Brazil Telecom Tower Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

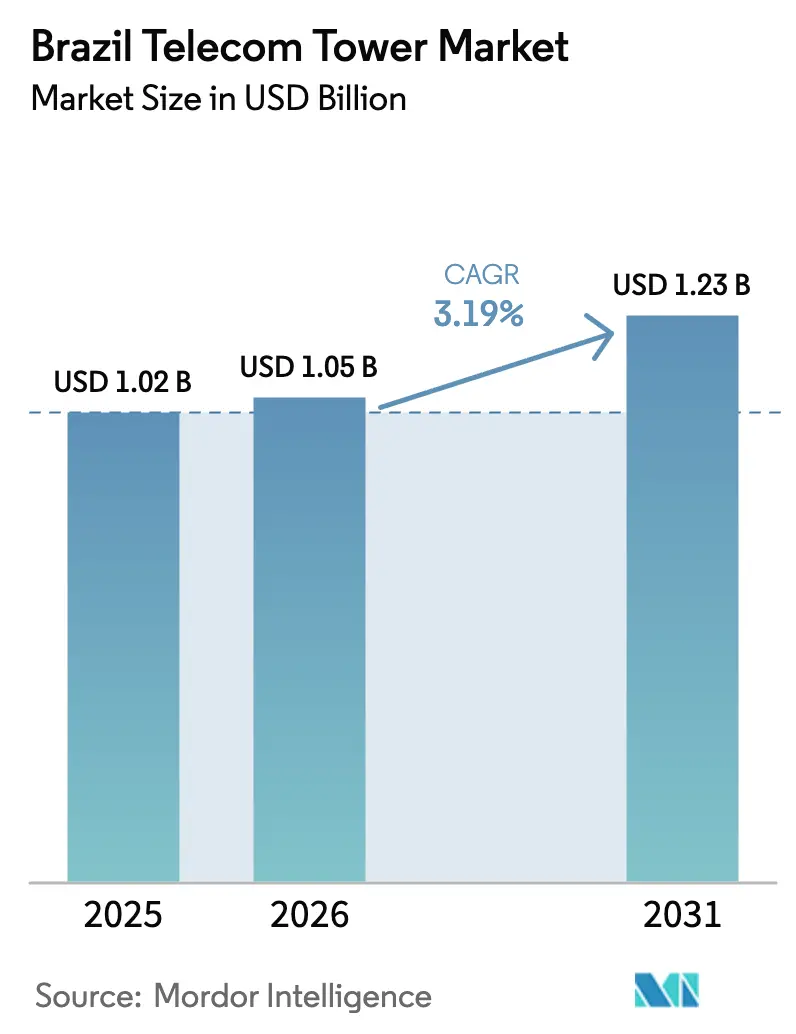

| Base Year Market Size (2025) | USD 1.02 Billion |

| Market Size (2026) | USD 1.05 Billion |

| Market Size (2031) | USD 1.23 Billion |

| Growth Rate (2026 - 2031) | 3.19% CAGR |

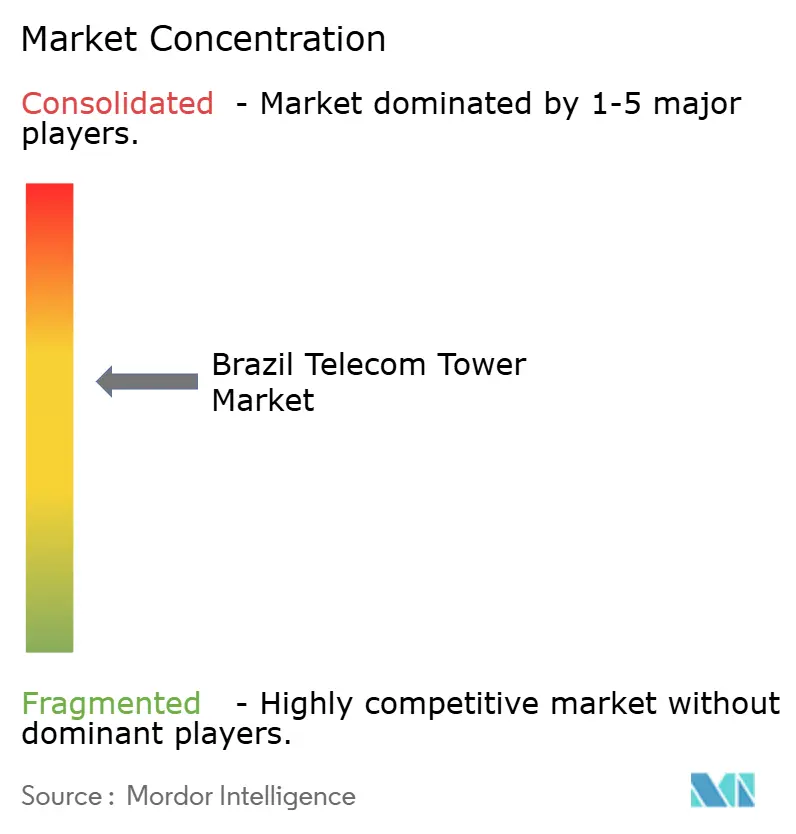

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Telecom Tower Market Analysis by Mordor Intelligence

Brazil Telecom Tower Market size in 2026 is estimated at USD 1.05 billion, growing from 2025 value of USD 1.02 billion with 2031 projections showing USD 1.23 billion, growing at 3.19% CAGR over 2026-2031.

Consolidation among independent tower companies, operators’ continued shift toward sale-leaseback arrangements, and ANATEL’s 5G coverage obligations together keep site-level tenancy demand resilient even as macro build activity normalizes. A gradual pivot from single-tenant to multi-tenant lease models is now the central driver of revenue expansion for tower owners because each incremental antenna requires marginal capex while lifting recurring tenancy income. Urban densification strategies, sustainable power mandates, and aesthetic regulations are prompting diversification toward rooftop structures, stealth poles, and hybrid solar-battery power plants, widening the solution set tower companies must master to secure new contracts. Independent TowerCos hold the financial capacity and permitting expertise to exploit these emerging opportunities, while operators focus scarce capital on radio networks and spectrum renewals. Persistent foreign-exchange volatility elevates the cost of imported steel and electronics, yet experienced multinationals continue to deploy hedging and inflation-linked contract escalators, allowing the Brazil telecom towers market to defend predictable long-term cash flows in real terms.

Key Report Takeaways

- By ownership, independent TowerCos led with 63.68% of Brazil telecom towers market share in 2025, while the same segment is projected to expand at a 5.03% CAGR through 2031.

- By installation type, ground-based towers accounted for 54.70% share of the Brazil telecom towers market size in 2025, whereas rooftop deployments record the highest forecast CAGR at 4.43% to 2031.

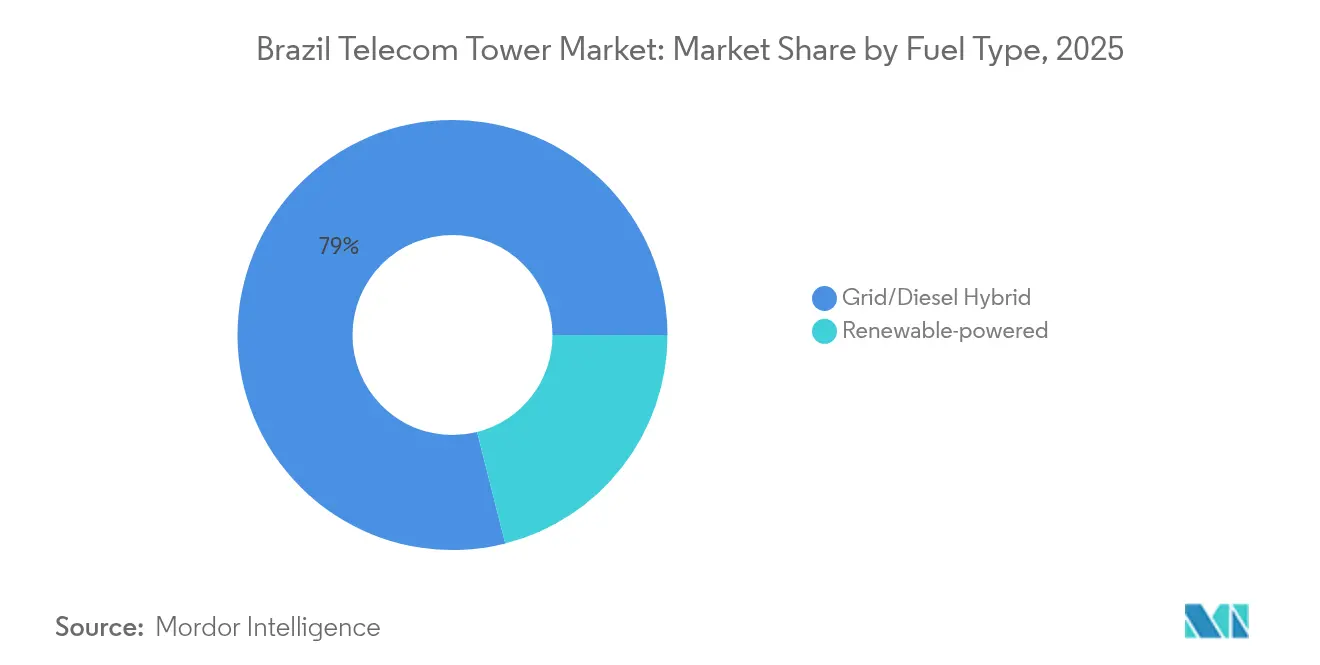

- By fuel type, grid/diesel hybrids captured 78.95% of Brazil telecom towers market share in 2025; renewable-powered solutions are advancing at an 17.9% CAGR during 2026-2031.

- By tower type, lattice designs commanded 21.12% of the Brazil telecom towers market size in 2025 and stealth/concealed structures are set to progress at the fastest 5.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Telecom Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G rollout obligations and spectrum milestones | +1.2% | National, concentrated in major metros | Medium term (2-4 years) |

| Operator sale-leaseback monetization wave | +0.8% | National, high-value urban assets | Short term (≤ 2 years) |

| FUST and Novo PAC subsidies for rural coverage | +0.6% | Rural, Amazon priority | Long term (≥ 4 years) |

| Surge in mobile video-streaming and IoT traffic | +0.7% | Urban centers, industrial corridors | Medium term (2-4 years) |

| Tower-fiber convergence via neutral fiber rings | +0.4% | Metropolitan areas | Long term (≥ 4 years) |

| Multi-operator active-sharing mandates | +0.3% | National, permit-constrained zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Rollout Obligations and Spectrum Milestones

ANATEL’s auction terms compel mobile network operators to reach 94.5% population coverage or risk spectrum forfeiture, anchoring demand for roughly 700,000 additional antennas across new and existing sites. [1]Gabriel Araujo, “Brazil telecom tower firms eye 5G rollout to spur deals,” REUTERS, reuters.comThe regulation transforms expansion into a non-discretionary expense, front-loading construction in São Paulo, Rio de Janeiro, and Belo Horizonte before rippling into tier-two cities and rural corridors. Predictable milestone calendars give TowerCos clear visibility into build-to-suit pipelines as operators pre-book locations to safeguard licenses. Multi-band 5G radios also raise loading on legacy structures, accelerating amendment-driven revenue from sector additions. Enforcement teeth—financial penalties and eventual reallocation of idle spectrum—reduce execution risk, allowing independent tower companies to finance capex with longer-tenor debt at competitive spreads.

Operator Sale-Leaseback Monetization Wave

Oi, TIM, and smaller regional carriers monetized more than USD 300 million of passive assets in 2024 alone, converting illiquid towers into 10- to 15-year leases that redirect proceeds to core network upgrades. The model expands acquisition targets for TowerCos and introduces sticky multiyear revenue under inflation-linked escalators. Sale-leasebacks typically bundle master service agreements that guarantee minimum new-colocation volumes, translating to low-risk internal growth. América Móvil’s USD 7.7 billion multi-year capital plan intensifies the need to recycle balance-sheet capital, indicating further divestiture pipelines. International owners leverage lower funding costs to outbid local rivals, deepening the Brazil telecom towers market penetration of large global players.

FUST and Novo PAC Subsidies for Rural Coverage

The federal Universal Service Fund shoulders up to 80% of capex for sites meeting connectivity criteria in Amazonia, the Northeast hinterland, and agribusiness corridors, effectively closing commercial gaps.[2]Agência Nacional de Telecomunicações, “Edital do 5G—Obrigações de Cobertura,” GOV.BR, gov.br Subsidy certainty unlocks towers that otherwise deliver sub-scale tenancy, while contractors familiar with environmental approvals for protected biomes gain an edge. Renewable micro-grids and satellite backhaul become standard engineering inclusions, raising average revenue per site even with fewer tenants. The long-term allocation of public capital insulates rural projects against election-cycle spending swings, ensuring recurring revenue well beyond the program’s present budget horizon.

Surge in Mobile Video-Streaming and IoT Traffic

Average smartphone data usage surpassed 12 GB per month in Brazil’s top cities during 2024, stretching spectral efficiency and prompting densification on existing footprints. Concurrently, agriculture, logistics, and smart-city deployments are adding millions of narrowband IoT devices that require broad coverage but low latency. These parallel traffic waves force operators to bolt additional sectors and massive-MIMO panels onto already-leased structures, delivering high-margin amendment rents to tower owners. Rising peak-hour congestion also validates rooftop micro-sites, sustaining the Brazil telecom towers market trajectory in districts where macro growth once appeared saturated.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented municipal permitting and environmental limits | -0.9% | National, acute in São Paulo | Short term (≤ 2 years) |

| FX volatility raising capex and lease uncertainty | -0.6% | National, international operators | Short term (≤ 2 years) |

| Coastal tourism zoning pushback on tower aesthetics | -0.2% | Coastal municipalities | Medium term (2-4 years) |

| Emerging LEO-satellite options in hinterlands | -0.3% | Remote Amazon basin | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Municipal Permitting and Environmental Limits

Brazil’s 5,500 municipalities apply disparate zoning, heritage, and height rules, extending São Paulo antenna approvals to as long as five years. Such fragmentation complicates project scheduling, inflates legal spend, and raises carrying costs for tower companies holding unused land options. Environmental studies for sites near protected water bodies trigger separate federal and state reviews, further elongating critical path timelines. Independent TowerCos with lean in-house legal teams are particularly exposed, often ceding projects to multinationals that can absorb prolonged negotiations. The uncertainty depresses near-term build counts and redistributes investment toward more permissive jurisdictions.

FX Volatility Raising Capex and Lease-Rate Uncertainty

The Brazilian real’s 22% depreciation in 2024 inflated imported steel, lithium-ion batteries, and RF electronics prices, eroding EBITDA margins on new builds. [3]Fernanda Camargo, “How currency turmoil hits tower economics,” BNPPARIBAS, group.bnpparibasAlthough lease contracts apply annual inflation adjustments, foreign parent companies must translate BRL cash flows into USD, exposing them to valuation swings. Hedging instruments mitigate part of the risk but add cost and are unavailable beyond five-year horizons. Operators also negotiate harder on rental escalators during currency stress, compressing the Brazil telecom towers market profitability spreads. Multinationals with balanced Latin American portfolios hedge naturally, yet smaller local peers face elevated cost of capital when FX turbulence raises risk premiums.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos Drive Consolidation

Independent TowerCos controlled 63.68% of Brazil telecom towers market share in 2025, and their stake is forecast to climb further because they are expanding at a 5.03% CAGR to 2031. The Brazil telecom towers market size attached to this segment is therefore poised to widen faster than overall industry revenue, underwritten by sale-leaseback inflows and multi-tenant leasing economics. Independent groups optimize asset utilization by onboarding two or three additional tenants without incurring the heavy structural reinforcement capex typical of single-operator portfolios. American Tower’s portfolio of 22,870 sites illustrates scale benefits, while Highline’s R$ 2.3 billion war-chest supports bolt-on deals that widen geographic density. The regulatory emphasis on infrastructure sharing further strengthens the independent model because operators face nondiscrimination clauses that compel them to accept co-location on divested sites. As a result, remaining operator-owned assets increasingly look like financial inefficiencies on carrier balance sheets, accelerating divestiture intent.

Momentum toward independence also arises from financiers’ preference for hard-asset cash-flow vehicles over spectrum-exposed MNO balance sheets. Project finance banks and infrastructure funds view long-dated master lease agreements as quasi-bond proxies, lowering funding costs for TowerCos and enabling aggressive bids. Meanwhile, joint-venture models-where an MNO retains a minority position-blend operational autonomy with anchor-tenant alignment. Strategic imperatives such as 5G densification, rural coverage subsidies, and renewable energy upgrades converge to magnify the capital demands most easily met by specialized TowerCos, solidifying the ownership transition well into the forecast horizon.

By Installation: Rooftop Deployments Accelerate Urban Densification

Ground-based structures retained 54.70% of Brazil telecom towers market size in 2025, yet rooftops are advancing at a 4.43% CAGR because dense metropolitan areas exhaust traditional ground options. Brazil telecom towers market share commanded by rooftops is expanding fastest in São Paulo’s south zone, Rio de Janeiro’s Barra da Tijuca, and Recife’s Boa Viagem, where community zoning boards favor less conspicuous antenna solutions. Rooftop sites require lower land rent, benefit from existing grid taps, and can often bypass the lengthy environmental reviews mandatory for new ground pads. The swap economics are compelling: a rooftop hosting fee averages 20–30% below a macro tower, but the condensed deployment timeline supports near-term 5G coverage KPIs, making operators willing to accept slightly higher OPEX to meet ANATEL service benchmarks.

Hybrid architecture emerges where a macro lattice feeds signal to adjacent rooftop repeaters, enhancing sector throughput without raising EIRP exposure over regulated thresholds. Building-owner negotiations constitute the principal bottleneck because freehold titles in Brazil can be fragmented across multiple heirs; experienced TowerCos deploy legal specialists to structure easements, adding a transaction-cost moat against new entrants. Municipalities simultaneously tighten visual-pollution codes, prompting demand for low-profile parapet-mounted antennas. Consequently, ground-based market supremacy persists in rural and peri-urban belts, but the trajectory tilts toward rooftops across most capital cities.

By Fuel Type: Renewable Energy Transition Accelerates

Grid/diesel hybrids accounted for 78.95% of Brazil telecom towers market share in 2025 as diesel gensets remained the de-facto resilience layer where grid reliability is erratic. Nevertheless, renewable-dominant systems will capture increasing portions of Brazil telecom towers market size because they are growing at 17.9% CAGR all the way to 2031. Solar PV panel prices have dropped below USD 0.20 per W, enabling rooftop solar arrays on shelters plus lithium-ion packs to achieve six-year paybacks compared with diesel. Regulatory frameworks permit net-metering in most states, giving TowerCos the option to feed surplus back into the grid, further diminishing lifecycle cost. In the Amazon region, where fuel logistics account for half the OPEX, hybrid solar-battery-diesel blends improve site uptime while slashing carbon emissions, aligning with multinational sustainability pledges.

Battery chemistry advances reduce footprint and thermal management expenses, making confined shelter retrofits more feasible. ANATEL weighs environmental criteria when allocating future spectrum, rewarding operators that commit to lower-carbon infrastructure. Renewable build-outs attract concessional financing from green-bond investors, shaving funding spreads by 50–75 basis points and compressing the overall WACC for forward-looking TowerCos. Resilience value also rises because solar-battery hybrids sustain service during prolonged grid outages, a non-trivial benefit given Brazil’s occasional storm-triggered blackouts.

By Tower Type: Stealth Solutions Address Aesthetic Concerns

Traditional lattice towers represented 21.12% of Brazil telecom towers market size in 2025 thanks to high equipment loading capacity, yet municipalities from Florianópolis to Fortaleza are tightening skyline codes that favor concealed or camouflaged poles. Stealth structures are forecast to achieve a market-leading 5.46% CAGR, gently siphoning Brazil telecom towers market share away from legacy lattice formats. Coastal tourist economies lobby for minimal visual intrusion, resulting in strict color-palette and height caps that lattice frames often breach. Concealed monopoles disguised as palm trees or flagpoles satisfy both regulators and hoteliers worried about property valuations.

Construction cost remains 15–25% higher than a bare lattice of equivalent height, yet TowerCos negotiate premium rents with carriers eager to secure right-of-way in high-ARPU districts. Guyed towers continue serving wind-prone, low-density locales where land is abundant and structural stress is elevated. Technological advances in fiberglass radomes, powder-coated steel, and integrated antenna shrouds decrease RF loss penalties once endemic to stealth designs, making them commercially viable across an expanding array of frequency bands-including 3.5 GHz 5G mid-band, which is most sensitive to environmental attenuation.

Geography Analysis

The Southeast and South corridors contain roughly 65% of all active sites, epitomized by São Paulo state contributing almost one-quarter of national inventory because of a population of 46 million and per-capita GDP 45% above the national mean. The Brazil telecom towers market therefore mirrors the spatial distribution of wealth, retail density, and corporate headquarters. Still, the highest incremental growth through 2031 will emanate from the Northeast and Center-West, buoyed by FUST-backed rural builds and agritech IoT connectivity in Mato Grosso’s soy belt. Fortaleza, Salvador, and Recife anchor new urban clusters where rooftop densification and neutral-host indoor systems are gaining prominence to satisfy soaring video-streaming demand during evening prime time.

The Amazon basin poses logistical challenges-long riverine supply lines, sparse roads, and fragile ecosystems-yet government subsidies combined with renewable micro-grid economics make selective tower deployment viable. Starlink’s 250,000 Brazilian subscribers crystallize competitive pressure, but ANATEL’s license terms still oblige terrestrial coverage, keeping the Brazil telecom towers market relevant even in remote Acre and Pará municipalities. Meanwhile, the South’s Rio Grande do Sul and Santa Catarina experience latency-critical manufacturing use cases that prefer terrestrial over satellite, fostering small-cell clusters inside industrial parks. Inter-regional fiber corridors complement tower builds, especially along BR-163 and BR-364 highways, ensuring robust backhaul for new 5G nodes.

Northeastern coastlines-rich in tourism receipts-are experimenting with town-planning schemes that reserve rooftop slots on historic buildings for shared concealed antennas, steering demand toward stealth micro-cell form factors. Conversely, Brasília’s federal district hosts capacity-driven multi-operator towers as ministries digitize citizen services. Population migration trends reinforce this geographic dispersion: IBGE reports net inflows into mid-size cities such as Goiânia and Campinas, triggering tower builds beyond legacy megacity cores. Taken together, regional growth vectors secure a balanced nationwide revenue base for investors in the Brazil telecom towers market across the approach to 2031.

Competitive Landscape

Market concentration hovers at moderate levels because the top four independent TowerCos hold roughly 60% of installed sites yet dozens of mid-tier contenders and residual operator portfolios fragment the remaining share. American Tower rules the field with 22,870 sites, deploying capital on distressed-asset purchases such as Oi’s small tower batch in late 2024 at attractive multiples. SBA Communications follows at 12,595 sites, leveraging its rooftop engineering know-how to score indoor subway DAS contracts. Sites Latinoamérica and IHS Towers round out the top tier, yet IHS seeks a USD 1.7 billion sale of its Brazilian arm, signaling capital rotation rather than retreat as infrastructure funds eye the stable cash flows on offer.

Scale confers bargaining power in land leases, equipment procurement, and financing, but regional specialists differentiate on permitting speed and municipal relationships. Brasil TecPar exemplifies roll-up ambition, completing 18 acquisitions in 2024 to surpass 820,000 fixed-broadband lines alongside its tower estate, proving convergence appeals to investors craving multi-utility platforms. Technology also frames competition: I-Systems pushes fiber rings that bundle tower access with 100 Gbps backhaul, creating sticky cross-product dependence among MNO clients. Environmental credentials constitute another battlefield; TowerCos integrating solar and lithium storage win favorable press and municipal goodwill when seeking new ground leases.

Price competition generally remains rational because site scarcity and long-term contracts limit churn. Still, auctions for sale-leaseback portfolios can tighten IRR spreads, evidenced by American Tower’s sub-12% levered returns on the latest Oi parcel. Operators judge partners on service delivery as much as on rent, penalizing owners who delay amendment work orders or fail SLA metrics. Consequently, quality of execution, renewable energy commitment, and engineering innovation emerge as decisive factors preserving or extending share within the Brazil telecom towers market.

Brazil Telecom Tower Industry Leaders

American Tower Brasil

SBA Communications Brasil

IHS Towers Brasil

Phoenix Tower International

QMC Telecom Brasil

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: IHS Brasil acquired assets from Oi’s isolated production unit amid the carrier’s restructuring.

- December 2024: Vrio’s Sky expanded fiber service to 400 cities by tapping neutral networks.

- December 2024: IHS Brazil completed 5G coverage at Campo Belo Station on São Paulo Metro Line 5-Lilac using distributed antenna systems.

- November 2024: American Tower Brazil purchased Oi telecom assets for R$ 41 million (USD 7.1 million).

Brazil Telecom Tower Market Report Scope

The telecommunication market is largely concerned with the operations and provision of infrastructure for transmitting data - voice, image, sound, text, and video. To expand its network and services, the telecommunication market relies on towers, which are used to mount telecommunication networking and power equipment.

The Report Covers Brazil Telecom Tower Companies and the Market is segmented by ownership (operator-owned, joint venture, private-owned, MNO captive sites), by installation (rooftop, ground-based), by fuel type (renewable, non-renewable), by type of tower (lattice towers, guyed towers, monopole towers, stealth towers). The market sizes and forecasts are provided in terms of installed base (in Thousand Units) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

How big is the Brazil telecom towers market in 2026?

The market stands at USD 1.05 billion in 2026, heading toward USD 1.23 billion by 2031 on a 3.19% CAGR.

Which ownership model leads tower deployment?

Independent TowerCos command 63.68% share and grow fastest at 5.03% CAGR as operators divest passive assets.

What installation format is expanding most quickly?

Rooftop sites post a 4.43% CAGR through 2031, driven by urban densification and easier permitting.

How are renewable systems affecting tower OPEX?

Solar-battery hybrids cut diesel use, and renewable-dominant towers are growing at an 17.9% CAGR, trimming long-term power costs.

What limits new tower construction in major cities?

Fragmented municipal permitting can stretch São Paulo approvals to five years, slowing near-term macro builds.

Who is the largest tower company in Brazil?

American Tower leads with roughly 22,870 active sites nationwide.

Page last updated on: