Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

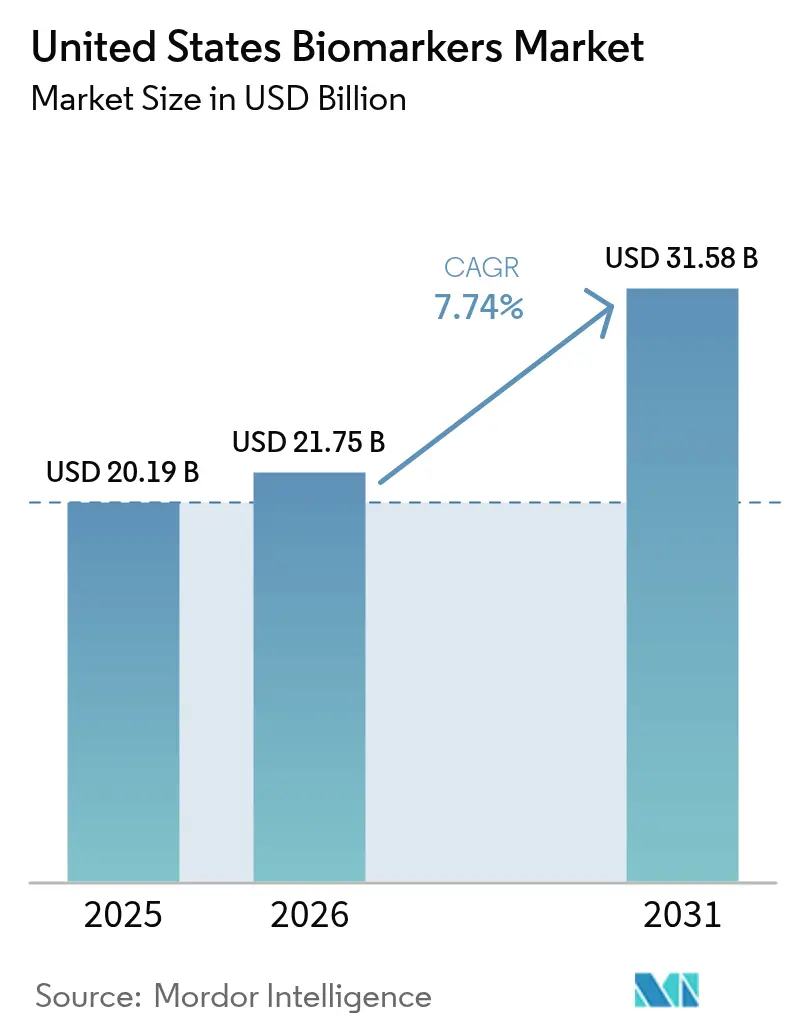

| Base Year Market Size (2025) | USD 20.19 Billion |

| Market Size (2026) | USD 21.75 Billion |

| Market Size (2031) | USD 31.58 Billion |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Biomarkers Market Analysis by Mordor Intelligence

The United States biomarkers market size is expected to grow from USD 20.19 billion in 2025 to USD 21.75 billion in 2026 and is forecast to reach USD 31.58 billion by 2031 at 7.74% CAGR over 2026-2031. Growth is reinforced by falling next-generation sequencing costs that expand test menus and accelerate validation timelines across clinical and research settings. Uptake is also supported by the continued integration of companion diagnostics in FDA drug labels, which tightens linkage between targeted therapies and test-enabled eligibility decisions. Coverage pilots by the Centers for Medicare & Medicaid Services for blood-based neurodegeneration biomarkers are opening earlier detection pathways and creating reimbursement precedents that broaden clinical use. Broader interoperability initiatives, including TEFCA and USCDI+, are improving data liquidity for real-world evidence and post-market assessment, which strengthens clinical utility claims and supports scale in the United States biomarkers market.

Key Report Takeaways

- By product, Consumables led with 51.78% revenue share in 2025, while Services & Software is forecast to expand at a 10.05% CAGR to 2031.

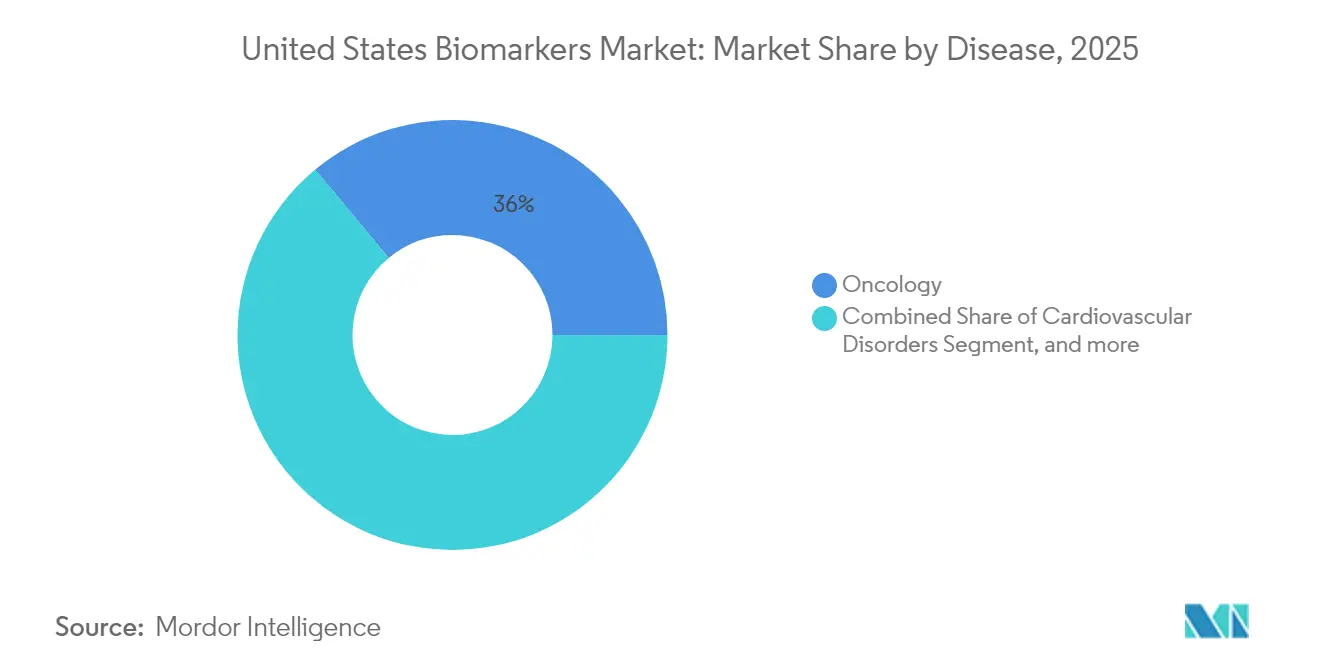

- By disease, Oncology held 36.02% of the United States biomarkers market share in 2025, while Neurological Disorders is projected to record a 8.86% CAGR to 2031.

- By type, Safety Biomarkers accounted for 41.23% share in 2025, and Efficacy Biomarkers are expected to grow at a 10.28% CAGR through 2031.

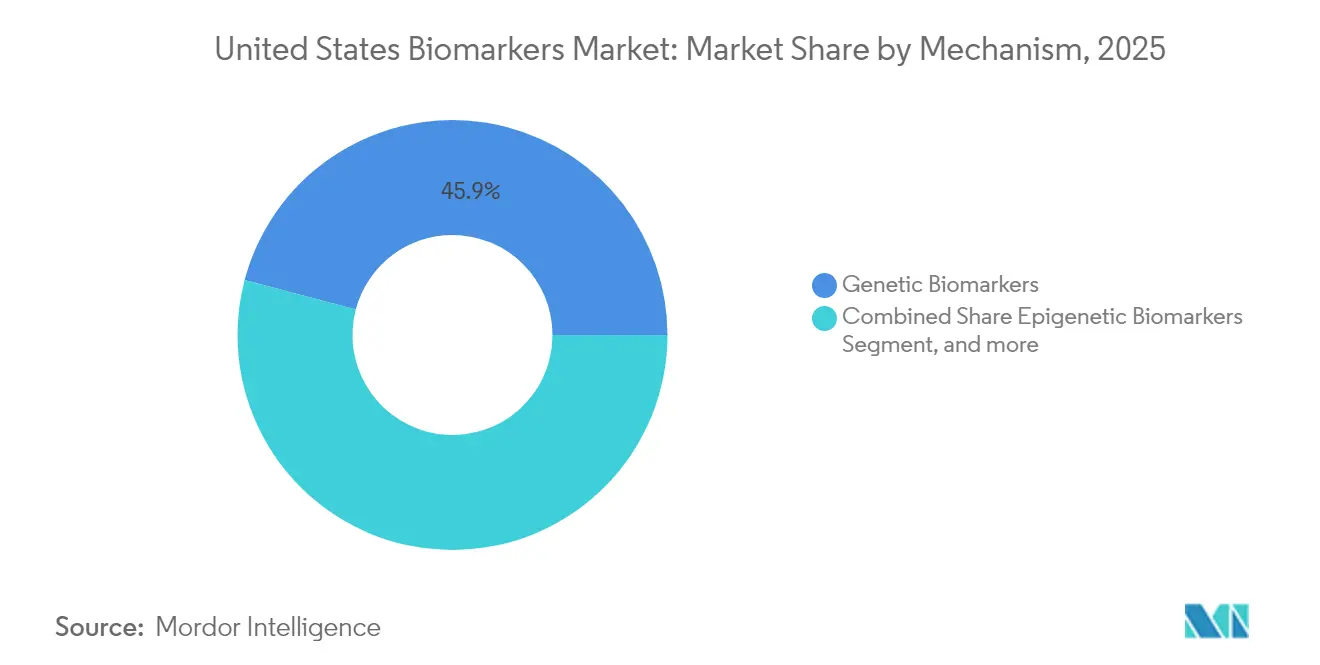

- By mechanism, Genetic Biomarkers held 45.89% share in 2025, while Epigenetic Biomarkers are set to expand at an 10.86% CAGR through 2031.

- By application, Drug Discovery & Development captured 30.89% of 2025 revenue, while Personalized Medicine is forecast to grow at a 11.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Biomarkers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising oncology burden and chronic disease prevalence in the U.S. | 1.2% | National, with higher concentration in aging Northeast and Midwest populations | Long term (≥ 4 years) |

| Broader adoption of biomarker-based clinical diagnostics & screening across U.S. health systems | 1.5% | National, early adoption in academic medical centers and integrated delivery networks | Medium term (2-4 years) |

| Acceleration of companion diagnostics embedded in drug labels and clinical trials | 1.3% | National, with concentration in oncology centers of excellence | Medium term (2-4 years) |

| Falling NGS/multi-omics costs enabling broader discovery and clinical validation | 1.4% | National, with spillover to community hospitals as reference-lab partnerships expand | Short term (≤ 2 years) |

| CMS coverage pilots for blood-based neurodegenerative biomarkers catalyzing earlier detection | 1.1% | National, initial impact in Medicare Advantage markets | Short term (≤ 2 years) |

| Data liquidity via TEFCA/USCDI+ enabling RWE pipelines for validation and label expansion | 0.9% | National, accelerated in states with mature health information exchanges | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Oncology Burden and Chronic Disease Prevalence in the U.S.

Cancer incidence projections indicate that the United States will see around 2 million new diagnoses annually through 2030, with lung and colorectal cancers representing large case volumes that benefit from biomarker-guided therapy selection[1]National Cancer Institute, “Cancer Statistics,” National Institutes of Health, cancer.gov. Chronic cardiovascular and metabolic conditions affect a large adult population, which sustains demand for cardiac and metabolic biomarkers embedded in treatment protocols across health systems. An aging demographic profile, with adults aged 65 and older expected to represent a rising share of the U.S. population by 2030, is increasing co-morbidities and encouraging multi-disease panels that streamline workflows for faster treatment initiation. Molecular profiling identifies actionable mutations in a significant share of advanced-stage cancers, which enables enrollment in precision trials and access to targeted therapies that outperform empirical regimens in specific settings. Regulatory programs such as the FDA’s tumor-agnostic biomarker policies and laboratory quality rules under CLIA continue to standardize assay performance, which supports payer confidence in the United States biomarkers market.

CMS Coverage Pilots for Blood-Based Neurodegenerative Biomarkers Catalyzing Earlier Detection

CMS draft coverage determinations in 2024 for plasma assays that measure phosphorylated tau and amyloid-beta ratios recognized their role in ruling out Alzheimer pathology in patients with mild cognitive impairment. Coverage with evidence development models require prospective registries to gather outcomes, which link reimbursement to real-world performance and clinical benefit. Clinicians are layering blood tests into diagnostic workflows, which shortens time to diagnosis and supports care planning earlier in the disease course[2]Alzheimer’s Association, “Clinical Trials and Studies,” Alzheimer’s Association, alz.org. Private insurers are observing Medicare pilots and adapting policies that use biomarker documentation as a predicate for specialty referrals in older adults. Diagnostic companies are scaling immunoassay and mass spectrometry platforms for high-volume processing as coverage expands beyond specialty centers. CLIA and local or national coverage determinations continue to anchor quality and access parameters for decentralized testing sites in the United States biomarkers market.

Data Liquidity via TEFCA/USCDI+ Enabling RWE Pipelines for Validation and Label Expansion

TEFCA is creating a framework for nationwide interoperability that allows biomarker and clinical outcomes data to move across health information exchanges for care and research use. USCDI+ is promoting standardized representation of laboratory results using LOINC and SNOMED, which improves analytics and reduces mapping friction across systems[3]SNOMED International, “SNOMED CT Overview,” SNOMED International, snomed.org. Providers and sponsors are running pragmatic trials that embed eligibility logic into EHRs to compress enrollment timelines and lower per-patient costs. Payers are leveraging interoperable registries to monitor test utilization patterns and align reimbursement with evidence-based ordering. Academic consortia use de-identified multi-institutional datasets to discover associations between molecular signatures and outcomes that inform guideline updates and FDA biomarker qualification submissions. The 21st Century Cures Act and HIPAA provisions balance data sharing with privacy safeguards, which ensures appropriate consent and de-identification for research.

Falling NGS/Multi-Omics Costs Enabling Broader Discovery and Clinical Validation

Sequencing costs have declined in recent years due to chemistry and throughput advances, which supports broader clinical and discovery use cases. Population genomics programs run by academic centers and national initiatives are generating variant insights that feed back into decision-support tools used at the point of care. Biopharma is deploying multi-omics approaches in early development to identify response-enriched cohorts and reduce the size and duration of pivotal trials. Clinical labs continue moving from single-gene tests to comprehensive tumor panels while preserving turnaround times consistent with urgent treatment planning, guided by published FDA validation expectations for NGS-based oncology assays. Reference labs are automating library preparation and bioinformatics pipelines to handle variable testing demand, aided by platform advances from major instrument suppliers. Clearer regulatory guidance for NGS validation around limit-of-detection and accuracy has supported adoption without compromising analytical performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex reimbursement and evolving FDA IVD/LDT regulation increases time-to-market | -0.8% | National, with acute impact on laboratory-developed tests in hospital and academic settings | Medium term (2-4 years) |

| High assay development and multi-site clinical validation costs | -0.6% | National, disproportionate burden on emerging diagnostics companies | Short term (≤ 2 years) |

| Limited assay standardization/interoperability across platforms hampers payer acceptance | -0.5% | National, most pronounced in decentralized laboratory networks | Long term (≥ 4 years) |

| Algorithmic transparency and change-control expectations for AI biomarkers slow adoption | -0.4% | National, concentrated in AI-enabled imaging and liquid biopsy interpretation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Reimbursement and Evolving FDA IVD/LDT Regulation Increases Time-to-Market

The FDA’s proposed framework to regulate laboratory-developed tests expands premarket review expectations for in-house assays, which lengthens development cycles and increases submission costs for hospital and academic laboratories. Many institutions are reassessing innovation pipelines or seeking commercial partners that can shoulder regulatory and quality requirements under the United States biomarkers market. Fragmented coverage policies across Medicare Administrative Contractors create region-by-region variability in approvals that constrains predictable reimbursement. Prior authorization and medical necessity checks add administrative steps that lower ordering rates even for tests with strong clinical evidence. The absence of specific CPT codes for newer biomarker categories often forces use of miscellaneous codes that pay at lower rates or face denials, which delays adoption. These barriers collectively slow market entry and scale for novel assays that would otherwise meet clinical needs.

High Assay Development and Multi-Site Clinical Validation Costs

End-to-end development for a clinically validated biomarker, from discovery to regulatory submission, requires multi-year investment and large prospective studies that stretch early-stage budgets in the United States biomarkers market. Smaller diagnostics firms struggle to fund multi-center trials for rare-disease populations where recruitment is slow and sites are widely distributed. Contract research activities, biospecimen logistics, and compliant site monitoring add cost layers that heighten the capital burden for new assay categories. Regulatory submissions demand comprehensive analytical validation, including limit-of-detection, precision, accuracy, and interference studies, which require extensive reference materials and months of lab work. Payers increasingly request credible health-economic models before issuing policies, which adds study complexity and time before covered clinical use. These cost factors shape the pace and sequencing of pipeline decisions for emerging test developers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease: Oncology Dominance Persists While Neurological Disorders Accelerate on Blood-Based Alzheimer Breakthroughs

Oncology accounted for 36.02% of disease-specific revenue in 2025 supported by widespread adoption of comprehensive genomic profiling for tumor characterization and therapy selection. The United States biomarkers market has embedded testing for targets that guide treatment in non-small cell lung cancer, colorectal cancer, breast cancer, and melanoma, and this underpins clinical trial enrollment and access to targeted agents. Neurological Disorders are expected to grow at a 8.86% CAGR through 2031 as plasma phospho-tau and amyloid assays move into routine use in primary care to triage suspected Alzheimer cases after recent coverage pilots. Cardiovascular biomarkers such as high-sensitivity troponin and natriuretic peptides support guideline-driven care that uses serial measurements to titrate therapy and assess residual risk in outpatient management. Immunology programs rely on biomarkers such as C-reactive protein and anti-CCP antibodies, though expansion is tempered by market maturity and fewer novel markers with superior performance.

Renal and urologic testing for chronic kidney disease staging remains essential, although pricing pressure challenges revenue growth as payers apply value-based models. Infectious disease and sepsis biomarkers continue to support stewardship protocols that target early intervention and better antibiotic use in hospital settings. Metabolic and endocrine biomarkers like hemoglobin A1c and TSH sustain volume through population health initiatives that identify and monitor at-risk individuals. Emerging areas in respiratory and gastrointestinal disorders include noninvasive fibrosis staging and phenotype-based asthma assessment, which may reduce reliance on invasive procedures once validation completes. The United States biomarkers market continues to see oncology as the anchor for precision diagnostics while neurology is the fastest-moving disease area based on recent coverage trends and new blood-based modalities.

By Product: Services & Software Surge as Cloud Analytics and AI Interpretation Reshape Workflow Integration

Consumables held 51.78% of revenue in 2025 as labs across hospitals, reference centers, and pharma research maintained high-volume ordering for reagents and kits across immunoassays, PCR, and sequencing workflows. The United States biomarkers market continues to depend on stable supply chains for these core inputs, which underpins routine testing across oncology, cardiology, and infectious disease programs. Services & Software is the fastest-growing category at a 10.05% CAGR through 2031, driven by cloud bioinformatics that automates variant calling, annotation, and report generation aligned to clinical standards for structured results. Health systems are embedding AI-enabled interpretation modules within EHRs to route clinically actionable findings into care pathways that improve ordering consistency and turnaround times. Vendors are differentiating with pharmacogenomic decision support and longitudinal tracking of circulating tumor DNA changes, which help clinicians adapt therapy sequences. The United States biomarkers industry is also seeing bundled offerings that combine wet-lab processing with expert review, which simplifies staffing needs for community providers.

Instrument demand remains mixed as cost containment pressures influence capital budgets, yet upgrades to higher-throughput sequencers and automation platforms continue where scale brings operating margin benefits. Reference labs are outsourcing specialist interpretation to centralized teams that run molecular tumor boards and hereditary risk consultations, which can improve clarity and reduce variability in recommendations. Software components that output patient-specific results fall within CLIA oversight, which requires validation that automation yields concordant results compared to expert review. The United States biomarkers market benefits from investments in template-based reporting and standardized codes that reduce manual mapping across LOINC and SNOMED terminologies. These product-layer dynamics reinforce a shift toward recurring revenue streams from analytics and services that complement consumable volumes.

By Mechanism: Epigenetic Biomarkers Surge on Methylation-Based Liquid Biopsy Momentum in Colorectal and Breast Residual Disease

Genetic Biomarkers accounted for 45.89% of mechanism-based revenue in 2025 anchored by NGS panels that interrogate key oncogenic drivers across solid tumors. These test menus support selection for targeted therapies or trial enrollment across tumor-agnostic or tumor-specific indications as supported by FDA-recognized genomic biomarkers. Epigenetic Biomarkers are forecast to grow at an 10.86% CAGR through 2031, powered by methylation-based liquid biopsy approaches that detect minimal residual disease after surgery or adjuvant therapy in colorectal and breast cohorts. The United States biomarkers industry is seeing strong development activity around methylation signatures for early detection and surveillance, including multi-cancer early detection platforms advancing clinical validation.

Proteomic biomarkers measured via mass spectrometry and multiplex immunoassays are gaining traction in immunology and neurology for longitudinal monitoring, but reimbursement remains a hurdle until clinical utility is established. Metabolomic approaches are used in targeted programs such as newborn screening and precision nutrition pilots, while broader adoption awaits simpler workflows and widely available reference materials. Lipidomic profiling for cardiovascular and neurodegenerative risk is under investigation, with translation dependent on proof of incremental predictive value beyond standard panels. Imaging biomarkers derived from PET, MRI, and CT contribute to pharmacodynamic assessment and response measurement in oncology trials, with quantitative imaging standards supported by professional collaborations. The United States biomarkers market continues to shift toward multi-modal signatures that integrate genomic, epigenomic, and imaging features for more reliable disease management.

By Application: Personalized Medicine Leads Growth as Pharmacogenomic Panels Reduce Adverse Events and Optimize Dosing in Cardiovascular and Psychiatric Care

Drug Discovery & Development captured 30.89% of application revenue in 2025 through biomarker-guided target validation and patient stratification that compresses trial sizes and timelines. Companion diagnostic co-development remains central to therapeutic submissions and post-approval commitments for label claims in the United States biomarkers market. Personalized Medicine is the fastest-growing application at a 11.65% CAGR through 2031, driven by preemptive pharmacogenomics for medications such as clopidogrel, warfarin, statins, and SSRIs that reduces adverse events and improves dose selection. Clinical Diagnostics remains a high-volume area across oncology, infectious diseases, cardiology, and neurology, guided by preventive and specialty guidelines.

Disease Risk Assessment using polygenic risk scores is emerging in wellness and employer settings, with clinical integration paced by evidence of actionability and payer coverage decisions. Prognosis and monitoring applications such as serial ctDNA testing are expanding, which supports response-adapted oncology regimens and creates recurring testing demand. The United States biomarkers market favors applications that couple clinical impact with clear reimbursement logic, which includes dose optimization and de-escalation strategies that lower downstream costs. As more real-world evidence accumulates, payers are likely to refine policies that align payment with outcomes and guideline adherence. This feedback loop between clinical utility evidence and coverage is shaping the slope of adoption across use cases.

By Type: Efficacy Biomarkers Outpace Safety Markers as Payers Demand Real-World Evidence Linking Response to Outcomes

Safety Biomarkers represented 41.23% of type-based revenue in 2025, reflecting the importance of toxicity monitoring during early-phase trials as sponsors identify maximum tolerated dosing. Payers and clinicians continue to rely on safety markers in clinical practice to manage therapy risks under intensive monitoring protocols. Efficacy Biomarkers are set to grow at a 10.28% CAGR through 2031 because coverage policies increasingly require objective evidence of treatment response to authorize continuation of high-cost therapies in the United States biomarkers market. Prognostic biomarkers help stratify patients by baseline risk, which informs when to escalate or de-escalate regimens, such as adjuvant therapy decisions in oncology. Predictive biomarkers identify patients likely to benefit from specific therapies, as seen with PD-L1 testing and tumor mutational burden assessment that supports immunotherapy selection in defined settings.

Pharmacodynamic markers that confirm on-pathway drug activity are crucial in early-phase development and can reduce costly late-stage attrition by validating mechanism of action. Surrogate endpoints such as minimal residual disease in hematologic cancers are being used in accelerated pathways, which can advance regulatory decisions pending confirmatory trials. Validation biomarkers that ensure sample integrity and assay consistency remain essential for credible interpretation of safety and efficacy markers. The United States biomarkers market size for Efficacy Biomarkers is expected to expand steadily alongside payer requirements that tie reimbursement to measurable clinical change.

Competitive Landscape

The United States biomarkers market features established diagnostics leaders alongside venture-backed innovators that focus on liquid biopsy, AI-enabled interpretation, and high-throughput workflows. Incumbents are broadening menus through acquisitions and partnerships that add neurodegeneration, oncology, and immunology assays, while they strengthen service layers that integrate directly with EHRs. Specialist firms are scaling multi-year contracts with integrated delivery networks and self-insured employers to reduce time-to-diagnosis and downstream costs, which intensifies competition in oncology surveillance and early detection. Payers are experimenting with outcomes-based contracts where test reimbursement is linked to adherence with guidelines and documented clinical benefit.

Strategic moves in 2024 highlight the pace of innovation and commercialization. Guardant Health announced FDA approval for a blood-based comprehensive genomic profiling assay for advanced solid tumors, which provides an alternative when tissue is limited or inaccessible. Exact Sciences signed a multi-year agreement with an integrated delivery network to deploy a multi-cancer early detection test in average-risk individuals, signaling diversification beyond colorectal screening. Thermo Fisher strengthened neurodegeneration assay capabilities through acquisition, which aligns with favorable coverage momentum for Alzheimer blood tests. Abbott received FDA clearance for a high-sensitivity troponin test optimized for point-of-care use, which supports emergency medicine protocols.

Platform and partnership activity continues to shape competitive positions. Illumina launched a next-generation sequencing platform that improves throughput and reduces per-sample costs for population genomics and hereditary cancer workloads. Foundation Medicine expanded its companion diagnostic co-development with a pharmaceutical partner focused on rare fusions, which reflects tighter coordination between drug and diagnostic commercialization. Natera completed enrollment for a pivotal trial of ctDNA monitoring in stage II colorectal cancer, with results expected to influence clinical guidelines and coverage decisions in 2025. Tempus announced an HIE integration to enable retrospective analyses of biomarker testing and outcomes, which supports label expansion and post-market surveillance. These moves indicate that services, analytics, and evidence-generation capabilities will be as important as wet-lab performance in defining leadership.

United States Biomarkers Industry Leaders

Abbott Laboratories Inc.

Thermo Fisher Scientific

F. Hoffmann-La Roche Ltd

Danaher Corporation

QIAGEN N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Exact Sciences Corporation entered a multi-year contract with a large integrated delivery network to provide multi-cancer early detection testing for average-risk individuals aged 50 and older, representing a strategic shift from colorectal cancer screening into broader oncology interception and positioning the company to capture incremental revenue as payer coverage policies evolve.

- August 2024: GRAIL, LLC published results from a 140,000-participant prospective study demonstrating that its methylation-based multi-cancer screening test detected 50 cancer types with high specificity, generating clinical utility evidence expected to inform CMS coverage deliberations and potentially expand the addressable market to tens of millions of Medicare beneficiaries.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States cancer biomarkers market as all FDA-approved and CLIA-validated molecular, protein, and imaging markers that are used in vivo or ex vivo to screen, diagnose, stage, monitor, or guide therapy for malignant tumors across hospital, reference-lab, and point-of-care settings. Value estimates capture gross test revenue plus companion-diagnostic kit sales that accrue inside U.S. borders during the calendar year.

Scope Exclusions: research-use-only reagent kits, purely prognostic investigational markers, and biomarkers targeting non-oncology indications are outside this assessment.

Segmentation Overview

- By Disease

- Oncology

- Cardiovascular Disorders

- Neurological Disorders

- Immunological & Inflammatory Disorders

- Renal & Urologic Disorders

- Infectious Diseases & Sepsis

- Metabolic & Endocrine Disorders

- Respiratory Disorders

- Gastrointestinal & Hepatic Disorders

- By Type

- Efficacy Biomarkers

- Prognostic Biomarkers

- Predictive Biomarkers

- Pharmacodynamic Biomarkers

- Surrogate Endpoint Markers

- Safety Biomarkers

- Validation Biomarkers

- Efficacy Biomarkers

- By Mechanism

- Genetic (Genomic) Biomarkers

- Epigenetic Biomarkers

- Proteomic Biomarkers

- Metabolomic Biomarkers

- Lipidomic Biomarkers

- Imaging Biomarkers

- By Application

- Clinical Diagnostics

- Drug Discovery & Development

- Personalized Medicine

- Disease Risk Assessment

- Prognosis & Monitoring

- By Product

- Consumables

- Instruments

- Services & Software

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed oncologists, molecular-pathology lab directors, diagnostics distributors, and reimbursement specialists across the Northeast, Midwest, Sun Belt, and Pacific regions. Dialogues tested penetration-rate assumptions, pricing shifts after Medicare LCD changes, and likely adoption curves for liquid-biopsy panels, thereby bridging data gaps left by desk work.

Desk Research

We began with authoritative public datasets such as the American Cancer Society incidence projections, NCI-SEER prevalence files, FDA Biomarker Qualification submissions, CMS reimbursement fee schedules, and USPTO oncology patent grants. Trade and professional bodies, such as the College of American Pathologists, Association for Molecular Pathology, and AdvaMed, offered procedure volumes and regulatory updates, while peer-reviewed journals provided sensitivity-specificity benchmarks that helped gauge test replacement cycles. Paid collections that Mordor analysts reference selectively include D&B Hoovers for supplier revenue splits and Dow Jones Factiva for deal flow. These sources shaped foundational assumptions; many additional references were consulted for corroboration and are not exhaustively listed here.

Market-Sizing & Forecasting

A top-down cancer-incidence and testing-penetration build was created. New and existing patient pools were multiplied by test frequency and weighted average reimbursement; results were stress-tested through selective bottom-up roll-ups of leading assay manufacturers' U.S. oncology revenue. Key variables like incidence growth, guideline-driven companion-diagnostic uptake, average selling price movements, lab-developed-test share, and multi-omic panel mix feed a multivariate-regression forecast that spans 2025 to 2030. Where bottom-up checks diverged, gaps were proportionally redistributed to high-uncertainty segments before final sign-off.

Data Validation & Update Cycle

Outputs run through variance checks against historical spend, private-payer claims data, and import statistics. Senior analysts review anomalies, after which a peer reviewer signs off. The model refreshes each year, with interim revisions triggered by material FDA approvals or reimbursement shifts, ensuring clients always receive the latest view.

Why Mordor's United States Cancer Biomarkers Baseline Commands Confidence

Published estimates often differ because providers adopt dissimilar disease scopes, include varying research-service revenues, and refresh at different times.

Key gap drivers in our comparison are inclusion of non-cancer biomarkers, reliance on North America to U.S. prorations, limited primary validation, or the use of single-source manufacturer disclosures that miss hospital-developed assays. By anchoring to incidence, reimbursement, and verified laboratory volumes, Mordor delivers a balanced baseline that boards can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.62 Bn (2025) | Mordor Intelligence | - |

| USD 20.50 Bn (2024) | Regional Consultancy A | Includes non-oncology biomarkers and bundled research services; relies on regional allocations with scant primary checks |

| USD 9.20 Bn (2023) | Global Consultancy B | Uses earlier base year and counts only FDA-cleared kits, ignoring hospital LDT volumes and ASP erosion |

In sum, while other publishers present wider or narrower figures, Mordor's disciplined scope selection, variable transparency, and yearly validation furnish decision-makers with a dependable, reproducible starting point for strategic planning.

Key Questions Answered in the Report

What is the current size and growth outlook of the United States biomarkers market?

The market reached USD 21.75 billion in 2026 and is projected to reach USD 31.58 billion by 2031 at a 7.74% CAGR.

Which disease area leads demand within the United States biomarkers market?

Oncology led with 36.02% of revenue in 2025, driven by comprehensive genomic profiling for therapy selection and clinical trial enrollment.

Which application is growing the fastest in the United States biomarkers market?

Personalized Medicine is the fastest-growing application at a 11.65% CAGR through 2031, supported by preemptive pharmacogenomic testing in cardiovascular and psychiatric care.

What product category is expanding the quickest in the United States biomarkers market?

Services & Software is expanding at a 10.05% CAGR through 2031 as cloud analytics and AI-enabled interpretation integrate with EHR workflows.

Which mechanism type shows the highest growth in the United States biomarkers market?

Epigenetic Biomarkers are forecast to grow at an 10.86% CAGR through 2031, led by methylation-based liquid biopsy for minimal residual disease detection.

Which U.S. region will grow fastest for biomarkers over the forecast period?

The Southeast is projected to grow at an 7.96% CAGR to 2031, while the West is expected at 7.78%, supported by payer innovation and expanding precision medicine programs.

Page last updated on: