Australia Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

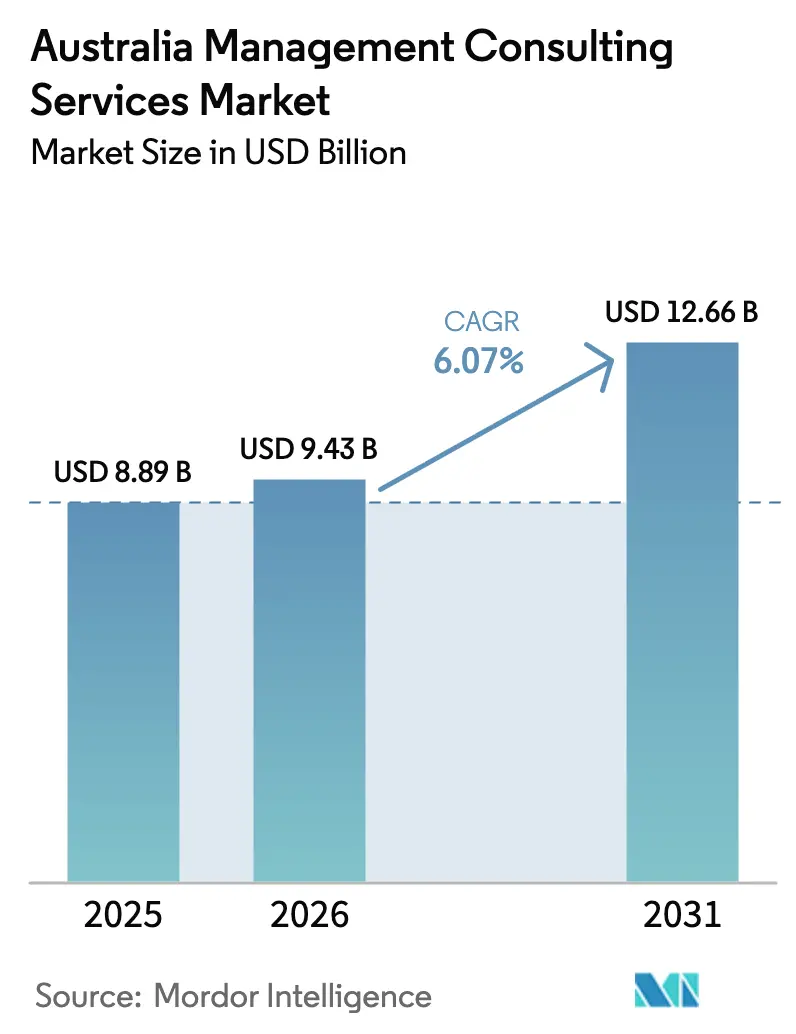

| Base Year Market Size (2025) | USD 8.89 Billion |

| Market Size (2026) | USD 9.43 Billion |

| Market Size (2031) | USD 12.66 Billion |

| Growth Rate (2026 - 2031) | 6.07% CAGR |

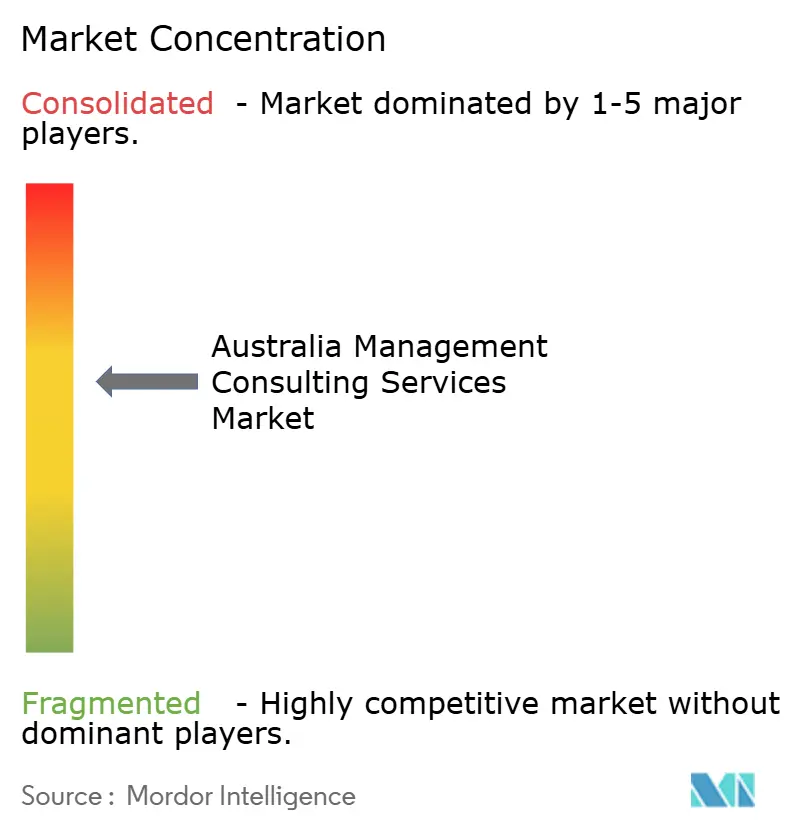

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Management Consulting Services Market Analysis by Mordor Intelligence

The Australia Management Consulting Services Market size was valued at USD 8.89 billion in 2025 and estimated to grow from USD 9.43 billion in 2026 to reach USD 12.66 billion by 2031, at a CAGR of 6.07% during the forecast period (2026-2031). Growing digital-transformation mandates, mandatory sustainability reporting and a pivot to hybrid delivery models underpin this expansion. Large enterprises continue to anchor demand, although procurement reforms now channel more projects to SMEs. Technology consulting is gaining momentum as artificial-intelligence use cases multiply across finance, mining and healthcare. Meanwhile, public-sector spending is rebalancing in favour of mid-tier providers as Canberra diversifies beyond the Big Four. Escalating wage pressures and skills shortages temper growth yet also open advisory opportunities around workforce redesign and automation.

Key Report Takeaways

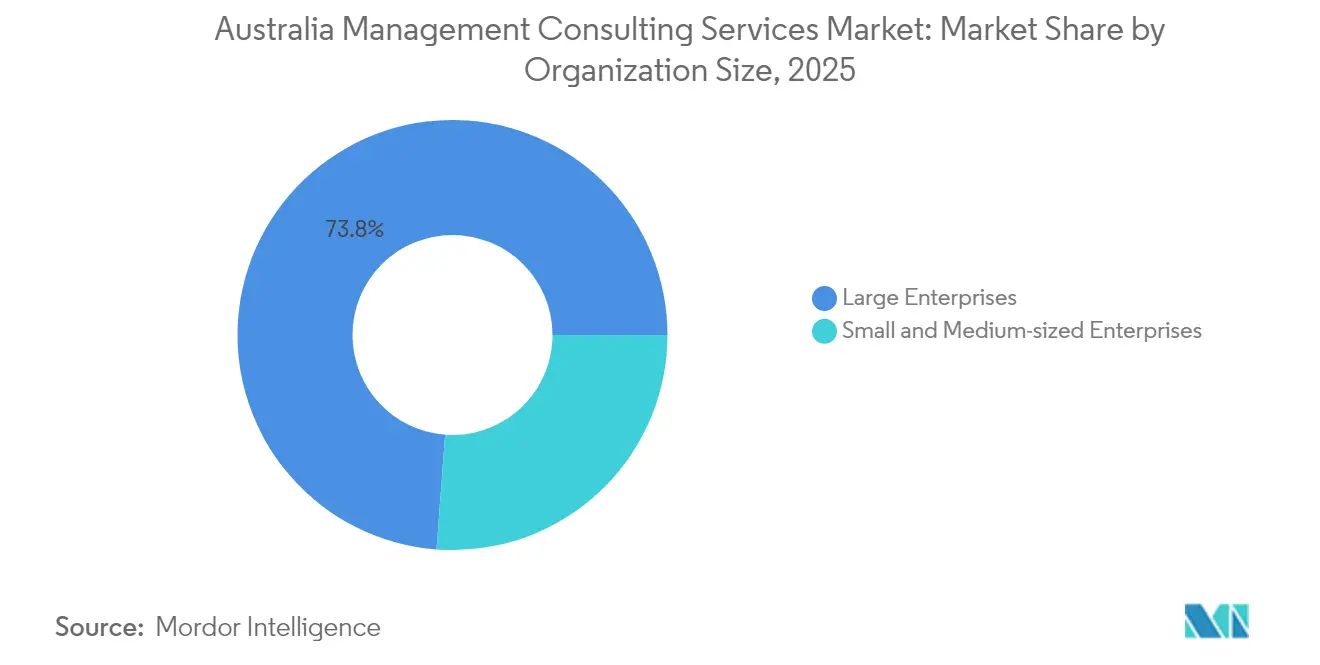

- By organization size, large enterprises held 73.82% of the Australia management consulting services market share in 2025; SMEs are poised to grow at a 9.62% CAGR through 2031.

- By service type, digital transformation consulting segment occupied the largest market share of 19.94% in 2025, and digital transformation consulting is expected to witness the highest 8.02% CAGR through 2031.

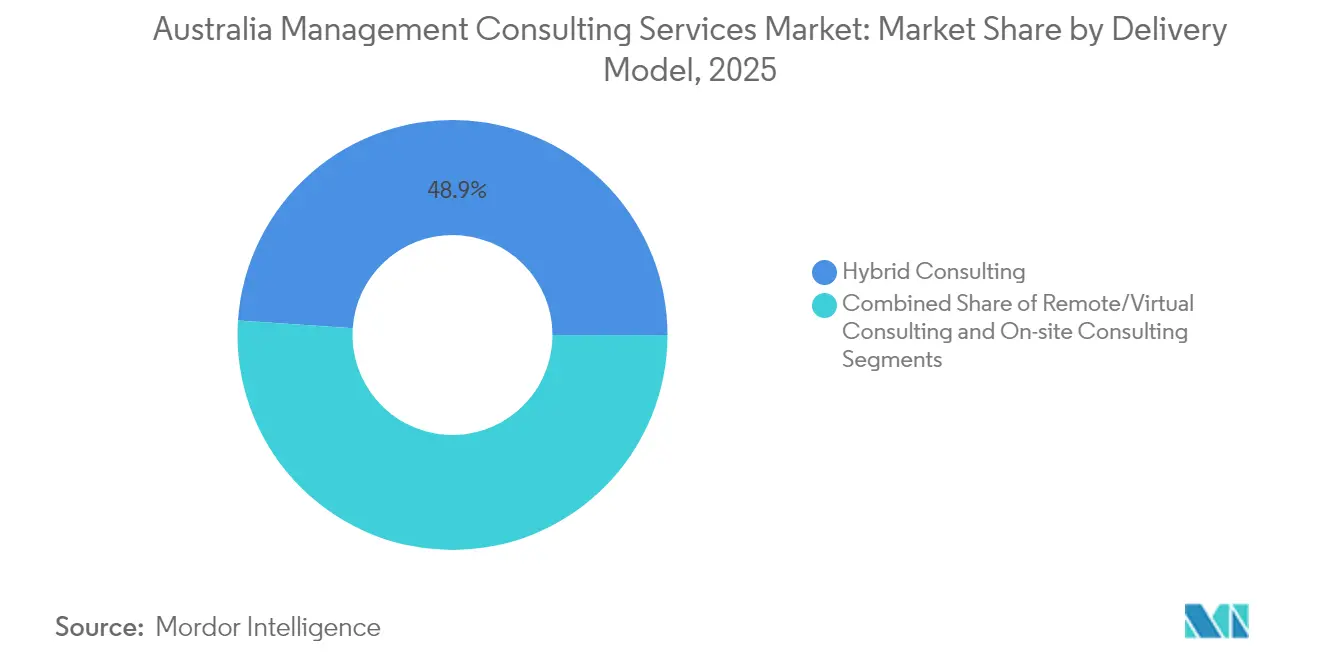

- By delivery model, the hybrid consulting segment occupied the largest market share of 48.92% in 2025, and remote / virtual consulting is expected to witness the highest CAGR of 8.35% CAGR through 2031.

- By end-user industry, the government and public sector segment occupied the largest market share of 18.24% in 2025, and energy and utilities are expected to witness the highest CAGR of 9.1% over the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated digital-transformation mandates | +1.8% | Global | Medium term (2-4 years) |

| Rising demand for cost optimisation | +1.2% | Global | Short term (≤ 2 years) |

| Rapid adoption of hybrid/remote work models | +0.9% | Global | Short term (≤ 2 years) |

| Public-sector shift away from Big Four | +0.7% | National (Canberra focus) | Medium term (2-4 years) |

| ESG and net-zero compliance needs | +1.1% | Global | Long term (≥ 4 years) |

| Generative-AI strategy and implementation | +1.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Digital-Transformation Mandates

Australian corporates are modernising legacy systems to unlock automation, cloud scalability and data analytics capabilities. Commonwealth Bank has pursued more than 50 generative-AI pilots, signalling board-level commitment to technology-led productivity gains.[1]Commonwealth Bank, “The Forces Impacting Digital Transformation in Manufacturing,” commbank.com.au Komatsu adopted SAP SuccessFactors, achieving up to 40% HR-process efficiency and a 2% enterprise-level productivity lift with four-year payback. Such results reinforce advisory demand that spans architecture design, change management and value tracking.

ESG and Net-Zero Compliance Needs

Mandatory Australian Sustainability Reporting Standards effective January 2025 obligate large companies to publish climate-related financial disclosures. Directors acknowledge the strategic risk yet often lack measurement competence, driving calls for external assurance frameworks. Rio Tinto’s pledge to halve Scope 1 and 2 emissions by 2030, coupled with a 28% rise in Indigenous procurement spend, illustrates how ESG ambitions now link operations, community and disclosure programmes.[2]Rio Tinto, “2024 Annual Report,” riotinto.com Consultants offering carbon-data governance, scenario analysis and assurance see widening pipelines across mining, finance and retail.

Generative-AI Strategy and Implementation Advisory

Federal modelling contends that AI could add USD 200 billion and 150,000 jobs annually by 2030. Healthcare already leads uptake, applying AI to clinical decision support and administrative automation. Rio Tinto deploys machine-learning for predictive maintenance, while BlueScope Steel leverages industrial AI to cut downtime. Adoption obstacles skills gaps, governance and data quality translate into sustained advisory briefs around operating-model redesign and risk controls.

Public-Sector Shift Away from Big Four Creates Mid-Tier Openings

Canberra has trimmed spending on large consulting partnerships by USD 890 million over two years and now requires that at least 25% of sub-USD 1 billion contracts go to SMEs. Boutique firms report four-fold jumps in new mandates as agencies diversify supplier rosters. New entrants like Oliver Wyman and KordaMentha have opened local offices, intensifying competition for policy, transformation and audit assignments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Client budget compression | -1.5% | Global | Short term (≤ 2 years) |

| Intensifying fee competition | -0.8% | Global | Medium term (2-4 years) |

| Government insourcing of consulting skills | -0.6% | National (Canberra focus) | Medium term (2-4 years) |

| Talent scarcity and wage inflation | -1.1% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Client Budget Compression During Economic Uncertainty

Reserve Bank surveys show expected price rises slowing to 4% as companies cite demand softness and competitive pressure.[3]Australian Industry Group, “Australian Industry Outlook 2024,” aigroup.com.au Energy-intensive manufacturers face triple-digit cost increases, with Orica and Incitec Pivot flagging production shifts and closures. Tighter cash flows lift scrutiny on consulting ROI, shortening project horizons and fuelling fixed-fee or outcome-based contracting.

Talent Scarcity and Wage Inflation

Australia lacks more than 50,000 qualified engineers, while renewable-energy build-outs could add 200,000 extra technical jobs by 2033. Consulting firms compete fiercely for scarce specialists, inflating compensation and eroding margin headroom. Simultaneously, clients divert budgets to internal capability building, dampening discretionary advisory spend but creating reskilling and automation consulting niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Large Enterprises Anchor Demand; SMEs Surge Under Reforms

Large enterprises generated 73.82% of 2025 revenue, reflecting deep pockets and multi-site transformation agendas. Their framework agreements underpin predictable pipelines, yet vendor rationalisation keeps fee rates in check. The Australia management consulting services market size attributable to this cohort is forecast to expand steadily on the back of continuing core-bank platform upgrades and cross-border compliance needs.

SMEs, buoyed by procurement quotas and affordable cloud tools, will post a 9.62% CAGR to 2031. Advisory scopes remain modular often centred on targeted AI pilots or ESG readiness but volume growth lifts aggregate spend. Government rules reserving 40% of sub-USD 20 million jobs for smaller contractors amplify addressable demand in Canberra and regional hubs, reinforcing competition among boutique providers.

By Service Type: Digital Transformation Consulting Leads and Accelerates

The digital transformation consulting segment occupied the largest market share of 19.94% in 2025, and digital transformation consulting is expected to witness the highest CAGR of 8.02% over the forecast period, digital transformation consulting has become a prominent segment within the management consulting market. This growth is driven by the increasing necessity for enterprises, government bodies, and SMEs to adopt technology as a fundamental component of their operations.

Advisory services in digital transformation include modernizing enterprise architecture, strategizing cloud migrations, developing data platforms, digitizing customer experiences, adopting agile models, and enhancing cybersecurity. These services require a combination of technological expertise and a strong understanding of change management and business strategy.

By Delivery Model: Hybrid Engagements Gain Traction

The hybrid consulting segment occupied the largest market share of 48.92% in 2025, hybrid consulting integrates on-site and remote delivery elements within unified engagement frameworks, strategically deploying physical presence for activities benefiting from face-to-face interaction while executing routine work virtually to optimize economics and consultant productivity. The model reflects the understanding that neither pure on-site nor fully remote approaches effectively balance efficiency, effectiveness, and stakeholder preferences across diverse engagement types. Hybrid consulting aligns consulting delivery to prevailing client organizational operating models and workforce expectations.

Remote and virtual engagements are expanding at a 8.35% CAGR, aided by collaboration platforms and acceptance of distributed work practices. Consultants now assemble cross-border specialist pods, compressing travel costs and tapping global talent pools. Nevertheless, relationship building and on-premise change-management remain critical in risk-heavy implementations.

By End-user Industry: Government and Public Dominant; Energy and Utilities Outpaces

The government and public sector segment occupied the largest market share of 18.24% in 2025, The government and public sector consulting landscape has undergone significant restructuring due to scrutiny of consulting practices, policy changes aimed at reducing reliance on external consultants, and the fallout from recent controversies. Public sector consulting spending has slowed considerably, reflecting a shift toward strengthening in-house advisory capabilities. This change has disproportionately affected larger firms, while mid-tier and boutique consultancies have benefited from a diversified vendor approach.

Energy and utilities are expected to witness the highest CAGR of 9.1% over the forecast period, Australia's transition to renewable energy, decarbonization efforts, and grid modernization have significantly increased the demand for energy and utilities consulting. The sector is undergoing a comprehensive transformation, including retiring fossil fuel-based generation, deploying renewables, enhancing interstate transmission, stabilizing the grid, orchestrating distributed energy resources, expanding EV charging infrastructure, and implementing advanced pricing and demand response programs. This restructuring has created sustained demand for consulting services in strategy, technology, regulatory compliance, and stakeholder management.

Geography Analysis

Metropolitan nodes dominate the Australia management consulting services market, with Sydney, Melbourne and Brisbane collectively accounting for roughly 70% of 2025 value. Sydney’s concentration of banks and insurers supports high-value risk, cyber and customer-experience projects. Melbourne’s diversified base across manufacturing and biotech fuels operations and technology engagements. Canberra, though smaller by revenue, exerts outsized influence through federal spending realignment that increasingly favours SMEs and niche specialists.

Regional opportunities are widening as mining-heavy Western Australia and Queensland pursue decarbonisation, predictive-maintenance and Indigenous-engagement mandates. Procurement reforms obligate agencies to source more work locally, encouraging regional consultancies to scale capabilities. National firms leverage virtual-delivery toolkits to serve dispersed clients while mitigating travel and talent shortages.

Political stability and a USD 15 billion National Reconstruction Fund provide long-term project visibility, contrasting with the volatility seen in some Asia–Pacific neighbours. Yet acute engineering deficits, clustered mainly in capitals, constrain delivery capacity for large infrastructure and energy programmes. Firms able to mobilise interstate talent quickly gain competitive distance.

Competitive Landscape

The market shows moderate concentration, with the Big Four plus Accenture still controlling a significant share yet experiencing erosion in government work. Canberra’s spending cuts lowered their public-sector billings by more than 40%, freeing space for agile challengers. Boutique specialists have capitalised, tripling or quadrupling win rates in defence, health and climate portfolios.

Differentiation has shifted from scale to sector depth and technology prowess. Firms with proprietary AI toolkits or ESG-data platforms attract premium engagements, while traditional strategy houses partner with cloud hyperscalers to stay relevant. Examples include HCLTech’s digital-fan-experience mandate for Cricket Australia and Cisco’s operational-efficiency collaboration with Woolworths.

Senior technologists and sustainability experts command salary premiums that squeeze margins. Firms offering flexible work models and equity participation report better retention, countering wage inflation and preserving delivery capacity.

Australia Management Consulting Services Industry Leaders

Deloitte Australia

PwC Australia

KPMG Australia

EY Australia

Accenture Australia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Scyne Advisory wins ethics clearance and re-enters federal tender panels.

- January 2025: Australian Sustainability Reporting Standards become mandatory, sparking immediate compliance-advisory demand.

- November 2024: Federal government cuts Big Four spending by USD 890 million over two years.

- September 2024: New Commonwealth Procurement Rules lift SME targets to 25% for sub-USD 1 billion contracts.

Australia Management Consulting Services Market Report Scope

The Australia Management Consulting Services Market encompasses professional advisory services spanning strategy development, operations optimization, digital transformation, regulatory compliance, risk management, and specialized industry expertise delivered to enterprises, government agencies, and organizations across Australia, including traditional management consulting, technology-enabled advisory, ESG consulting, and implementation support services, while excluding pure technology implementation, software development, and training services without strategic advisory components, with market evolution toward AI-enabled consulting and integrated digital transformation solutions.

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Other Service Types |

| On-site Consulting |

| Remote / Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other Industries |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Other Service Types | |

| By Delivery Model | On-site Consulting |

| Remote / Virtual Consulting | |

| Hybrid Consulting | |

| By End-user Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other Industries |

Key Questions Answered in the Report

What is the current size of the Australia management consulting services market?

The market is valued at USD 9.43 billion in 2026.

How fast is the Australia management consulting services market expected to grow?

It is projected to expand at a 6.07% CAGR, reaching USD 12.66 billion by 2031.

Which service type is growing fastest?

Digital transformation consulting consulting is forecast to post the highest 8.02% CAGR through 2031.

Why are SMEs gaining traction in consulting engagements?

Revised Commonwealth Procurement Rules reserve at least 25% of sub-USD 1 billion federal contracts for SMEs, lifting their addressable demand.

How are ESG regulations influencing consulting demand?

Mandatory sustainability disclosures effective January 2025 are driving firms to seek advisory support on data governance, scenario analysis and assurance frameworks.

Page last updated on: