In-vitro Colorectal Cancer Screening Tests Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

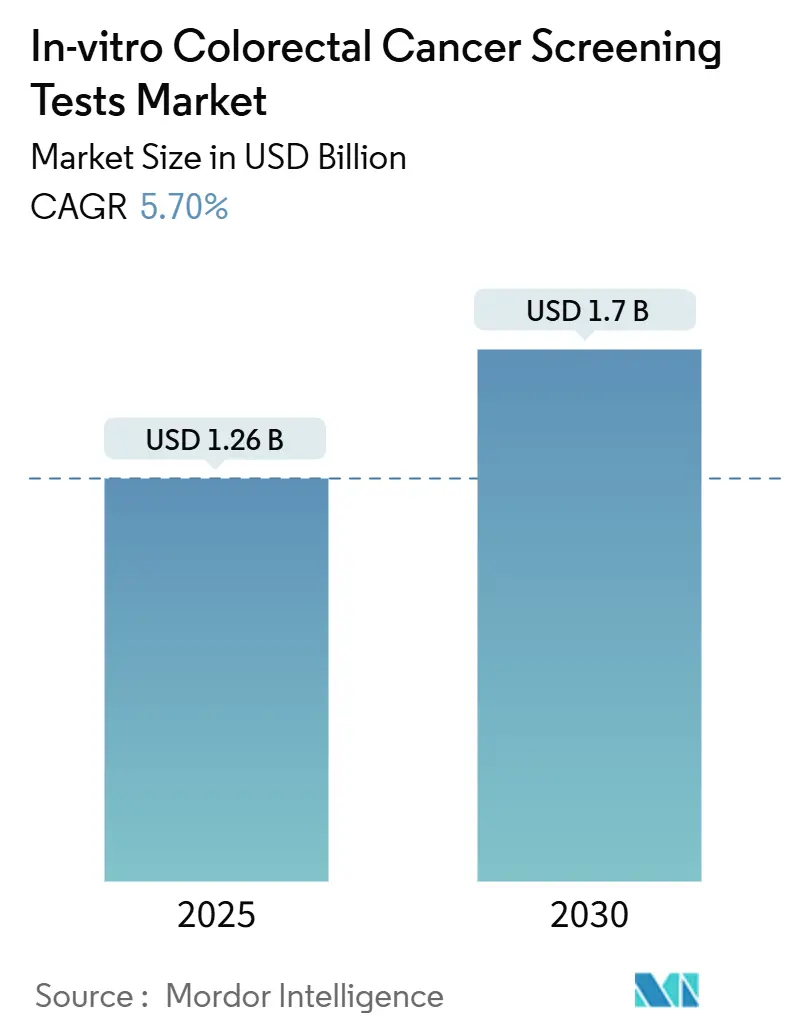

| Market Size (2025) | USD 1.26 Billion |

| Market Size (2030) | USD 1.7 Billion |

| Growth Rate (2025 - 2030) | 5.70% CAGR |

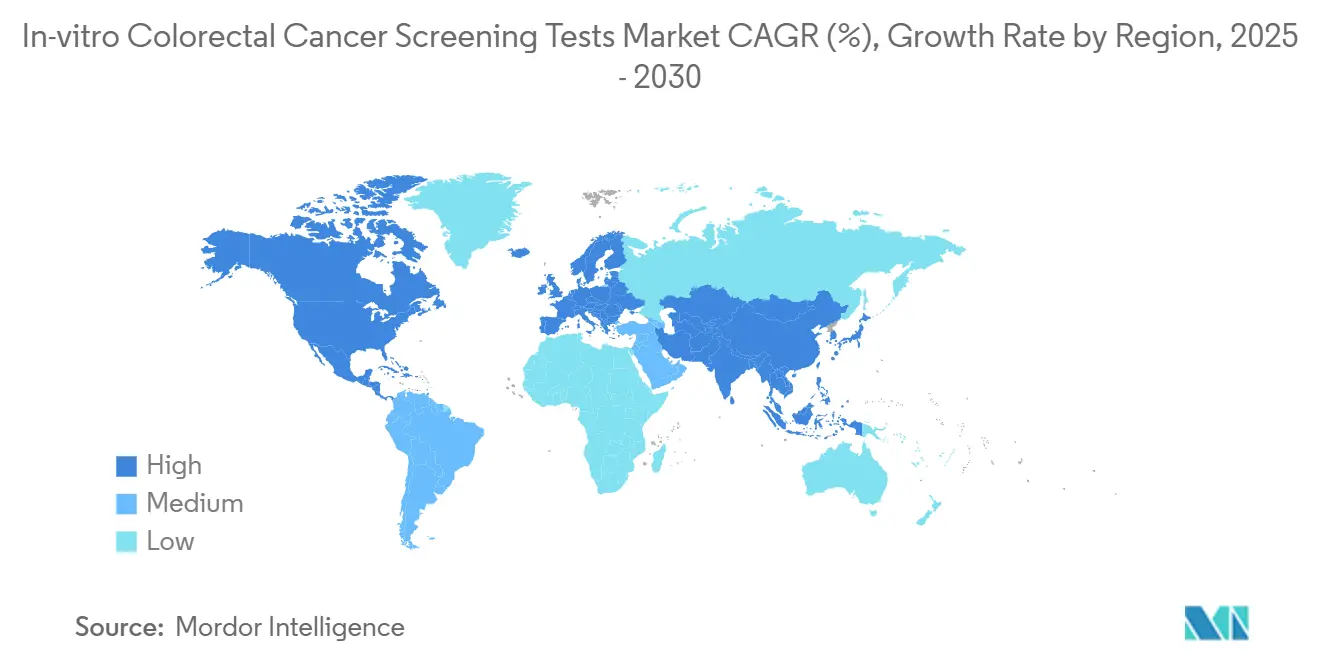

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

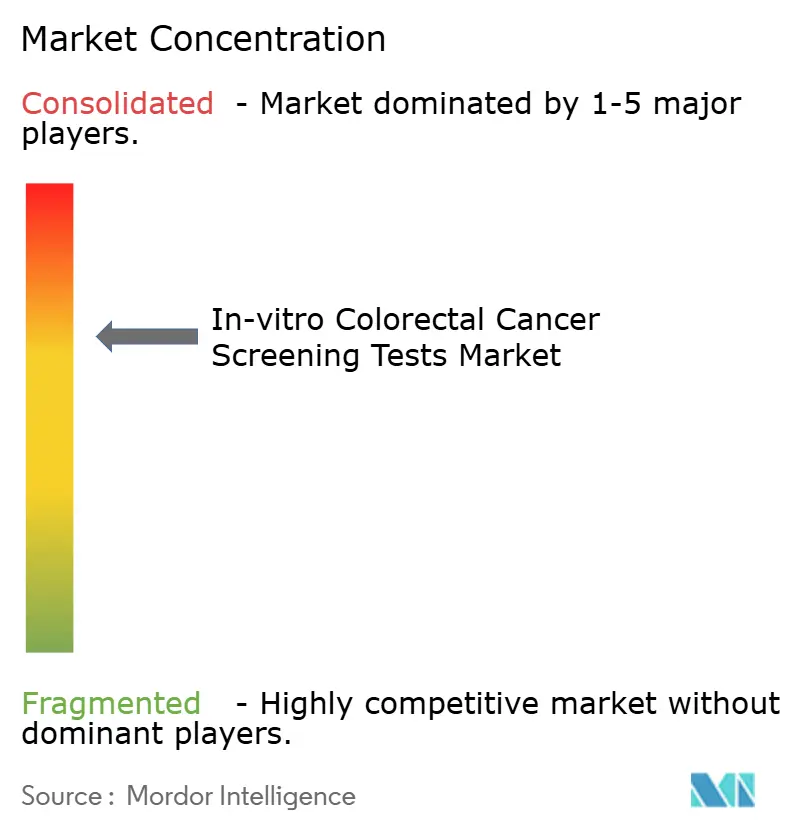

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

In-vitro Colorectal Cancer Screening Tests Market Analysis by Mordor Intelligence

The in-vitro colorectal cancer screening tests market size stands at USD 1.26 billion in 2025 and is forecast to expand to USD 1.70 billion by 2030, advancing at a 5.7% CAGR. This moderate, steady trajectory reflects simultaneous demographic pressures, payer-driven policy mandates, and rapid diffusion of AI-enabled diagnostic technologies that are reshaping early-detection workflows across hospital, ambulatory, and home-collection settings. Guideline harmonization, led by the U.S. Preventive Services Task Force’s 2021 age-reduction to 45 years, instantly expanded the eligible screening cohort by more than 19 million U.S. adults and catalyzed similar policy shifts in Canada, Mexico, and several European member states, thereby locking-in a structural volume uplift across the in-vitro colorectal cancer screening tests market. Reimbursement parity for at-home tests, finalized by CMS in the 2025 Physician Fee Schedule, removed residual out-of-pocket cost barriers and accelerated test uptake across commercial and Medicare risk pools. At the same time, corporate wellness programs in North America and parts of the EU are bundling non-invasive colorectal screening into annual benefit packages, cementing employer-sponsored channels as a new demand vector for the in-vitro colorectal cancer screening tests market. Finally, AI-assisted colonoscopy systems, now reimbursed in Japan, are enhancing adenoma-detection rates by 27%, freeing limited endoscopy capacity for high-risk patients and amplifying demand for triage tests such as FIT and multi-target stool DNA assays.

Key Report Takeaways

- By test type, FIT led with 39.8% of in-vitro colorectal cancer screening tests market share in 2024, whereas blood-based ctDNA tests recorded the fastest growth, advancing at a 7.4% CAGR through 2030.

- By technology platform, immunoassay methods accounted for 41.5% revenue share in 2024, while next-generation sequencing platforms are projected to rise at a 6.9% CAGR to 2030.

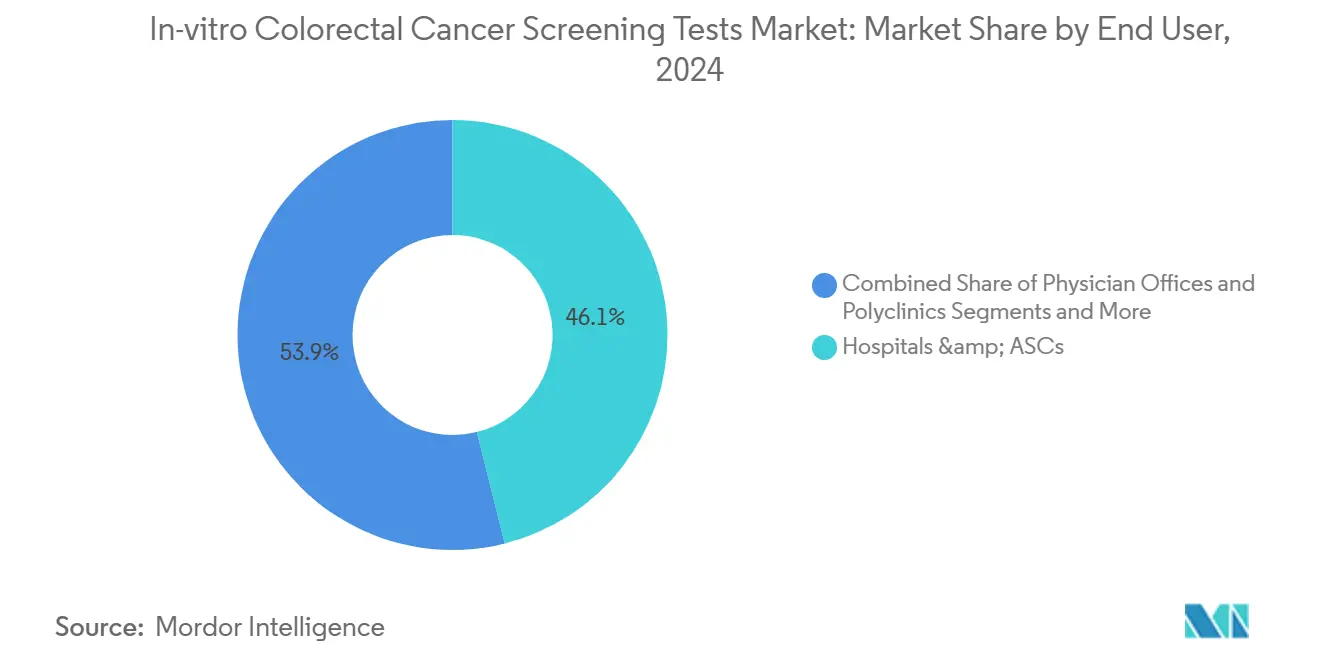

- By end user, hospitals and ambulatory surgery centers commanded 46.1% share of the in-vitro colorectal cancer screening tests market size in 2024; home-collection and direct-to-consumer channels exhibit the highest projected CAGR at 5.1% over the same period.

- By geography, North America captured 45.2% of the in-vitro colorectal cancer screening tests market in 2024, whereas Asia Pacific is forecast to expand at the fastest 5.8% CAGR through 2030.

Global In-vitro Colorectal Cancer Screening Tests Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lowered CRC screening age to 45 | +1.20% | Global (highest in North America) | Medium term (2-4 years) |

| Rapid uptake of next-gen stool-DNA tests | +0.80% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Parity reimbursement for at-home tests | +0.60% | North America; spillover to developed APAC | Medium term (2-4 years) |

| AI-driven triage of colonoscopy backlog | +0.40% | Global, early in North America & EU | Long term (≥ 4 years) |

| Corporate wellness mandates | +0.30% | North America, emerging in EU | Medium term (2-4 years) |

| Liquid-biopsy MRD assays for first-line use | +0.20% | Global, advanced economies first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lowered CRC Screening Age to 45 In Major Guidelines

Guideline harmonization opened a structural, multi-decade growth runway. USPSTF, ACS, and CMS policy shifts now mandate no-cost coverage for average-risk adults from age 45, a cohort projected to reach 27 million individuals by 2030. Commercial insurers mirrored the move within 18 months, eliminating co-payments for initial tests and follow-up colonoscopies. This alignment effectively removed price elasticity from patient decision-making and redirected payer focus toward test completion rates and downstream cost avoidance.[1]Centers for Medicare & Medicaid Services, “CY 2025 Medicare Physician Fee Schedule Final Rule,” cms.gov

Rapid Uptake of Next-Generation Multi-Target Stool-DNA Tests

Cologuard use leaped from 3% of colorectal screens in 2018 to 31% by 2023. FDA clearance of Cologuard Plus in October 2024 lifted cancer sensitivity to 95% while slashing false positives by 40%, positioning the assay as a high-value alternative to guaiac FOBT and FIT. Modeling shows the original test prevented 623,000 cancers and precancers over ten years, generating USD 22 billion in system savings.

Parity Reimbursement for At-Home Tests

CMS now treats colonoscopy after a positive non-invasive result as a screening procedure, eliminating prior cost-sharing loopholes. Anthem, Cigna, and UnitedHealthcare extended identical policies, making home-collection pathways cost-neutral versus facility screening for 180 million privately insured lives. Providers can therefore deploy mail-out testing at scale, reserving colonoscopy suites for positive cases and high-risk cohorts.

AI-Driven Colonoscopy Backlog Triaging

Randomized trials reveal 58.7% adenoma-detection with Endocuff-AI compared with 46.3% under conventional high-definition optics, translating to a 27% relative lift. Japan’s 2024 reimbursement for CAD tools validated the economics, incentivizing other payers to consider similar add-on fee schedules. Health systems can therefore deploy AI scopes for positive FIT or stool-DNA cases and standard scopes for routine surveillance, optimizing throughput without compromising quality.[2]Masashi Misawa et al., “Implementation of Artificial Intelligence in Colonoscopy Practice in Japan,” jmaj.jp

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High false-positive cascade costs | -0.90% | Global, cost-sensitive markets hit hardest | Medium term (2-4 years) |

| Sensitivity gaps for advanced adenomas in blood tests | -0.60% | Global, early adopters of blood screening | Short term (≤ 2 years) |

| Genomic-data privacy regulation tightening | -0.40% | North America & Europe | Long term (≥ 4 years) |

| IVD reagent supply-chain fragility post-COVID | -0.30% | Global, especially emerging economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High False-Positive Cascade Costs

Annual FIT can yield a cumulative 23% false-positive rate over a decade, driving up to 1.3 million extra colonoscopies across G7 markets and adding USD 1.8 billion in avoidable direct spending.[3]Aasma Shaukat et al., “AGA Clinical Practice Update on Blood Tests for CRC Screening,” cghjournal.org Stool-DNA tests improve sensitivity but still carry a 13% false-positive frequency, compelling payers to factor colonoscopy capacity and labor constraints into population-health economics.

Sensitivity Gaps for Advanced Adenomas in Blood Tests

While Shield and similar assays meet FDA thresholds for cancer detection, sub-15% sensitivity for advanced precancerous lesions limits their preventive value. Clinical societies now advise blood tests only for patients refusing or unable to perform stool-based screening, thereby capping near-term adoption ceilings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: FIT Scale versus ctDNA Momentum

The in-vitro colorectal cancer screening tests market size for test-type revenue favored FIT at 39.8% in 2024 as public health agencies continue bulk mail-out programs that prioritize affordability and logistical simplicity. Blood-based ctDNA platforms, however, post a 7.4% CAGR, the fastest within the test-type matrix, as payer parity and patient comfort propel wider trial deployment. FIT vendors compete on unit price and automated analyzer throughput, whereas stool-DNA suppliers differentiate on superior sensitivity and patient-navigation services, creating a nuanced, dual-track expansion path for the in-vitro colorectal cancer screening tests market.

In volume terms, guaiac FOBT still underpins mass screening in several emerging economies but is losing share as middle-income nations integrate FIT into insurance benefit packages. Multi-target stool-DNA occupies a premium niche, capturing risk-averse consumer cohorts and employer programs. With FDA approval of Cologuard Plus, Exact Sciences positioned stool-DNA at the confluence of non-invasive convenience and near-endoscopic sensitivity, thereby pressuring blood-test entrants to demonstrate meaningful adenoma performance before they can erode the in-vitro colorectal cancer screening tests market share held by established stool-based assays.

By Technology Platform: Immunoassay Dominance Meets NGS Upswing

Immunoassay chemistry supports 41.5% of 2024 revenue, leveraging low-cost reagents and decades-long familiarity among laboratory technologists. The segment benefits from high throughput and abundant supplier competition, which compresses per-test costs and sustains mass-screening economics, especially in publicly funded systems. In contrast, next-generation sequencing is carving out a 6.9% CAGR niche by enabling multiplex ctDNA panels and RNA-signature workflows that promise pan-cancer utility alongside colorectal screening.

PCR-based assays retain relevance for targeted mutation detection in centralized labs, while epigenetic signature platforms attract venture funding for ‘one-tube, multi-cancer’ ambitions. FDA clearance of ColoSense, an eight-RNA-marker stool test, attests to regulatory acceptance of more complex molecular readouts and reinforces the narrative that analytic sophistication can translate into clinically material sensitivity gains, thereby justifying higher average selling prices within the in-vitro colorectal cancer screening tests market size calculus.

By End User: Hospitals Anchor, Home-Collection Accelerates

Hospitals and ambulatory surgery centers generated 46.1% of 2024 revenue, reflecting their central role in colonoscopy, polypectomy, and pathology confirmation workflows. Yet the home-collection channel, nourished by employer programs and mail-order pharmacy integrations, is tracking a 5.1% CAGR to 2030, the fastest among end-user groups. Clinical laboratories, though not patient-facing, sit at the operational nexus, processing roughly 68% of all non-invasive assay volumes and monetizing each platform transition within the in-vitro colorectal cancer screening tests market.

Physician offices drive initial patient education and funnel test selection toward lab hubs, but digital platforms now supplement counseling with app-based reminders, raising completion rates from 56% to 78% in pilot programs run by integrated delivery networks. Corporate wellness providers, sensing tangible ROI in reduced absenteeism, are embedding stool-DNA kits into annual screenings, further accelerating specimen flow through decentralized logistics chains.

Geography Analysis

North America retains leadership with a 45.2% in-vitro colorectal cancer screening tests market share, underpinned by payer parity, employer adoption, and rapid regulatory clearance for novel diagnostics. The United States accounts for roughly four-fifths of regional revenue, with expanded coverage for CT colonography and stool-DNA follow-up colonoscopy underwriting steady test uptake across commercial and Medicare Advantage lives. Canada follows with phased provincial rollout of FIT mailers, while Mexico’s social-security system began pilot FIT distribution in urban zones during 2024.

Europe contributes a robust but slower-growing base, tempered by budget ceilings in single-payer frameworks. The United Kingdom’s NHS Bowel Screening Programme is transitioning from gFOBT to FIT, but cost containment caps rapid oscillation toward newer, pricier molecular alternatives. Germany and France approve stool-DNA reimbursement on a case-by-case basis for average-risk adults with prior screening non-compliance, signaling a cautious yet open stance toward innovation.

Asia Pacific, forecast at a 5.8% CAGR, benefits from China’s accelerating urbanization and related lifestyle shifts that elevate colorectal incidence. Japan’s early reimbursement of AI-colonoscopes sets a precedent for technologically progressive payers, while South Korea institutes combined FIT-plus-colonoscopy pathways for citizens age 45-80. India’s nascent national cancer mission earmarks funds for FIT pilot procurement, yet per-capita spending lags, suggesting gradual uptake curves. Middle East & Africa and South America remain opportunity pockets; Brazil’s SUS plans to extend FIT coverage nationwide by 2027, and GCC states invest in premium AI-scope fleets for private centers catering to medical tourism.

Competitive Landscape

Market concentration remains moderate. Exact Sciences anchors multi-target stool-DNA with Cologuard Plus, buttressed by a decade of clinical-outcome evidence and tight payer partnerships. Guardant Health’s Shield blood test marks a strategic diversification from oncology monitoring into population screening and targets high-compliance patient segments who refuse stool collection. Traditional IVD majors—Roche, Abbott, Siemens—defend share via high-throughput FIT analyzers and bundled chemistry menus, leveraging procurement synergies across hospital labs.

Upstarts such as Geneoscopy push RNA-based assays that promise superior specificity, while AI-scope vendors (Olympus, Fujifilm, Medtronic) bundle detection algorithms into hardware refresh cycles, securing long-tail service contracts. Corporate wellness integrators (Color Health, Everlywell) build digital front-ends that circumvent primary-care bottlenecks and negotiate directly with self-insured employers, opening an adjacent channel that could mature into a sub-segment valued at roughly USD 220 million by 2030. Regulatory clarity on laboratory-developed tests, finalized by FDA in May 2024, raises the compliance bar, favoring players with established quality-systems infrastructure.

Strategic collaborations intensify: Exact Sciences inked co-marketing deals with Epic, integrating electronic orders directly into clinician workflows, while Guardant partners with Quest Diagnostics to scale blood-test processing. M&A appetite centers on data-analytics assets to refine risk-stratification algorithms that steer patients toward the most cost-effective modality, thereby lowering payer total cost of care while reinforcing vendor differentiation.

In-vitro Colorectal Cancer Screening Tests Industry Leaders

Exact Sciences Corporation

Guardant Health Inc.

Roche Diagnostics

Abbott Laboratories

Polymedco CDP, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Exact Sciences commercially launched Cologuard Plus with Medicare coverage and updated guideline inclusion.

- July 2024: FDA cleared Guardant Health’s Shield blood test as the first blood-based primary screening option.

- May 2024: FDA authorized Geneoscopy’s ColoSense RNA-biomarker stool test.

Global In-vitro Colorectal Cancer Screening Tests Market Report Scope

| Guaiac-based FOBT (gFOBT) |

| Fecal Immunochemical Test (FIT) |

| Multi-target Stool-DNA Test (mt-sDNA) |

| Blood-based ctDNA Test |

| Serum / Other Biomarker Panels |

| Immunoassay |

| PCR-based Molecular Assays |

| Next-Generation Sequencing (NGS) |

| Epigenetic Biomarker Detection |

| Protein Microarray / Others |

| Hospitals & ASCs |

| Clinical Reference Laboratories |

| Physician Offices & Polyclinics |

| Home-Collection / DTC Channels |

| Corporate Wellness Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Guaiac-based FOBT (gFOBT) | |

| Fecal Immunochemical Test (FIT) | ||

| Multi-target Stool-DNA Test (mt-sDNA) | ||

| Blood-based ctDNA Test | ||

| Serum / Other Biomarker Panels | ||

| By Technology Platform | Immunoassay | |

| PCR-based Molecular Assays | ||

| Next-Generation Sequencing (NGS) | ||

| Epigenetic Biomarker Detection | ||

| Protein Microarray / Others | ||

| By End User | Hospitals & ASCs | |

| Clinical Reference Laboratories | ||

| Physician Offices & Polyclinics | ||

| Home-Collection / DTC Channels | ||

| Corporate Wellness Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2025 global value of colorectal screening?

The in-vitro colorectal cancer screening tests market size is USD 1.26 billion in 2025.

How fast will revenue grow to 2030?

Revenue is projected to rise to USD 1.70 billion by 2030, reflecting a 5.7% CAGR.

Which test type is expanding quickest?

Blood-based ctDNA assays lead growth at a 7.4% CAGR.

Which region grows fastest after 2025?

Asia Pacific posts the highest regional CAGR of 5.8% through 2030.

Which technology now holds the largest share?

Immunoassay platforms command 41.5% of 2024 revenue.

What restrains blood-test adoption most?

Advanced adenoma sensitivity remains below 15%, limiting preventive value.

Page last updated on: