Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

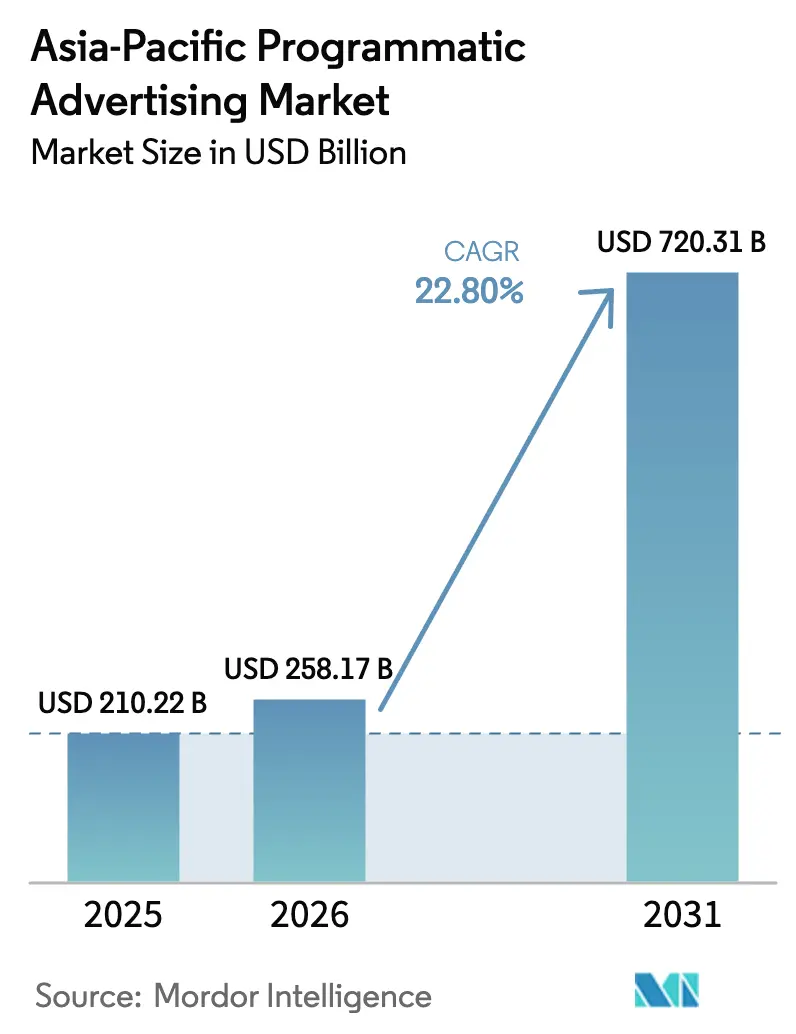

| Base Year Market Size (2025) | USD 210.22 Billion |

| Market Size (2026) | USD 258.17 Billion |

| Market Size (2031) | USD 720.31 Billion |

| Growth Rate (2026 - 2031) | 22.80% CAGR |

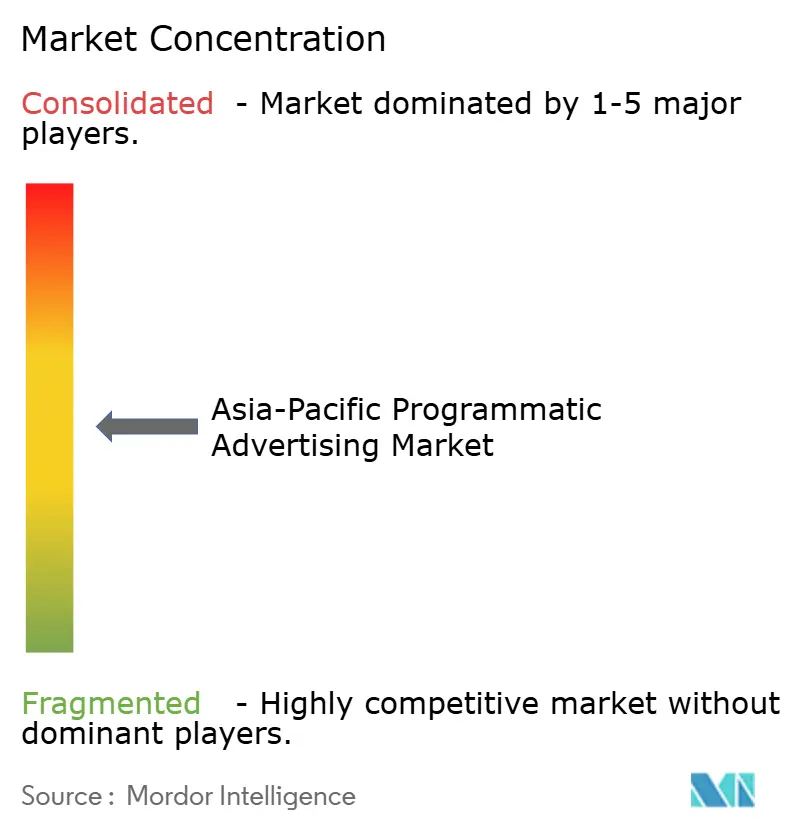

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Programmatic Advertising Market Analysis by Mordor Intelligence

The Asia-Pacific programmatic advertising market size is expected to grow from USD 210.22 billion in 2025 to USD 258.17 billion in 2026 and is forecast to reach USD 720.31 billion by 2031 at 22.8% CAGR over 2026-2031. Current growth is fueled by rapid mobile adoption, 5G roll-outs, and the measurable returns that programmatic delivers over traditional media.[1]Digital Turbine Investor Relations, “Mobile Growth Press Releases,” digitalturbine.com Advertisers are reallocating budgets toward automated buying models that blend auction efficiency with inventory certainty, while publishers monetize new formats such as connected TV (CTV) and programmatic digital out-of-home (pDOOH). Government digital-economy agendas, especially in China, India, and South Korea, are expanding premium ad supply, and AI-driven optimization is helping brands manage language and cultural diversity at scale. Competitive intensity is rising as regional specialists use vernacular data and contextual algorithms to close performance gaps left by global platforms. Sustainability metrics, notably carbon-emission dashboards embedded in ad platforms, are emerging as a differentiator for responsible brand spending.[2]LoopMe, “LoopMe Partners with Cedara,” loopme.com

Key Report Takeaways

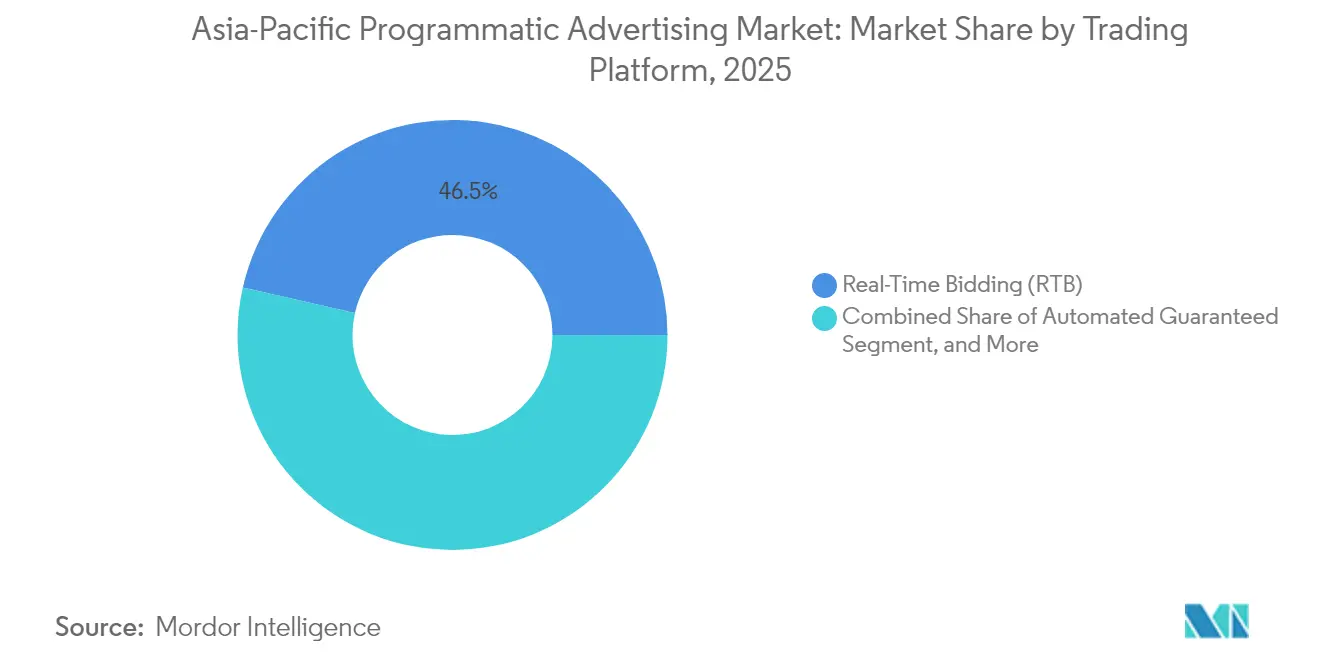

- By trading platform, Real-Time Bidding led with a 46.45% revenue share of the Asia-Pacific programmatic advertising market in 2025; Automated Guaranteed is projected to expand at a 24.06% CAGR through 2031.

- By advertising media, Mobile Display captured 49.10% of the Asia-Pacific programmatic advertising market share in 2025, while Connected TV/OTT is forecast to surge at a 24.5% CAGR to 2031.

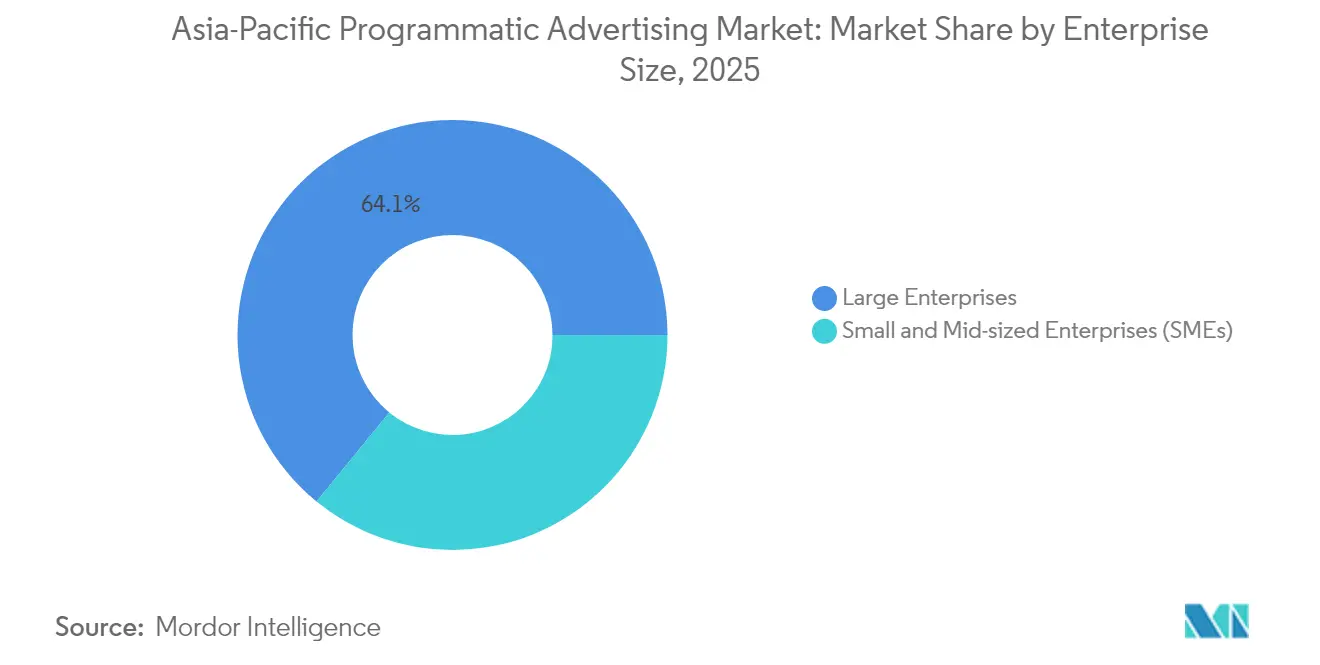

- By enterprise size, Large Enterprises accounted for 64.10% of the Asia-Pacific programmatic advertising market size in 2025, and Small and Mid-sized Enterprises are growing at a 23.57% CAGR through 2031.

- By industry vertical, E-commerce and Retail commanded 29.70% of spending of the Asia-Pacific programmatic advertising market in 2025; Travel and Hospitality is advancing at a 24.7% CAGR through 2031.

- By geography, China held a 42.05% share of the Asia-Pacific programmatic advertising market size in 2025, whereas India is forecast to expand at a 24.6% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Programmatic Advertising Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift of Asia Pacific ad budgets from traditional to digital channels | +6.2% | Global Asia-Pacific, strongest in China and India | Medium term (2-4 years) |

| Mobile-first user base fuelling in-app inventory growth | +5.8% | Southeast Asia core, spill-over to broader Asia-Pacific | Short term (≤ 2 years) |

| Government-led 5G roll-outs expanding high-quality ad slots | +4.1% | China, South Korea, Japan, expanding to India and Southeast Asia | Long term (≥ 4 years) |

| Rising adoption of AI/ML for real-time campaign optimisation | +3.9% | Technology hubs: Singapore, Hong Kong, Tokyo, expanding regionally | Medium term (2-4 years) |

| Brand-safety algorithms tailored for Asian languages and cultures | +2.1% | Multi-language markets: India, Southeast Asia, China | Medium term (2-4 years) |

| Emergence of programmatic digital out-of-home networks in tier-2 Asian cities | +1.4% | Tier-2 cities across China, India, Indonesia, Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid shift of ad budgets to digital channels

Digital media captured a larger share of advertising spend across Asia-Pacific in 2025 as brands pursued measurable, audience-level outcomes that traditional media struggled to deliver.[3]Dentsu Global, “Digital Advertising Growth Trends in Asia-Pacific,” dentsu.com Programmatic platforms benefited as marketers adopted attribution tools that optimize cross-channel journeys in real time. Markets with historically limited linear TV reach, such as Indonesia and Vietnam, leapfrogged directly into mobile-led programmatic models. Regulators reinforced the shift by mandating transparency and data-access standards that favor automated trading. As a result, programmatic now attracts even brand-building budgets that once defaulted to television, widening the addressable pool of spend.

Mobile-first ecosystem fuels in-app inventory

Mobile devices generate more impressions than desktops across every major APAC market, making in-app ad space the prime real estate for the Asia-Pacific programmatic advertising market. Higher engagement rates and richer behavioral data raise bid density and effective CPMs. Partnerships such as AnyMind Group with InMobi yielded 4.3× year-over-year revenue gains for publishers by automating mediation across demand sources. Advertisers are layering geo-location and app-usage signals to serve real-time offers near stores, while publishers roll out rewarded video and playable formats that drive completion rates above 90%. The depth of mobile data also supports privacy-compliant look-alike modeling that compensates for cookie deprecation on browsers.

AI and machine learning transform optimization

Sophisticated AI models now analyze user intent, lifetime value, and contextual cues in milliseconds, improving bid accuracy and creative relevance. Appier embedded generative AI features after acquiring AdCreative.ai, enabling dynamic asset iteration tailored to local languages and cultural references. These models predict conversion likelihood and throttle spend to the highest-value audiences, shrinking waste and raising return on ad spend. AI also automates fraud filtering and brand-safety enforcement, critical for campaigns spanning thousands of small publishers across multiple scripts. Early adopters report double-digit lift in conversion rates and cost-per-action reductions, reinforcing AI as a default capability for platforms serving the Asia-Pacific programmatic advertising market.

Government 5G roll-outs create premium inventory

Governments in China, South Korea, and Japan have accelerated 5G deployment, unlocking high-bandwidth ad formats such as interactive video and AR overlays that command premium pricing. Faster networks lower latency in real-time bidding and improve verification pings, reducing discrepancies. They also enhance GPS accuracy, enabling hyper-local retail activations. In emerging markets, planned 5G expansions promise to leapfrog fixed-line limitations, widening rural audience reach for programmatic campaigns. Publishers expect 5G video to raise completion rates, while advertisers can deploy immersive storytelling without buffering risks, strengthening brand affinity, and justifying higher CPMs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented data privacy regulations across the Asia-Pacific markets | -3.2% | Regional fragmentation, strongest impact in China, India, Singapore | Medium term (2-4 years) |

| Shortage of skilled programmatic talent outside top metro areas | -2.1% | Tier-2 and tier-3 cities across Asia-Pacific, rural markets | Long term (≥ 4 years) |

| Browser and OEM-level restrictions on device IDs in China and India | -1.8% | China and India primarily, potential expansion to other markets | Short term (≤ 2 years) |

| Limited premium local inventory for vernacular content in South-East Asia | -1.3% | Southeast Asia, particularly Indonesia, Thailand, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented privacy regulations add compliance cost

Divergent data-protection laws force platforms to maintain market-specific consent flows, data shores, and reporting templates, inflating overheads and delaying campaign launches. Larger vendors absorb the burden through dedicated legal teams, while smaller players risk fines or exit less-profitable markets. Cross-border campaigns must often partition user data, reducing scale advantages. Advertisers, wary of penalties, favor partners with audited compliance credentials, concentrating spend and potentially limiting innovation from startups.

Talent shortage outside top metros hampers scaling

Expertise in demand-side platforms, data analysis, and advanced creative optimization remains scarce beyond major hubs like Singapore, Tokyo, and Mumbai. This gap slows adoption among local brands in fast-growing secondary cities despite rising digital budgets. Agencies struggle to recruit certified traders, and turnover remains high as specialists migrate to higher-paying regional roles. E-learning programs and vendor academies are expanding, but skill pipelines will take several years to meet demand, tempering growth in underserved markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Trading Platform: Advertisers balance certainty with auction efficiency

Real-Time Bidding represents the largest slice of the Asia-Pacific programmatic advertising market at 46.45% revenue share in 2025, reflecting its flexibility and dynamic pricing benefits. The segment’s scale stems from open exchange liquidity and sophisticated bid-shading tools that minimize overpayment. However, inventory quality concerns and brand-safety requirements have led premium advertisers to commit budgets through Automated Guaranteed, which is growing at a 24.06% CAGR. The Asia-Pacific programmatic advertising market share for Automated Guaranteed is rising as publishers package high-visibility placements with fixed rates, ensuring predictable delivery during peak events. Private Marketplace Guaranteed straddles both models, letting buyers access curated impressions with preferential terms, while Unreserved Fixed-Rate remains a niche option for campaigns prioritizing rate stability over reach.

Hybrid buying strategies are emerging: brands start with a guaranteed block to secure prime slots, then chase incremental reach via RTB as frequency caps are met. Platform integrations, such as X deploying Magnite to monetize remnant social inventory, illustrate how publishers blend direct and auction channels to maximize yield. The outcome is a trading landscape where buyers flex between certainty and efficiency, broadening revenue streams across platform types.

By Advertising Media: CTV and pDOOH supplement mobile dominance

Mobile Display holds 49.10% of the Asia-Pacific programmatic advertising market size due to smartphone ubiquity and superior engagement metrics. Deep in-app data and first-party identifiers reinforce mobile’s targeting edge, while rewarded and playable ads drive performance for gaming and commerce apps. Connected TV/OTT, though smaller today, is scaling at a 24.5% CAGR as viewers migrate from linear TV to streaming. Programmatic pipes now plug into local broadcasters and over-the-top services, letting brands execute audience buys across large-screen environments once reserved for upfront deals. Digital Display on desktop maintains pockets of influence in office-centric segments, whereas pDOOH is reinventing outdoor with dynamic scheduling tied to audience movement patterns.

Samsung’s healthcare pDOOH campaign with Hivestack synchronized mobile retargeting, showcasing omnichannel storytelling that boosts recall and lifts foot traffic. As broadband penetration widens, CTV ad loads rise, and household co-viewing provides incremental reach. Advertisers, therefore, allocate budgets across screens, reinforcing omnichannel measurement tools that stitch exposures into unified frequency caps.

By Enterprise Size: Self-service unlocks SME growth

Large enterprises commanded 64.10% of 2025 spend, leveraging cross-market data lakes and private marketplaces for scale. Yet SMEs are the fastest-growing customer cohort, expanding at 23.57% annually as intuitive dashboards remove technical barriers. Retail-media networks embed programmatic modules into merchant portals, letting small sellers extend on-site promotions to off-site inventory with a few clicks. For instance, PubMatic’s Tokopedia link enables Indonesian merchants to target high-intent audiences beyond the marketplace. The Asia-Pacific programmatic advertising market size generated by SMEs is set to climb as minimum IOs drop and AI-guided setup templates suggest bid ceilings, creatives, and audiences.

Vendor roadmaps prioritize simplified UX, one-click pixel integration, and automatic conversion optimization to cater to resource-constrained businesses. As SMEs gain confidence, many progress from lower-funnel retargeting to upper-funnel brand building, diversifying spend across video, CTV, and pDOOH.

By Industry Vertical: Travel rebounds, retail sustains leadership

E-commerce and Retail accounted for 29.70% of 2025 spend, driven by always-on customer acquisition, cart-abandon retargeting, and loyalty upsells. On-platform ads deliver closed-loop attribution, making budgets highly defensible. Travel and Hospitality is the breakout vertical, posting a 24.7% CAGR as borders reopened and consumers resumed booking trips. Airlines and tourism boards deploy dynamic deals based on seat inventory and search trends, capitalizing on programmatic’s speed. BFSI maintains steady investment in data-driven acquisition for credit-card and loan products, while Automotive pivots to lead generation for electric-vehicle launches. Healthcare, education, and tech round out the “other” category, each gradually increasing programmatic mix as compliance frameworks mature.

Retailers themselves are doubling as media owners: Southeast Asia’s retail-media revenues are projected at USD 4.7 billion by 2030, with Indonesia growing 219% as marketplaces monetize first-party shopper data. This convergence of advertiser and publisher roles reshapes buying models and expands programmatic inventory pools.

Geography Analysis

China contributed 42.05% of the Asia-Pacific programmatic advertising market in 2025, thanks to super-apps that unify social, payments, and commerce. China remains the largest contributor to the Asia-Pacific programmatic advertising market size, yet its pace is settling as Personal Information Protection Law compliance raises operating thresholds. Super-app ecosystems still deliver unrivaled reach and data richness, particularly in commerce-linked ad units, and tier-2 cities add incremental inventory as 5G and pDOOH footprints expand. Foreign platforms continue to face entry barriers, but domestic rivals compete vigorously on AI features and carbon-reporting add-ons, ensuring ongoing innovation.

Affordable data plans underpin India’s 24.6% CAGR through 2031, UPI payment ubiquity, and government digital-service portals that onboard new internet users daily. India is the fastest-growing geography, propelled by surging smartphone adoption, nationwide digital-infrastructure projects, and a maturing data-privacy law that clarifies compliance expectations. Vernacular content formats thrive, and programmatic engines segment audiences across more than 20 official languages. Rural penetration gains, coupled with low-cost Android devices, bring newcomers online, enlarging impression pools. Local DSPs with language-aware categorization challenge global incumbents, and the government’s Open Network for Digital Commerce hints at future first-party data opportunities for advertisers.

Japan, South Korea, and Australia offer advanced but saturated environments where value creation depends on sophisticated measurement, CTV expansion, and cross-device frequency controls. These markets pioneer privacy-safe identity frameworks that avoid cookies, setting templates for broader regional rollout. Southeast Asian countries Thailand, Singapore, and Malaysia show double-digit growth as broadband access widens and cross-border e-commerce rises. Regional players leverage cultural fluency to win brand budgets, while investment flows into local content studios to boost premium inventory. Fragmented regulations remain a hurdle for campaign orchestration across borders, necessitating modular compliance stacks within DSPs.

Competitive Landscape

The Asia-Pacific programmatic advertising market features mid-level concentration; top global exchanges, demand-side platforms, and ad-verification suites coexist with regional specialists tuned to local scripts and consumer behaviors. Market share leadership differs by country, creating a mosaic where one player rarely exceeds 25% share region-wide. Technology innovation, rather than inventory exclusivity, is the prime battleground: AI-native platforms tout cost-efficient user-acquisition models, while incumbents emphasize scaled identity graphs and brand-safety credentials.

Fragmentation is most evident in emerging markets, where language fragmentation and vernacular video surge. Companies such as SQREEM gain traction by offering cookie-less behavioral targeting aligned with local privacy rules. Meanwhile, environmental accountability grows; LoopMe’s integration of Cedara’s carbon dashboard positions it favorably with sustainability-focused advertisers. Competitive moves also highlight vertical integration. Digital Turbine embeds app-discovery ads at the device level, while PubMatic partners with marketplaces to broaden commerce signal access. Patent filings across AI bidding and privacy-preserving analytics point to fierce IP defense. Scale players leverage compliance investments to navigate multi-country laws, setting a high bar for smaller entrants and nudging the market toward gradual consolidation around identity-secure, multilingual platforms.

Local acquisitions continue: Catcha Digital’s stake in Digital Symphony boosts regional omnichannel reach, whereas FreakOut’s UUUM purchase bundles influencer marketing into programmatic offers. These tie-ups reflect advertiser demand for holistic solutions spanning social, video, and outdoor. Vendors that unify activation, measurement, and carbon tracking under one login are best placed to capture incremental budgets.

Asia-Pacific Programmatic Advertising Industry Leaders

Amazon.com LLC (Amazon Advertising)

Appier Inc.

Aarki, Inc.

Adform A/S

AnyMind Group Pte. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Digital Turbine partnered with Alcatel to embed on-device programmatic ads for Indian users, improving engagement and OEM monetization.

- April 2025: PubMatic and Tokopedia enabled Indonesian sellers to extend on-site ads across premium publishers via programmatic pipes.

- April 2025: LoopMe integrated Cedara’s carbon-intelligence layer, offering emission tracking for campaigns.

- March 2025: Catcha Digital bought 51% of Digital Symphony for RM 22.95 million (USD 5.1 million) to scale data-driven marketing in Malaysia.

- February 2025: X enlisted Magnite to monetize unsold social inventory through third-party exchanges.

Asia-Pacific Programmatic Advertising Market Report Scope

The traditional advertising model could be more efficient, as it needs the functionality to measure the Return on Investment (ROI). Programmatic advertising introduces an elaborate system that doesn't require human intervention and uses programming applications to complete this process and display ads across the internet. It is the real-time buying and selling of ad inventory through an automated bidding system. With a sophisticated infrastructure, programmatic advertising lets brands or agencies buy ad impressions on publisher websites. Various methods are involved in programmatic advertising, like display ads placed at the header, footer, sidebar, social Ads, audio ads, native ads, and more.

Asia-Pacific Programmatic Advertisement Market is segmented by trading platform (real-time bidding (RTB), private marketplace guaranteed, automated guaranteed, and unreserved fixed-rate), advertising media (digital display and mobile display), and enterprise size (SMBs and large enterprises). The market sizes and forecasts are provided regarding value (USD).

By Trading Platform

| Real-Time Bidding (RTB) |

| Private Marketplace Guaranteed |

| Automated Guaranteed |

| Unreserved Fixed-Rate |

By Advertising Media

| Digital Display (Web) |

| Mobile Display (In-App and Web) |

| Connected TV/OTT |

| Digital Out-of-Home |

By Enterprise Size

| Small and Mid-sized Enterprises (SMEs) |

| Large Enterprises |

By Industry Vertical

| E-commerce and Retail |

| Media and Entertainment |

| BFSI |

| Travel and Hospitality |

| Automotive |

| Other Industry Verticals |

By Country

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Thailand |

| Singapore |

| Malaysia |

| Rest of Asia-Pacific |

| By Trading Platform | Real-Time Bidding (RTB) |

| Private Marketplace Guaranteed | |

| Automated Guaranteed | |

| Unreserved Fixed-Rate | |

| By Advertising Media | Digital Display (Web) |

| Mobile Display (In-App and Web) | |

| Connected TV/OTT | |

| Digital Out-of-Home | |

| By Enterprise Size | Small and Mid-sized Enterprises (SMEs) |

| Large Enterprises | |

| By Industry Vertical | E-commerce and Retail |

| Media and Entertainment | |

| BFSI | |

| Travel and Hospitality | |

| Automotive | |

| Other Industry Verticals | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Thailand | |

| Singapore | |

| Malaysia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is spending on automated buying in the Asia-Pacific programmatic advertising market?

The Asia-Pacific programmatic advertising market size reached USD 258.17 billion in 2026 and is projected at USD 720.31 billion by 2031.

Which country is growing fastest for programmatic ad spend in Asia-Pacific?

India is forecast to expand at a 24.6% CAGR through 2031, driven by mobile adoption and digital-payment uptake.

What media channel leads programmatic budgets today?

Mobile Display commands 49.10% of spend because smartphones dominate internet access across the region.

Why are advertisers shifting to Automated Guaranteed deals?

Automated Guaranteed offers inventory certainty and brand-safe environments, prompting a 24.06% CAGR even as RTB remains dominant.

How is sustainability addressed in programmatic campaigns?

Vendors such as LoopMe integrate carbon-measurement dashboards so brands can track and reduce emissions tied to ad delivery.

What is the biggest restraint on cross-border programmatic campaigns in Asia-Pacific?

Fragmented data-privacy laws add compliance complexity and cost, reducing the ease of running unified regional campaigns.

Page last updated on: