Egypt Telecom Tower Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 241.60 Million |

| Market Size (2026) | USD 247.37 Million |

| Market Size (2031) | USD 278.35 Million |

| Growth Rate (2026 - 2031) | 2.39% CAGR |

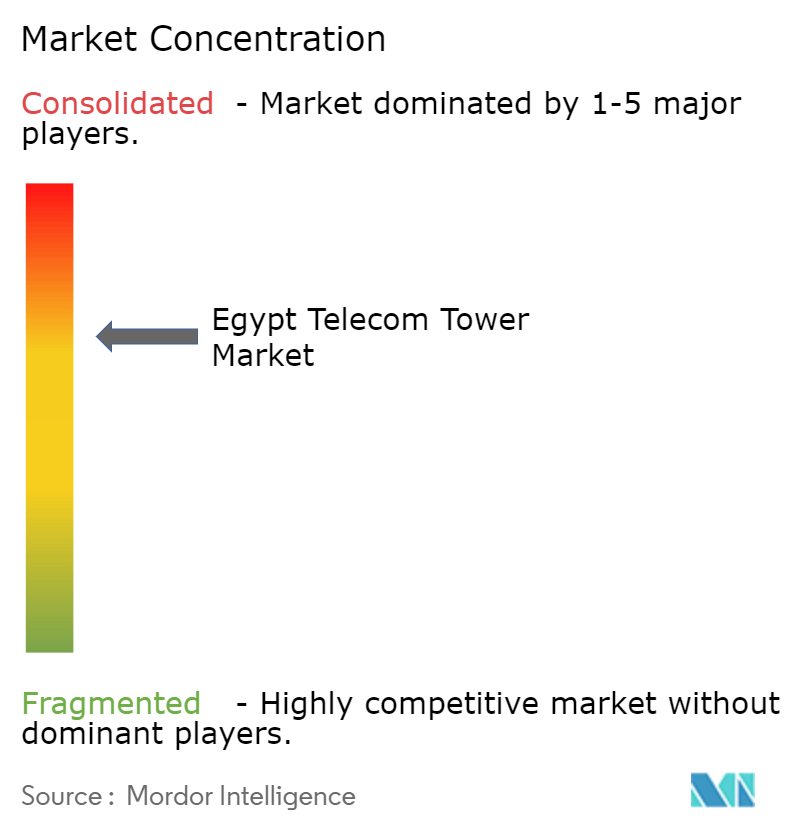

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Telecom Tower Market Analysis by Mordor Intelligence

The Egypt Telecom Tower Market size was valued at USD 241.60 million in 2025 and estimated to grow from USD 247.37 million in 2026 to reach USD 278.35 million by 2031, at a CAGR of 2.39% during the forecast period (2026-2031).

Moderate growth reflects Egypt’s shift from green-field roll-outs to network densification and technology upgrades that follow the USD 675 million 5G licensing round. Higher data-traffic intensity in Cairo and Alexandria, supportive regulation for infrastructure sharing, and the rapid move toward renewable power solutions underpin demand, while currency volatility and permitting delays temper momentum. IHS Towers’ government-backed entry and forthcoming tower divestitures by Telecom Egypt illustrate the market’s structural evolution as operators adopt asset-light strategies. Neutral-host coverage for smart-city projects and subsea-cable landing-station clustering along the Mediterranean and Red Sea coasts create specialized build-to-suit opportunities. At the same time, the sector’s low tenancy ratio below 1.35x limits cash-flow leverage compared with mature markets where ratios surpass 2.0x.

Key Report Takeaways

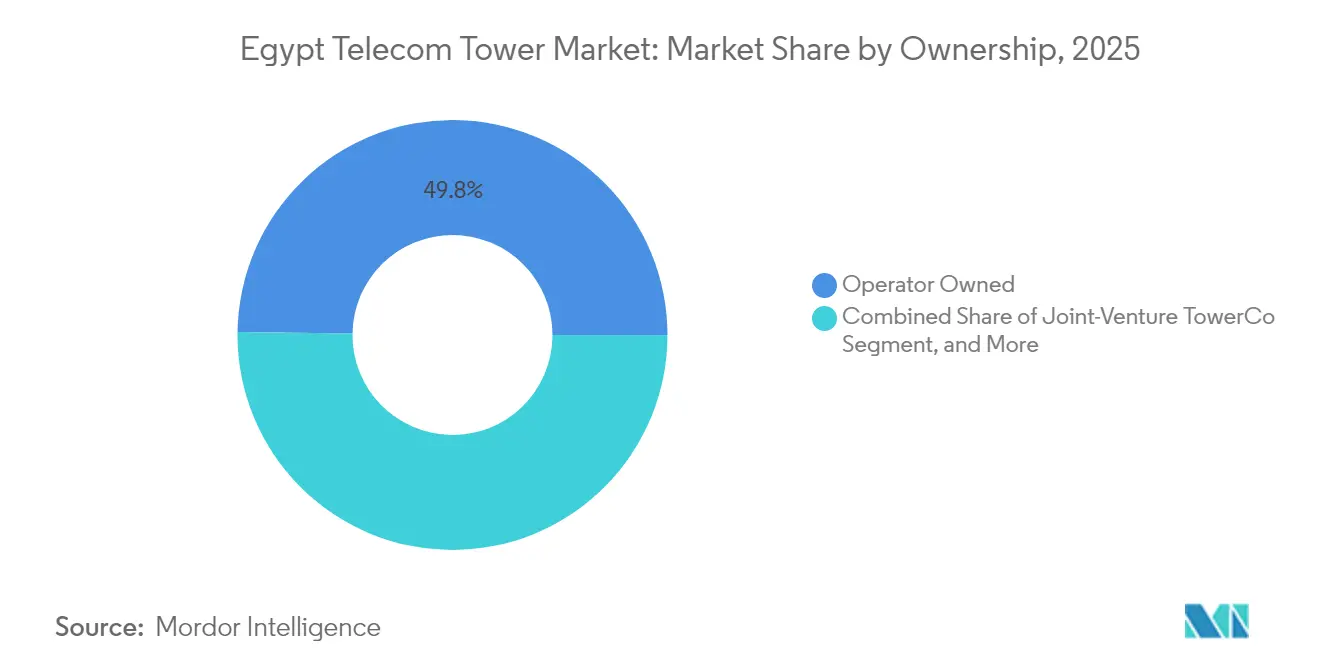

- By ownership, operator-owned towers held 49.78% revenue share in 2025, while independent TowerCos are projected to grow at a 11.65% CAGR to 2031.

- By installation type, ground-based sites captured 50.92% of the Egypt telecom towers market share in 2025, whereas rooftop deployments are advancing at a 3.52% CAGR through 2031.

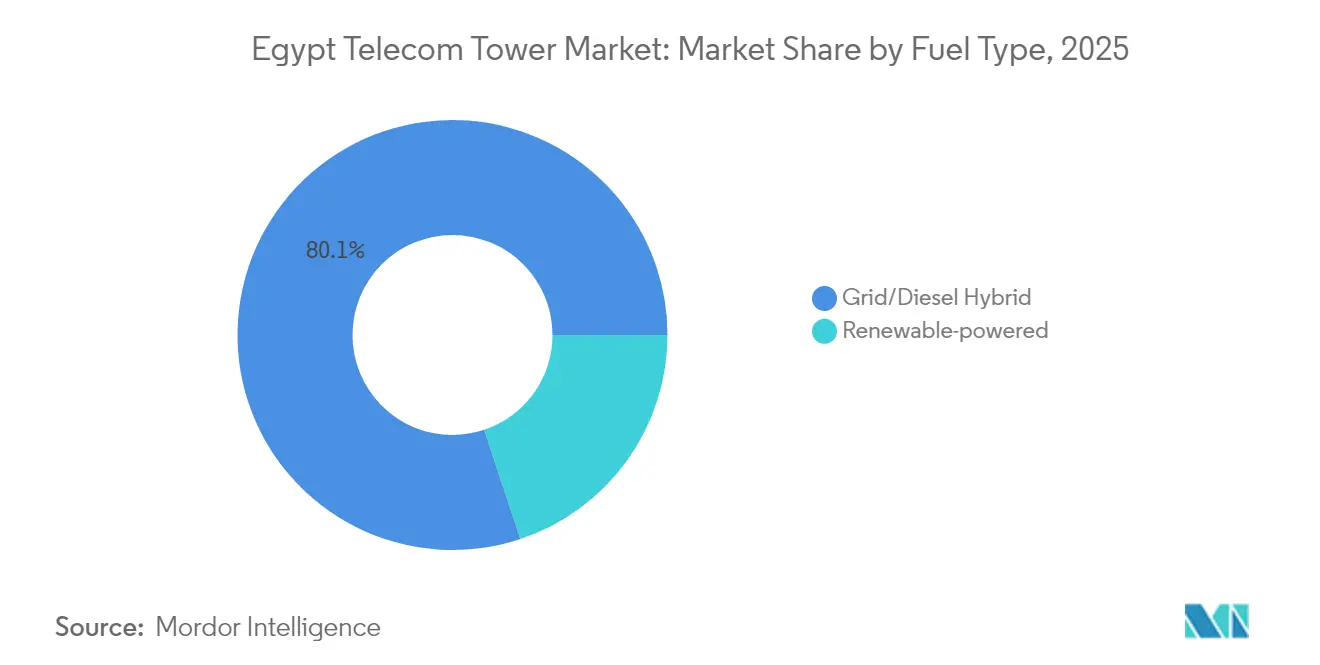

- By fuel type, grid/diesel hybrids accounted for 80.12% of the Egypt telecom towers market size in 2025; renewable-powered towers are expected to rise at an 18.25% CAGR to 2031.

- By tower design, stealth structures contributed 21.24% revenue in 2025 and are set to expand at a 7.31% CAGR over the forecast period.

- Vodafone Egypt, Orange Egypt, e& Egypt, and Telecom Egypt collectively managed a tenancy ratio below 1.35x in 2024, limiting scale benefits relative to international benchmarks.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Telecom Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 4G/5G spectrum awards accelerating densification | +0.8% | National, Greater Cairo and Alexandria | Medium term (2-4 years) |

| Government push for infrastructure-sharing and new tower-licence regime | +0.4% | National | Long term (≥ 4 years) |

| High urban data-traffic growth in Cairo and Alexandria corridors | +0.6% | Greater Cairo and Alexandria | Short term (≤ 2 years) |

| Rising demand for green-energy tower retrofits to curb diesel costs | +0.3% | National, rural priority | Medium term (2-4 years) |

| Smart-city projects requiring neutral-host coverage | +0.2% | New Administrative Capital, SCZONE | Medium term (2-4 years) |

| Subsea-cable landing-station clustering boosting coastal tower rollout | +0.2% | Mediterranean and Red Sea coasts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

4G/5G spectrum awards accelerating densification

Completion of the USD 675 million 5G licensing round in October 2024 compels all four mobile operators to add capacity quickly. Vodafone Egypt’s May 2025 deployment of Ericsson triple-band radios exemplifies the advanced multi-band equipment now required. Higher-frequency 5G bands demand denser site grids, prompting upgrades of existing macro towers and fresh rooftop micro-cell installations. The coordinated licensing schedule prevents duplicative builds, yet it also raises competitive pressure to achieve first-mover coverage benefits. New use cases in IoT, smart logistics, and health care set by the Ministry of Communications and Information Technology further tighten time-to-market imperatives.

Government push for infrastructure-sharing and new tower-licence regime

The National Telecommunications Regulatory Authority (NTRA) now embeds sharing incentives into licence terms, offering spectrum fee rebates when two or more operators co-locate equipment. [1]Orange Business, “Shared Infrastructure Powers Egypt’s New Administrative Capital,” orange-business.comShared towers in the New Administrative Capital showcase how neutral-host models cut capital intensity while meeting urban aesthetic norms. The regime aligns with the Digital Egypt Strategy that targets accelerated rural coverage at lower cost. It also opens the door for TowerCos that can aggregate demand and use global best practices to lift tenancy ratios, thereby improving site economics over the long term.

High urban data-traffic growth in Cairo and Alexandria corridors

Commuters lose EGP 50 billion (USD 1.6 billion) in productivity each year due to Cairo traffic, spurring greater in-transit video streaming and social networking. [2]Airwave Advisors, “Historic Site Permitting Challenges for Cell Towers,” airwaveadvisors.comPopulation density above 15,000 per km² in central districts overwhelms legacy macro coverage, generating concentrated demand for small cells and distributed antenna systems. Alexandria’s industrial ports add separate enterprise capacity needs, especially for logistics applications tied to maritime trade. Both corridors therefore require simultaneous increases in spectrum efficiency and physical site numbers, encouraging innovative deployment forms such as street-level poles and building-integrated antennas.

Rising demand for green-energy tower retrofits to curb diesel costs

Egypt’s target to reach 42% renewable generation by 2030 underpins policy support for solar-hybrid telecom sites. Orange Egypt has already cut carbon emissions 18% versus its 2023 baseline, validating operational savings through on-site photovoltaic arrays. Currency depreciation pushed diesel expenses sharply higher after the pound’s 40% slump in March 2024. As a result, payback periods on solar retrofits shorten, especially in grid-unreliable rural areas where diesel gensets previously ran 10-12 hours daily. TowerCos can leverage abundant irradiation and concessional green-finance lines to lock in lower life-cycle energy costs.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Egyptian-pound volatility inflating imported steel and radio costs | -0.7% | National | Short term (≤ 2 years) |

| Slow municipal permitting, especially heritage and coastal zones | -0.3% | Cairo heritage districts, Alexandria coast | Medium term (2-4 years) |

| Low current tenancy ratio curbing TowerCo ROI | -0.4% | National | Long term (≥ 4 years) |

| Grid unreliability outside Greater Cairo raising opex for power | -0.2% | Rural and Upper Egypt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Egyptian-pound volatility inflating imported steel and radio costs

The pound’s 40% slide against the U.S. dollar in March 2024 raised steel and radio-equipment prices that account for as much as 70% of tower build budgets. Telecom Egypt responded by securing a USD 200 million loan in May 2024 to refinance costlier short-term debt and hedge future imports. While the NTRA allowed 10-17% tariff uplifts to soften the blow, many projects still face longer payback horizons. Currency hedging tools remain expensive, meaning capital outlays stay vulnerable to further FX swings during multi-year construction cycles.

Slow municipal permitting, especially heritage and coastal zones

Heritage districts require sign-offs from antiquities, urban harmony, and local governorate bodies, stretching approval times to several months. Coastal developments must also pass environmental impact assessments, complicating roll-outs in Red Sea tourism hubs. The absence of standardized processes across 27 governorates forces operators to navigate divergent documentation and informal practices. These delays raise project management costs and deter smaller TowerCos that lack the local relationships needed to expedite permits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos Drive Consolidation

Operator-owned assets still dominated the Egypt telecom towers market with 49.78% share in 2025. However, independent TowerCos are projected to record a 11.65% CAGR as divestiture programs gather pace. The IHS Towers 80%-20% joint venture with the Egyptian government gives the company rights to deploy 5,800 sites within three years. This move validates independent models under Egypt’s advancing regulatory environment and injects international tower management know-how into the ecosystem.

Independent TowerCos benefit from currency-linked funding sources that operators often lack, letting them acquire towers from cash-constrained MNOs. Telecom Egypt’s plan to sell 2,500 sites for USD 200-250 million exemplifies this trend and could lift the Egypt telecom towers market size for independent players by 2026. With tenancy ratios under 1.35x, TowerCos aim to create new revenue streams through energy-as-a-service offers and co-location deals that raise utilization. Those that secure early mover scale are positioned to capture the Egypt telecom towers market share gains as infrastructure sharing becomes mandatory in new smart-city zones.

By Installation: Rooftop Deployments Accelerate Urban Coverage

Ground-based structures maintained 50.92% share of the Egypt telecom towers market in 2025, reflecting legacy roll-out patterns in suburban and rural districts. Yet rooftops are growing 3.52% annually as Cairo’s real-estate density prompts operators to substitute scarce land plots with building-mounted solutions. The New Administrative Capital integrates smart lampposts and rooftop antennas orchestrated through centralized monitoring, illustrating how planning authorities streamline rooftop approvals.

Rooftop towers shorten deployment lead times and reduce rent expenses, making them attractive in premium urban districts where ground leases have surged. Aesthetic norms set by heritage bodies now favor low-profile installations, which rooftop setups can satisfy using concealed enclosures that blend with skylines. These trends improve network reach while mitigating community pushback, supporting incremental growth in the Egypt telecom towers market.

By Fuel Type: Renewable Power Gains Momentum

Grid/diesel hybrids still comprised 80.12% of the Egypt telecom towers market size in 2025. Diesel reliance persists because grid stability remains a challenge outside Greater Cairo. Nonetheless, renewable-powered sites should grow 18.25% per year through 2031 as solar module costs keep falling and green-finance lines expand. Egypt’s abundant irradiation averages 2,300 kWh/m² annually, allowing payback periods under five years for hybrid solar systems, especially where diesel gensets run more than eight hours daily.

Operators such as Orange Egypt have committed to net-zero timelines, catalyzing portfolio-wide retrofit programs that replace diesel gensets with photovoltaic arrays and lithium batteries. TowerCos see energy services as a diversification lever that can lift tenancy economics and lower opex volatility stemming from FX-linked diesel imports. As renewable penetration rises, the Egypt telecom towers market share of green sites will likely exceed 25% by 2031, creating scale for local EPC contractors and battery suppliers.

By Tower Type: Stealth Solutions Lead Innovation

Stealth or concealed designs captured 21.24% revenue in 2025 and are predicted to advance at 7.31% CAGR. Municipal ordinances in Cairo heritage districts stipulate visual harmony, steering new builds toward camouflaged monopoles and palm-tree replicas. Coastal tourist zones along the Red Sea impose similar aesthetic constraints to protect sightlines, fostering demand for bespoke concealment solutions.

Monopoles and lattice structures continue to dominate open-area deployments where cost per meter remains critical. Yet stealth innovations now integrate multi-band antennas internally, supporting 4G and 5G layers without external protrusions. Suppliers able to manufacture such composite structures domestically can mitigate FX risk on imported steel, further boosting adoption. As a result, concealed designs will account for a rising slice of the Egypt telecom towers market size, particularly in urban infill and smart-city contexts.

Geography Analysis

Greater Cairo and Alexandria corridors together accounted for nearly 60% of national mobile data traffic in 2025 despite covering less than one-quarter of Egypt’s land mass. The capital’s density and chronic traffic congestion, costing USD 1.6 billion in annual productivity losses, fuel mobile video consumption and heighten 5G capacity needs. Rooftop micro-cells and street-level poles now complement traditional macro towers to hit coverage obligations in districts exceeding 15,000 inhabitants per km².

Alexandria benefits from its dual role as a port city and submarine-cable hub. The arrival of the 2Africa system adds multi-terabit capacity and stimulates terrestrial backhaul demand, prompting coastal tower clusters for redundancy. Meanwhile, the Suez Canal Economic Zone attracts logistics and industrial tenants that need dedicated low-latency links, further expanding the Egypt telecom towers market.

Upper Egypt and rural governorates remain under-served. The government’s Decent Life initiative allocates EGP 9 billion (USD 290 million) to improve rural telecom access, including macro sites with solar-hybrid power kits scheduled for completion in mid-2025. Lower site rents and streamlined permitting partially offset weaker revenue per user, creating viable business cases for TowerCos employing standardized lattice designs and shared backhaul.

Red Sea tourism corridors represent niche but high-value pockets. Resorts prioritize uninterrupted coverage for international visitors, leading to build-transfer-lease agreements with TowerCos that integrate stealth poles into resort architecture. Subsea-cable landing points in Suez and Ras Ghareb also demand coastal towers that provide microwave redundancy to cable stations, reinforcing the geographic diversification of the Egypt telecom towers market

Competitive Landscape

Egypt’s tower sector is moderately concentrated. Four mobile operators still control the majority of passive assets, yet the entry of IHS Towers introduces a specialist with global economies of scale. The joint venture’s 80% stake and target of 5,800 towers grant it a springboard to raise tenancy ratios through co-location strategies, while the government’s 20% holding aligns national interests.

Telecom Egypt’s proposal to divest 2,500 towers for USD 200-250 million indicates a broader pivot toward infrastructure monetization. Independent TowerCos with access to hard-currency funding stand to benefit, as FX stability is critical when purchasing steel-intensive assets. Operators retain strategic focus on spectrum investments and customer experience, outsourcing passive infrastructure to unlock capital for active-layer enhancements such as Ericsson triple-band radios deployed by Vodafone Egypt in May 2025.

The tenancy ratio under 1.35x pressures TowerCos to innovate. Many now bundle power, edge computing cabinets, and IoT sensor hubs, improving marginal revenue per site. Regulatory mandates from the NTRA incentivize sharing in smart-city zones, further reinforcing co-location economics. However, permitting complexities in heritage districts still grant competitive advantage to firms with local stakeholder networks and in-house concealment capabilities. Overall, the Egypt telecom towers market rewards scale, FX resilience, and aesthetic engineering expertise.

Egypt Telecom Tower Industry Leaders

HOI-MEA TowerCo

IHS Towers

BenyaTower

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vodafone Egypt deployed Ericsson triple-band radios across its network to enhance 5G coverage and spectral efficiency.

- February 2025: Telecom Egypt and Orange Egypt signed EGP 15 billion (USD 484 million) service agreements covering fiber backhaul for more than 1,000 sites.

- January 2025: Orange Egypt introduced Wi-Fi calling at no extra cost, initially supporting iOS devices.

- December 2024: NAIA Developments partnered with Vodafone Egypt to deliver triple-play services in Ras Al-Hikma and New Sheikh Zayed projects.

Egypt Telecom Tower Market Report Scope

The telecommunication market is largely concerned with the operations and provision of infrastructure for transmitting data - voice, image, sound, text, and video. To expand its network and services, the telecommunication market relies on towers, which are used to mount telecommunication networking and power equipment.

The Report Covers Egypt Telecom Tower Companies and the Market is Segmented by Ownership (Operator-Owned, Private-Owned, MNO Captive Sites), by Installation (Rooftop, Ground-Based), by Fuel Type (Renewable, Non-Renewable). The Market Sizes and Forecasts are Provided in Terms of Installed Base (in Thousand Units ) for all the above Segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

How large will the Egypt telecom towers market be in 2031?

Forecasts indicate the Egypt telecom towers market will reach USD 278.35 million by 2031, expanding at a 2.39% CAGR from 2026.

Which ownership model is expanding fastest?

Independent TowerCos are projected to grow at 11.65% annually through 2031 as operators divest sites and regulators promote sharing.

Why are rooftop deployments gaining traction in Cairo?

Limited land availability and strict urban aesthetics make building-mounted antennas easier to permit and faster to deploy, driving 3.52% CAGR growth in rooftop towers.

What is driving interest in renewable-powered sites?

The 40% pound depreciation has lifted diesel costs, while Egypt’s 42% renewable energy target and abundant solar resources shorten payback periods on hybrid solar systems.

How does the tenancy ratio in Egypt compare with mature markets?

Egypt’s ratio sits below 1.35x versus more than 2.0x in mature markets, which constrains TowerCo cash flow and spurs efforts to attract additional tenants.

What regulatory steps encourage infrastructure sharing?

The NTRA now offers spectrum-fee rebates and streamlined licensing for multi-operator sites, especially in smart-city zones like the New Administrative Capital.

Page last updated on: