South Africa Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

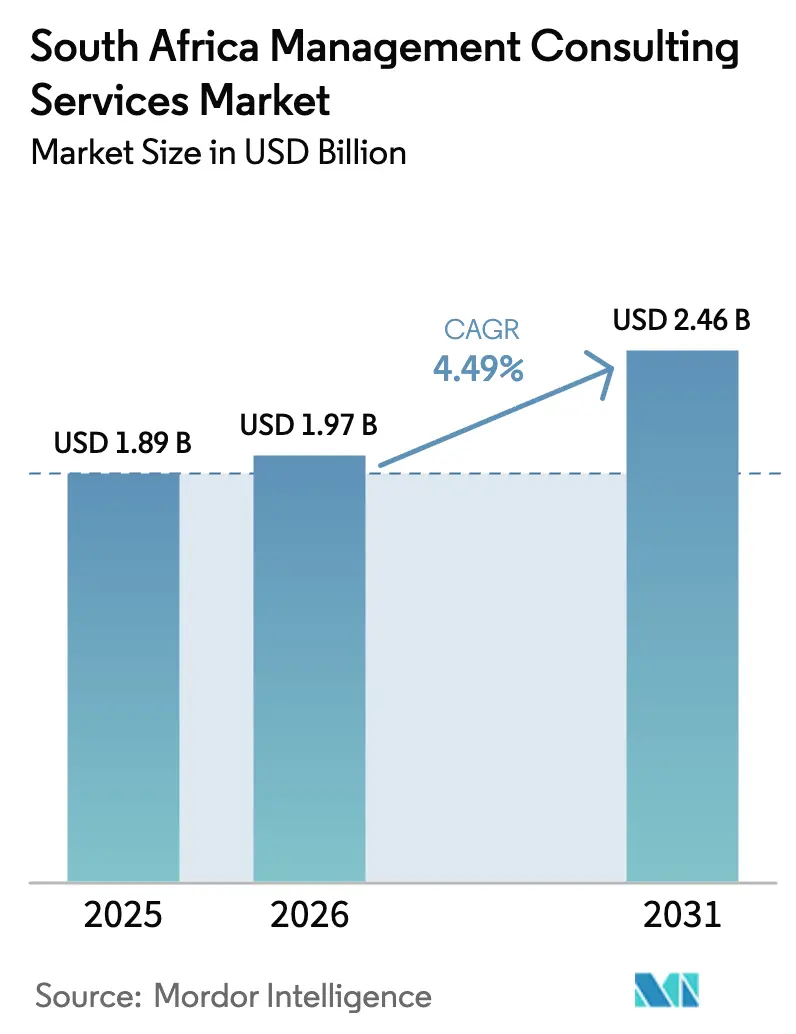

| Base Year Market Size (2025) | USD 1.89 Billion |

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.46 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Management Consulting Services Market Analysis by Mordor Intelligence

The South Africa management consulting services market size is expected to grow from USD 1.89 billion in 2025 to USD 1.97 billion in 2026 and is forecast to reach USD 2.46 billion by 2031 at 4.49% CAGR over 2026-2031. A stable electricity supply after 300 days without load-shedding has restored business confidence, allowing organisations to revive long-term transformation programmes. Government commitment of ZAR 500 million (USD 27.8 million) to a national Digital Skills Initiative targeting 100,000 youth by 2026 is enlarging the domestic talent pool and lowering implementation barriers for consulting-led digital projects. Accelerated cloud build-outs, highlighted by Teraco’s 40 MW data-centre investment in Johannesburg, are pushing demand for technology and operations expertise.[1]Data Center Dynamics Editorial Team, “South Africa's Teraco breaks ground on 40 MW data center in Johannesburg,” Data Center Dynamics, datacenterdynamics.com Meanwhile, regulatory pressure from B-BBEE and emerging ESG mandates is driving recurring advisory spend as firms seek external guidance on complex scorecards and compliance roadmaps. Together, these factors underpin healthy expansion in the South Africa management consulting services market.

Key Report Takeaways

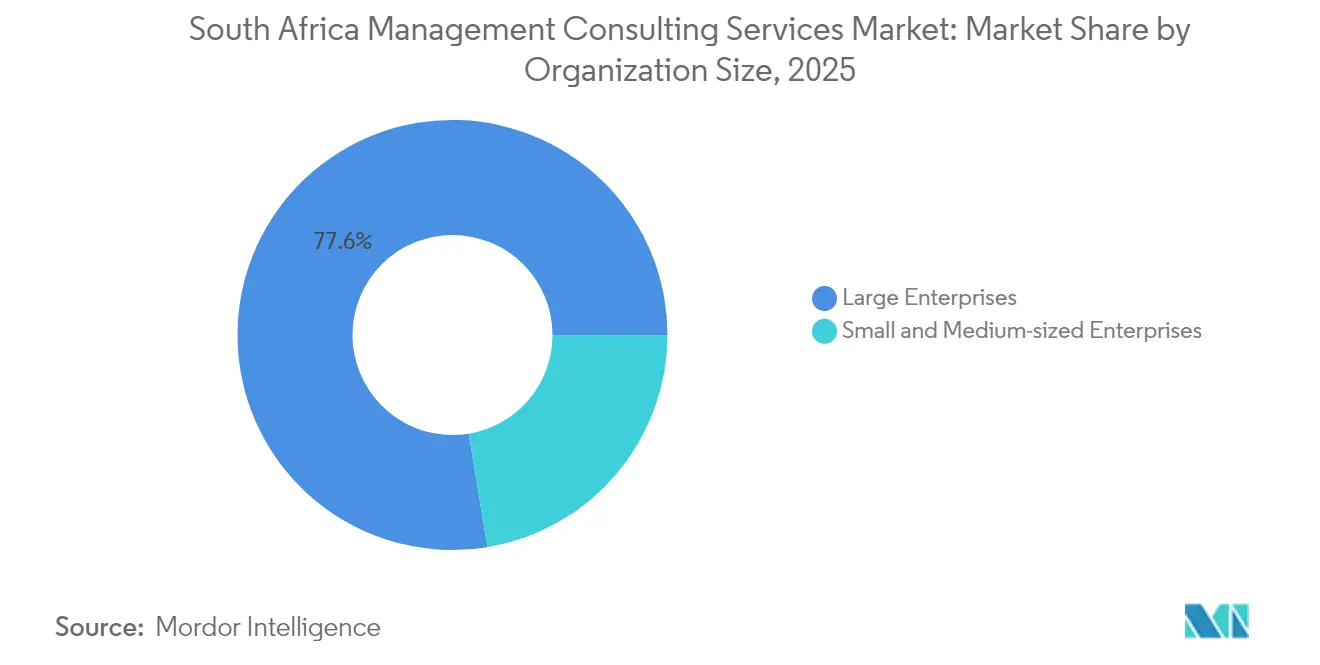

- By organization size, large enterprises held 77.60% of the South Africa management consulting services market share in 2025, while small and medium-sized enterprises are set to grow the fastest at a 5.39% CAGR through 2031.

- By service type, operations consulting commanded 32.75% revenue share in 2025; technology consulting is forecast to expand the quickest at a 4.61% CAGR to 2031.

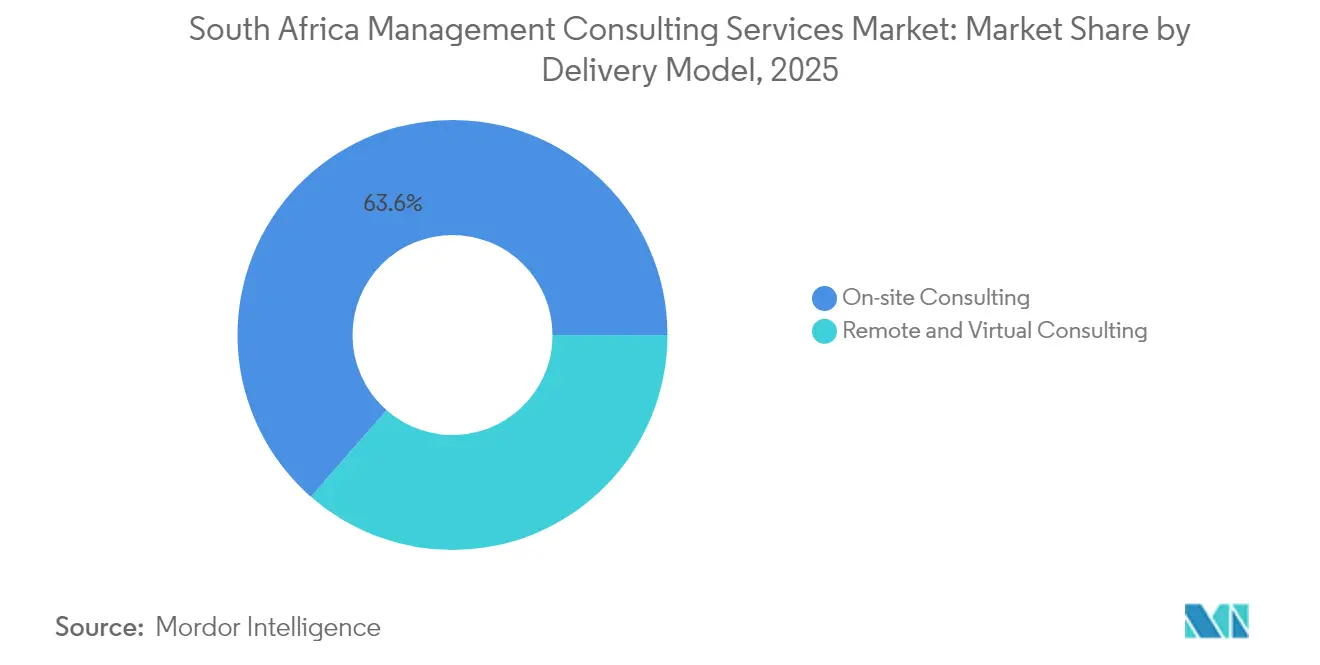

- By delivery model, on-site consulting captured 63.55% of the South Africa management consulting services market size in 2025, whereas remote/virtual consulting is advancing at a 5.01% CAGR through 2031.

- By end-user industry, financial services led with 25.05% market share in 2025; healthcare and life sciences are projected to post the highest 4.82% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-transformation acceleration across South African enterprises | +1.2% | National, with concentrations in Johannesburg and Cape Town | Medium term (2-4 years) |

| Regulatory pressure from B-BBEE and ESG compliance | +0.8% | National, with emphasis on major urban centers | Long term (≥ 4 years) |

| Post-pandemic operational resilience and cost-optimization push | +0.7% | National, with a focus on the manufacturing and retail sectors | Short term (≤ 2 years) |

| Expanding public-sector "consultocracy" spend | +0.6% | National, concentrated in government centers | Medium term (2-4 years) |

| Johannesburg's rise as a pan-African HQ hub | +0.4% | Johannesburg and Gauteng province | Long term (≥ 4 years) |

| SME uptake of remote-consulting platforms in secondary cities | +0.3% | Secondary cities and rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-transformation Acceleration Across South African Enterprises

Widespread grid stability and ongoing investments in hyperscale infrastructure have reignited enterprise appetite for large-scale digital makeovers. Major cloud providers are doubling local capacity, while Teraco’s latest data-centre build signals confidence in sustained demand for co-location and inter-connection services. The state-funded skills initiative is expected to furnish a steady pipeline of certified developers and cybersecurity specialists, trimming project risk and shortening deployment cycles. Corporations are therefore ramping up cloud migration, AI experimentation, and zero-trust security frameworks, driving a 4.7% CAGR in technology consulting revenues. As digital value chains expand to fintech, e-commerce, and smart-manufacturing domains, consulting firms with end-to-end execution capabilities are capturing multi-year mandates across industry verticals.

Regulatory Pressure from B-BBEE and ESG Compliance

Updated Codes of Good Practice and tighter verification thresholds continue to elevate the strategic importance of B-BBEE planning. Companies must recalibrate ownership, supply-chain, and socio-economic development levers to protect tender eligibility and brand reputation, stimulating demand for specialised scorecard optimisation and scenario modelling. Concurrently, global buyers are factoring ESG credentials into sourcing decisions; the EU Carbon Border Adjustment Mechanism is already nudging exporters toward decarbonisation pathways.[2]Zawya Newsdesk, “South Africa's energy trends for 2025 – the light at the end of the tunnel grows brighter,” Zawya, zawya.com Consulting mandates now combine B-BBEE restructuring with greenhouse-gas audits and sustainability reporting, creating bundled compliance offerings that reinforce client stickiness. Local boutiques with deep regulatory fluency are partnering with global sustainability practices to deliver integrated solutions spanning policy interpretation, target-setting, and impact measurement.

Post-pandemic Operational-resilience and Cost-optimization Push

The pandemic underscored supply-chain fragility and intensified the need for leaner operating models. Manufacturing firms employing 1.6 million people in 2024 pivoted toward automation, predictive maintenance, and near-shoring to mitigate future shocks. Retailers, facing margin pressure from cost-sensitive consumers, are redesigning fulfilment networks and deploying omnichannel inventory systems. These interventions underpin the 33.1% share held by operations consulting in 2024 and affirm continued spend on process diagnostics, value-stream mapping, and technology-enabled workforce management. Consulting engagements increasingly hinge on quantifiable cost take-outs and resilience metrics, reinforcing demand for hybrid teams that blend industry engineers with data scientists.

Expanding Public-sector “Consultocracy” Spend

Persistent skills shortages in government departments have entrenched reliance on external advisory capacity. The Government Technical Advisory Centre channels specialist procurement, project-finance, and change-management expertise into national infrastructure and service-delivery programmes. Municipalities, utilities, and transport agencies are similarly outsourcing feasibility studies and organisational redesign, sustaining a positive demand outlook for public-sector consulting. Tender frameworks that prioritise B-BBEE credentials reward firms with diverse ownership structures, encouraging global networks to partner with empowered local entities. Long-horizon mandates covering digital government, revenue-collection enhancement, and smart-city planning bolster multi-year revenue visibility for consultancies with proven public-sector track records.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Client-budget squeeze from stubborn unemployment | -0.9% | National, with a concentration in secondary cities | Medium term (2-4 years) |

| Load-shedding and energy insecurity are disrupting project delivery | -0.6% | National, with rural areas most affected | Short term (≤ 2 years) |

| Wage inflation from global talent poaching | -0.4% | Major urban centers, particularly Johannesburg and Cape Town | Medium term (2-4 years) |

| Emerging client skepticism of AI-generated advice | -0.2% | National, with emphasis on traditional industries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Client-budget Squeeze from Stubborn Unemployment

Unemployment-linked household strain is tightening discretionary spending, particularly among SME clients that already operate on thin working-capital buffers. Retailers are shifting focus toward essential categories and value-led propositions, leaving less room for broad-based consulting assignments. To preserve pipeline momentum, advisory firms are reframing proposals around quick-win diagnostics, shared-risk pricing, and phased deployments that align fees with realised benefits. While this flexibility sustains engagement volumes, average contract size growth remains subdued, trimming the overall uplift potential for the South Africa management consulting services market.

Load-shedding and Energy Insecurity Disrupting Project Delivery

Although grid performance improved markedly in 2025, businesses still recall costly production stoppages and therefore favour modular investment horizons. Manufacturing plants are diverting capital to embedded solar, battery storage, and diesel backup, crimping budgets available for discretionary advisory spend.[3]RSM South Africa Analysts, “Five routes to manufacturing growth in South Africa,” RSM South Africa, rsm.global Project timelines must also account for potential power interruptions in remote facilities, raising logistical overheads for on-site consulting teams. Remote engagement mitigates some risk, yet critical phases such as plant walk-throughs and user-acceptance testing often require physical presence, exposing schedules to residual energy-supply uncertainty. These factors temper market growth despite broader infrastructure gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Enterprise Dominance Drives Market Stability

Large enterprises, encompassing financial conglomerates, telecom carriers, and diversified industrial groups, accounted for 77.60% of the South Africa management consulting services market share in 2025. Their scale necessitates integrated transformation roadmaps covering cloud migration, supply-chain visibility, and regulatory alignment, enabling multi-stream engagements that sustain consultant utilisation over several years. Budget depth also permits experimentation with advanced analytics, generative AI pilots, and holistic ESG programmes that smaller firms often defer.

Small and medium-sized enterprises contributed a modest portion of 2025 revenue, yet are forecast to grow 5.39% annually to 2031, outpacing the overall South Africa management consulting services market. Government loan guarantees, incubator networks, and accessible remote-consulting platforms are widening advisory affordability. Boutique firms tailor bite-sized diagnostic offerings and outcome-based pricing, demonstrating pay-back within months and easing cash-flow anxiety. As digitally native SMEs emulate the rapid scale trajectory of pioneers like TymeBank, they increasingly view external advisors as essential partners for governance, cybersecurity, and data-driven marketing.

By Service Type: Operations Leadership Meets Technology Acceleration

Operations consulting controlled 32.75% of 2025 revenue as clients pursued productivity rebounds after years of power-related disruptions. Engagements centre on process mining, warehouse automation, and resilience scorecards, linking fee triggers to cost-out targets and throughput gains. The South Africa management consulting services market size for operations is expected to rise steadily but concede relative share as digital transformation matures.

Technology consulting, advancing at a 4.61% CAGR, benefits from cloud-first mandates, AI use-case exploration, and aggressive cybersecurity posture upgrades. Public-cloud spending expanded 36% in 2025, catalysing demand for migration blueprints, DevSecOps frameworks, and talent-upskilling pathways. The segment also covers smart-grid planning, telemedicine platform roll-outs, and fintech core-system modernisation, ensuring cross-industry relevance. Strategy, HR, and other specialist advisory practices continue to complement digital agendas by aligning leadership, culture, and sustainability narratives.

By Delivery Model: Traditional On-site Dominance Faces Remote Disruption

On-site engagements held a 63.55% share of the South Africa management consulting services market size in 2025, reflecting relationship-centric project cultures and the perceived value of co-located problem-solving. Board-level workshops, change-management roadshows, and facility diagnostics still require physical immersion to capture organisational nuances.

Remote and hybrid models are, however, rising fastest at 5.01% CAGR as bandwidth improvements, collaboration suites, and the Digital Nomad Visa expand talent pools. International practitioners stationed in Cape Town can now serve overseas clients while contributing niche expertise to domestic projects, compressing turnaround times and lowering rate cards. Local firms are embedding virtual playbooks—covering stakeholder mapping, sprint governance, and digital-whiteboard protocols—to maintain quality parity with on-site delivery while harvesting cost efficiencies.

By End-user Industry: Financial Services Leadership Amid Healthcare Acceleration

Financial services generated 25.05% of 2025 advisory spend, driven by open-banking mandates, fintech competition, and stringent capital adequacy oversight. Traditional lenders are overhauling core architectures and embedding AI-led risk analytics, underpinning high-value technology and strategy consulting mandates. Insurers, meanwhile, are piloting usage-based policies and parametric covers, requiring actuarial-tech integration support.

Healthcare and life sciences are predicted to log the fastest 4.82% CAGR through 2031, underpinned by National Health Insurance roll-out and rising telemedicine adoption. Hospitals and clinics must redesign patient-flow models, integrate electronic health records, and vet interoperability standards, spurring demand for process redesign and cybersecurity expertise. Elsewhere, energy utilities, manufacturing, public administration, and retail sectors each contribute meaningful volumes, sustaining service-portfolio diversification across the wider South Africa management consulting services industry.

Geography Analysis

Johannesburg and its Sandton financial precinct anchor the bulk of consulting revenue, hosting the JSE and more than 12,300 millionaires who influence board-level decision-making. Concentrated corporate head offices create dense demand for enterprise-scale transformation and regulatory advisory services, reinforcing premium bill rates. Cape Town, buoyed by a vibrant start-up ecosystem and an attractive lifestyle for digital nomads, is fast becoming the country’s technology-consulting hotspot, with global cloud providers expanding regional infrastructure to service pan-African workloads.

Gauteng province captures the largest slice of the South Africa management consulting services market, yet Western Cape’s entrepreneurial culture is fuelling above-average growth in remote-first engagements and sustainability projects. Average residential property values of ZAR 1.8 million (USD 96,000) signal robust purchasing power, supporting higher fee tolerance for mid-caps adopting sophisticated analytics solutions. KwaZulu-Natal follows as an emerging cluster, where port logistics modernisation and industrial corridor upgrades necessitate supply-chain optimisation expertise.

Secondary cities such as Bloemfontein and Kimberley are joining the consulting map as SMEs embrace digital channels to access virtual advisory sessions. Government-backed innovation hubs are helping rural agribusinesses deploy precision-farming platforms, opening nascent pockets of demand. While physical travel remains essential for complex infrastructure audits, the spread of high-speed fibre is broadening the geographic footprint of the South Africa management consulting services market.

Competitive Landscape

The market exhibits moderate fragmentation, with the top five global networks and several regional specialists sharing roughly 55% combined revenue. Deloitte, Accenture, McKinsey, and BCG target enterprise-wide transformations, leveraging global delivery centres and proprietary analytics platforms. Accenture’s 2024 launch of a generative-AI centre of excellence in Johannesburg underscores the shift toward technology-infused consulting propositions.[4]Accenture South Africa, “Let there be change,” Accenture, accenture.com

Local boutiques differentiate through regulatory depth and sector intimacy. Firms such as SERR Synergy advise on intricate B-BBEE structures, while niche operators service pan-African expansion, cross-border transaction support, and family-business governance. Andersen Global broadened its domestic reach in 2024 by acquiring Johannesburg-based Merchantec Capital, adding investment-banking and valuation skills that blend with strategic consulting.

Competitive advantage now hinges on measurable ROI, flexible contracting, and multi-disciplinary squads blending industry veterans with data scientists and sustainability engineers. Remote-delivery capability is an increasingly decisive factor in bid evaluations, especially for cost-sensitive public and SME sectors. With PwC exiting nine Sub-Saharan markets in early 2025, mid-tier rivals are vying to capture displaced clients, signalling potential shake-ups in regional share dynamics.

South Africa Management Consulting Services Industry Leaders

Deloitte

PwC

Accenture Plc

KPMG

EY (Ernst & Young)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: PwC wound down operations across nine Sub-Saharan African countries after a strategic review, opening market space for local and regional competitors.

- March 2025: The South African government allocated ZAR 500 million (USD 27.8 million) to the Digital Skills Initiative, targeting 100,000 trained youth by 2026 to enhance the national digital talent pipeline.

- February 2025: Eskom registered 300 days without load-shedding for the first time since 2018, stabilising operating conditions and encouraging long-term consulting engagements.

- December 2024: The Energy Council of South Africa signed an MoU with Energy Exemplar to build national capacity in energy-system modelling, supporting consulting demand in transition planning.

South Africa Management Consulting Services Market Report Scope

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types |

| On-site Consulting |

| Remote / Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other Industries |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types | |

| By Delivery Model | On-site Consulting |

| Remote / Virtual Consulting | |

| By End-user Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other Industries |

Key Questions Answered in the Report

What is the current size of the South Africa management consulting services market?

The market is valued at USD 1.97 billion in 2026 and is forecast to reach USD 2.46 billion by 2031.

Which segment holds the largest share of the South Africa management consulting services market?

Operations consulting leads by service type with a 32.75% revenue share in 2025.

Why are technology consulting services growing faster than other categories?

Enterprise cloud migrations, AI adoption, and heightened cybersecurity requirements are propelling a 4.61% CAGR for technology consulting.

How is the Digital Nomad Visa influencing consulting delivery models?

The visa widens access to global talent, enabling hybrid teams that combine on-site insight with cost-effective remote execution, supporting a 5.01% CAGR for virtual consulting engagements.

What factors restrain market growth despite improved grid stability?

Client-budget pressures linked to high unemployment and residual concerns over energy security continue to temper large-scale consulting investments.

Which end-user industry is expected to grow the fastest through 2031?

Healthcare and life sciences are projected to expand at a 4.82% CAGR as the National Health Insurance roll-out and telemedicine adoption accelerate demand for advisory support.

Page last updated on: