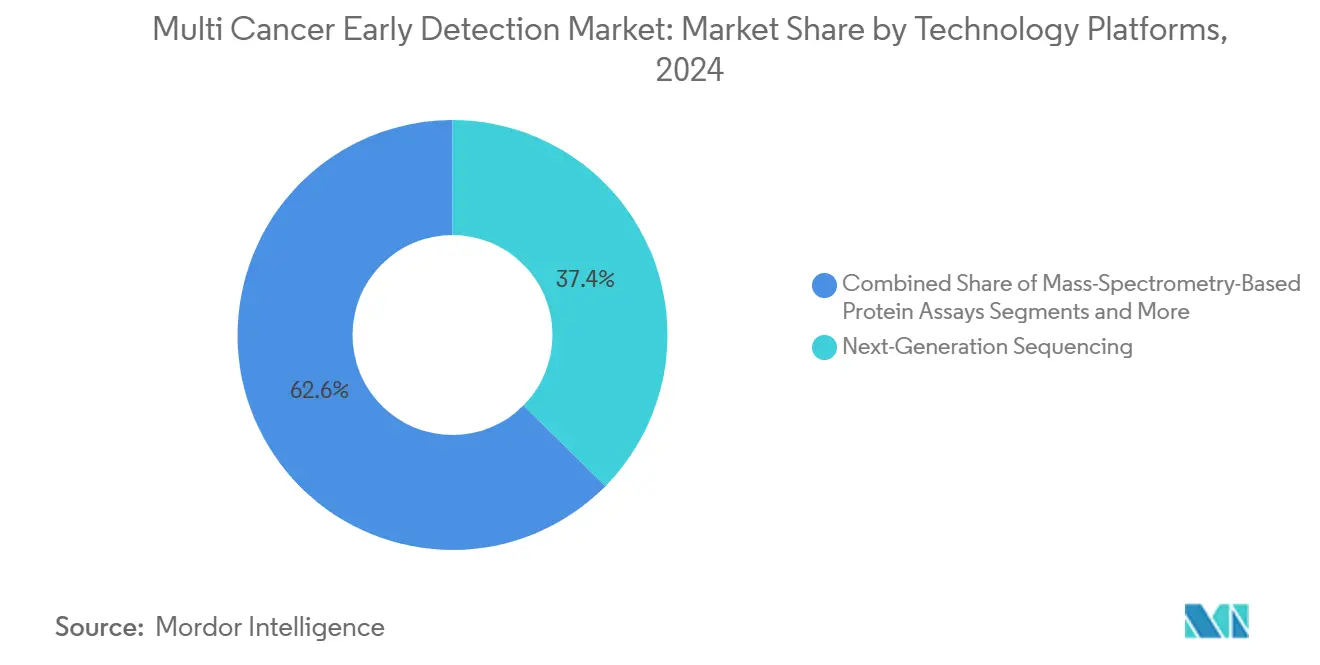

- By technology platform, next-generation sequencing accounted for 37.41% of the multi-cancer early detection market size in 2024, while AI-enabled multi-omics analytics is projected to grow at 10.72% CAGR between 2025 and 2030.

- By end-user, hospitals and academic medical centers held 47.63% of multi-cancer early detection market share in 2024; specialty oncology and diagnostic clinics are recording the highest projected CAGR at 11.45% through 2030.

- North America controlled 32.31% of multi-cancer early detection market share in 2024, whereas Asia-Pacific is the fastest-growing region with a 9.32% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Multi Cancer Early Detection Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of hard-to-screen cancers | +1.2% | North America and Europe highest, global relevance | Medium term (2-4 years) |

| Rapid cfDNA-methylation NGS cost compression | +0.9% | North America and Asia-Pacific | Short term (≤ 2 years) |

| FDA breakthrough designations & CMS pilots | +0.8% | Primarily United States, spillover into Europe | Short term (≤ 2 years) |

| Self-insured employers adding MCED benefits | +0.7% | United States, emerging in Europe | Medium term (2-4 years) |

| AI-powered multi-omics fusion | +0.6% | Developed markets first, global in long run | Long term (≥ 4 years) |

| Subscription-based longevity clinics | +0.4% | North America and Europe, Asia-Pacific nascent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Hard-to-Screen Cancers & Demand for Non-Invasive Population Screening

Pancreatic, ovarian, and lung cancers account for more than 400,000 new U.S. diagnoses each year, yet none has a widely accepted population-level screen. GRAIL’s PATHFINDER trial showed that a single blood draw can detect molecular signals from over 50 tumor types at an early stage, demonstrating clinical utility that traditional imaging lacks. Value-based providers calculate that stage I treatment is USD 60,000 less per patient than stage IV, creating a direct incentive to incorporate multi-cancer panels into annual exams. The economic argument resonates with accountable care organizations responsible for lifetime member costs. Health systems are therefore shifting budgets from late-stage therapeutics toward preventive liquid biopsy programs. Employers view the same data through a productivity lens, recognizing that an early diagnosis reduces absenteeism and disability payments.

Rapid Advances in cfDNA-Methylation NGS Workflows and Reagent Cost Compression

Illumina’s 2024 NovaSeq X reduced sequencing cost per gigabase by half compared with its predecessor, dropping the blended reagent cost of a 50-cancer methylation panel below USD 500.[1]Illumina, “Illumina completes the divestiture of GRAIL,” investor.illumina.comBurning Rock Biotech leveraged those gains to obtain breakthrough device status in both China and the United States for its OverC assay, underscoring global regulatory momentum. Methylation signatures are stable across tumor evolution and include tissue-of-origin clues that facilitate diagnostic triage, so clinicians prefer them over mutation-only panels. Lower run costs make it economically feasible for regional labs to install sequencers rather than send samples to distant reference centers. As price falls, payer actuaries can justify coverage because the cost-benefit ratio aligns with colonoscopy benchmarks. These dynamics collectively accelerate volume and open mid-income geographies to adoption.

Favorable FDA Breakthrough Device Designations & CMS Parallel Review Pilots

Shield from Guardant Health secured breakthrough status in 2024, triggering real-time feedback loops with regulators that shaved quarters off development timelines. Parallel CMS review allows pivotal trial data to serve both approval and reimbursement dossiers, eliminating the historic one-to-two-year reimbursement gap. Medicare’s 2025 payment updates broadened coverage for genetic screening tests that fill unmet need, sending a strong demand signal to commercial insurers.[2]Centers for Medicare & Medicaid Services, “Calendar Year 2025 Medicare Physician Fee Schedule Final Rule,” cms.gov This policy architecture rewards companies that pursue rigorous clinical endpoints early, thereby tilting the competitive field toward well-capitalized players. For providers, synchronized approval and reimbursement simplifies implementation planning because coding, billing, and compliance rules are known at product launch. Europe monitors U.S. progress closely and has begun fast-track evaluations under the EU In Vitro Diagnostic Regulation, indicating a trans-Atlantic regulatory alignment.

Self-Insured Employers Adding MCED Tests to Wellness Benefits

Curative Insurance bundled GRAIL’s Galleri test into its employer plans in 2025, positioning the assay as a workforce health hedge that can limit catastrophic oncology claims. Stage-I therapy averages USD 50,000 versus USD 150,000 for stage IV, and the employer pays both when self-funded. UnitedHealthcare expanded its Preventive Care Benefit to include liquid biopsy options for high-risk employees, citing strong interest among technology and financial-services firms. Adoption skews toward firms with older, higher-salary workforces where cancer prevalence and replacement-cost risk are greatest. Third-party administrators now pitch multi-cancer panels as a quantifiable return-on-investment tool rather than a wellness perk. As claims data accumulate, actuarial models will refine premium incentives that reward employers who deploy evidence-based screening.

Restraints Impact Analysis of Multi Cancer Early Detection Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High test price and limited reimbursement pathways | -1.8% | Global, strongest in emerging economies | Medium term (2-4 years) |

| False-positive / false-negative concerns and imaging demand | -1.1% | Worldwide, amplified in resource-constrained settings | Short term (≤ 2 years) |

| Equity and consent dilemmas in population genomic screening | -0.7% | North America and Europe, Asia-Pacific emerging | Long term (≥ 4 years) |

| Shortage of downstream diagnostic imaging capacity | -0.9% | Europe and many emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Test Price & Limited Reimbursement Pathways

Average list prices between USD 500 and USD 1,500 remain above the financial comfort zone for population screens, especially where per-capita health budgets lag OECD norms. Medicare covers only a narrow subset of genetic assays, so older adults—the cohort with highest cancer incidence—often pay out of pocket. GRAIL’s Galleri lists at USD 949, a figure payers still classify as premium relative to mammography or FIT tests. Emerging markets face steeper hurdles because public payers lack actuarial data to justify large-scale liquid biopsy funding. Private coverage is inconsistent, and value-based contracts tying payment to outcomes require long-range evidence many startups have yet to accumulate. Until unit costs approach USD 300, penetration outside high-income populations will stay restrained.

Persisting False-Positive / False-Negative Concerns & Need for Confirmatory Imaging

Even with <1% false-positive rates reported in pivotal trials, millions of annual screens could still generate tens of thousands of inconclusive results. Each positive triggers CT, PET-CT, or targeted MRI scans that strain already limited radiology capacity, notably in the United Kingdom where waiting lists top 1.5 million referrals.[3]National Health Service England, “Diagnostic Waiting Times and Activity Data,” nhs.uk False-negatives carry clinical risk that erodes physician confidence, especially if a delayed diagnosis leads to malpractice exposure. Algorithm calibration across ethnic and age cohorts remains a work in progress, so some providers defer adoption pending broader validation. Radiography workforce shortages in Europe exacerbate the bottleneck, elongating diagnostic pathways and dampening enthusiasm among hospital administrators who must manage patient flow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Multi Cancer Early Detection Market Segment Analysis

By Test Type:

Gene-Panel LDTs Retain Dominance as IVD Kits Gain MomentumGene-panel laboratory-developed tests commanded 94.21% of 2024 orders, reflecting the flexibility CLIA labs enjoy in iterating panels without a protracted FDA filing. LDT status allowed rapid incorporation of new methylation markers, keeping analytical sensitivity ahead of regulatory guidance curves. Yet the in-vitro diagnostic kit segment outpaces every other category with an 11.33% CAGR from 2025 to 2030. FDA breakthrough pathways and synchronized CMS review encourage manufacturers to pursue full-device clearances that unlock nationwide reimbursement codes. Exact Sciences’ Cancerguard program embodies this shift, investing in a 20,000-participant trial to support a pre-market approval dossier. LDT providers now weigh the cost of trial enrollment against the reimbursement upside of kit conversion.

The multi-cancer early detection market size for IVD kits could rise sharply once the first device wins national coverage determination. Hospital purchasing committees prefer FDA-cleared solutions because liability is lower and electronic ordering pathways are preconfigured. LDT stalwarts respond by enhancing clinical decision-support portals and offering bundled confirmatory testing to preserve share. Research-use-only panels remain a small but vital niche, supplying biomarker discovery projects that feed the next generation of commercial assays. “Other” formats such as microfluidic nanowell cartridges remain early stage but draw venture funding for potential in decentralized primary-care settings.

By Biomarker Class:

cfDNA Methylation Anchors Emerging Multi-Analyte PlatformsWith a 63.24% share in 2024, cfDNA methylation dominates biomarker selection because its epigenetic footprints are both cancer-specific and tissue-resolving. Machine-learning pipelines trained on millions of CpG islands produce probability maps that point radiologists toward likely tumor origin, streamlining work-ups. Multi-analyte panels that merge DNA, protein, and glycan signatures deliver the fastest 10.47% CAGR, riding evidence that complementary analytes lift early-stage sensitivity beyond 90%. GRAIL’s Galleri integrates methylation with proprietary classifier architecture to cover 50 cancers in one assay, setting the competitive bar for breadth. Somatic mutation panels persist in tumor types with hallmark driver genes, but their single-omic scope struggles against heterogeneity in cohort screening.

Fragmentomics and aneuploidy detection offer orthogonal signal sources by quantifying chromosomal break patterns and copy-number distortion. These features enrich models for cancers that shed scant DNA or lack distinctive methyl footprints. The challenge is computational: fusing sparse mutation counts, wide methylation matrices, and high-dynamic-range protein spectra in a clinically interpretable form. Vendors invest in scalable bioinformatics, often via cloud deployment, to manage terabytes of raw data per thousand patients. The payoff is a composite risk score that oncologists can act on with confidence.

By Technology Platform:

NGS Backbone Faces Accelerating AI-Centric DisruptionNext-generation sequencing underpins 37.41% of 2024 volume and remains the reference architecture for any assay needing broad genomic coverage. The multi-cancer early detection market size tied to NGS will keep growing as reagent prices fall and global install bases widen. Still, AI-enabled multi-omics platforms clock a 10.72% CAGR, reflecting investor appetite for software-weighted margins and differentiated intellectual property. Illumina-Tempus collaboration illustrates the convergence of silicon and wet lab, aiming to shorten sample-to-answer cycles and automate report generation. Digital PCR and BEAMing continue to serve ultra-low allele frequency applications, such as minimal residual disease, where read-depth beats breadth.

Mass-spectrometry protein assays re-emerge as cost-effective adjuncts that capture secreted tumor signals invisible to DNA screens. Hybrid workflows send a plasma aliquot for sequencing and another for proteomics, merging outputs in cloud engines that assign cancer likelihood scores. Vendors promote modularity—labs can add a proteomics module without overhauling existing NGS investment. Regulatory agencies are drafting guardrails that treat software classifiers as medical devices, so code versioning and real-world drift monitoring are becoming core competencies.

By End-User:

Specialty Clinics Erode Hospital PrimacyHospitals and academic medical centers still hold 47.63% of orders because they already coordinate oncology workflows and command the imaging infrastructure essential for follow-up. However, specialty diagnostic clinics post an 11.45% CAGR, benefiting from tightly focused protocols that cut turnaround time. These centers often staff genetic counselors on-site, reducing referral leakage and improving patient satisfaction scores. Independent reference laboratories capture volume from smaller practices via courier networks and electronic ordering portals, a model Quest Diagnostics scaled nationally. Corporate wellness and concierge providers represent a cash-pay frontier that absorbs test price premiums more readily than insurance-mediated channels.

The transition toward decentralized testing mirrors broader healthcare consumerization. Specialty centers market shorter wait times and integrated care paths, winning share among time-sensitive, tech-savvy patients. Hospitals respond by embedding pop-up liquid biopsy suites in outpatient wings and offering subscription-based screening memberships. As payer policies settle, end-user segmentation will likely stabilize around convenience, cost, and clinical depth trade-offs.

Geography Analysis

North America Multi Cancer Early Detection Market

North America controlled 32.31% of 2024 revenue, anchored by a mature regulatory ecosystem that granted multiple breakthrough device designations in one calendar year. CMS parallel review keeps reimbursement clocks synchronized, so innovators can price confidently at launch. Employer-sponsored demand boosts volume because self-insured corporations recoup avoided late-stage care costs directly. Canada trails the United States but benefits from provincial genomics initiatives that subsidize pilot programs. Mexico’s private hospital chains import U.S.-validated tests for high-income patients, while public-sector adoption waits on cost drops.

APAC Multi Cancer Early Detection Market

Asia-Pacific is the fastest-growing territory at 9.32% CAGR, propelled by China’s precision-medicine grants and Japan’s rapidly aging populace. Burning Rock Biotech and BGI Genomics conduct mega-scale verification cohorts that feed governmental cancer-control strategies. Australia funds national genomic screening pilots that include multi-cancer panels as part of its 10-year Cancer Plan. India’s private oncology networks buy sequencers outright, taking advantage of lower labor costs to competitively price tests for the burgeoning middle class. Regulatory diversity remains a hurdle, yet mutual-recognition compacts among ASEAN members could ease cross-border kit distribution.

Europe Multi Cancer Early Detection Market

Europe advances steadily but faces heterogeneous reimbursement structures. NHS England earmarked capital for Community Diagnostic Centres to absorb imaging demand generated by blood-based screens, yet radiographer shortages slow throughput. Germany and France move faster under sickness-fund models that reward early detection savings, whereas Southern European systems remain cautious on cost grounds. The EU In Vitro Diagnostic Regulation imposes uniform performance and vigilance standards, which may lengthen time-to-market but ultimately harmonize quality.

MEA and South America Multi Cancer Early Detection Market

Middle East and Africa plus South America presently contribute low single-digit shares. Gulf Cooperation Council states buy Western assays for premium expatriate clinics, creating beachheads for expansion. Brazil’s private insurers trial MCED coverage for high-risk members, but public adoption is years away due to budget constraints.

Competitive Landscape

Market concentration is moderate because clinical-evidence generation demands capital, favoring incumbents such as GRAIL, Guardant Health, and Exact Sciences. GRAIL’s June 2024 spin-off from Illumina preserved access to NovaSeq throughput while freeing commercial strategy from antitrust scrutiny. Guardant leverages oncology-practice detail via its LUNAR-2 colorectal assay to cross-sell Shield, demonstrating platform economics. Exact Sciences invests in Cancerguard trials that match its Cologuard storytelling with multi-cancer breadth, betting on brand trust.

AI-focused entrants like Singlera Genomics and Owkin pursue software-centric business models that promise faster gross-margin scaling. Partnerships define go-to-market playbooks: Quest Diagnostics connected its 2,000-site draw network to distribute Galleri nationwide, while Labcorp aligned with Ultima Genomics for cost-trimmed whole-genome sequencing. Regionally, Burning Rock Biotech dominates Chinese hospital channels and holds dual China-U.S. breakthroughs, illustrating cross-border regulatory savvy.

Supplier bargaining power is high for sequencing instruments but falling as new entrants like Element Biosciences and Ultima expand choice. Buyer power rises with employer coalitions negotiating enterprise pricing. Threat of substitution is low; imaging cannot non-invasively deliver pan-cancer coverage. Overall rivalry intensifies around data ownership: the largest clinical-genomic repositories will likely dictate algorithm performance, creating a feedback loop that entrenches scale leaders.

Multi Cancer Early Detection Industry Leaders

Exact Sciences Corporation

F. Hoffmann-La Roche AG

Freenome Holdings, Inc.

Illumina, Inc.

Guardant Health, Inc.

- *Disclaimer: Major Players sorted in no particular order

Multi Cancer Early Detection Market Companies Covered in this Report

- AnPac Bio-Medical Science Co.

- BGI Genomics Co., Ltd.

- Burning Rock Biotech Ltd.

- Elypta AB

- Exact Sciences

- Roche

- Freenome Holdings, Inc.

- GRAIL, LLC

- Guardant Health, Inc.

- Helio Health, Inc.

- Illumina

- Lucence Diagnostics Pte Ltd

- Natera, Inc.

- Nucleix Ltd.

- QIAGEN

- Singlera Genomics, Inc.

- Thermo Fisher Scientific

Recent Industry Developments in Multi Cancer Early Detection Market

- May 2025: Illumina expanded Medicare reimbursement access for its comprehensive cancer testing portfolio and rolled out companion-diagnostic functionalities across U.S. oncology networks

- April 2025: Illumina and Tempus AI partnered to integrate multimodal AI pipelines with NovaSeq workflows, aiming to enhance early detection accuracy and therapy matching.

Global Multi Cancer Early Detection Market Report Scope

Segmentation Overview

| Gene-panel LDTs |

| IVD Kits (regulated) |

| Research-use-only Panels |

| Others |

| cfDNA Methylation |

| Somatic Mutation Panels |

| Fragmentomics / Aneuploidy |

| Multi-analyte (DNA + Protein + Glycan) |

| Next-Generation Sequencing |

| Digital PCR / BEAMing |

| Mass-Spectrometry-Based Protein Assays |

| AI-enabled Multi-omics Analytics |

| Hospitals & Academic Medical Centers |

| Independent / Reference Laboratories |

| Specialty Oncology & Diagnostic Clinics |

| Corporate Wellness / Concierge Health Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Gene-panel LDTs | |

| IVD Kits (regulated) | ||

| Research-use-only Panels | ||

| Others | ||

| By Biomarker Class | cfDNA Methylation | |

| Somatic Mutation Panels | ||

| Fragmentomics / Aneuploidy | ||

| Multi-analyte (DNA + Protein + Glycan) | ||

| By Technology Platform | Next-Generation Sequencing | |

| Digital PCR / BEAMing | ||

| Mass-Spectrometry-Based Protein Assays | ||

| AI-enabled Multi-omics Analytics | ||

| By End-User | Hospitals & Academic Medical Centers | |

| Independent / Reference Laboratories | ||

| Specialty Oncology & Diagnostic Clinics | ||

| Corporate Wellness / Concierge Health Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the multi-cancer early detection market in 2025?

It is valued at USD 1.34 billion and is projected to grow to USD 1.91 billion by 2030.

What CAGR is projected for multi-cancer early detection between 2025 and 2030?

The market is forecast to advance at a 7.34% CAGR during the period.

Which test type currently dominates orders?

Gene-panel laboratory-developed tests account for 94.21% of 2024 volume.

Which region is expanding fastest?

Asia-Pacific shows the highest growth, registering a 9.32% CAGR through 2030.

Why are employers adding multi-cancer blood tests to benefits?

Self-insured firms expect savings because stage I treatment costs USD 100,000 less than stage IV, improving financial risk profiles.

What technology trend is reshaping early detection accuracy?

AI-powered multi-omics fusion boosts early-stage sensitivity above 95% by combining genomic, epigenomic, and proteomic data.

Page last updated on: