Morocco Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

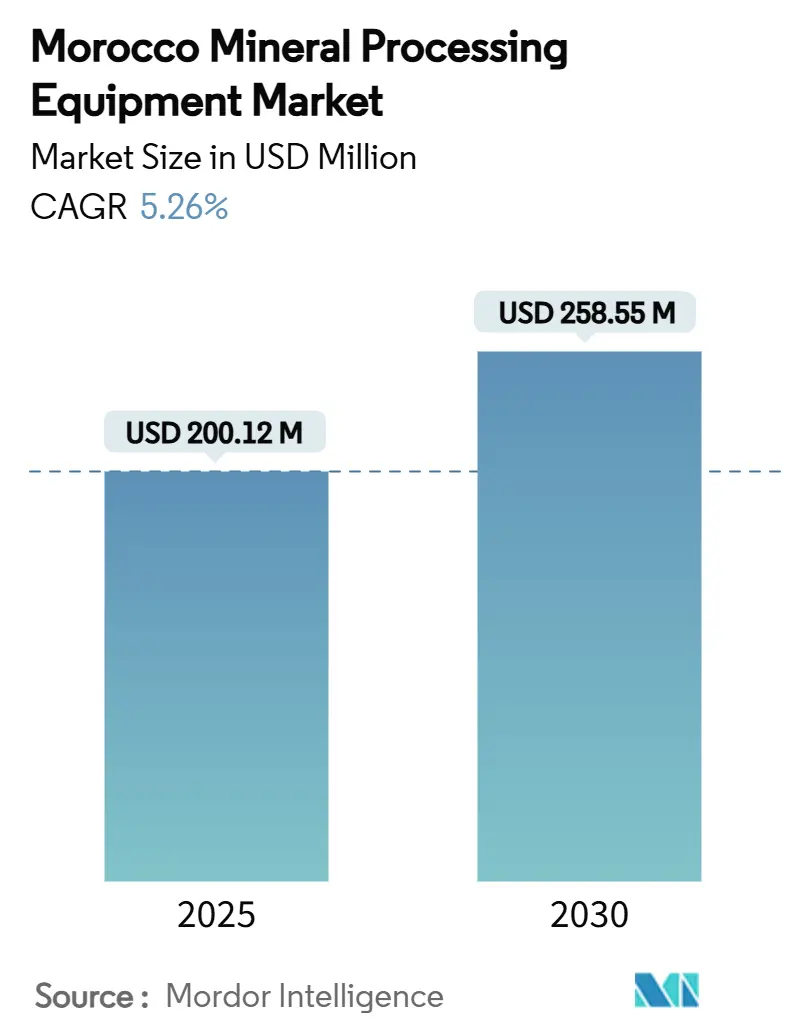

| Market Size (2025) | USD 200.12 Million |

| Market Size (2030) | USD 258.55 Million |

| Growth Rate (2025 - 2030) | 5.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco Mineral Processing Equipment Market Analysis by Mordor Intelligence

The Morocco mineral processing equipment market size stands at USD 200.12 million in 2025 and is projected to reach USD 258.55 million by 2030, delivering a 5.26% CAGR across the forecast horizon. Strong demand arises from Morocco’s status as the world’s largest phosphate producer, its growing battery-mineral ambitions, and a USD 13 billion green investment program that pushes operators toward modern, water-efficient plants. Replacement cycles at legacy beneficiation facilities, near-shoring incentives under the EU Critical Raw Materials Act, and government tax breaks for advanced machinery further anchor growth. Global suppliers respond by localizing service centers, while automation firms benefit from operators seeking tighter process control amid labor shortages. Capital spending remains sensitive to phosphate-price swings, yet the country’s free-trade pacts with the EU and the United States steady long-term investor confidence.

Key Report Takeaways

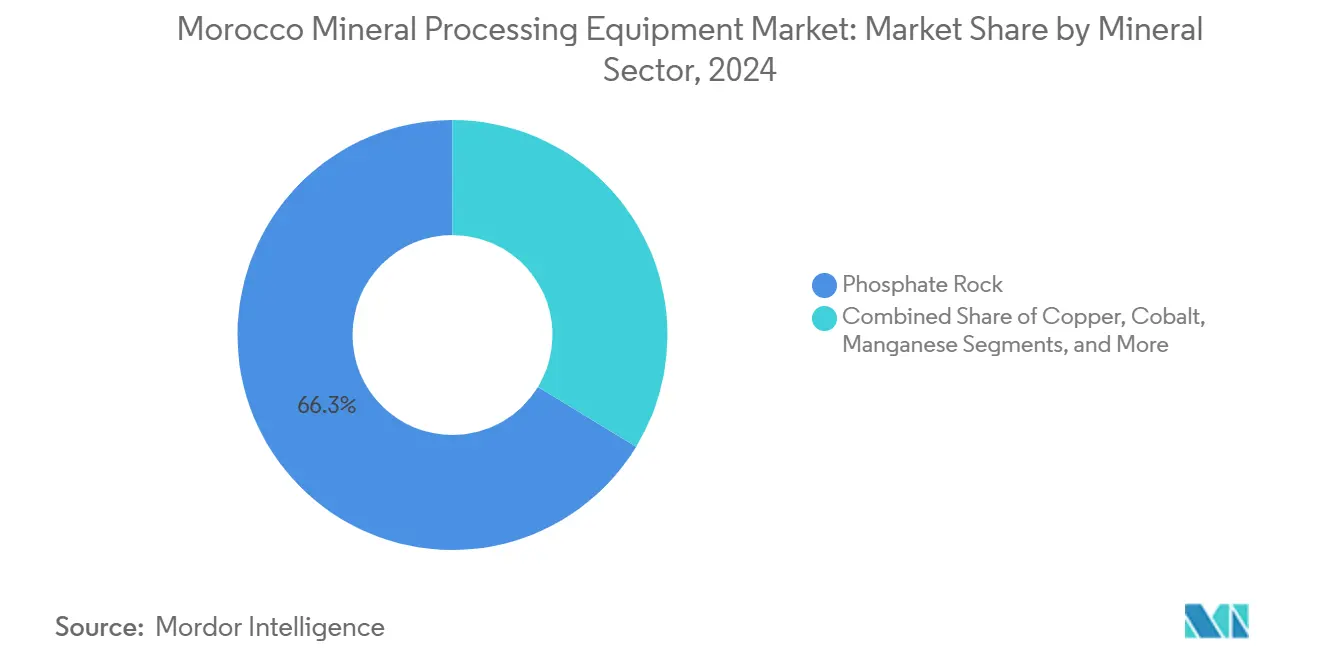

- By mineral sector, phosphate rock led with a 66.31% of the Moroccan mineral processing equipment market share in 2024, whereas cobalt processing is tracking the fastest 11.21% CAGR through 2030.

- By equipment type, crushers held 33.45% of the Moroccan mineral processing equipment market share in 2024, while flotation cells posted the quickest 10.85% CAGR toward 2030.

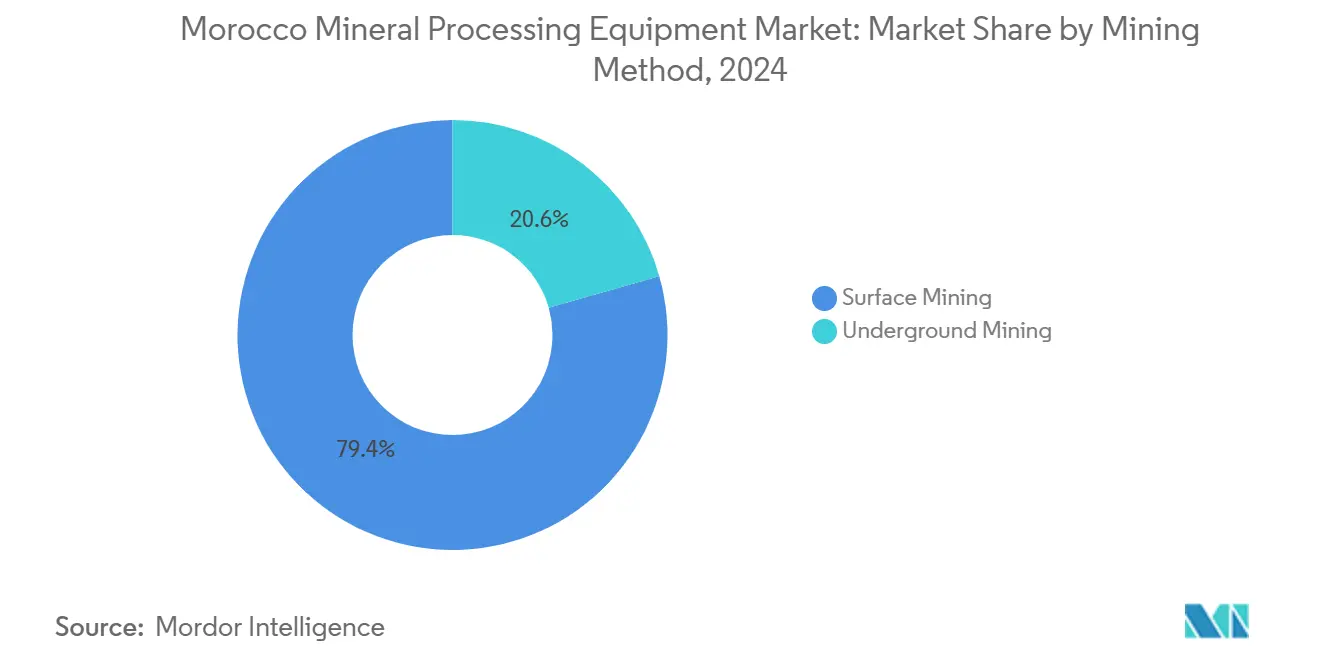

- By mining method, surface operations commanded 79.42% of the Moroccan mineral processing equipment market share in 2024, but underground projects advanced at an 11.65% CAGR on deeper ore development.

- By automation level, manual plants retained a 57.81% of the Moroccan mineral processing equipment market share in 2024, semi-automated lines expanded most rapidly at a 16.82% CAGR to 2030.

Competitive positioning in Morocco includes both locally based firms and those operating across multiple regions. The market landscape in the global mineral processing equipment industry research shows how these players are arranged internationally.

Morocco Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ramp-Up of Battery-Grade Cobalt and Manganese Refining | +1.5% | Tangier and Casablanca zones | Long term (≥ 4 years) |

| Surging Domestic Phosphate-Rock Output | +1.2% | Khouribga and Gantour basins | Medium term (2-4 years) |

| Upgrade Cycle of Legacy Beneficiation Plants | +0.9% | Existing OCP facilities | Short term (≤ 2 years) |

| Government-Backed Industrial Acceleration Plan 2028 | +0.8% | Casablanca-Settat and Tangier-Tetouan | Medium term (2-4 years) |

| EU Critical Raw Materials Act Prompting Near-Shoring | +0.6% | Nationwide with North-Africa spillover | Long term (≥ 4 years) |

| ESG-Driven Switch to Water-Efficient Flotation Reagents | +0.4% | Water-stressed districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ramp-up of Battery-Grade Cobalt and Manganese Refining Projects

Chinese and European investors have earmarked more than USD 2 billion for cathode-material complexes that require autoclaves, ion-exchange columns, and high-purity crystallizers. Managem’s Bou-Azzer mine supplies feedstock under a USD 100 million contract with BMW, and new hydrometallurgical trains must hit automobile-grade impurity thresholds. Suppliers with proven cobalt-purification flowsheets win early-mover advantage, while laboratory-scale analytical instruments see brisk demand for trace-element verification.

Surging Domestic Phosphate-Rock Output

Morocco’s goal to double phosphate-rock extraction by 2027 requires heavy investment in high-capacity crushers, screens, and conveyors able to handle surging tonnage. Ten mines with 47.5 million t output already feed roughly 33% of global supply, and the Benguerir expansion alone demands triple-capacity crushing circuits. Equipment suppliers that understand local ore abrasiveness gain an advantage, while OCP’s integrated fertilizer chain fuels follow-on orders for thickening, filtration, and chemical-processing units. The elevated throughput obliges robust condition-monitoring systems to avoid costly stoppages, driving uptake of semi-automated instrumentation.

Upgrade Cycle of Legacy Beneficiation Plants

Processing lines erected in the 1970s now need column flotation cells, high-pressure grinding rolls, and smart controllers to lift recovery and cut fresh-water draw. Retrofit bids often span complete flowsheet redesigns rather than single-unit swaps, favoring vendors able to deliver integrated packages. Environmental permits tie plant relicensing to lower emissions and saline discharge levels, accelerating replacement spend despite price volatility.

Government-Backed Industrial Acceleration Plan 2028

The Ministry of Industry’s framework accelerates mining-ecosystem creation through import-duty exemptions and expedited permits for advanced machinery [1]“Industrial Acceleration Plan 2028,” Ministère de l’Industrie et du Commerce, industrie.gov.ma. Priority clusters near Casablanca and Tangier lower logistics friction, encouraging overseas OEMs to assemble feeders, mills, and pumps locally. Tax holidays spur brownfield modernization, while new rules on minimum local content motivate joint ventures between global brands and Moroccan fabricators. Policy clarity keeps procurement pipelines visible, cushioning the sector from temporary commodity dips.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Expenditure Squeeze Amid Phosphate-Price Volatility | -1.1% | All mining basins | Short term (≤ 2 years) |

| Strict Discharge-Water Salinity Limits | -0.7% | Coastal operations | Short term (≤ 2 years) |

| Shortage of Sensor-Integration Skill Sets | -0.5% | Rural mining areas | Medium term (2-4 years) |

| Delayed Customs Clearance for Imported Spares | -0.3% | Major ports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Capital-Expenditure Squeeze Amid Phosphate-Price Volatility

Spot-price swings during 2024 cut cash flow at OCP and smaller operators, prompting maintenance-only spending phases [2]“Global Phosphate Price Trend Report,” U.S. Department of Commerce, commerce.gov. Equipment OEMs face elongated sales cycles and sharper price negotiations, although EU off-take contracts partly stabilize income streams. Suppliers diversify into service agreements to soften the revenue trough.

Strict Discharge-Water Salinity Limits

Tightened effluent norms oblige coastal concentrators to install reverse-osmosis and ion-exchange units that can add 5-10% to project capex. Compliance audits create scheduling risk for new‐builds, and retrofits must dovetail with seasonal water-table constraints. Vendors offering modular water-treatment skids have an edge, but smaller miners often postpone upgrades, slowing addressable demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Sector: Phosphate Dominance Drives Cobalt Emergence

Phosphate rock captured 66.31% of the Morocco mineral processing equipment market in 2024 because the country holds roughly 75% of global reserves and ships finished fertilizers worldwide [3]“Mineral Commodity Summary: Phosphate,” U.S. Geological Survey, usgs.gov. OCP’s multibillion-dollar expansion funnels steady orders for primary crushers, megawatt-class mills, and overland conveyors tailored to soft-sedimentary ores. In contrast, cobalt equipment demand although starting from a smaller base advances at an 11.21% CAGR through 2030 as battery supply chains seek diversified sourcing. The Morocco mineral processing equipment market size for cobalt lines is therefore expected to rise sharply as hydrometallurgical trains scale, while copper maintains a stable share thanks to the 120,000 t/y Tizert project and upgrades at Akka. Manganese and silver installations add marginal yet strategic volumes that diversify vendor pipelines.

Strategic implications extend beyond volume totals. Phosphate line expansions favor rugged, water-efficient scrubbers and high-capacity belt filters to handle slurried ore, whereas cobalt projects demand stainless autoclaves, impurity-stripping columns, and class 1 vacuum-pump packages. The Morocco mineral processing equipment market continues to bifurcate along these technical lines, rewarding suppliers that can field both bulk-handling and high-purity solutions. Policy incentives for downstream battery manufacturing further anchor cobalt and manganese opportunities, transforming Morocco from an exporter of concentrates into a producer of near-finished battery precursors.

By Equipment Type: Flotation Technology Transformation

Crushers dominated with 33.45% market share in 2024, mirroring vast open-pit phosphate tonnage requiring primary size reduction. Secondary grinding mills occupy the next-largest slot, especially as older rod-mill circuits convert to energy-saving SAG-ball combinations. Yet the fastest trajectory belongs to flotation cells, which register a 10.85% CAGR to 2030 as mines chase finer liberation and higher recovery. New column and pneumatic designs slash reagent burn and accommodate water-scarcity limits, supporting widespread retrofits across OCP’s estates.

Dewatering equipment also gains attention because every cubic meter of recycled process water reduces environmental capex. High-rate thickeners and paste filters become standard in new bids, nudging the Morocco mineral processing equipment market toward integrated water-balance solutions. Simultaneously, sensor-rich automation suites laser scanners for crusher chutes, online particle-size analyzers post-mill, and AI-driven froth cameras shift procurement conversations from standalone machines to smart-connected circuits. Suppliers that bundle digital twins with hardware secure margin uplift as operators quantify total-life cost savings.

By Mining Method: Surface Operations Drive Underground Growth

Surface pits represented 79.42% of 2024 revenue, a logical outcome of shallow phosphate seams worked by OCP’s Khouribga, Benguerir, and Youssoufia mines. Open pits order large mobile crushers, kilometer-length conveyors, and high-throughput screening stations designed for desert dust conditions. However, the fastest expansion occurs underground, rising at 11.65% CAGR, as deeper polymetallic ores come online. The Morocco mineral processing equipment market size for underground support packages from ore-passes and shaft hoists to load-haul-dump fleets therefore grows faster than the headline average, even if its absolute base remains modest.

Underground flowsheets tend to install more compact, enclosed crushers and fine grinding units to mitigate noise and ventilation loads. Ventilation-on-demand systems integrate with gas sensors, and shotcrete robots improve safety. As operators pursue deeper cobalt and precious-metal lodes, demand intensifies for high-strength drills, paste backfill plants, and robust dewatering pumps that combat hydrostatic pressures. Vendors skilled in remote-monitoring software benefit because underground visibility is restricted, amplifying the value of predictive analytics.

By Automation Level: Digital Transformation Accelerates

Manual plants still control 57.81% of 2024 throughput because many small or mid-tier operators rely on skilled labor and traditional instruments. Manual setups incur lower upfront expense but suffer from variable recovery and higher downtime. Semi-automated lines, however, post a 16.82% CAGR as miners retrofit PLC-based loop controls, SCADA dashboards, and low-cost sensor suites that strike a balance between capex and operational stability. Fully automated concentrators roll out mainly at greenfield cobalt and manganese sites where ROI models justify higher spend through reduced water-to-ore ratios and 24-hour steady-state operation.

The Morocco mineral processing equipment market is thus evolving in stages. Step one covers digitized instrumentation such as density gauges and air-flow meters. Step two involves closed-loop process control leveraging machine-learning algorithms. Step three adopts autonomous haulage and AI-driven scheduling that feed plant digital twins. Training gaps remain the key hurdle, so OEMs bundle e-learning modules and on-site mentoring, ensuring sustained after-sale revenue streams.

Geography Analysis

Regional demand patterns amplify Morocco’s dual stature as both an Atlantic export platform and a North-African mineral hub. Khouribga anchors roughly 70% of national phosphate throughput, creating the single largest cluster for crushers, mills, and high-capacity overland conveyors. The Morocco mineral processing equipment market size in Khouribga, therefore, outpaces other basins, especially because its ores require intensive washing that spurs filtration equipment purchases.

To the west, the Gantour basin encompassing Benguerir and Youssoufia mines represents the second-heaviest spender on beneficiation upgrades. OCP’s multi-stage expansion plan injects orders for advanced flotation cells and water-recycling plants designed to fit arid climate constraints. Pipeline corridors linking these sites with the Jorf Lasfar industrial port complex drive sustained demand for slurry pumps and pipeline-monitoring systems. The region’s logistics backbone shortens lead times for spare parts, encouraging OEMs to stock service hubs nearby.

The Tangier-Tetouan-Al Hoceima zone is rapidly becoming Morocco’s battery-chemicals corridor, benefiting from Chinese capital and fixed-link ferry routes to Spain. Hydrometallurgical cobalt and manganese converters require stainless agitators, impurity-removal ion-exchange columns, and clean-room grade dryers. Consequently, the Morocco mineral processing equipment market pivots toward smaller, high-precision units in this region. Southern provinces, notably Laayoune-Sakia El Hamra, host the Boucraa open-pit mine with its 102 km conveyor, demanding rugged bearings and remote-diagnostic lubrication skids for desert service. Government decentralization grants and renewable-energy incentives further seed equipment orders in these frontier zones. Coastal provinces prioritize corrosion-resistant alloys, interior basins emphasize dust-sealed motors, and northern battery hubs demand clean-chemistry compatibility. OEMs that segment their product portfolios accordingly secure higher customer stickiness and service-contract extensions.

Mordor Intelligence tracks the mineral processing equipment market with additional country-level coverage spanning Egypt, South Africa, Saudi Arabia, Australia, China, Canada, Germany, France, and Spain, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

International players such as FLSmidth, Metso, Weir Group, and Sandvik compete against emerging Chinese OEMs and regional workshops, producing a moderately fragmented seller base. No firm controls even one-quarter of supply, yet brand credibility and full-flowsheet expertise grant incumbents a pricing premium. Weir’s recent GBP 25 million order for Warman pumps and Cavex hydrocyclones at two OCP greenfield sites underscores the pull of bundled wear-parts and lifecycle services. FLSmidth’s acquisition of thyssenkrupp Mining widens its reference list, allowing turnkey bids that cover crushing through filtration.

Sustainability credentials increasingly separate finalists. Vendors able to demonstrate water-recovery ratios, carbon-intensity audits, and recyclable liner programs earn extra scoring in bid evaluations aligned with OCP’s 2040 carbon-neutral roadmap. Digitalization offers an additional wedge: Metso’s online particle-size sensors, Sandvik’s OptiMine fleet-monitoring suite, and Chinese OEMs’ AI-enabled grinding-media optimizers address Morocco’s shortage of skilled instrumentation staff. Local assembly plants in Casablanca free zones enable a duty-free status under rules-of-origin thresholds, leveling the field between Western and Asian brands.

Financial flexibility also frames competition. Suppliers willing to structure vendor financing or outcome-based service contracts mitigate buyer hesitation during phosphate-price troughs. Aftermarket presence remains critical because customs delays raise the value of in-country inventory. Consequently, the Morocco mineral processing equipment market rewards firms that combine technical breadth, ESG compliance, digital capability, and agile financing a blend few competitors master simultaneously.

Morocco Mineral Processing Equipment Industry Leaders

Metso Oyj

FLSmidth A/S

Sandvik AB

The Weir Group plc

Thyssenkrupp AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Morocco is set to unveil new mining tenders, presenting 328 blocks in the Eastern High Atlas and Tafilalet-Maider regions for lead and zinc exploration. The country's mining sector boasts an annual revenue exceeding USD 54 million.

- September 2024: Weir Group secured USD 33.5 million in process-equipment orders for OCP’s Benguerir and Louta phosphate projects, supplying Warman slurry pumps and Cavex hydrocyclones.

Morocco Mineral Processing Equipment Market Report Scope

| Phosphate Rock |

| Copper |

| Cobalt |

| Manganese |

| Precious Metals (Gold, Silver) |

| Others |

| Crushers |

| Mills and Grinders |

| Screens and Classifiers |

| Flotation Cells |

| Thickening and Dewatering Equipment |

| Conveyors and Feeders |

| Process Control and Automation Systems |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully-Automated |

| By Mineral Sector | Phosphate Rock |

| Copper | |

| Cobalt | |

| Manganese | |

| Precious Metals (Gold, Silver) | |

| Others | |

| By Equipment Type | Crushers |

| Mills and Grinders | |

| Screens and Classifiers | |

| Flotation Cells | |

| Thickening and Dewatering Equipment | |

| Conveyors and Feeders | |

| Process Control and Automation Systems | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully-Automated |

Key Questions Answered in the Report

What is the projected value of the Morocco mineral processing equipment market in 2030?

The market is forecast to reach USD 258.55 million by 2030.

Which mineral segment is set to grow fastest in Morocco by 2030?

Cobalt processing equipment is tracking an 11.21% CAGR, the quickest among all mineral segments.

How large is the crushers category inside Moroccan mineral processing?

Crushers commanded 33.45% of 2024 equipment revenue and continue to anchor bulk-handling spend.

Why are semi-automated systems gaining ground over manual plants?

Semi-automation boosts recovery, reduces downtime, and eases skilled-labor shortages, hence its 16.82% CAGR through 2030.

Page last updated on: