Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Radio Advertising Market Report is Segmented by Type (Traditional Radio Advertising, Terrestrial Radio Broadcast Advertising, Terrestrial Radio Online Advertising, and Satellite Radio Advertising), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), and Geography (North America, Europe, South America, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

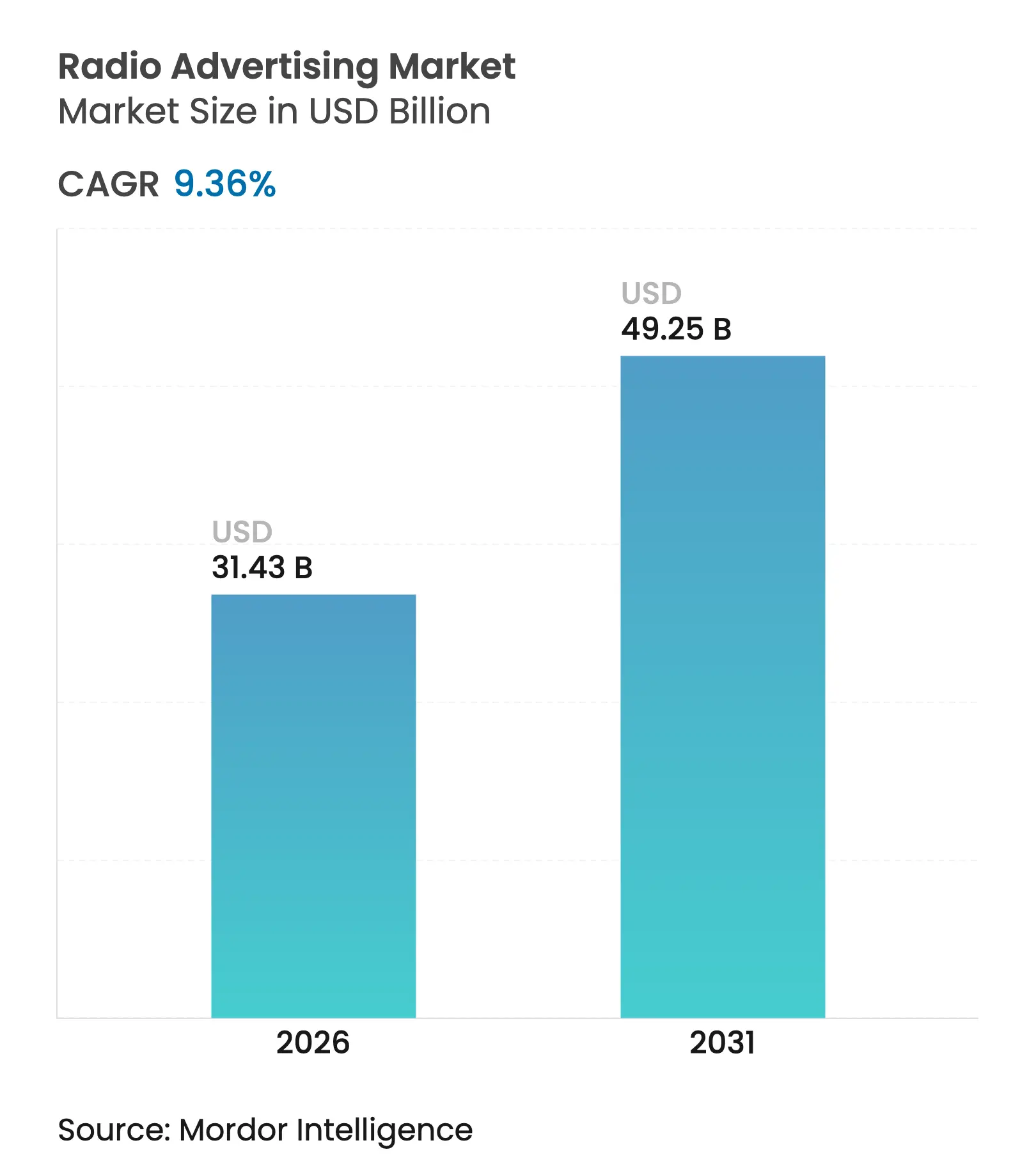

| Market Size (2026) | USD 31.43 Billion |

| Market Size (2031) | USD 49.25 Billion |

| Growth Rate (2026 - 2031) | 9.36 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Radio advertising market size in 2026 is estimated at USD 31.43 billion, growing from 2025 value of USD 28.75 billion with 2031 projections showing USD 49.25 billion, growing at 9.36% CAGR over 2026-2031. Advertisers are sustaining spend because radio supplies a high-trust, brand-safe environment, reaches more than 82% of U.S. adults each week, and now extends far beyond the dial through streaming, podcast, and smart-speaker channels soundcharts.com. Increased programmatic capacity, advancing audience measurement, and ongoing political cycles are also pushing budgets toward audio. Automakers are embedding hybrid receivers that merge over-the-air signals with IP streams, enlarging premium drive-time inventory. Meanwhile, small and mid-size advertisers are finally able to exploit radio through self-service buying tools that align cost with hyper-local reach.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Smart-speaker-led programmatic audio spend surge Smart-speaker-led programmatic audio spend surge | +2.1% | North America, spillover to Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:North America, spillover to Europe | Impact Timeline:Medium term (2-4 years) |

FM band digitization mandates FM band digitization mandates | +1.8% | India and Mexico, influence across Asia & Latin America | Long term (≥ 4 years) | |||

Automotive OTA dash integrations Automotive OTA dash integrations | +1.5% | Europe, North America | Medium term (2-4 years) | |||

Political advertising windfall 2028 Political advertising windfall 2028 | +1.2% | United States, Mexico | Short term (≤ 2 years) | |||

Brand-safety migration from social to radio Brand-safety migration from social to radio | +0.9% | Australia, New Zealand, developed markets | Medium term (2-4 years) | |||

Hyper-local geotargeted campaigns Hyper-local geotargeted campaigns | +0.7% | Brazil, wider Latin America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Smart-speaker-led programmatic audio spend surge

Programmatic audio spend is projected to climb 18% to USD 2.3 billion in 2025 as voice-activated devices become a mainstream listening gateway.[1]SiriusXM Media, “Programmatic Audio: Pragmatic, Powerful, Profitable,” siriusxmmedia.com Listeners now devote roughly 4.5 hours daily to digital audio, creating fresh inventory without diluting engagement. Roughly 38% of Pandora’s U.S. audience already accesses content via smart speakers, prompting advertisers to exploit dynamic creative optimization. Campaigns using programmatic audio have started to report measurable sales lift comparable to social channels while avoiding brand-safety concerns. Because the buying is automated, smaller advertisers can participate alongside national brands, reinforcing radio advertising market democratization.

FM band digitization mandates in India and Mexico

Compulsory migration to digital FM standards is elevating audio quality, opening multicasting capacity, and enabling metadata-rich ad triggers. Mexico’s HD Radio rollout has let broadcasters deliver secondary channels that carry segmented ad loads, improving CPMs while holding listener time spent. India’s phased digitization is likewise expected to protect radio’s 400+ million weekly reach, even as mobile data usage explodes. The policy support ensures long-tail stations keep spectrum, anchoring rural coverage and sustaining the radio advertising market in regions where broadband penetration stays uneven.

Automotive OTA dash integrations expanding drive-time inventory

Hybrid receivers that fuse terrestrial signals with IP streams are now standard on many European models. The technology lets broadcasters append synchronized visuals to audio spots, resulting in documented brand-lift gains of up to 60% for sectors such as legal services.[2]National Association of Broadcasters, “NAB Digital Dashboard Best Practices Report,” nab.org Because new vehicles remain on roads for a decade, each model year’s install base compounds available impressions, solidifying radio’s relevance at the moment purchase intent often peaks.

Political advertising windfall ahead of 2028 elections

The 2024 U.S. cycle delivered USD 326 million to radio and confirmed the medium’s potency for localized persuasio. Early bookings for 2028 indicate campaigns will broaden spend beyond television because radio reaches habitual voters without the price inflation typical in swing-state TV markets. Stations in battleground counties are packaging terrestrial and digital streams, amplifying return for down-ballot races that depend on cost-efficient frequency.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Streaming substitution among millennials Streaming substitution among millennials | -1.4% | North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:North America & Europe | Impact Timeline:Long term (≥ 4 years) |

Mobile OS privacy curbs on attribution Mobile OS privacy curbs on attribution | -1.1% | Developed markets worldwide | Medium term (2-4 years) | |||

Spectrum re-farming for 5G Spectrum re-farming for 5G | -0.8% | European Union | Long term (≥ 4 years) | |||

Measurement currency fragmentation Measurement currency fragmentation | -0.6% | Global | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Streaming service substitution shrinking millennial audiences

Terrestrial listening time among 18-34-year-olds has slipped in large metros as on-demand audio offers personalized playlists. Even though radio still captures 32% of aggregate music time among U.S. consumers aged 13+, that share is gradually ceding to subscription services.[3]Dmitry Pastukhov, “Music Market Focus: Sizing Up the US Music Industry,” Soundcharts, soundcharts.com Advertisers targeting digitally native cohorts must therefore book both broadcast and digital radio to preserve reach, a reality that inflates planning complexity and could deter spend if budgets remain flat.

iOS/Android privacy updates hindering ad attribution

Apple’s App Tracking Transparency framework and upcoming Google Play Privacy Sandbox make deterministic mobile attribution harder, raising the cost of validating radio-to-mobile conversion paths. Independent studies estimate aggregate revenue losses of nearly USD 10 billion across ad networks post-ATT.[4]Brandon Baum-Zepeda, “Apple vs. the Free Internet? Privacy and Antitrust in Mobile App Advertising,” UC Davis Business Law Journal, blj.ucdavis.edu Radio operators now depend on incrementality experiments and modeled outcomes rather than precise device IDs, a shift that weakens proof-of-performance arguments in CFO reviews.

By Type: Digital transformation reshapes revenue mix

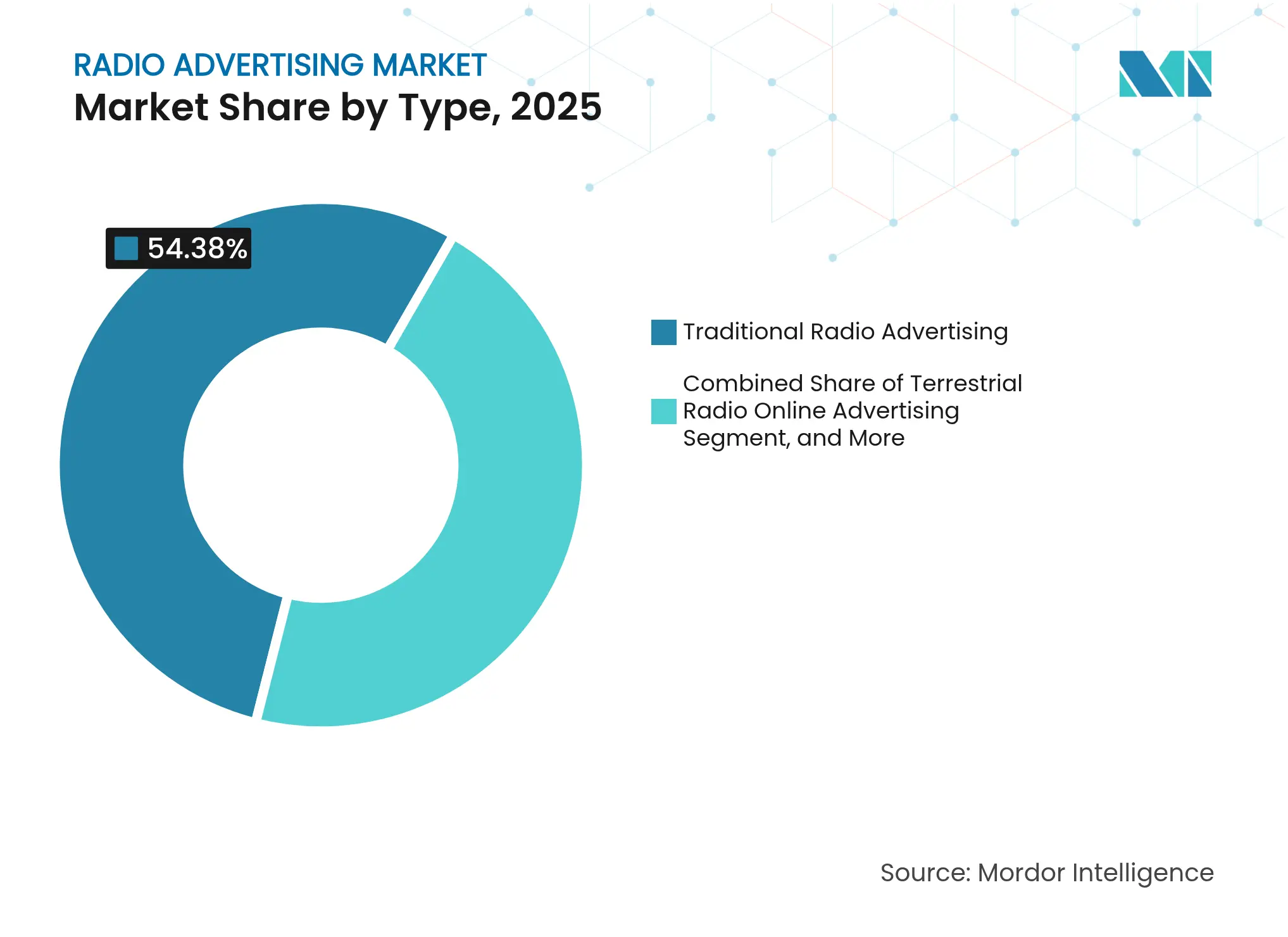

Traditional Radio Advertising contributed 54.38% of 2025 revenue, anchored by vast terrestrial footprints that deliver cost-efficient reach in every county. Major retailers, automotive brands, and political campaigns rely on these broadcasts for message ubiquity during high-interest windows, ensuring the radio advertising market retains robust spot volume even as digital channels multiply. The segment benefits from favorable economics-once capital investments in towers are sunk, incremental spots carry minimal extra cost, supporting margin stability.

In contrast, Terrestrial Radio Online Advertising is forecast to post a 12.98% CAGR through 2031 as broadcasters simulcast live streams, insert dynamic ads, and monetize time-shifted content. Programmatic platforms have reduced insertion-order friction, attracting digital-native advertisers that value auction-based price discovery. Digital extensions also deepen listener data, allowing segments like young commuters or Spanish-language households to be packaged with precision. Because most groups sell combined linear-plus-streaming bundles, they preserve traditional share while growing digital dollars-an approach that helps the radio advertising market size for online sub-formats scale without cannibalizing core income.

Satellite Radio Advertising, while representing a smaller slice, continues to command premium CPMs thanks to its national reach and affluent subscriber base. Cross-channel audio-visual packages on connected dashboards are carving out multi-sensory formats, creating distinctive sponsorship opportunities that diversify the radio advertising industry revenue stream beyond time-based spots.

Note: Segment shares of all individual segments available upon report purchase

By Enterprise Size: SMEs embrace radio’s digital evolution

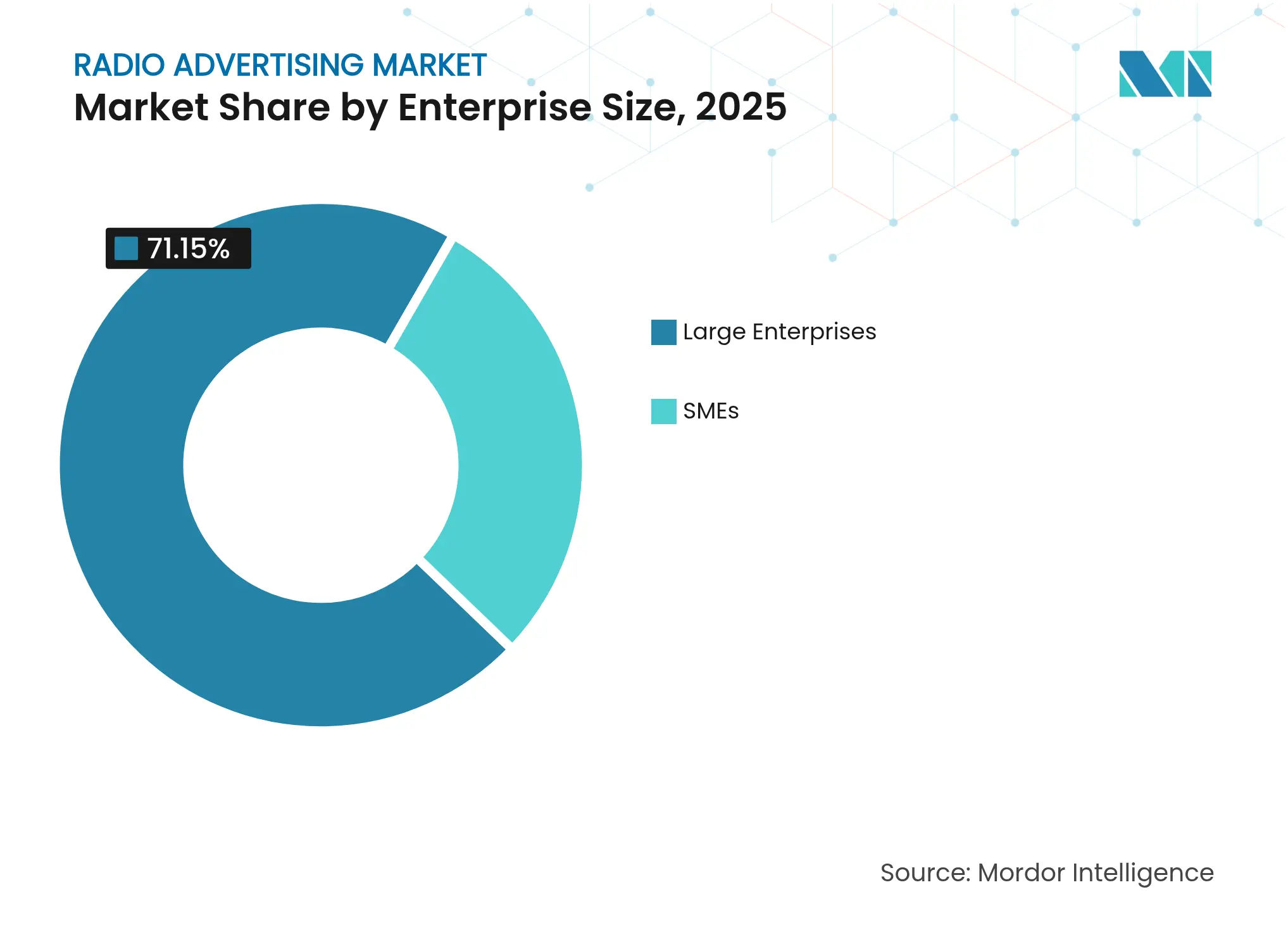

Large Enterprises controlled 71.15% of spend in 2025, leveraging comprehensive flighting across national networks and regional clusters for brand building. Financial services, insurers, and QSR chains account for a large portion of these commitments, as they value radio’s ability to balance frequency with geographic granularity. Most blue-chip advertisers now incorporate podcast and streaming inventory into their audio plans, elevating their share of radio advertising market size linked to authenticated digital impressions and first-party data overlays.

SMEs are projected to expand outlays at a 10.14% CAGR to 2031, catalyzed by self-serve buying portals that mirror social-platform ease. Dynamic ad insertion lets a neighborhood hardware store promote snow shovels during blizzards in Minneapolis while a branch in Phoenix simultaneously touts patio grills—capability unimaginable in the legacy fixed-spot model. Geotargeting reduces waste, and real-time dashboards quantify foot-traffic lift, eroding the perception that radio is immeasurable. As these tools proliferate, they are bringing thousands of incremental advertisers into the radio advertising market, softening reliance on a few national brands.

Note: Segment shares of all individual segments available upon report purchase

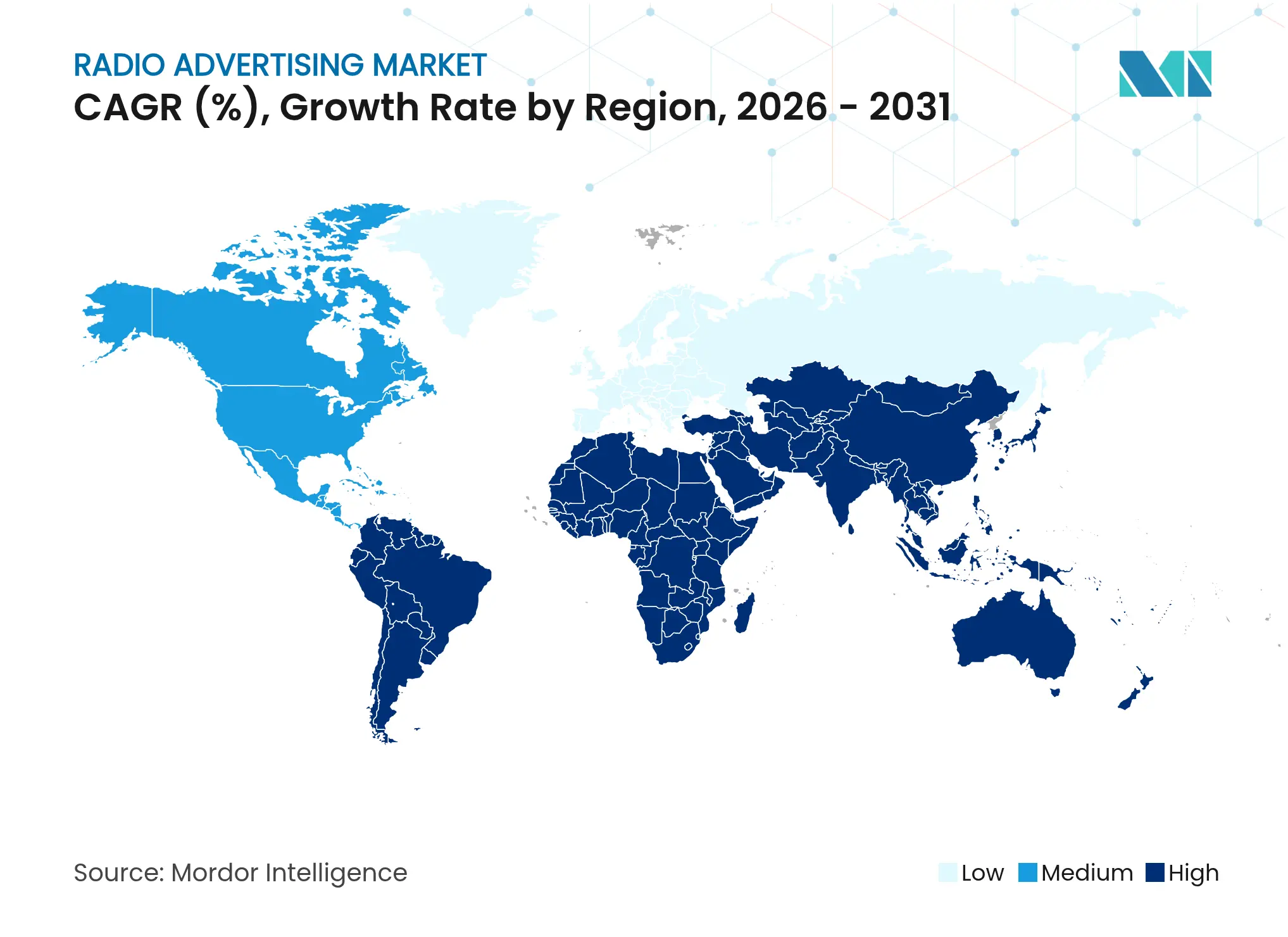

North America retained a commanding 37.62% share of the radio advertising market in 2025 on the back of mature measurement currencies and rapid uptake of programmatic audio. Local revenue is expected to reach USD 13.45 billion in 2026, with an additional USD 3.17 billion sourced from digital audio streams. Political advertising remains a pronounced driver, and connected-car dashboards are delivering synchronized banner-plus-spot formats that enhance recall for CPG and auto finance brands.

Asia-Pacific is the fastest-growing territory, on track for an 11.28% CAGR through 2031. India’s mandated shift toward digital FM, coupled with steady urbanization, preserves rural reach while unlocking metadata and addressability. China’s fusion of radio with live-commerce platforms is generating transaction-linked audio spots that integrate QR codes in companion apps, establishing novel ROI metrics. South Korea and Japan are piloting household-level audio panels powered by set-top boxes, promising granular ratings that could rival television, thereby enticing performance marketers into the radio advertising market.

Europe portrays mixed momentum. Spectrum re-farming for 5G constrains new FM licenses in dense corridors, yet the rollout of DAB+ and mandatory hybrid receivers in cars is mitigating signal loss. Germany and the United Kingdom contribute the majority of regional revenue, aided by advanced joint-industry committees that reconcile broadcast and streaming impressions. Advertisers are testing privacy-compliant addressable audio that uses contextual rather than personal data, aligning with robust GDPR enforcement and ensuring the radio advertising market continues to draw multinational brands.

Latin America shows fragmented dynamics. Brazil, the region’s largest economy, is coupling geotargeted radio campaigns with retail loyalty apps, driving measurable store traffic lifts that justify higher CPMs. Mexico’s HD Radio framework permits multicasting, broadening advertiser choice while safeguarding community programming. Argentina’s broadcasters have preserved audience trust amid economic volatility, allowing them to maintain rate integrity even as other media faced price compression. This resilience assures advertisers that the radio advertising market remains a safe harbor for brand equity across the region.

Market Concentration

The top three U.S. audio groups-Sirius XM Holdings, iHeartMedia, and Audacy-collectively control roughly 80% of revenue, indicating moderately concentrated structure. Sirius XM leverages its subscription base to bundle ad inventory with data-enhanced segments on Pandora and Stitcher, while iHeartMedia continues deleveraging via financial restructurings that freed USD 4.8 billion in debt and funded digital expansion. Audacy emphasizes podcast acquisitions and wagering content for differentiated networks. All three are integrating linear spots into programmatic exchanges, competing for the USD 2.3 billion pool forecast for 2025 programmatic audio.

Second-tier operators are carving niches. Beasley Media demonstrates 60% brand-lift gains when companion visuals accompany radio ads on connected dashboards, presenting a template smaller clusters can replicate. Regional groups in Latin America exploit hyper-localism, offering town-specific flighting that global platforms cannot match. Independent podcast networks partner with legacy stations for cross-promotion, blending new-format elasticity with heritage credibility, thereby safeguarding the radio advertising industry against audience erosion.

White-space innovation is emerging in voice commerce tie-ins. Some U.S. grocery chains now trigger Alexa skills when a shopper hears an in-store radio ad, enabling same-day coupon downloads. These interplays rely on authenticated data from smart-speaker ecosystems, signaling the next battleground where broadcasters, tech giants, and retail media networks will converge.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

Radio advertising is defined as the promotion of goods or services through radio broadcasts, whether in the form of commercials or programming. Radio ads are sold in dayparts, or segments of time.

The radio advertising market is segmented by type (traditional radio advertising, terrestrial radio broadcast advertising, terrestrial radio online advertising, satellite radio advertising), by enterprises (SMEs, large enterprises), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.