Spain Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

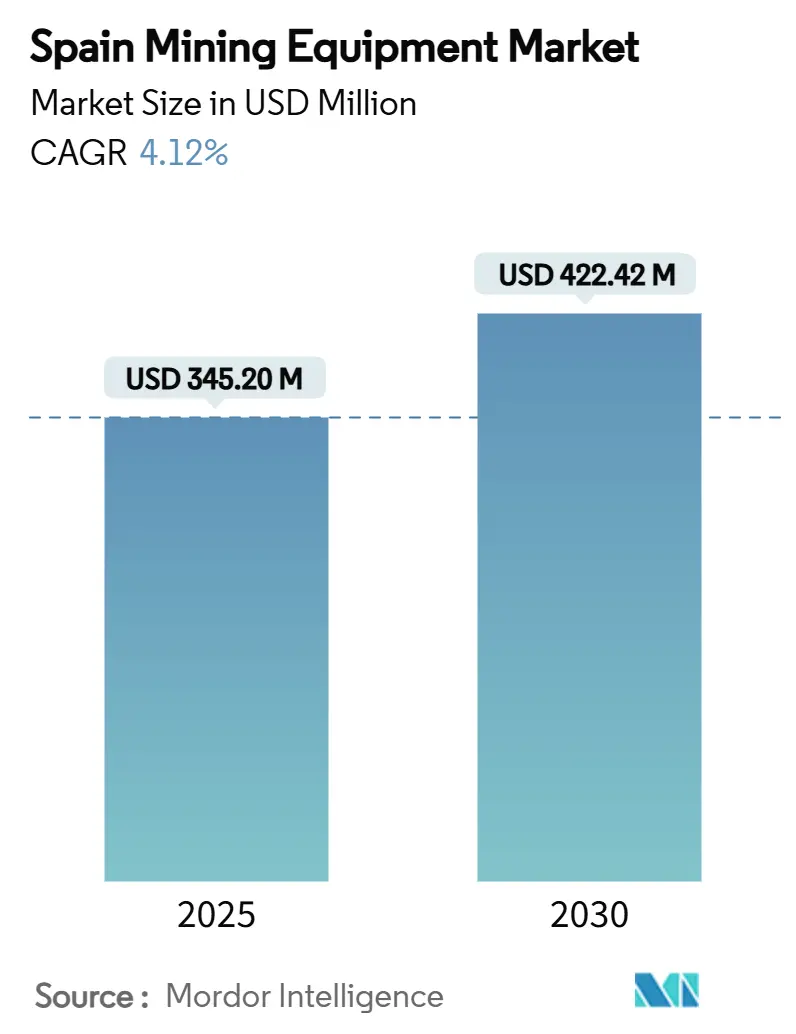

| Market Size (2025) | USD 345.20 Million |

| Market Size (2030) | USD 422.42 Million |

| Growth Rate (2025 - 2030) | 4.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Mining Equipment Market Analysis by Mordor Intelligence

The Spain mining equipment market size stood at USD 345.20 million in 2025 and is anticipated to touch USD 422.42 million by 2030, advancing at a 4.12% CAGR during the forecast period. Demand momentum stems from the European Union’s Critical Raw Materials Act, Spain’s large-scale open-pit projects in Andalusia and Extremadura, and accelerating electrification across heavy mobile machinery. Operators are scaling capital expenditure to unlock lithium, copper, tungsten, and rare-earth deposits that support EU energy-transition targets. Automation rollouts, performance-based maintenance contracts, and modular robotics pilots are simultaneously reshaping procurement criteria toward uptime guarantees, digital diagnostics, and remote-operation readiness. Suppliers offering energy-efficient, water-conserving technologies capture outsized opportunities as regional water-stress regulations tighten and permitting timelines lengthen.

Key Report Takeaways

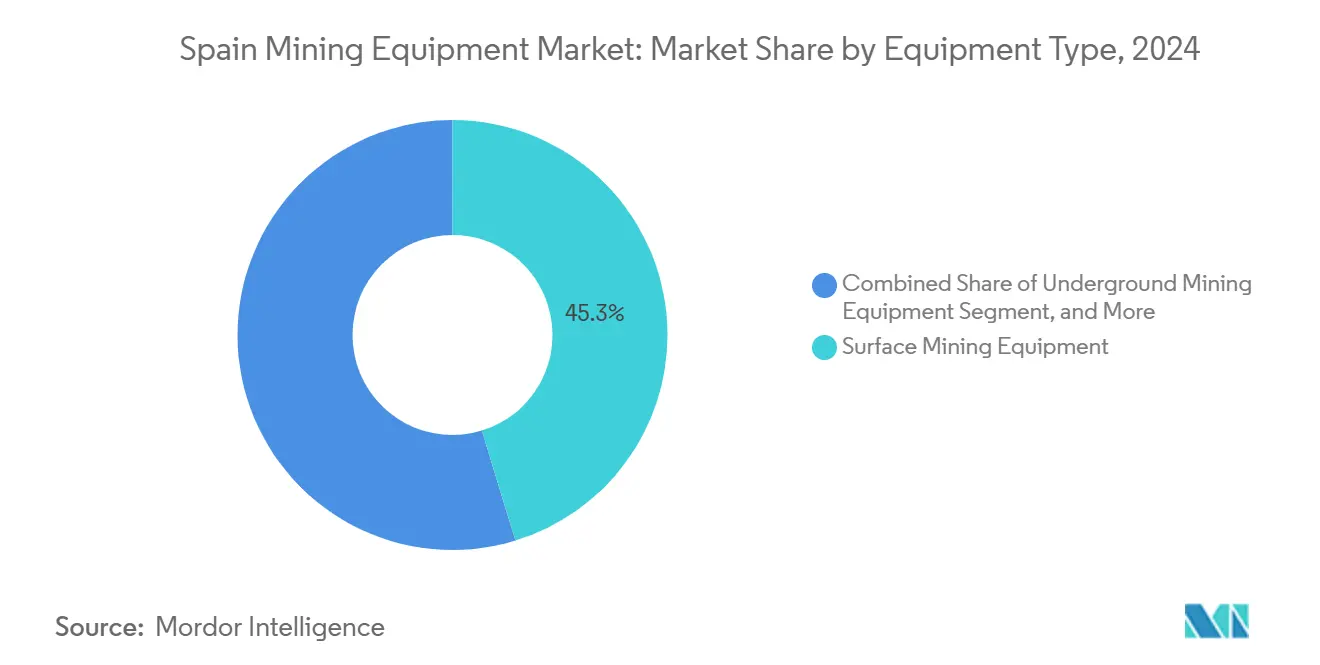

- By equipment type, surface mining systems led with 45.27% share of the spain mining equipment market in 2024; loaders and haul trucks are projected to expand at an 8.46% CAGR through 2030.

- By automation level, manual equipment retained 68.28% share of the spain mining equipment market in 2024, while fully autonomous systems recorded the highest projected CAGR at 9.43% to 2030.

- By powertrain, internal-combustion machines comprised 76.58% share of the spain mining equipment market in 2024; battery-electric variants are forecast to grow at a 9.28% CAGR over 2025-2030.

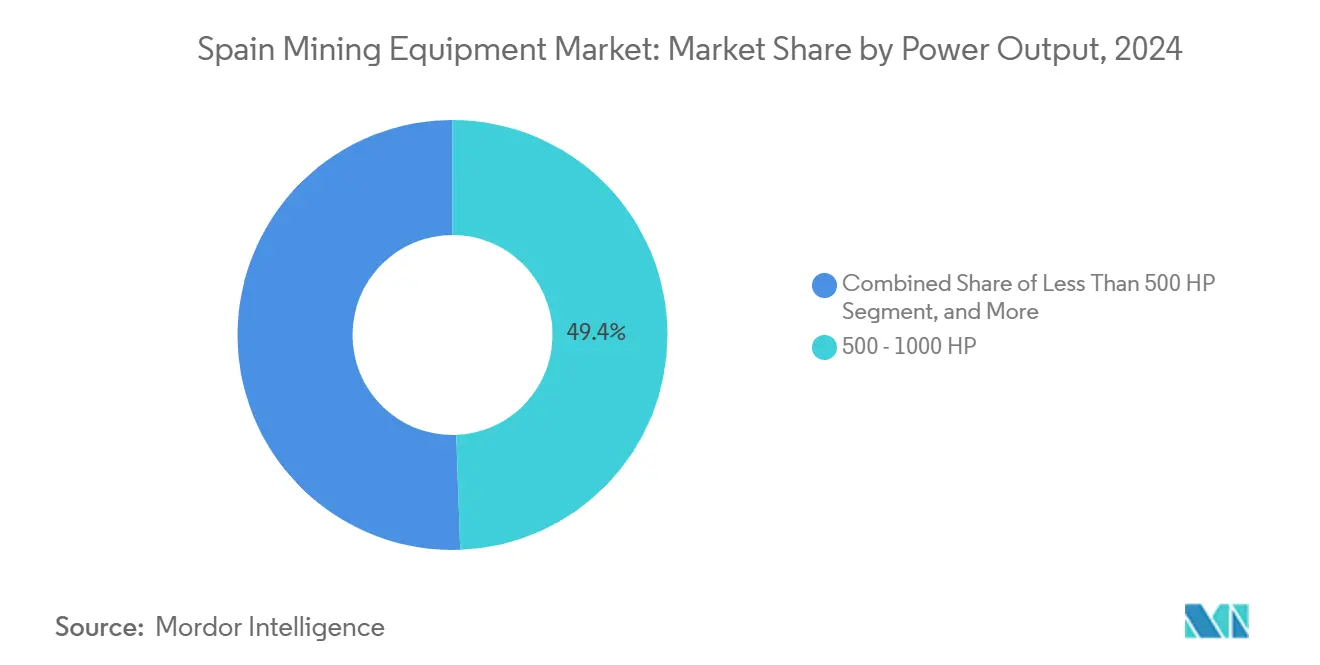

- By power output, the 500-1,000 HP class commanded 49.42% share of the spain mining equipment market in 2024, whereas units above 1,000 HP are advancing at a 7.37% CAGR through 2030.

- By application, metal mining accounted for a 46.75% share of the spain mining equipment market in 2024 and is moving forward at a 7.43% CAGR through 2030.

Spain Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Raw Materials Push | +1.8% | National, Andalusia, Extremadura, Galicia | Medium term (2-4 years) |

| Metals Boom | +1.5% | Extremadura, Castilla y León, Galicia | Long term (≥ 4 years) |

| Automation Demand | +1.2% | Major mining regions nationwide | Medium term (2-4 years) |

| Performance-Based Maintenance | +0.9% | Large mines nationwide | Medium term (2-4 years) |

| Low-Emission Incentives | +0.8% | National (MOVES III) | Short term (≤ 2 years) |

| Micro-Mine Robotics | +0.6% | EU-wide with Spanish sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Critical Raw Materials Push Revives Domestic Mining Investments

Spain’s elevation to strategic supplier status inside the EU has ignited spending on surface drills, haulage fleets, and on-site processing plants. Seven Spanish projects are now named “Strategic” under the Critical Raw Materials Act, a designation that cuts permitting lead times and channels EU capital toward equipment-intensive developments. Campo de Montiel and El Moto headline the pipeline, each demanding high-capacity excavators, 100-t trucks, and modular concentrators capable of rapid redeployment across adjacent deposits. Ministries have embedded geological mapping funds into the national budget, guiding investors to lithium-rich pegmatites and tungsten skarns that previously lay idle. The resulting alignment between EU autonomy targets and domestic economic policy has restored industry credibility, boosting lender appetite and compressing financing spreads for high-specification equipment acquisitions[1]“Critical Raw Materials Act – Strategic Projects List”, European Commission, ec.europa.eu.

Renewables-Led Metals Boom (Lithium, Copper, Tin) Expanding Equipment Demand

Rooftop-solar installs, grid-scale batteries, and offshore wind arrays lock in multi-decade demand for copper and lithium, funneling investment toward Spain’s Iberian Pyrite Belt and Valdeflores Valley. Contractors mobilize high-reach electric shovels and tier-4 compliant loaders to strip saprolite horizons above lithium pegmatites without breaching local particulate limits. New concentrators integrate dry-stack tailings and ore-sorting modules, curbing water use significantly—a decisive procurement attribute in drought-prone Andalusia. International Energy Agency scenarios projecting a tenfold spike in lithium by 2050 underpin forward contracts for advanced reels of medium-voltage cable and on-board inverter cabinets, stimulating the Spain mining equipment market[2]“Global Critical Minerals Outlook 2024”, International Energy Agency, iea.org.

Surge in Automation and Remote-Operation Demand to Improve Safety / Productivity

Significant concessions in Andalusia and Asturias now specify autonomous-ready equipment as a tender prerequisite to mitigate skilled-labor shortages and compliance incidents. Epiroc’s driverless drill rigs operating at El Valle-Boinás cut cycle times, freeing shift supervisors for higher-value tasks and lowering recordable injuries. Mines outfitted with AI-enabled fleet-management platforms are logging double-digit reductions in idle hours, translating into leaner fuel burn even before full electrification. Predictive-maintenance algorithms flag hydraulic anomalies days ahead of failure, anchoring performance-based service contracts. Remote-operation centers emerging in Seville and León extend labor pools while meeting new silica-dust exposure thresholds. These digital capabilities convert into faster ore release schedules and a measurable uplift in the Spain mining equipment market[3]“2024 Annual and Sustainability Report”, Epiroc AB, epirocgroup.com.

Performance-Based Maintenance Contracts Boosting Equipment Replacement Cycles

Fleet owners migrating to outcome-based service deals shift risk to OEMs. Epiroc’s aftermarket model bundles telematics, condition-monitoring, and parts logistics into five-year contracts that lock in predictable opex. Operators report an uplift in effective production hours and an accelerated retirement of legacy fleets that lack sensor infrastructure. Predictive analytics tied to vibration signatures allow component change-outs in planned stoppages, curbing unplanned downtime by half. This realignment of incentives steers capital toward new units designed around plug-and-play sub-assemblies, enlarging replacement volumes in the Spain mining equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Permitting And Opposition | -1.1% | Andalusia, Extremadura | Medium term (2-4 years) |

| Cap-Ex Inflation And Supply Chain | -0.9% | Global with regional exposure | Short term (≤ 2 years) |

| Skilled-Tech Shortage | -0.8% | Automated sites nationwide | Medium term (2-4 years) |

| Water Stress Limits | -0.7% | Andalusia, Extremadura | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy Permitting and Strong Local Environmental Opposition

Complex multi-tier authorizations and vocal activist groups delay project timelines, extending supplier lead-times and elevating inventory-carry costs. The Boliden spill legacy still shapes public sentiment, driving rigorous baseline studies and multi-agency reviews. Municipal councils wield discretionary powers that can override national approvals, prompting miners to run protracted community-engagement campaigns before equipment orders gain board sign-off. Suppliers respond by staging long-lead components—such as mill shells and shovel car-bodies—in European hubs to compress delivery once permits clear. Even with recent Critical Raw Materials Act fast-track provisions, procedural appeals remain frequent, tempering immediate upside for the Spain mining equipment market.

Cap-Ex Inflation & Component Supply-Chain Disruption Post-COVID

Port congestion, microcontroller shortages, and volatile freight rates inflate delivered equipment pricing by double digits compared with pre-pandemic averages. Spanish operators delay high-horsepower truck purchases or opt for phased fleet rollouts to hedge cost risk. OEMs localize wear parts and truck bed fabrication to Zaragoza and Bilbao, shortening transit routes and adding resilience. Despite mitigation, fluctuating steel premiums and energy tariffs compress supplier margins, slowing replacement cycles that feed the Spain mining equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Dominance Aligns with Open-Pit Strategy

Surface mining equipment captured 45.27% of the spain mining equipment market in 2024 as operators exploited shallow orebodies across Andalusia and Extremadura. This segment’s ascendancy mirrors investor preference for short construction lead times and lower ventilation overheads relative to deep-underground mines. Loaders and haul trucks will post the fastest 8.46% CAGR on the back of stripping requirements at new lithium deposits, reinforcing revenue visibility for the Spanish mining equipment market size at the segment level. Underground rigs, while smaller in share, remain indispensable at El Valle-Boinás and Cobre Las Cruces, where narrow-vein geometries necessitate twin-boom jumbos with advanced automation packages.

Processing lines involving cone crushers, high-pressure grinding rolls, and flotation cells pivot toward finer grind targets needed for battery-grade chemicals, boosting aftermarket parts turnover. Drill-and-blast operations stay resilient, with exploration campaigns around Galicia’s pegmatites sustaining order books for down-the-hole hammers and core-logging consumables. Suppliers integrating energy-recapture technologies and hybrid drives differentiate within the Spain mining equipment market.

By Automation Level: Gradual Shift from Manual to Autonomous

Manual fleets still dominate 68.28% of the spain mining equipment market in 2024, reflecting legacy assets and caution toward upfront capex. However, safety legislation now requires collision avoidance, nudging operators toward semi-autonomous retrofits. Mines employing tele-remote LHDs in Asturias report significant productivity gains without workforce reductions, underpinning the incremental move up the autonomy curve within the spain mining equipment market.

Fully autonomous haulage will rise 9.43% CAGR through 2030, accelerated by EU subsidies for digital transformation and the proven uptime of driverless fleets in Australian iron ore basins. Spanish case studies demonstrate cycle-time consistency and reduced tire wear, uplifting NPV for expansion pits. OEMs leverage subscription-based software licenses, smoothing revenue streams tied to data analytics rather than hardware alone.

By Powertrain Type: ICE Leads as Battery-Electric Accelerates

Internal combustion equipment held 76.58% of the spain mining equipment market in 2024 due to entrenched refueling infrastructure and multi-shift duty cycles. Yet battery-electric trucks are tipping total-cost-of-ownership parity by 2027. MOVES III grants and corporate decarbonization pledges catalyze a 9.28% CAGR for electric units, boosting the Spanish mining equipment market size when coupled with depot-charging EPC packages.

In remote sites, hybrid bridge constraints grapple with limited grid access, posing significant challenges for operations. However, by integrating regenerative braking systems and small diesel generators, operators can effectively extend their range while reducing particulate emissions, contributing to improved environmental performance.

Recognizing the growing demand for sustainable solutions, suppliers in Spain's mining equipment market are taking proactive measures by offering bundled lifecycle-carbon accounting dashboards. These dashboards provide clients with detailed insights into their carbon footprint, enabling them to meet stringent environmental standards and qualify for green-finance instruments. This approach supports clients in achieving their sustainability goals and strengthens the suppliers' competitive edge, creating a robust market position in an increasingly eco-conscious industry.

By Power Output: Mid-Range Rules but High-Power Grows on Scale

Units rated 500-1,000 HP satisfy most bench-height and payload scenarios, accounting for 49.42% of the spain mining equipment market in 2024. Nonetheless, super-pits at Cobre Las Cruces and Abenójar migrate toward above 1,000 HP electric drive trucks to cut fleet size. This segment’s 7.37% CAGR raises drivetrain and tire-supply complexities yet unlocks economies of scale, magnifying aftermarket parts volume for the Spain mining equipment market share narrative.

Equipment under 500 HP is pivotal in exploration, decline development, and narrow-vein selective mining. These machines are essential for operations requiring precision and efficiency in confined spaces. Demand for this equipment is closely tied to drilling meters and prospecting budgets, as mining companies prioritize cost-effective and reliable solutions.

OEMs increasingly offer modular engine upgrades and predictive-maintenance analytics as optional packages to safeguard their margins and remain competitive. These features enhance equipment performance and help reduce downtime and operational costs, making them attractive to end-users in the mining industry.

By Application: Metal Mining Captures Critical-Mineral Upside

Metal mining applications contributed 46.75% of the spain mining equipment market in 2024, thanks to copper and zinc at Riotinto and silver-rich polymetallic feeds at La Romana. Spain's mining equipment market share in metals benefits from EU sourcing mandates that favor domestic suppliers over extra-EU imports. Mineral mining, including lithium and rare earths, will outpace at a 7.43% CAGR as green-tech demand multiplies through 2030.

Coal extraction dwindles to a single-digit share after Spain’s last thermal plants exit baseload, though rehabilitation works use dozers and water trucks, sustaining niche demand. Non-metallic aggregates cycle with construction output, offering a steady baseload for the revenues of Spain's mining equipment market segment.

Geography Analysis

Andalusia anchors most of Spain’s metal output and posted major turnover in 2024, underwriting the most significant regional slice of equipment orders. Cobre Las Cruces’ planned underground expansion for high-capacity conveyors, battery-electric loaders, and deep-well dewatering pumps. Junta-mandated water quotas press operators to adopt dry-stack filters and electric dust-suppression sprayers, opening niches for vendors specializing in low-water circuits.

Extremadura follows lithium, tungsten, and rare-earth metals. El Moto tungsten targets most of Europe’s supply, ordering high-pressure grinders and gravity spirals from European OEMs. Regional SMEs leverage EU Just Transition funds to co-finance modern fleets, expanding the Spanish mining equipment market footprint.

Northern provinces, Galicia, Asturias, and Castilla y Leon, offer skilled labor and port proximity for equipment imports. Epiroc’s Boomer rigs reduced drilling rounds by 40 minutes at El Valle-Boinás, highlighting the productivity upside when advanced automation meets competent crews. Ports of Vigo and Gijón expedite inbound heavy-lift modules, shortening project ramp-up times compared with Mediterranean gateways.

Competitive Landscape

Global majors dominate strategic contracts yet rely on Spanish dealers for localized service. Caterpillar’s CES-shown retrofit hybrids meet MOVES III criteria, lining up unit sales and 10-year parts annuities. Epiroc’s services arm generates most of its global revenue via outcome-based agreements guarantee uptime, a model rapidly replicating in Spain. Komatsu invests in a Granada-based component rebuild center to shrink turnaround time.

Differentiation pivots on electrification, digital twins, and water-smart technology. ABB and Hitachi Construction Machinery co-develop 220-t battery dump trucks with pantograph-assisted fast-charge, clinching pre-orders from Andalusian copper mines. Niche robotics startups arising from EU research grants widen innovation bandwidth, but consolidation is likely once prototypes are commercialized, shaping the future structure of the Spain mining equipment market.

Spain Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Liebherr-Group

Sandvik AB

Epiroc AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Spain, with an added budget of EUR 400 million, has extended the MOVES III initiative until December 2025, promoting the use of low-emission heavy machinery.

- March 2025: The European Commission approved seven Spanish mining projects under the Critical Raw Materials Act, unlocking streamlined permits for equipment mobilization.

- December 2024: Cadence Minerals took a 40% stake in Pompeya Tungsten, signaling an anticipated rise in demand for drill rigs and crushers. This acquisition underscores the growing importance of tungsten in industrial applications and strengthens Cadence Minerals' market position.

Spain Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills & Breakers |

| Crushing, Pulverizing & Screening |

| Loaders & Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 - 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills & Breakers | |

| Crushing, Pulverizing & Screening | |

| Loaders & Haul Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 - 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining |

Key Questions Answered in the Report

What is the current size of Spain's mining equipment market in 2025?

It stands at USD 345.20 million, with a 4.12% CAGR projected through 2030.

Which Spanish region drives the largest share of mining equipment spending?

Andalusia accounts for major share of national metal output, making it the primary buyer of heavy machinery.

What incentives support electrification of heavy mining machinery in Spain?

The MOVES III program offers EUR 400 million in subsidies plus a 15% tax deduction on qualifying electric equipment.

Which equipment type holds the top revenue share in Spain’s mining sector?

Surface mining systems lead with 45.27% of the Spain mining equipment revenue in 2024.

How are performance-based maintenance contracts affecting procurement cycles?

Guaranteed uptime clauses shorten replacement intervals and shift risk to OEMs, accelerating new-equipment purchases.

Page last updated on: