South Africa Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

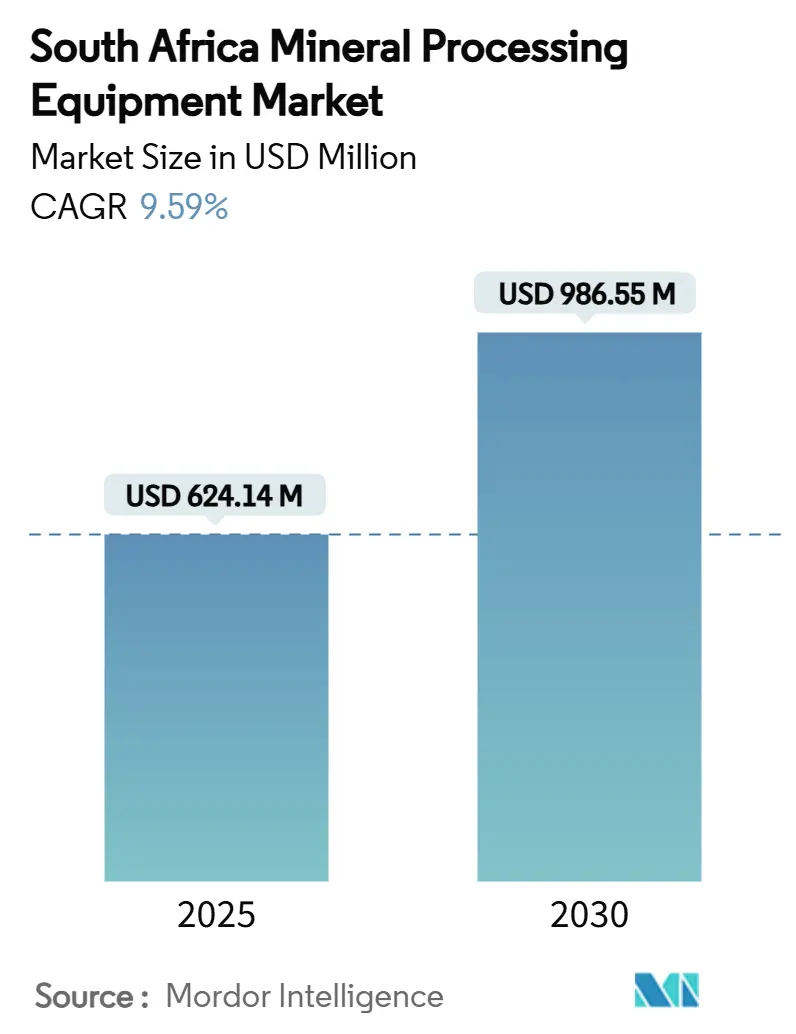

| Market Size (2025) | USD 624.14 Million |

| Market Size (2030) | USD 986.55 Million |

| Growth Rate (2025 - 2030) | 9.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Mineral Processing Equipment Market Analysis by Mordor Intelligence

The South Africa mineral processing equipment market size stands at USD 624.14 million in 2025 and is projected to reach USD 986.55 million by 2030, registering a 9.59% CAGR. This expansion reflects the country’s position as the world’s primary producer of platinum group metals and a significant supplier of iron ore, manganese, and emerging battery minerals. Government beneficiation mandates require miners to add value locally, which underpins sustained capital spending on comminution, separation, and automation technologies. Increased private-sector participation in rail-port logistics, along with modular plant adoption by junior miners, is strengthening demand for flexible processing systems. Parallel pressure to cut electricity use and carbon emissions pushes operators toward high-efficiency equipment that lowers the total cost of ownership.

Key Report Takeaways

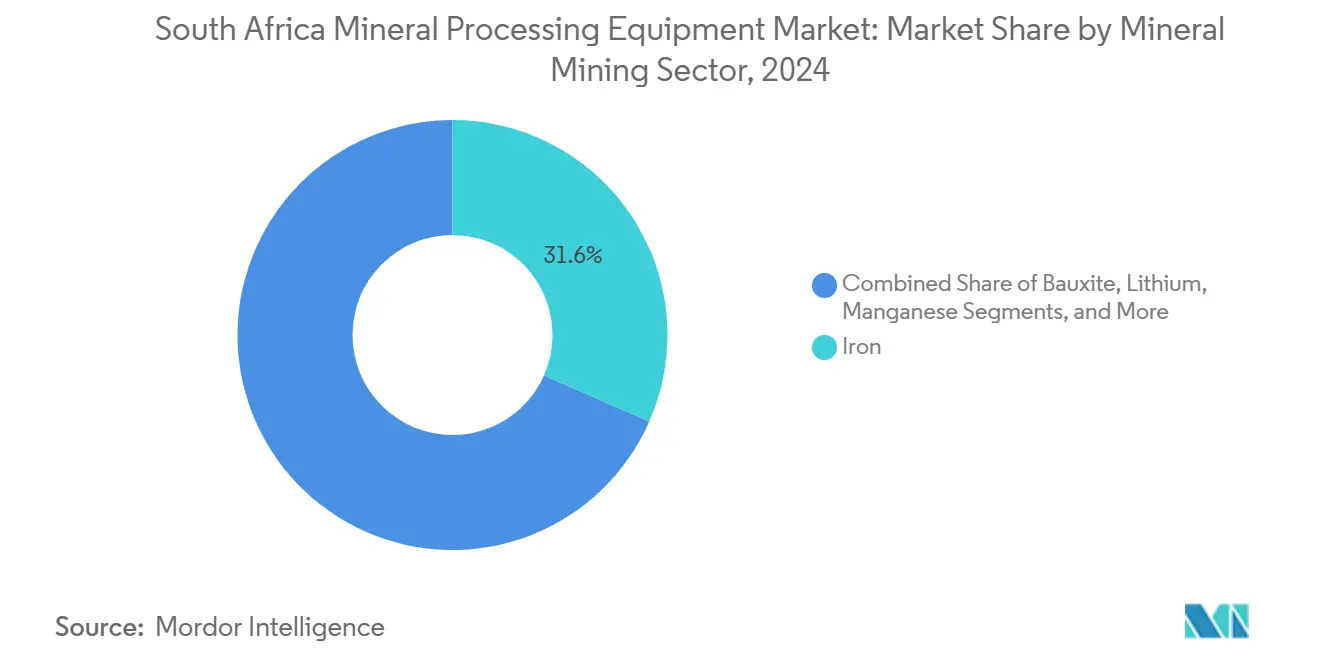

- By mineral mining sector, iron ore processing led with 31.62% of the South Africa mineral processing equipment market share in 2024, while lithium processing is forecast to expand at an 11.21% CAGR through 2030.

- By equipment type, crushers accounted for 26.81% of the South Africa mineral processing equipment market size in 2024; flotation cells represent the fastest-growing category at a 10.85% CAGR between 2025 and 2030.

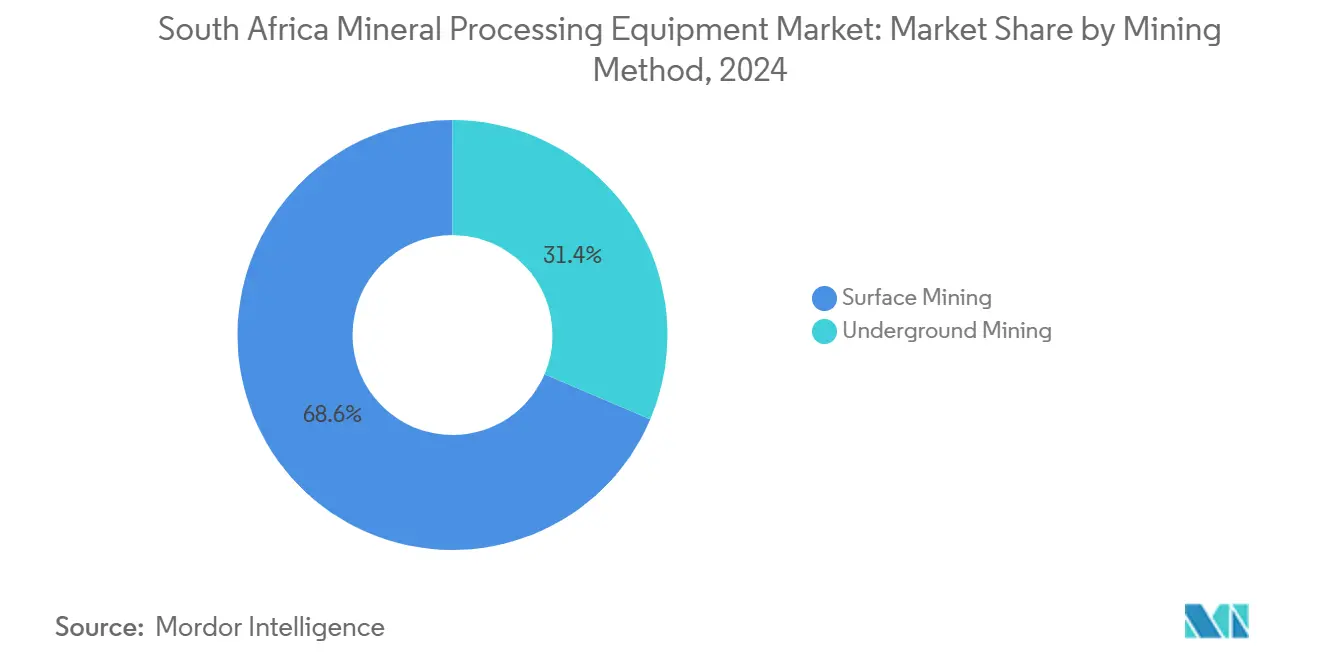

- By mining method, surface operations commanded 68.55% of the South Africa mineral processing equipment market share in 2024, whereas underground mining is advancing at an 11.65% CAGR over the forecast horizon.

- By automation level, manual plants retained 53.77% of the South Africa mineral processing equipment market size in 2024; fully automated systems are accelerating at a 16.82% CAGR to 2030.

Future direction is shaped by developments occurring across multiple countries and regions, with South africa contributing to the overall trajectory. The outlook on worldwide mineral processing equipment market reflects how these are expected to evolve collectively.

South Africa Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Mineral Output of Critical Metals | +2.1% | Northern Cape, Limpopo | Medium term (2-4 years) |

| Government Incentives and Beneficiation Mandates | +1.8% | National | Long term (≥ 4 years) |

| Digitization and Plant Automation Adoption | +1.4% | National | Medium term (2-4 years) |

| ESG-Driven Demand for Energy-Efficient Equipment | +1.2% | National | Long term (≥ 4 years) |

| Rail-Port De-Bottlenecking Projects | +0.9% | Coastal provinces, Northern Cape corridors | Short term (≤ 2 years) |

| Modular Plants for Junior Miners | +0.7% | Regional | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Mineral Output of Critical Metals

South Africa’s surge in battery and platinum group metal production is reshaping equipment demand as miners boost capacity to serve global energy transition supply chains. Lithium processing equipment is the fastest-growing segment, because hard-rock spodumene ore requires specialized crushing, dense media separation, and advanced flotation technologies. Platinum group metal output rose to 2.73 million oz during the nine months ended March 2024, prompting concentrator expansions that favor high-capacity milling and cleaner separation circuits. Iron ore producers are investing in ultra-high-density media separation to lift premium product ratios from 18% to 55%, which raises uptake of energy-efficient pumps and cyclones. Eight flagship projects under the national Critical Minerals Strategy—including the Steelpoortdrift vanadium and Platreef platinum expansions—will add billions in processing spend through 2030. Each project requires plant designs that can treat complex multi-metal mineralogy while maximizing recovery and minimizing water use[1]“Critical Minerals Strategy,” Department of Mineral Resources and Energy, dmr.gov.za.

Government Incentives and Beneficiation Mandates

The Department of Mineral Resources and Energy has proposed export taxes on unprocessed ores and stricter thresholds in Mining Charter III, which already requires 70% local procurement of goods and 80% for services. These policies anchor long-term visibility for the South Africa mineral processing equipment market by forcing mines to install concentrators and smelters before shipping. The ministry allocated ZAR 2.86 billion for 2025/26 to modernize licensing and exploration support, encouraging greenfield discoveries that will need new processing lines. Domestic manufacturers such as Multotec operate more than 20 plants, positioning to supply compliant wear liners, screens, and cyclones. Regulatory certainty and potential fiscal incentives for ferroalloy restarts are creating space for modular plant suppliers that can commission local beneficiation capacity within one budget cycle.

Digitization and Plant Automation Adoption

Mining operators are embracing digital twins, machine-learning-driven process control, and real-time asset monitoring to lift margins by up to 15 percentage points. Equipment now ships with embedded sensors and cloud connectivity that feed predictive-maintenance algorithms, cutting unplanned downtime and reducing liner change frequency. Electric drill rigs equipped with onboard analytics, for example, enhance blast accuracy and downstream throughput. At the concentrator level, computer-vision ore characterization enables automatic reagent dosing in flotation. However, an aging workforce and limited controls engineers slow full autonomy roll-outs, sustaining demand for hybrid semi-automated solutions that layer analytics over manual oversight. Vendors that bundle software, condition-monitoring services, and training capture a premium share in the South Africa mineral processing equipment industry.

ESG-Driven Demand for Energy-Efficient Equipment

The pending national carbon tax and a corporate shift to net-zero goals are redirecting capital budgets toward high-efficiency comminution and water-saving separation. Concentrators now evaluate kilowatt-hours per tonne and greenhouse-gas intensity alongside recovery rate. Utilities plan a 36.15% electricity tariff increase for 2026, which pushes mines to specify high-pressure grinding rolls, coarse‐particle flotation, and paste-thickening circuits that lower power and water bills. Major miners have entered large-scale renewable power purchase agreements, compelling OEMs to design equipment that integrates with variable-renewable energy, supports soft-start capability, and rebounds quickly after grid interruptions. Suppliers that demonstrate verifiable emissions reductions secure preferred-vendor status[2]Eskom Holdings, “Tariff Application MYPD 6,” eskom.co.za .

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unreliable Power Supply and High Tariffs | -2.2% | National | Short term (≤ 2 years) |

| Stringent Environmental Regulations | -1.5% | National | Long term (≥ 4 years) |

| Low-Priced Chinese OEM Competition | -1.1% | National | Medium term (2-4 years) |

| Scarce Automation and Controls Talent | -0.8% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Unreliable Power Supply and High Tariffs

Frequent load-shedding and anticipated double-digit tariff hikes compel mines to reassess processing routes and prioritize energy-thrifty equipment. Some operators adopt onsite solar or wheeling agreements, yet grid instability still necessitates drives and controls able to handle voltage dips and restarts without process upset. The power premium creates a two-speed market: plants with continuous renewable access invest in high-throughput circuits, while others favor modular stages that can idle during curtailment without re-lining losses. OEMs differentiate by offering low-specific-energy grinding mills and fine-grinding alternatives that deliver recovery at reduced power draw, sustaining competitiveness in the South Africa mineral processing equipment market.

Stringent Environmental Regulations

The National Environmental Management Act’s mining amendments cap water discharge, dust, and noise levels, compelling mines to redesign process circuits and adopt closed-loop water systems. From January 2026, the national carbon tax will apply to Scope 1 emissions, raising costs for energy-intensive crushing, grinding, and smelting equipment as electricity tariffs climb. Regulatory authorities now require detailed tailings stewardship plans and rehabilitation bonds before any concentrator expansion, increasing upfront capital outlays and extending permitting timelines. Operators are retrofitting dry-stack tailings, paste thickeners, and low-carbon power feeds, which lifts demand for filter presses, high-efficiency cyclones, and variable-speed drives. Suppliers that certify lower water consumption and verified greenhouse-gas reductions win procurement preference as mines strive to meet buyer ESG criteria and avoid compliance penalties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Iron Dominates, Lithium Accelerates

Iron ore processing controlled 31.62% of the South Africa mineral processing equipment market in 2024, reflecting large-scale hematite operations that deploy massive primary crushers and high-density media circuits. Kumba’s flagship investment at Sishen aims to lift premium-grade output to 55%, a shift that drives orders for precision cyclones and magnetic separation. Lithium’s 11.21% CAGR through 2030 outpaces every other commodity as spodumene projects in Limpopo and Northern Cape commission fine-grinding, magnetic, and flotation packages to deliver battery-grade concentrate. Platinum group metal plants sustain steady equipment demand through debottlenecking upgrades, while coal processing tapers amid global decarbonization targets, yet continues to replace aging spirals and screens. The South Africa mineral processing equipment market size allocated to manganese, copper, and vanadium grows in line with downstream steel and energy-storage applications, stimulating suppliers to tailor packages for multi-metal recovery streams.

Processing plants for minor metals—titanium, bauxite, and rare earths—favor specialized hydrometallurgical and gravity circuits that reward OEMs with niche metallurgical know-how. Copper 360’s push to scale production to 50,000 t by 2027 exemplifies a new wave of mid-tier mines seeking compact, high-recovery concentrators. As commodity mix broadens, plant designers increasingly specify flexible flowsheets capable of treating variable feed chemistry without remodeling, strengthening long-term demand for modular separators and reconfigurable control logic in the South Africa mineral processing equipment market.

By Equipment Type: Crushers Lead, Flotation Cells Surge

Crushers generated 26.81% of the South Africa mineral processing equipment market in 2024, cementing them as the backbone of every flowsheet and a dependable replacement cycle. Large surface operations select high-throughput gyratory units; underground mines prefer compact, energy-efficient jaw or sizer technologies. Flotation cells record the fastest 10.85% CAGR, aligned with complex polymetallic ores that need selective reagent regimes and sophisticated gas dispersion control. Orders increasingly bundle online froth cameras, automatic level controllers, and reagent optimization software, signaling integration of digital layers across mechanical equipment.

Grinding mills and high-pressure grinding rolls capture a stable share as miners pivot from energy-intensive SAG circuits to fine-grinding options that cut power by up to 30%. Screening technology evolves toward multiple-deck vibration designs with polyurethane media that enhance wear life and classification accuracy. Conveyors, pumps, and valves maintain predictable replacement demand proportional to plant expansions. The South Africa mineral processing equipment market size linked to automation and control hardware accelerates as greenfield projects set autonomous-ready standards, embedding sensors and edge computing into even auxiliary components.

By Mining Method: Surface Dominates, Underground Gains

Surface operations contributed 68.55% of the South Africa mineral processing equipment market in 2024, because bulk commodities like iron ore, coal, and manganese remain open-pit. Equipment selections emphasize robust primary crushers, overland conveyors, and large-format screens capable of handling multi-million tonne per annum throughput. Underground projects grow at an 11.65% CAGR since deeper orebodies sustain higher grades that justify mechanized block cave or room-and-pillar systems. These mines procure compact feeders, mobile crushers, and energy-efficient ventilation linked to process control for dust and gas management.

Mechanized underground projects, exemplified by the Waterberg PGM development with a 54-year mine life, require integrative engineering where equipment footprints must fit shaft dimensions while meeting output targets. Demand rises for backfill systems, paste thickeners, and narrow-vein sorting modules that minimize dilution. As open pits deepen and strip ratios climb, surface mines consider in-pit crushing and conveying to cut haul-truck fuel use, creating fresh opportunities for semi-mobile crusher-conveyor packages in the South Africa mineral processing equipment market.

By Automation Level: Manual Persists, Full Automation Accelerates

Manual processing still represents 53.77% of the South Africa mineral processing equipment market in 2024, because labor costs remain competitive, and legacy plants have yet to retrofit control systems. The hybrid segment installs selective automation—ore tracking, density control, or advanced process control—while retaining human oversight. Fully automated operations post the fastest 16.82% CAGR as mines confront safety regulations, power cost spikes, and skills gaps. Autonomous mills adjust media charge and power draw without operator input, while drones and computer-vision inspection replace manual liner checks.

Automation suppliers bundle training and remote support, mitigating workforce shortages. Mines transitioning to autonomy adopt phased roadmaps: instrumentation upgrades, control-loop stabilization, model-predictive control, and eventually closed-loop plants. Equipment capable of plug-and-play integration with existing PLCs and MES platforms is gaining rapid uptake, bolstering high-margin software and service revenue within the South Africa mineral processing equipment industry.

Geography Analysis

Northern Cape anchors the largest slice of the South Africa mineral processing equipment market, propelled by iron ore giants that deploy capital-dense dense-media separations and robust primary crushing. Limpopo is the fastest-growing province as it hosts new-age battery mineral and platinum projects with forecast double-digit growth in flotation, magnetic separation, and ultra-fine grinding.

Mpumalanga maintains a steady pipeline of replacement spirals and screens for coal washeries even as export volumes face logistic headwinds. The Western Cape houses a burgeoning cluster of equipment manufacturing and refurbishment, with large fabrication workshops that supply both domestic and regional orders.

Gauteng serves as the commercial nucleus, concentrating OEM sales teams, application specialists, and parts distribution centers that underpin aftermarket competitiveness. Coastal provinces benefit from port expansions that incentivize local pre-shipment beneficiation of chrome and manganese. As rail-port upgrades open export routes, mines invest in modular and mobile plants near production hubs to reduce haul distances. Up-country base-metal prospects are adopting movable concentrators to keep pace with exploration drift, spreading demand across every province and cementing national integration in the South Africa mineral processing equipment market.

Analysis of the mineral processing equipment market by Mordor Intelligence is supported by country-level insights for Egypt, Morocco, Australia, China, Canada, Germany, France, Spain, and South Korea, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The market shows moderate concentration: several OEMs face persistent share erosion from agile Chinese entrants and specialized local fabricators. International majors such as FLSmidth, Metso, Sandvik, and Weir defend their share through patented wear solutions, high-performance metallurgy, and digital services that guarantee uptime. Domestic producers, notably Multotec and Bell, exploit proximity advantages, Mining Charter procurement preferences, and rapid lead times on customized spares.

Service contracts now outweigh the initial equipment margin. FLSmidth’s Mining Service revenue grew 14% in Q1 2025 as mines seek lifecycle partnerships. Weir secured a USD 67 million high-pressure grinding roll package for a new copper concentrator, underscoring the pivot to process-intensive commodities. Chinese brands expand via price-led bids in commodity pumps and standard crushers, but struggle to penetrate critical applications requiring stringent metallurgical guarantees.

White-space growth lies in modular plant packages for juniors, integrated automation retrofits, and energy-efficiency upgrades. OEMs that present measurable kilowatt-hour savings and carbon-reduction pathways secure strategic supplier status. Skills shortages in process controls spur demand for remote monitoring and training services, creating recurring revenue that buffers price competition in the South Africa mineral processing equipment market.

South Africa Mineral Processing Equipment Industry Leaders

Multotec

FLSmidth A/S

Metso Outotec

Sandvik AB

The Weir Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Athos Crushing & Screening will launch fully electric Powertrack mobile crushers and screens, manufactured by SRHeavy, covering jaw, cone, triple-deck, and scalping units.

- June 2025: A domestic polymetallic mine awarded design and supply of fifteen DELKOR BQR flotation cells to increase fine-particle recovery.

- February 2025: XCMG and Kiboko Group formed a partnership announced at Mining Indaba 2025, aiming to localize production and enhance skills transfer within South Africa’s mining supply chain.

South Africa Mineral Processing Equipment Market Report Scope

| Bauxite |

| Iron |

| Lithium |

| Platinum Group Metals |

| Manganese |

| Coal |

| Gold |

| Copper |

| Other Minerals |

| Crushers |

| Feeders |

| Conveyors |

| Drills and Breakers |

| Grinding Mills |

| Screening Equipment |

| Cyclones and Separators |

| Flotation Cells |

| Pumps and Valves |

| Automation and Control Systems |

| Others |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| By Mineral Mining Sector | Bauxite |

| Iron | |

| Lithium | |

| Platinum Group Metals | |

| Manganese | |

| Coal | |

| Gold | |

| Copper | |

| Other Minerals | |

| By Equipment Type | Crushers |

| Feeders | |

| Conveyors | |

| Drills and Breakers | |

| Grinding Mills | |

| Screening Equipment | |

| Cyclones and Separators | |

| Flotation Cells | |

| Pumps and Valves | |

| Automation and Control Systems | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated |

Key Questions Answered in the Report

How large is the South Africa mineral processing equipment market in 2025?

The South Africa mineral processing equipment market size is USD 624.14 million in 2025 with a projected 9.59% CAGR to 2030.

Which mineral drives the fastest equipment demand growth?

Lithium processing equipment posts the strongest outlook, advancing at an 11.21% CAGR due to hard-rock spodumene projects.

What equipment category is expanding most rapidly?

Flotation cells lead growth with a 10.85% CAGR as complex ores need advanced separation and digital control.

How is power instability influencing purchasing decisions?

Mines prioritize energy-efficient mills and modular circuits that withstand load-shedding, which favors suppliers offering lower kilowatt-hour per tonne solutions.

Page last updated on: