Belgium Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

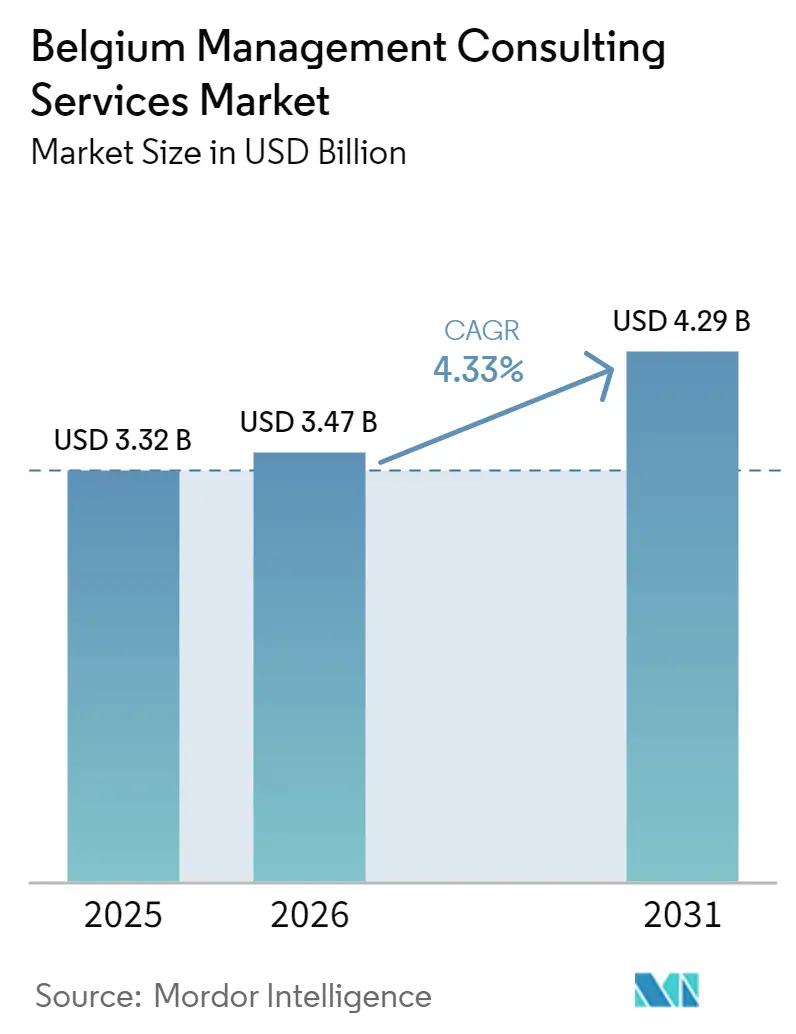

| Base Year Market Size (2025) | USD 3.32 Billion |

| Market Size (2026) | USD 3.47 Billion |

| Market Size (2031) | USD 4.29 Billion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

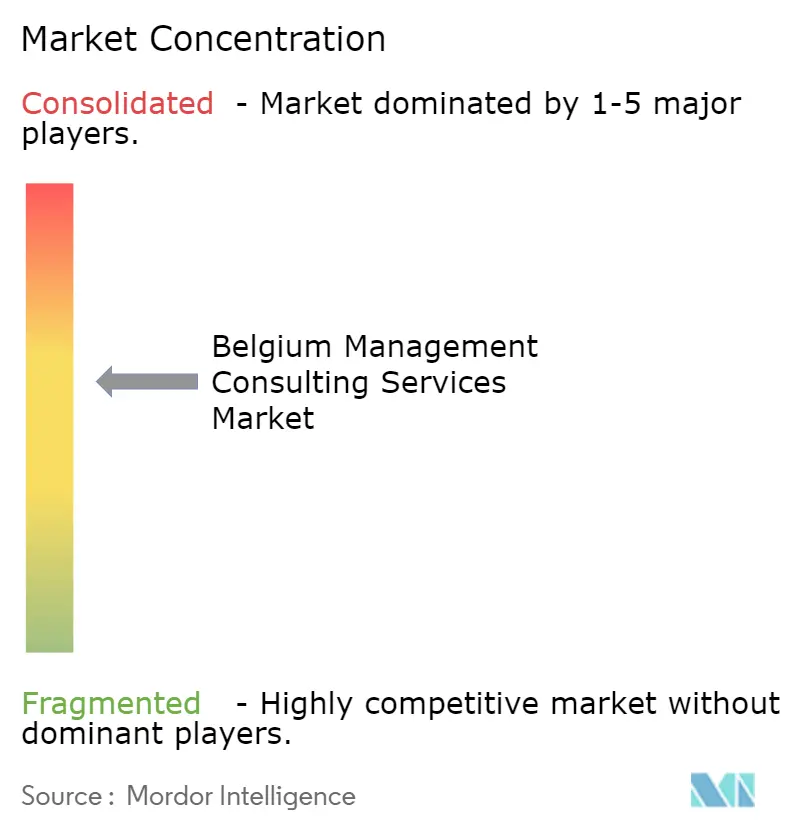

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium Management Consulting Services Market Analysis by Mordor Intelligence

The Belgium management consulting services market size is expected to grow from USD 3.32 billion in 2025 to USD 3.47 billion in 2026 and is forecast to reach USD 4.29 billion by 2031 at 4.33% CAGR over 2026-2031. Structural demand derives from Brussels’ role as the European Union’s administrative hub, which concentrates regulatory, funding, and public-affairs mandates within a two-kilometer radius of the European Commission. Sustainability assurance engagements linked to the Corporate Sustainability Reporting Directive (CSRD) continue to post double-digit revenue growth among Big Four firms, while specialist policy boutiques record a brisk pipeline of AI Act and Critical Raw Materials Act implementation projects. The Belgium management consulting services market also benefits from generous regional subsidies that reimburse up to 90% of consulting fees for small and medium-sized enterprises, effectively lowering price barriers and broadening the client base. Rising digital-transformation outlays, particularly in cloud migration, data modernization, and sovereign-AI deployments, sustain high utilization rates across technology-focused practices.

Key Report Takeaways

- By consulting service line, Digital Transformation Consulting held 26.47% of Belgium management consulting services market share in 2025, reflecting sustained enterprise investment in cloud and AI modernization. Risk and Compliance Consulting is projected to expand at a 5.02% CAGR through 2031, the fastest among all major service categories.

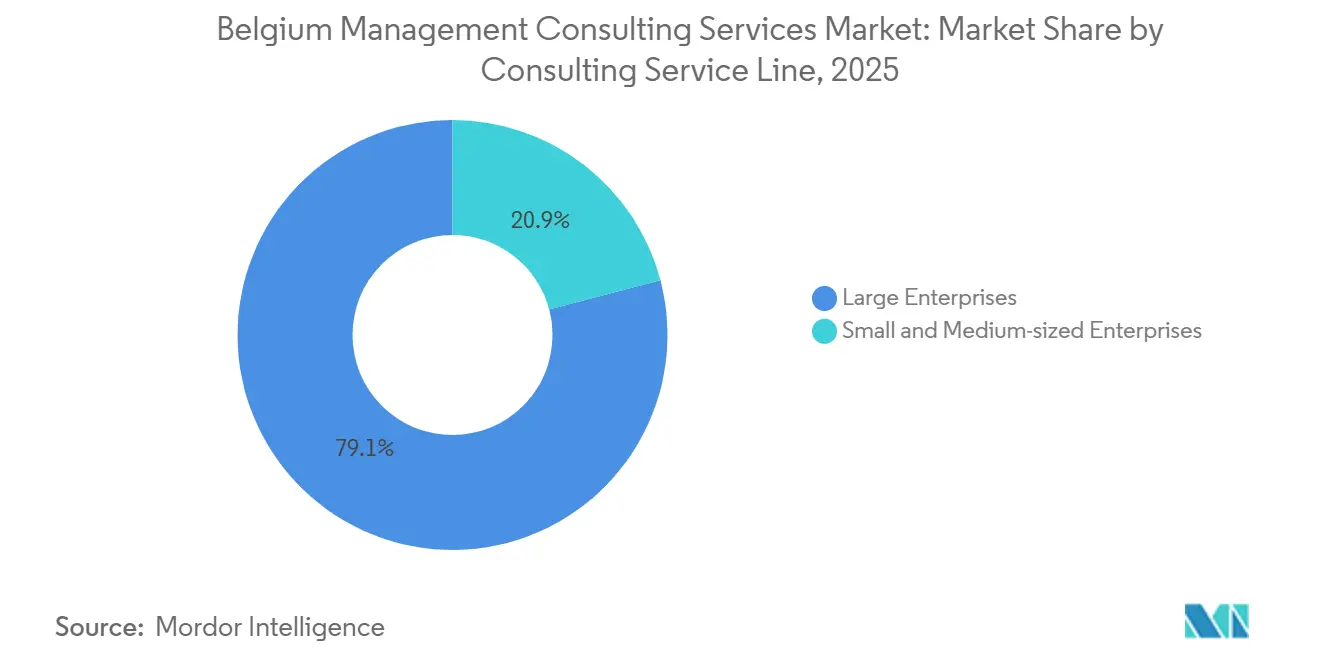

- By organization size, Large Enterprises captured 60.86% of 2025 revenues, while the SME segment is expected to advance at a 4.41% CAGR as regional grants subsidize consulting fees.

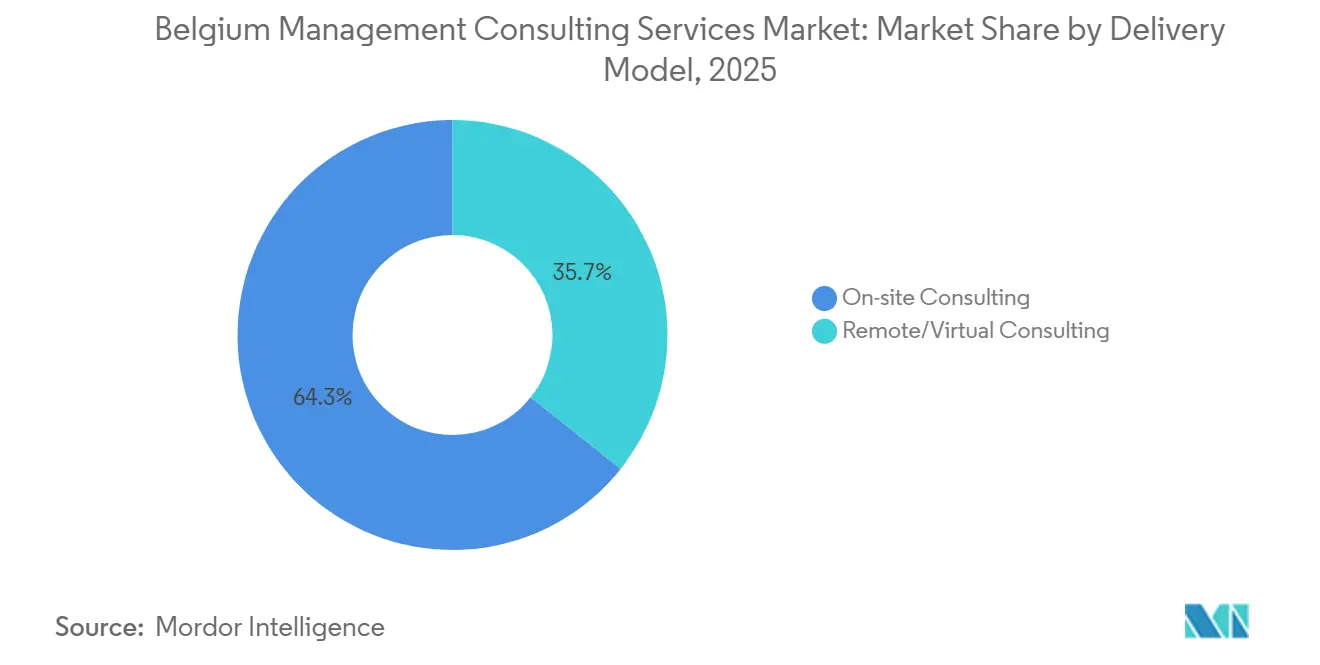

- By delivery model, On-Site Consulting retained 68.39% of 2025 spending, yet Hybrid Consulting is poised to grow at a 4.87% CAGR through 2031 on post-pandemic client preferences.

- By end-user industry, Banking and Insurance led with a 20.17% share in 2025; Healthcare is forecast to grow at 4.76% CAGR on the back of the national eHealth Action Plan.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Belgium Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-Funded Digital Transformation Wave in Belgian Mid-Market Firms | +0.9% | National, concentrated in Brussels-Capital and Flanders | Medium term (2-4 years) |

| Mandatory CSRD Sustainability Reporting Advisory Demand | +0.8% | National, with spillover to EU subsidiaries | Short term (≤ 2 years) |

| Brussels-Based EU Policy Consulting Tailwinds for 2026-2029 Funding Cycle | +0.7% | Brussels-Capital, EU-wide client base | Long term (≥ 4 years) |

| Post-COVID Operational Excellence and Cost-Out Imperatives | +0.6% | National, stronger in Flanders and Wallonia | Medium term (2-4 years) |

| AI-Driven Shared-Service Reshoring to Low-Tax Zones | +0.5% | National, focus on Brussels-Capital and Flemish Brabant | Long term (≥ 4 years) |

| Flanders Moonshot 2040 Grants Stimulating Deep-Tech Consulting | +0.3% | Flanders region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU-Funded Digital Transformation Wave in Belgian Mid-Market Firms

Belgium’s Digital Decade National Roadmap directs EUR 1.5 billion (USD 1.69 billion) into digital infrastructure, cybersecurity, and advanced skills through 2027, channeling significant volumes toward accredited consultancies. Regional co-funding programs reimburse 25%-90% of advisory fees, effectively amplifying demand among small and medium-sized clients that traditionally deferred professional services.[1]European Commission, “Digital Decade National Roadmaps,” digital-strategy.ec.europa.eu The pipeline is strongest for cloud migration, ERP modernization, and data-integration mandates that align with eGovernment interoperability requirements. Consulting firms with SME-appropriate delivery models capture quick-turn projects, while larger players monetize follow-on implementation and managed-services deals. As subsidy disbursements peak in 2027-2028, the Belgium management consulting services market registers a measurable uplift in volume and average contract value.

Mandatory CSRD Sustainability Reporting Advisory Demand

The CSRD obliges roughly 50,000 European companies, including Belgian multinationals, to publish ESG-aligned disclosures backed by limited assurance from 2025 and reasonable assurance from 2028.[2]KPMG Belgium, “CSRD Reporting Obligations,” kpmg.com Belgian consultancies staff dedicated practices for materiality assessment, ESG data architecture, and audit-readiness, generating multi-year recurring engagements. Technology partners contribute automated double-materiality analysis and peer-benchmarking tools that compress project timelines and boost margins. As regional language requirements add documentation complexity, bilingual consultants capture a premium, widening the talent gap. The directive’s phased extension to non-EU subsidiaries anchors a steady revenue stream for the Belgium management consulting services market through 2031.

Brussels-Based EU Policy Consulting Tailwinds for 2026-2029 Funding Cycle

The overlapping close-out of the 2021-2027 Multiannual Financial Framework and preparatory work for the 2028-2034 cycle sustain advisory demand in grant strategy, stakeholder engagement, and regulatory positioning. Specialist teams guide clients through AI Act conformity assessments, NIS2 cybersecurity obligations, and Digital Europe Programme tenders, driving premium pricing in Brussels’ tight labor market.[3]KiTalent Research Team, “Brussels EU Professional Services in 2026: The Two Markets Hiding Inside One City,” KiTalent, kitalent.com Elevated office rents and competition for multilingual talent raise overhead for mid-tier firms but reinforce entry barriers for new entrants. The confluence of funding and rule-making activities supports the Belgium management consulting services market well beyond the near term.

Post-COVID Operational Excellence and Cost-Out Imperatives

Persistent cost inflation and regulatory scrutiny of margin drivers compel Belgian corporates to pursue lean transformations, shared-service optimization, and data-driven pricing strategies. Process-mining, robotic automation, and advanced analytics engagements yield documented savings of 15%-25% in back-office operations, strengthening the value proposition of consulting interventions. Pricing-transformation projects gain traction as 78% of Belgian companies identify pricing as a critical lever yet lack granular data. The Belgium management consulting services market therefore maintains a balanced mix of top-line growth and cost-out programs, diversifying revenue against macro shocks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Price-Based Competition Among Tier-1 and Big Four | -0.4% | National, acute in Brussels-Capital | Short term (≤ 2 years) |

| Shortage of Senior Bilingual Consultants Inflating Fees | -0.3% | National, notably Brussels-Capital and Flanders | Medium term (2-4 years) |

| Linguistic Fragmentation Raising Project Complexity | -0.2% | National, region-specific variation | Long term (≥ 4 years) |

| Near- and Off-Shoring of Small Projects to Eastern Europe | -0.2% | National, affects routine work | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Price-Based Competition Among Tier-1 and Big Four

A finite pool of large-enterprise mandates creates aggressive fee pressure as global strategy houses and the Big Four converge on the same accounts. Margins compress further when clients benchmark Brussels rates against lower-cost hubs, prompting firms to differentiate through technology enablement and offshore leverage. Compliance costs rise as authorities scrutinize algorithmic pricing and public-procurement practices, eroding profitability for firms without scale economies. The Belgium management consulting services industry therefore faces a short-term headwind until excess capacity rebalances.

Shortage of Senior Bilingual Consultants Inflating Fees

Belgium’s trilingual structure constrains supply of senior professionals fluent in Dutch, French, and English, extending hiring cycles and inflating compensation packages by 15%-35% versus neighboring markets. Scarcity is most pronounced in EU-policy and digital-risk domains, where mandates remain open for 8-12 months. Consultancies absorb higher salaries or risk delivery delays that jeopardize client satisfaction. Over the medium term, coordinated talent pipelines and selective off-shoring may gradually ease the constraint yet continue to temper growth for the Belgium management consulting services market.[4]Brussels Economy and Employment, “Cheque Entreprise,” economie-emploi.brussels

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Digital and Risk Services Take the Lead

Digital Transformation Consulting accounted for 26.47% of Belgium management consulting services market share in 2025, underpinned by cloud, data, and AI investments. Growing adoption of agentic AI platforms, sovereign cloud enclaves, and industry-specific accelerators ensures steady deal flow through 2031. In contrast, Strategy and Operations Consulting grapple with commoditization as technology players bundle advisory with implementation. Risk and Compliance practices, benefiting from NIS2 and DORA enforcement, are projected to outpace overall market growth at a 5.02% CAGR, reinforcing portfolio diversification across the Belgium management consulting services market.

Risk-specific engagements increasingly integrate cyber-resilience, third-party governance, and incident-simulation exercises, commanding premium day rates. Financial Advisory remains tied to deal volumes but gains a lift from restructuring assignments as interest-rate volatility continues. Sustainability advisory migrates from standalone projects to cross-functional programs that weave ESG metrics into enterprise-wide performance dashboards, contributing incremental margin uplift.

By Organization Size: Subsidies Fuel the SME Upswing

Large Enterprises retained 60.86% of 2025 revenue, leveraging multi-year transformation budgets that fund sizable consultant teams across core and non-core functions. Yet subsidy schemes that reimburse up to 90% of fees widen the addressable pool of SME clients, propelling the SME segment toward a 4.41% CAGR. The Belgium management consulting services market size for SME engagements is therefore on a positive trajectory, with rapid-cycle projects in eCommerce enablement, cybersecurity hygiene, and ESG data onboarding.

Consultancies recalibrate delivery models to fit compressed budgets and faster decision cycles typical of mid-market businesses. Certification requirements for subsidy eligibility further encourage SMEs to engage registered providers, embedding consultancies as long-term partners. Large Enterprises, meanwhile, continue to drive demand for CSRD, AI Act, and global-platform modernization, anchoring revenue stability across the cycle.

By Delivery Model: Hybrid Consulting Gains Lasting Acceptance

On-site Consulting captured 68.39% of 2025 spending, yet client appetite for flexibility fuels a robust 4.87% CAGR for hybrid models. Project teams now blend on-premise workshops with remote sprints and cloud-based tooling, lowering travel expenses and widening the talent bench. The Belgium management consulting services market benefits as firms source scarce skill sets from near-shore hubs while preserving in-person interactions for sensitive stakeholder engagements.

Sovereign-cloud capabilities and secure virtual rooms enable classified data handling within hybrid constructs, satisfying public-sector and regulated-industry mandates. Remote-only delivery finds traction with SMEs and compliance checklist engagements but remains a minority share because board-level transformation still relies on face-to-face leadership alignment.

By End-User Industry: Banking Holds Ground, Healthcare Accelerates

Banking and Insurance remained the largest vertical with a 20.17% share in 2025, sustained by DORA-driven technology refreshes and customer-experience modernization. Healthcare emerges as the fastest-growing vertical at 4.76% CAGR as the eHealth Action Plan funds 41 data-capability projects. The Belgium management consulting services market size attributed to healthcare is poised to expand as hospitals invest in interoperability, AI-driven diagnostics, and value-based care analytics.

Manufacturing and Energy clients focus on operational excellence in response to energy-price volatility, while the Public Sector unlocks EU-funded digital-government mandates. Retail and logistics firms pursue omnichannel integration and supply-chain resilience, rounding out a diversified industry mix that insulates the Belgium management consulting services market from sector-specific shocks.

Geography Analysis

Flanders, with its manufacturing and deep-tech clusters in Antwerp, Ghent, and Leuven, generates the largest regional revenue share and captures a sizeable portion of Moonshot Flanders grant-funded innovation projects. High vacancy rates for bilingual Dutch-English talent temper growth but simultaneously lift billable rates. Regional subsidies that cover 30%-40% of SME consulting spend stimulate a vibrant mid-market pipeline, bolstering the Belgium management consulting services market in the north.

Brussels-Capital commands a premium segment anchored in EU-policy advisory, public-sector transformation, and multinational headquarters engagements. Proximity to EU institutions compresses competition into a small geographic footprint with office rents that exceed the national average by more than 40%. Hybrid working norms ease space constraints yet do little to relieve the scarcity of senior multilingual consultants, keeping fee rates elevated and contributing outsized profitability to the Belgium management consulting services market.

Wallonia, though smaller in absolute terms, records above-average growth as generous Chèque Entreprise subsidies reimburse up to 90% of consultancy costs. AI adoption grants and the WalHub digital-services platform draw consulting spend into data integration, eGovernment design, and SME upskilling. Improving economic conditions and EU structural funds further reinforce Wallonia’s contribution to the Belgium management consulting services industry, helping to balance the regional revenue mix.

Competitive Landscape

The Big Four collectively hold an estimated 35%-40% share, anchoring a moderately concentrated market. Deloitte’s EMEA consolidation and EUR 1.5 billion (USD 1.69 billion) technology investment strengthen cross-border delivery credentials, while PwC’s Microsoft partnership exemplifies the pivot to platform-based advisory. Strategy boutiques such as McKinsey, BCG, and Bain focus on high-margin C-suite transformations, leveraging Brussels-based EU hubs to win policy mandates. Mid-tier European firms differentiate through sector-specific R&D and proprietary IP, targeting niches in circular economy, Industry 4.0, and low-carbon transitions.

Digital-native consultancies, notably Capgemini Invent, Cognizant, and Accenture, exploit offshore leverage and AI accelerators to compete on speed and cost. Capgemini’s sovereign-AI alliance with Google Cloud secures a first-mover edge in regulated sectors that require air-gapped environments. Niche disruptors such as KiTalent apply AI-driven talent platforms to compress executive-search lead times, potentially disintermediating traditional recruitment channels.

Rising compliance costs related to algorithmic pricing, sustainability cooperation, and no-poach rules elevate the relevance of competition-law advisory, favoring firms with dedicated antitrust practices. Overall, the Belgium management consulting services market retains healthy profitability, yet competitive dynamics shift toward technology enablement, specialized talent, and regional subsidy alignment.

Belgium Management Consulting Services Industry Leaders

Deloitte Belgium CVBA/SCRL

Accenture NV/SA

McKinsey and Company Belgium BV

PwC Business Advisory Services BV

Boston Consulting Group SPRL/BVBA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Deloitte launched a unified EMEA firm structure, backed by a EUR 1.5 billion (USD 1.69 billion) investment aimed at scaling AI-enabled service platforms and streamlining cross-border delivery.

- February 2026: Capgemini and Google Cloud expanded their partnership to offer secure sovereign cloud and AI solutions, establishing a dedicated Center of Excellence in Belgium.

- February 2026: Bain and Company appointed Cédric Bovy as Benelux Managing Partner, signaling a strategic focus on Brussels-based EU policy consulting growth.

- November 2025: Capgemini deepened its SAP partnership to provide sovereign technology offerings for highly regulated industries across Europe.

Belgium Management Consulting Services Market Report Scope

The Belgium Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current Belgium management consulting services market size and how fast is it growing?

The market stood at USD 3.32 billion in 2025, is valued at USD 3.47 billion in 2026, and is projected to reach USD 4.29 billion by 2031, reflecting a 4.33% CAGR over 2026-2031.

Which service line is the largest revenue contributor?

Digital Transformation Consulting held 26.47% of 2025 revenue, driven by cloud migration, data modernization, and AI-enabled process redesign.

How do regional subsidies influence consulting demand among Belgian SMEs?

Grant schemes in Brussels-Capital, Flanders, and Wallonia reimburse 25%-90% of consulting fees, lowering price barriers and fueling a 4.41% CAGR in the SME segment.

What factors are driving demand for sustainability consulting services?

Mandatory CSRD disclosures, phased assurance requirements, and the need for ESG data-management systems are generating multi-year advisory engagements across sectors.

Why is hybrid consulting gaining traction in Belgium?

Clients favor cost efficiency and talent flexibility, prompting a 4.87% CAGR for hybrid delivery models that blend on-site workshops with remote execution.

Which end-user industry is expected to grow fastest through 2031?

Healthcare is forecast to expand at a 4.76% CAGR as the national eHealth Action Plan funds data-capability and interoperability projects.

Page last updated on: