Mexico Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

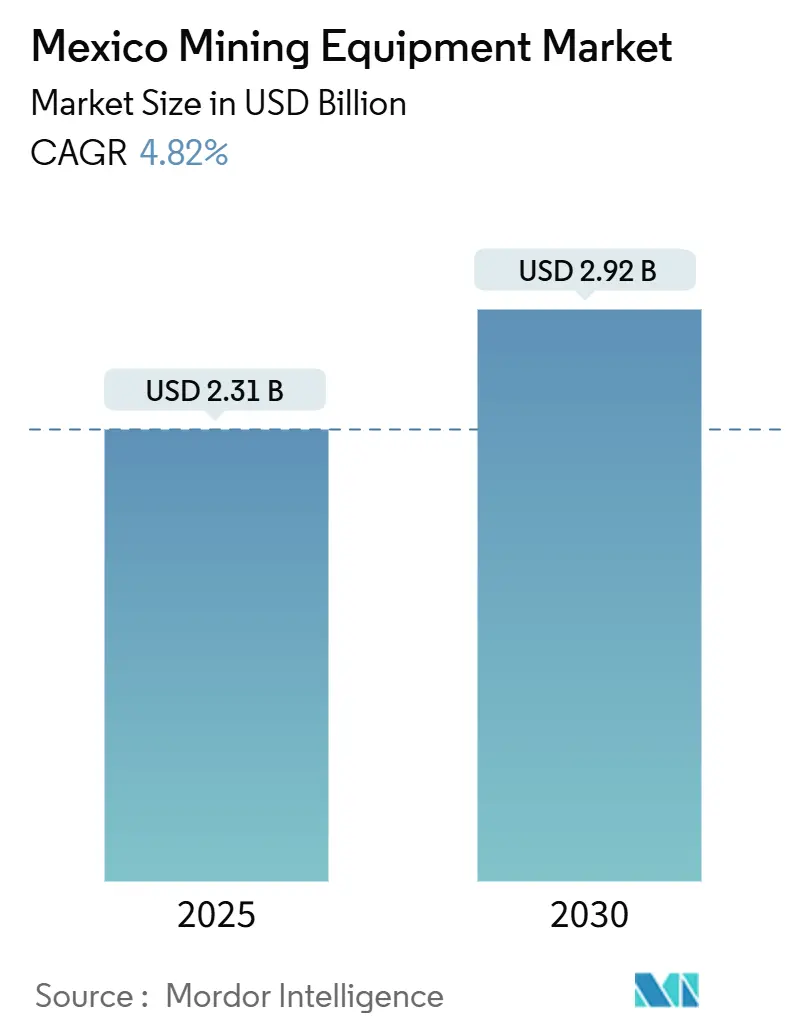

| Market Size (2025) | USD 2.31 Billion |

| Market Size (2030) | USD 2.92 Billion |

| Growth Rate (2025 - 2030) | 4.82% CAGR |

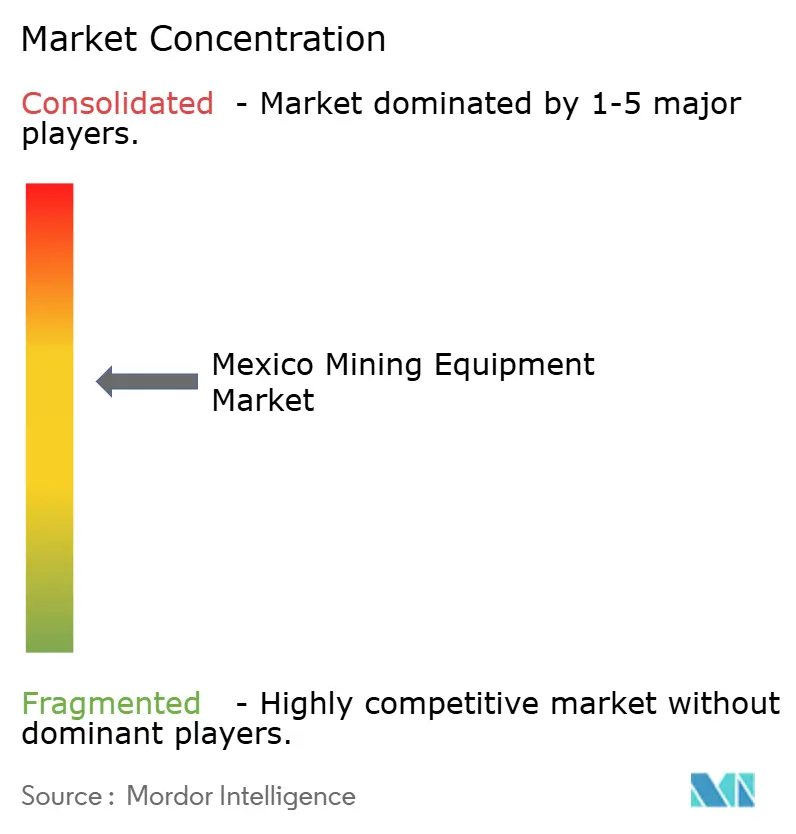

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Mining Equipment Market Analysis by Mordor Intelligence

The Mexico mining equipment market size is estimated at USD 2.31 billion in 2025 and is on track to expand to USD 2.92 billion by 2030, translating into a 4.82% CAGR over the period. Robust investment in copper projects, the first wave of clay-hosted lithium pilots and a generous accelerated-depreciation regime are propelling the Mexico mining equipment market, even as operators navigate regulatory change and security-related cost inflation. Uptake of battery-electric haulage, digital-twin service contracts and autonomous fleet modules is accelerating because these technologies boost uptime, cut diesel consumption and help firms satisfy tighter carbon-reporting rules. Currency volatility and intermittent grid curtailments create procurement headwinds, yet the Mexico mining equipment market continues to benefit from strong cross-border financing flows triggered by USMCA-aligned ESG funds. Competitive intensity remains moderate: global OEMs defend share through embedded service networks, while niche suppliers look to specialized lithium-extraction hardware as the next growth pocket.

Key Report Takeaways

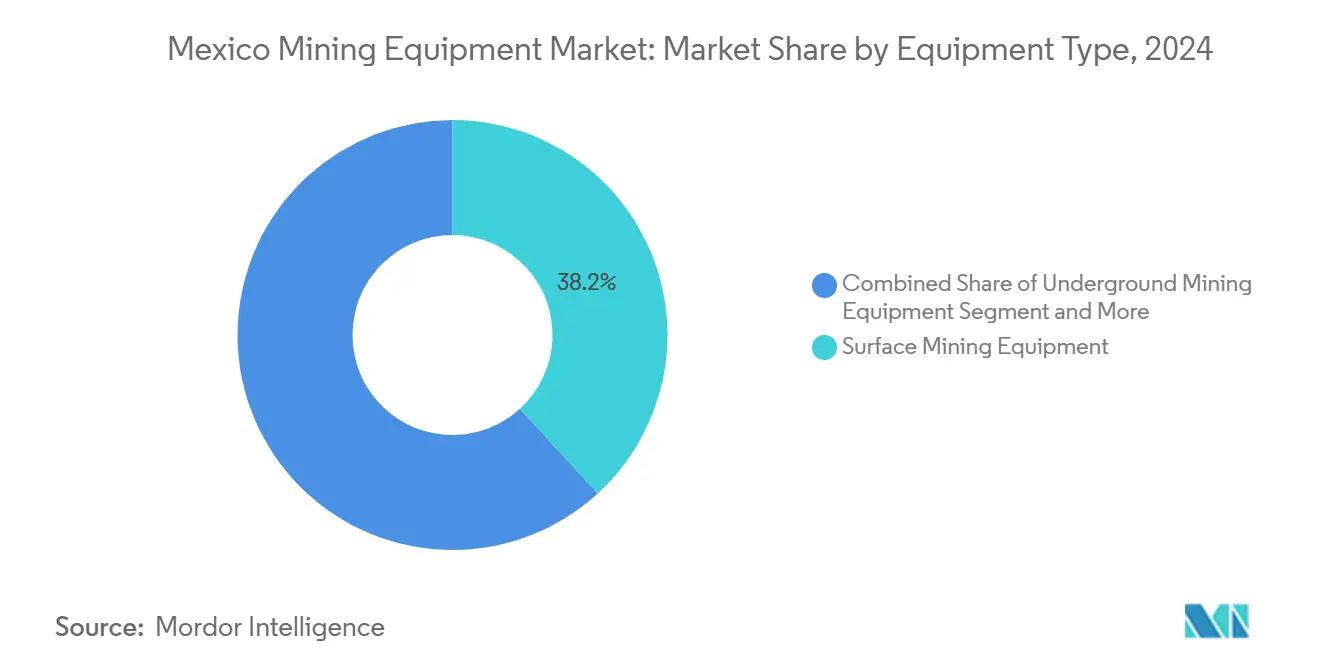

- By equipment type, Surface Mining Equipment captured 38.23% of Mexico mining equipment market share in 2024; Battery-Electric Loaders are forecast to achieve a 17.53% CAGR to 2030.

- By automation level, Manual Equipment retained 57.43% of the Mexico mining equipment market size in 2024, whereas Fully Autonomous systems are projected to climb at 22.06% CAGR through 2030.

- By powertrain, Internal-Combustion engines accounted for 82.15% of the Mexico mining equipment market size in 2024, while Battery-Electric vehicles will post a 24.01% CAGR during the same horizon.

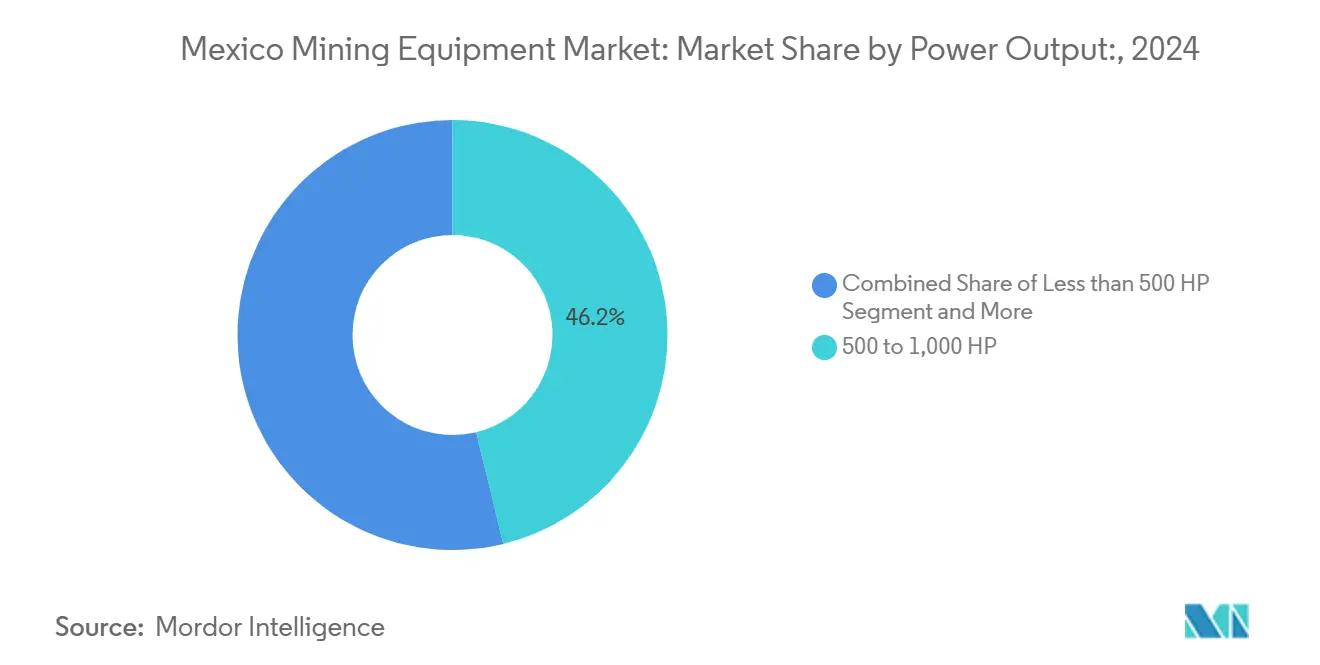

- By power output, the 500 to 1,000 HP range commanded 46.22% of Mexico mining equipment market share in 2024; equipment rated above 1,000 HP is expanding at a 13.09% CAGR.

- By application, Metal Mining held 52.37% of the Mexico mining equipment market size in 2024, and Lithium Mining is advancing at a 15.48% CAGR to 2030.

Mexico Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Open-Pit Copper Projects, esp. in Sonora | +1.2% | Sonora state, with spillover to Chihuahua | Medium term (2–4 years) |

| Expansion of Lithium Exploration and Pilot Extraction | +0.9% | Sonora clay deposits, potential Zacatecas expansion | Long term (≥ 4 years) |

| Federal Incentives for Low-Carbon Haulage Fleets | +0.8% | National, with concentration in major mining states | Short term (≤ 2 years) |

| Post-2024 Overhaul of Mining Royalty Regime | +0.6% | National regulatory framework | Medium term (2–4 years) |

| OEM Digital-Twin Service Contracts Boosting Uptime | +0.5% | Large-scale operations in Sonora, Zacatecas, Chihuahua | Short term (≤ 2 years) |

| Cross-Border Financing via USMCA-Aligned ESG Funds | +0.4% | Border states and major export-oriented operations | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in Open-Pit Copper Projects, Especially in Sonora

Sonora's copper belt transformation represents the most significant driver of Mexico's mining equipment demand, with Grupo México's multi-billion-dollar expansion program catalyzing regional equipment procurement. The Buenavista del Cobre operation, extending its life-of-mine plan to 2065, requires 5 to 14 electric rope shovels and 100 to 160 haul trucks annually, demonstrating the scale of equipment deployment[1]"SEC S-K 1300 Technical Report Summary," sec.gov.. Sonora's strategic advantage stems from established infrastructure and proximity to U.S. markets, with the state contributing over 20% of Mexico's mining output. The El Pilar project's 36,000 tons of annual copper cathode production and the Pilares project's 35,000 tons of copper concentrate further amplify equipment demand across surface mining, crushing, and processing categories. This concentration effect creates economies of scale for equipment suppliers while establishing Sonora as Mexico's primary mining equipment hub.

Expansion of Lithium Exploration and Pilot Extraction

Mexico's lithium development trajectory presents unique equipment challenges due to the predominance of clay-based deposits, requiring specialized extraction technologies distinct from traditional brine operations. The Bacanora lithium deposit in Sonora exhibits unusually high concentrations averaging 3,415 ppm, with some samples reaching 16,000 ppm, positioning Mexico as a potential major lithium producer[2]"Exclusive-Top Mexican geologist touts 'very good' Bacanora lithium deposit," Reuters, reuters.com.. However, commercial extraction from clay formations remains technically unproven, necessitating innovative processing equipment and pilot-scale testing facilities. The government's partnership with LitioMx and PEMEX to develop extraction capabilities, supported by CONAHCYT's research initiatives, indicates substantial future equipment demand for specialized lithium processing systems. This emerging segment requires different equipment profiles compared to traditional hard-rock mining, including advanced separation technologies and chemical processing systems.

Federal Incentives for Low-Carbon Haulage Fleets

Mexico's Plan México strategy fundamentally alters mining equipment economics through accelerated depreciation benefits ranging from 35%-91% for new fixed assets, creating compelling financial incentives for fleet modernization. The program's USD 1.5 billion budget allocation through September 2030 specifically targets training and innovation expenses with 25% additional deductions, encouraging adoption of advanced mining technologies. Caterpillar's Dynamic Energy Transfer system and Epiroc's battery-electric drill rigs exemplify the technologies benefiting from these incentives, as operators seek to reduce both operational costs and environmental impact. The Isthmus of Tehuantepec development poles offer additional benefits, including 100% income tax credits for six years, particularly relevant for equipment manufacturing and assembly operations. These incentives accelerate the transition from diesel-powered to electric and hybrid systems, fundamentally reshaping Mexico's mining equipment procurement patterns.

Post-2024 Overhaul of Mining Royalty Regime

The mining law reforms enacted in May 2023 create new operational frameworks that indirectly drive equipment demand through compliance requirements and operational adjustments. Mining concessions now require specific guarantees for environmental restoration and community engagement, necessitating enhanced monitoring and safety equipment. The reduction of concession terms from 50 to 30 years, coupled with mandatory public bidding processes, incentivizes operators to maximize extraction efficiency through advanced equipment deployment. Water usage reporting requirements and 60% recycling mandates drive demand for specialized water management and processing equipment. The requirement for indigenous community consultations and profit-sharing arrangements (minimum 5% of net profits) creates additional operational costs that operators seek to offset through productivity-enhancing equipment investments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Permitting Delays after 2023 Mining Law Reforms | -1.1% | National, with particular impact on new projects | Short term (≤ 2 years) |

| Intermittent Power-Grid Curtailments in Remote Sites | -0.7% | Remote mining regions in Sonora, Chihuahua, Guerrero | Medium term (2–4 years) |

| Rising Security Costs in Gold-Silver Belts | -0.6% | Guerrero, Sinaloa, Chihuahua gold-silver regions | Long term (≥ 4 years) |

| Peso Volatility vs. USD-Denominated Cap-Equipment | -0.4% | National impact on equipment procurement decisions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Permitting Delays After 2023 Mining Law Reforms

The comprehensive mining law overhaul has created significant administrative bottlenecks, with President Claudia Sheinbaum announcing no new mining concessions, further constraining project development. The transition from first-come-first-served to public bidding systems for concessions has introduced uncertainty and extended timelines for project approvals. Environmental impact assessments now require more comprehensive restoration plans and community consultation processes, adding 6-12 months to typical permitting cycles. Major projects like Torex Gold's Media Luna and Luca Mining's Tahuehueto have experienced delays extending into 2025, impacting equipment procurement schedules. The regulatory uncertainty has prompted some international investors to reassess their Mexico strategies, with the Fraser Institute ranking Mexico 74th out of 86 jurisdictions for investment attractiveness in 2023.

Rising Security Costs in Gold-Silver Belts

Criminal activities targeting Mexico's mining sector have escalated operational costs by 10%-20% industry-wide, with severe cases exceeding 20% increases. The theft of 7,000 ounces of gold from McEwen Mining's El Gallo mine exemplifies operators' security challenges [3]"Insecurity: Key Concern for Mining Companies," Mexico Business News, mexicobusiness.news.. Guerrero state has become particularly problematic, with social conflicts and cartel activities disrupting operations and deterring new investments. Some companies resort to paying protection money to criminal organizations, adding approximately 3% to mineral production costs. Establishing specialized mining police forces provides limited relief, as companies increasingly rely on private security services and enhanced surveillance equipment, diverting capital from productive equipment investments toward defensive measures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Operations Drive Market Leadership

Surface Mining Equipment's 38.23% market share in 2024 reflects Mexico's geological advantages and operational preferences, with open-pit operations accounting for 60% of national mining production value. The segment's dominance stems from Mexico's extensive copper and gold deposits that favor large-scale surface extraction methods, particularly in Sonora's established mining corridors. Battery-Electric Loaders emerge as the fastest-growing subsegment at 17.53% CAGR (2025-2030), driven by Caterpillar's Dynamic Energy Transfer system and similar electrification initiatives that reduce operational costs while meeting environmental compliance requirements. Underground Mining Equipment serves specialized applications in silver and polymetallic operations, particularly in Zacatecas and Chihuahua, while facing growth constraints from the proposed open-pit mining ban discussions.

Mineral Processing Equipment benefits from Mexico's strategic focus on value-added production, with Metso's new USD 51 million dewatering development hub in Irapuato exemplifying the sector's infrastructure investments. Drills and Breakers experience steady demand from exploration activities, though regulatory constraints on new concessions limit expansion potential. Crushing, Pulverizing, and Screening equipment aligns with Mexico's emphasis on domestic processing capabilities, supported by USMCA trade preferences that favor regional value chains. Loaders and Haul Trucks represent the largest equipment category by volume, with autonomous haulage systems gaining traction as operators seek to mitigate security risks in remote locations while improving operational efficiency through 24/7 operations capability.

By Automation Level: Manual Dominance Faces Autonomous Disruption

Manual Equipment's substantial 57.43% market share in 2024 reflects Mexico's cost-conscious operational approach and abundant skilled labor availability, particularly in established mining regions where traditional methods remain economically viable. However, Fully Autonomous systems' remarkable 22.06% CAGR (2025-2030) signals a fundamental shift driven by security concerns and operational efficiency imperatives. Epiroc's automated fleet of over 3,450 driverless machines globally, with significant growth in South American deployments, demonstrates the technology's maturation and acceptance. The company's Mexico order from Dumas Contracting for underground mining equipment includes safety-enhancing digital solutions and asset tracking capabilities, indicating growing sophistication in automation adoption.

Semi-Autonomous Equipment is a transitional category, allowing operators to implement automation while gradually maintaining human oversight for complex operations. The segment benefits from Mexico's pragmatic approach to technology adoption, where operators seek to balance efficiency gains with employment considerations. Mining companies increasingly view automation as essential for operations in high-risk security zones, where unmanned equipment reduces exposure to criminal activities. Integrating private LTE networks enhances autonomous system capabilities, enabling real-time monitoring and control from secure locations. Rio Tinto's reported 15% reduction in load and haul costs through autonomous trucks, combined with zero injury records, provides compelling evidence for Mexico's mining operators considering similar investments

By Powertrain Type: Electrification Accelerates Despite ICE Dominance

Internal-Combustion Engine vehicles maintain overwhelming market control at 82.15% share in 2024, reflecting Mexico's established infrastructure and lower initial capital requirements for traditional powertrains. However, Battery-Electric vehicles' exceptional 24.01% CAGR (2025-2030) represents the market's most dramatic transformation, driven by operational cost advantages and environmental compliance requirements. Sandvik's record battery-electric mining equipment order demonstrates growing market acceptance. In contrast, Epiroc's commitment to offer emission-free versions of all underground equipment by 2025 and surface equipment by 2030 indicates industry-wide electrification momentum. The SmartROC D65 battery-electric drill rig exemplifies the technology's evolution, offering zero-emission drilling capabilities that address environmental and operational efficiency concerns.

Hybrid Vehicles occupy a strategic middle position, providing operational flexibility while reducing fuel consumption and emissions compared to pure ICE systems. The segment appeals to operators seeking to transition gradually toward full electrification while maintaining operational reliability in remote locations with limited charging infrastructure. Mexico's Plan México incentives, offering 35%-91% accelerated depreciation for new assets, significantly improve the economic case for electric and hybrid equipment adoption. The mining industry's projection of 1 million electric vehicles by 2030 globally suggests substantial growth potential for Mexico's market, particularly as battery technology advances, reduces charging times, and extends operational ranges. Fortescue Metals' development of zero-emission electric haul trucks, part of a USD 6.2 billion decarbonization strategy, provides a roadmap for Mexico's major mining operators considering similar investments.

By Power Output: Mid-Range Dominance Supports Operational Flexibility

The 500 to 1,000 HP segment's 46.22% market share in 2024 reflects an optimal balance between operational capability and cost efficiency for Mexico's diverse mining applications. This power range accommodates most surface mining trucks, underground loaders, and processing equipment while maintaining reasonable fuel consumption and maintenance costs. The growth trajectory of above 1,000 HP equipment's 13.09% CAGR (2025-2030) aligns with Mexico's large-scale copper and gold operations, where massive haul trucks and draglines justify higher power requirements for productivity gains. Southern Copper's Buenavista operation, requiring 100-160 haul trucks annually, exemplifies the demand for high-power equipment in major mining complexes.

Less than 500 HP equipment serves specialized applications including exploration drilling, small-scale underground operations, and auxiliary support functions. The segment benefits from Mexico's diverse mining landscape, where smaller operations in silver and polymetallic deposits require appropriately sized equipment. The power output distribution reflects Mexico's mining industry maturity, with established operations favoring proven mid-range equipment while expansion projects drive demand for higher-power alternatives. Electrification trends particularly impact the higher power segments, where battery technology advances enable electric alternatives to traditional diesel powertrains. The integration of renewable energy sources at mining sites, with 38% of the sector's energy mix already from renewables, supports the economic viability of electric equipment across all power ranges.

By Application: Metal Mining Leadership Faces Lithium Challenge

Metal Mining's dominant 52.37% market share in 2024 reflects Mexico's position as a major copper, silver, and gold producer, with established operations driving consistent equipment demand across surface and underground applications. The segment benefits from Mexico's geological advantages and established infrastructure in states like Sonora, Zacatecas, and Chihuahua. Lithium Mining's remarkable 15.48% CAGR (2025-2030) emergence represents the market's most significant growth opportunity, driven by global electric vehicle demand and Mexico's substantial clay-based lithium resources. The Bacanora deposit's high-grade concentrations and government support for extraction technology development position lithium as a transformative application segment, though commercial viability remains under development.

Mineral Mining encompasses industrial minerals and construction materials, serving both domestic consumption and export markets. The segment benefits from Mexico's infrastructure development programs and USMCA trade preferences that favor regional suppliers. Coal Mining represents a declining application segment, constrained by environmental policies and Mexico's energy transition toward renewable sources. The application segmentation reflects Mexico's strategic positioning in critical minerals supply chains, with lithium and copper applications receiving priority support through federal incentives and regulatory frameworks. Developing specialized extraction technologies for clay-based lithium deposits requires different equipment profiles than traditional hard-rock mining, creating opportunities for innovative processing and separation equipment suppliers.

Geography Analysis

Sonora is the undisputed epicenter of the Mexico mining equipment market. Grupo México’s USD 15 billion multi-asset program, plus Clay-Lithium pilot clusters, propel Sonoran equipment outlays at a projected 6.2% CAGR to 2030. Its highway and rail links to the U.S. border compress logistics cycles for spare parts, and OEMs have responded by expanding service hubs in Hermosillo and Cananea.

Zacatecas ranks second as the nation’s top silver province. Orla Mining’s Camino Rojo produced 136,748 oz of gold in 2024, financing fresh orders for crushing circuits and high-capacity conveyors. OEMs like Metso have opened offices in the state’s mining cluster to provide rapid mill-liner change-outs and process-optimization audits.

Chihuahua contributes 20.7% of national output and has more than 160 active projects, anchoring a vibrant supplier base of roughly 130 firms. The state’s proximity to U.S. Interstate networks facilitates cross-border equipment leasing, a niche financing model gaining ground in the Mexico mining equipment market. While geologically endowed, Guerrero faces procurement disruption from security incidents; several operators have postponed autonomous-truck deployments until perimeter infrastructure improves. Collectively, these regional dynamics illustrate how geography shapes capital-spending cadence across the Mexico mining equipment market.

Competitive Landscape

The Mexico mining equipment market is moderately concentrated. Caterpillar, Komatsu, and Epiroc command the top tiers by leveraging life-cycle contracts, parts depots, and proprietary autonomy stacks. Caterpillar’s Dynamic Energy Transfer system, unveiled in 2024, lets haul trucks regenerate power on downhill hauls, cutting emissions and offering a strong economic story for high-altitude pits.

Epiroc’s driverless fleet, now topping 3,450 machines globally, is gaining ground in Mexican underground projects where security risks advocate for remote operation. Its digital-twin analytics reduce unplanned downtime by up to 20%, locking operators into multi-year subscription models and boosting the firm’s aftermarket share. Komatsu focuses on hybrid powertrains and open-platform autonomy, forging alliances with local distributors for faster parts turnaround.

White-space competition is intensifying around the lithium-processing kit, where startups specializing in clay-leach circuits could disrupt incumbents. Asian OEMs such as XCMG court price-sensitive mid-tier miners but face barriers tied to brand perception and parts availability. Sustainability performance has become a significant differentiator: Metso reports a 73% emissions reduction since 2019 and pledges net-zero by 2030, resonating with lenders that link borrowing costs to ESG scores. As service revenues rise toward 50% of total OEM turnover, relationship depth rather than unit price is becoming decisive in the Mexico mining equipment market.

Mexico Mining Equipment Industry Leaders

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Sandvik AB

-

Epiroc AB

-

Liebherr-International AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Orla Mining reported record gold production of 136,748 ounces in 2024, exceeding guidance and ending the year debt-free with USD 160.8 million cash position, supporting continued equipment investments at the Camino Rojo project.

- March 2024: Epiroc announced a large order in Mexico from Dumas Contracting Ltd. for underground mining equipment and related services valued at approximately SEK 200 million (USD 18 million), including safety-enhancing digital solutions and asset tracking capabilities.

Mexico Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills and Breakers |

| Crushing, Pulverizing and Screening |

| Others Equipment Type |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 to 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills and Breakers | |

| Crushing, Pulverizing and Screening | |

| Others Equipment Type | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 to 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining |

Key Questions Answered in the Report

How large is the Mexico mining equipment market in 2025?

The Mexico mining equipment market size stands at USD 2.31 billion in 2025 and is projected to reach USD 2.92 billion by 2030.

What is the expected growth rate for mining equipment in Mexico?

The overall CAGR for the Mexico mining equipment market is forecast at 4.82% between 2025 and 2030.

Which equipment segment leads demand in Mexico?

Surface Mining Equipment accounts for 38.23% of Mexico mining equipment market share, driven by large open-pit copper operations.

How fast are battery-electric units growing?

Battery-Electric vehicles are registering a 24.01% CAGR, the fastest among powertrain categories in the Mexico mining equipment market.

Which region buys the most mining equipment in Mexico?

Sonora leads regional demand thanks to extensive copper projects and emerging lithium pilots, with equipment spending forecast to grow at 6.2% CAGR.

What fiscal incentives support equipment modernization?

Plan Mexico allows accelerated depreciation of 35%–91% on new machinery and an extra 25% deduction for training and innovation through September 2030.

Page last updated on: