Indonesia Digital Advertising Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

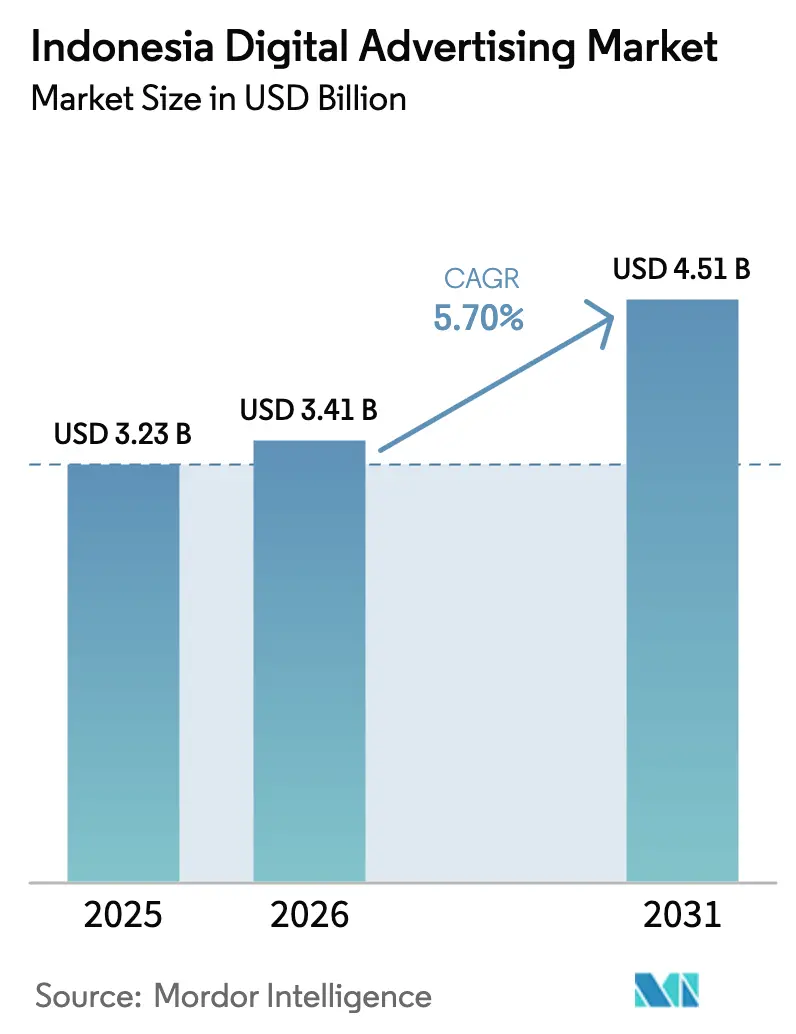

| Base Year Market Size (2025) | USD 3.23 Billion |

| Market Size (2026) | USD 3.41 Billion |

| Market Size (2031) | USD 4.51 Billion |

| Growth Rate (2026 - 2031) | 5.70% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Digital Advertising Market Analysis by Mordor Intelligence

The Indonesia digital advertising market size is expected to grow from USD 3.23 billion in 2025 to USD 3.41 billion in 2026 and is forecast to reach USD 4.51 billion by 2031 at 5.70% CAGR over 2026-2031. Rising broadband smartphone adoption, social-commerce integration, and video-first consumption patterns continue to redefine media budgets, while performance-oriented models gain traction as brands demand measurable outcomes. Intensifying consolidation talks among super-apps, sovereign AI investments that localize creative at scale, and stricter data-privacy enforcement collectively reshape platform economics and competitive tactics. Meanwhile, connected-TV expansion and live-commerce monetization unlock fresh inventory, encouraging omnichannel strategies that link awareness to conversion across devices. In parallel, higher brand-safety standards and contextual verification tools protect reputation without eroding reach.

Key Report Takeaways

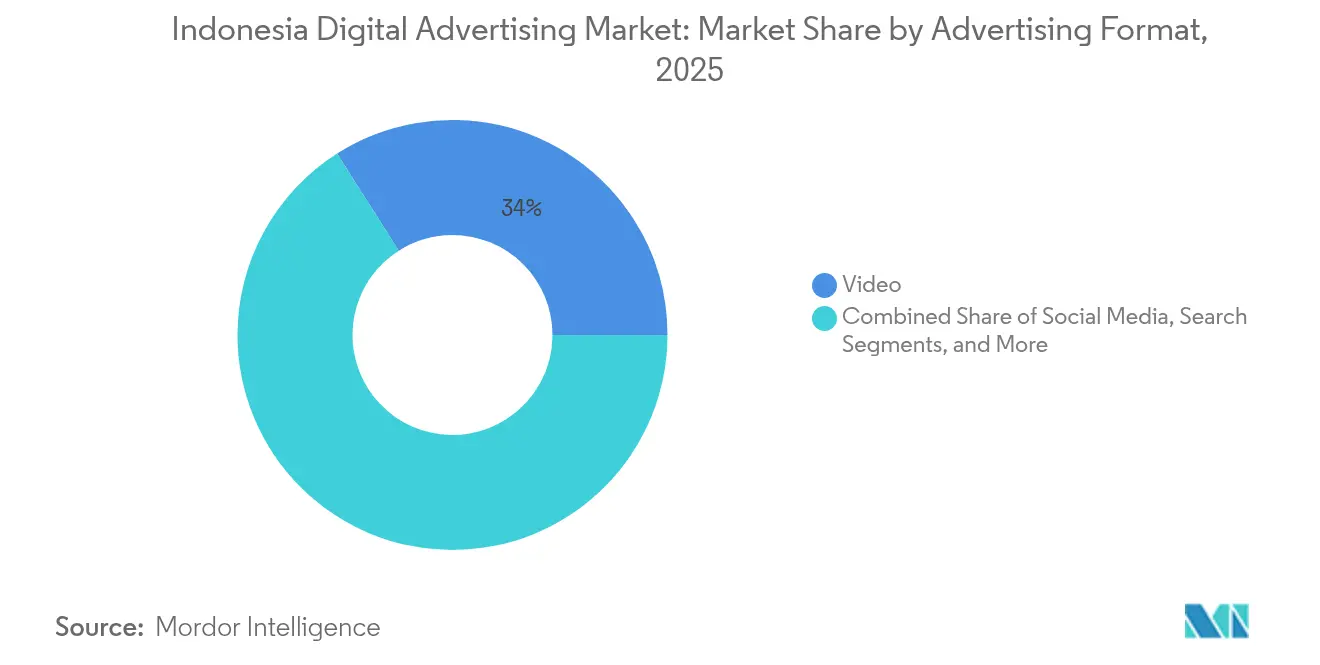

- By advertising format, video led with 34.02% revenue share of the Indonesia digital advertising market in 2025, and social media is projected to expand at a 6.11% CAGR through 2031, the fastest pace across formats.

- By device, mobile handsets held 68.10% of the Indonesia digital advertising market share in 2025, while connected TV is advancing at a 6.72% CAGR to 2031.

- By industry vertical, e-commerce commanded 22.20% share of the Indonesia digital advertising market size in 2025; healthcare and pharma is poised to grow at a 5.86% CAGR between 2026-2031.

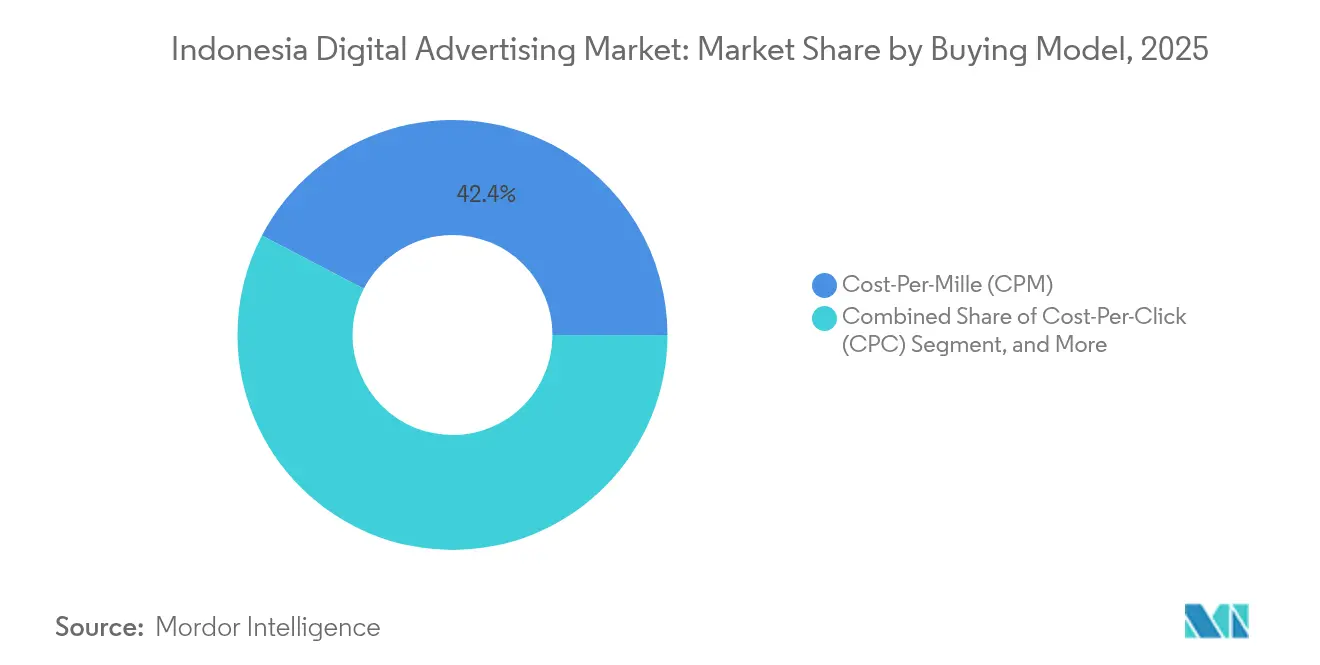

- By buying model, CPM accounted for 42.35% of spend in 2025; CPA is forecast to post a 6.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Digital Advertising Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone penetration and mobile internet boom | +1.2% | National, concentrated in Java and urban centers | Short term (≤ 2 years) |

| Budget shift from traditional to digital media | +0.9% | National, led by Jakarta and major cities | Medium term (2-4 years) |

| E-commerce and social-commerce surge | +1.4% | National, expanding to tier-2/3 cities | Medium term (2-4 years) |

| OTT / short-form video consumption spike | +0.8% | National, youth-concentrated in urban areas | Short term (≤ 2 years) |

| Govt "Making Indonesia 4.0" SME digitization incentives | +0.6% | National, rural and MSME-focused | Long term (≥ 4 years) |

| AI-driven hyper-local targeting via ride-hailing and POS data | +0.5% | Urban centers, expanding via Gojek/Grab networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smartphone penetration and mobile internet boom

Indonesia’s mobile-first transition accelerates advertising-budget shifts as smartphone ownership is forecast to climb from 86% in 2025 to 91.3% by 2028. Daily app usage now exceeds 5 hours, and 4G coverage blankets 96.48% of populated areas, enabling reliable programmatic reach even in peri-urban zones.[1]Directorate General of PPI, “Data Penyelenggaraan Pos dan Informatika 2023,” djppi.kominfo.go.id Operator concentration around Telkomsel, Indosat, and XL Axiata provides scaled inventory and deterministic audience data, while Telkomsel’s TADEX platform packages premium impressions across thousands of publishers. Rising mobile traffic, up 17.99% YoY in 2024, ensures that the Indonesia digital advertising market remains anchored to handheld screens for the foreseeable future.

Budget shift from traditional to digital media

Marketers allocate progressively larger shares of total spend online as linear-TV ratings wane and OOH fragmentation dilutes impact. National advertisers moved 7 percentage-points of budget from analog to digital between 2023-2025, spurred by compelling ROI evidence and granular targeting unavailable on legacy channels. The shift is led by Jakarta-based multinationals, yet regional brands quickly replicate best practices through performance-marketing workshops. The Indonesia digital advertising market consequently benefits from multi-format experimentation, with dynamic creative optimization and sequential-storytelling campaigns replacing static mass-reach placements.

E-commerce and social-commerce surge

Live-commerce adoption now reaches 60% of shoppers, and TikTok Shop’s GMV quadrupled to USD 16.3 billion in 2023, igniting merchant demand for shoppable ads and one-click checkout journeys. The TikTok–Tokopedia tie-up controls 39% of gross merchandise value, nearly matching Shopee’s dominance, intensifying bidding wars for sponsored listings. Attribution models that track creator-led conversions across walled gardens lower acquisition costs, thus sustaining the Indonesia digital advertising market’s rapid expansion into tier-2 and tier-3 cities where traditional retail options remain limited.

OTT / short-form video consumption spike

Indonesia hosts millions of OTT viewers who stream billion hours monthly, a signficiant rise, and half are willing to watch four or more ads hourly. Brand-recall for CTV spots improved signficiantly in 2024, encouraging FMCG and automotive advertisers to reallocate linear-TV money. Youth-centric demand for Korean dramas and short-form comedic clips drives higher-than-average completion rates, allowing frequency capping without sacrificing engagement. Consequently, connected-TV spend represents the fastest-growing slice of the Indonesia digital advertising market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ad-fraud and brand-safety concerns | -0.7% | National, concentrated in programmatic channels | Short term (≤ 2 years) |

| Measurement and attribution fragmentation | -0.5% | National, affecting cross-platform campaigns | Medium term (2-4 years) |

| Personal-Data Protection Law (PDP) compliance burden | -0.9% | National, affecting all data processors | Medium term (2-4 years) |

| Uneven broadband outside tier-1 cities | -0.6% | Eastern Indonesia and rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ad-fraud and brand-safety concerns

Election-year misinformation surged, with most of consumers perceiving fake news as severe. Brands thus tighten controls, opting for verification partners that classify content at page level rather than blunt keyword blocks. Demand for impression-level transparency grows, yet fragmented publisher quality and livestream complexity raise monitoring costs. Until verification standards mature, pockets of the Indonesia digital advertising market may face supply-side pricing pressure.

Personal-Data Protection Law compliance burden

Full enforcement of the PDP Law since October 2024 mandates Data-Protection Officers and caps fines at a rate of revenue, compelling ad-tech players to rearchitect consent flows and cross-border data transfers. Smaller publishers struggle with compliance overhead, nudging them toward consolidation or managed-service partnerships. While stricter governance elevates user trust, it also constrains behavioral-targeting scale, marginally slowing Indonesia digital advertising market growth during the transition period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Advertising Format: Video dominance meets social acceleration

Video ads represented 34.02% of spend in 2025, capturing the largest slice of the Indonesia digital advertising market size as OTT viewership soared beyond 3.5 billion monthly hours. High completion rates and improved measurement tools attracted FMCG, automotive, and telco budgets, while six-second bumper ads safeguarded user experience on constrained bandwidth connections. Social media, however, is poised for the quickest ascent at a 6.11% CAGR, buoyed by TikTok’s 157.6 million users and frictionless commerce checkout journeys forged after its Tokopedia merger. Even with stricter social-commerce rules, branded-content labeling and first-party data access underpin performance consistency, ensuring continued share gains.

Display and banner formats evolve with responsive designs optimized for vertical video feeds, whereas search remains indispensable for high-intent conversions, especially within travel and financial-services categories. Audio ads benefit from a weekly podcast reach of 42.6%, providing brand-safe storytelling environments. Native integrations and email nurture flows add complementary frequency touches. Collectively, these dynamics keep the Indonesia digital advertising market expanding as advertisers diversify creative to match nuanced consumer moments.

By Device: Mobile supremacy with connected TV emergence

Mobile handsets absorbed 68.10% of expenditure in 2025, underlining the Indonesia digital advertising market share leadership of smartphones in a country where SIM penetration exceeds population and 67% of e-commerce checkouts occur on handhelds. Lightweight SDKs that compress creatives for low-bandwidth regions drive incremental reach without compromising latency. Simultaneously, connected-TV spending is forecast to grow at 6.72% CAGR, turning living-room screens into addressable inventory. Subscription-video households surpass pay-TV, enabling dynamic ad insertion and household-level frequency capping, a boon for brand-lift studies that previously relied on panel-based measurement.

Desktop campaigns persist for B2B intent harvesting and long-form research journeys, while tablets furnish incremental impressions across education and children’s content. Next-generation 5G rollouts across Surabaya and Medan further reduce buffering, allowing interactive shoppable ads that merge QR codes with broadcast visuals. Fiber-to-home coverage reaching 97.86% of districts cushions peak-time quality. These infrastructure upgrades reinforce omni-device planning as the Indonesia digital advertising market matures.

By Industry Vertical: E-commerce leadership with healthcare acceleration

E-commerce platforms controlled 22.20% of vertical spend in 2025, riding Indonesia’s retail digitization wave that is projected to lift GMV to USD 95.84 billion by 2029. Conversion-optimized placements such as sponsored product listings and dynamic retargeting dominate tactical mixes. Emerging sellers in tier-3 cities leverage low-cost creator partnerships to sidestep congested keywords, preserving ROAS. Healthcare and pharma, while currently smaller, will expand fastest at a 5.86% CAGR as telemedicine normalizes post-pandemic and older demographics seek convenient prescription refills.

FMCG brands sustain hefty reach campaigns, but sophisticated data-clean rooms with GoTo and Shopee now power incrementality tests. Fintech promotion escalates in tandem with digital-banking transactions growing 23.2% in 2024, whereas media-and-entertainment players promote local productions via programmatic video bursts. Electric-vehicle makers and ed-tech providers round out a diverse advertiser base that broadens the Indonesia digital advertising market size over the forecast period.

By Buying Model: CPM dominance with CPA performance growth

Cost-per-mille captured 42.35% of bookings in 2025 as brands prioritized awareness to feed the upper funnel of the Indonesia digital advertising market. Nonetheless, CPA contracts will swell at a 6.29% CAGR as attribution windows tighten and BI-FAST real-time payments enable instant post-click validation. Retail-media networks refine first-party datasets, letting merchants bid on bottom-funnel placements with guaranteed return thresholds. CPC continues to underpin search and social, whereas CPV thrives on skippable video ads that balance reach with attention. Hybrid algorithms now auto-pivot between goals, driven by machine-learning models that ingest conversion probabilities to optimize bidding in flight, further professionalizing the Indonesia digital advertising industry.

Geography Analysis

Java’s dense infrastructure, 52.5+ Digital Society Index scores, and elevated disposable incomes make Jakarta and its satellite cities the epicenter of campaign launches, accounting for well over half of the Indonesia digital advertising market size. Advertisers exploit granular neighborhood data to calibrate geo-fenced offers, while bilingual creatives toggle between Indonesian and informal Jakartan vernacular depending on context. Competitive clutter pushes CPMs 15-20% higher than the national mean, yet higher lifetime values justify the premium.

Sumatra and Kalimantan witness rising investment as logistics corridors improve and mining, agriculture, and tourism sectors digitize sales funnels. Social-commerce influencers from Medan and Palembang now drive notable traffic spikes during payday periods, highlighting the Indonesia digital advertising market’s expanding geographic diversity. Government fiber rollouts along the Trans-Sumatra highway and forthcoming 5G licenses unlock HD-video inventory previously hampered by buffering complaints. Rural markets present substantial growth opportunities, with 42% of Indonesia's 285 million population residing outside urban centers and platforms like Dagangan targeting 88,000 stores across 25,000 villages for FMCG advertising.

Eastern provinces remain under-penetrated; Papua, for instance, achieves significant rate of 4G coverage, but targeted government subsidies and universal-service obligations are scheduled to raise connectivity. Retail start-ups like Dagangan partner with village stores, facilitating brand promotions in vernacular languages across 700+ dialects. As cultural nuance becomes paramount, localized AI-generated voice-overs reduce production costs while maintaining authenticity, allowing national brands to secure footholds in low-competition territories and extend the Indonesia digital advertising market footprint.

Competitive Landscape

Global platforms continue to dominate: Google’s search and YouTube assets command unrivaled intent and reach, Meta’s family of apps underpins social feed advertising, and ByteDance accelerates monetization through commerce integrations. Collectively, these three players generated an estimated 58% share of the Indonesia digital advertising market in 2024, indicating moderate concentration. Yet local giants GoTo and Telkomsel are closing gaps via proprietary first-party data, sovereign AI initiatives, and exclusive inventory deals that resonate with cultural preferences.

Rumored Grab–GoTo merger talks, valued at USD 7 billion, threaten to reshape ride-hail and food-delivery media buying, potentially pooling MAU datasets that rival global walled gardens. Telkomsel’s TADEX exchange aggregates premier publishers, offering transparency sought by brand advertisers wary of obscure SSP fee structures. Gojek’s IoT-enabled GoScreen adds measurable OOH impressions, while Superbank’s in-app financial tools unlock closed-loop attribution for cost-conscious consumer-goods firms.

Agency ecosystems adapt: Moonfolks (ex-M&C Saatchi) prioritizes “accelerated commerce,” leveraging AI-generated multilingual assets to cut turnaround times. Meanwhile, holding-company networks invest in data-clean rooms and contextual intelligence to navigate PDP-law restrictions. Consolidation pressures mount for smaller DSPs unable to fund compliance upgrades, suggesting that the Indonesia digital advertising industry will witness further M&A as scale becomes prerequisite for sustainable margins.

Indonesia Digital Advertising Industry Leaders

PT Google Indonesia (Alphabet Inc.)

Meta Platforms Inc.

ByteDance Ltd. (TikTok Indonesia)

PT Emtek Digital

PT RedComm Indonesia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GoTo Group reported record 2024 results with 92% advertising-revenue growth and positive adjusted EBITDA of IDR 386 billion, while CEO Patrick Walujo secured contract extension through 2029 with performance-based incentives.

- February 2025: Grab advanced talks to acquire GoTo in a potential USD 7 billion deal, hiring advisers and arranging bridge financing up to USD 2 billion.

- January 2025: Indonesia drafted national AI regulation, with Communications Minister Meutya Hafid targeting completion within three months following stakeholder consultations.

- October 2025: The Personal Data Protection Law took full effect, mandating Data-Protection Officer appointments and introducing revenue-based fines for non-compliance.

Indonesia Digital Advertising Market Report Scope

Digital advertising is marketing through online channels, including websites, streaming content, spanning media formats such as text, image, audio, and video. Digital advertising enables users to achieve business goals ranging from brand awareness and customer engagement to launching new products and driving sales.

The Indonesian digital advertising market is segmented by type (audio advertising, video advertising, influencer advertising, banner advertising, search advertising, and classifieds), platform (desktop and mobile), and industry (FMCG, telecom, healthcare, media and entertainment, and others). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Display/Banner |

| Video |

| Social Media |

| Search |

| Audio/Podcast |

| Native |

| Mobile Handset |

| Desktop / Laptop |

| Connected TV |

| Tablet and Others |

| FMCG |

| Telecom |

| Healthcare and Pharma |

| Media and Entertainment |

| Financial Services |

| Travel and Tourism |

| E-commerce and Marketplaces |

| Others Industry Verticals |

| Cost-Per-Click (CPC) |

| Cost-Per-Mille (CPM) |

| Cost-Per-Acquisition (CPA) |

| Cost-Per-View (CPV) |

| Hybrid / Other Buying Models |

| By Advertising Format | Display/Banner |

| Video | |

| Social Media | |

| Search | |

| Audio/Podcast | |

| Native | |

| By Device | Mobile Handset |

| Desktop / Laptop | |

| Connected TV | |

| Tablet and Others | |

| By Industry Vertical | FMCG |

| Telecom | |

| Healthcare and Pharma | |

| Media and Entertainment | |

| Financial Services | |

| Travel and Tourism | |

| E-commerce and Marketplaces | |

| Others Industry Verticals | |

| By Buying Model | Cost-Per-Click (CPC) |

| Cost-Per-Mille (CPM) | |

| Cost-Per-Acquisition (CPA) | |

| Cost-Per-View (CPV) | |

| Hybrid / Other Buying Models |

Key Questions Answered in the Report

What is the current valuation of the Indonesia digital advertising market?

It is valued at USD 3.41 billion in 2026 and projected to reach USD 4.51 billion by 2031.

Which advertising format attracts the most spending?

Video commands the largest share at 34.02% of 2025 spend, followed by social media.

Why is connected-TV advertising growing so quickly in Indonesia?

OTT viewership hit 83 million users streaming 3.5 billion hours monthly, raising advertiser demand for household-level, non-skippable inventory.

How does the Personal Data Protection Law affect advertisers?

The law imposes revenue-based fines and mandates Data-Protection Officers, pushing platforms to strengthen consent flows and first-party data strategies.

Which vertical is expected to be the fastest-growing through 2031?

Healthcare and pharma advertising is forecast to expand at a 5.86% CAGR, driven by telemedicine uptake and rising health awareness.

Page last updated on: