Africa Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 3.12 Billion |

| Market Size (2030) | USD 3.84 Billion |

| Growth Rate (2025 - 2030) | 4.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Mining Equipment Market Analysis by Mordor Intelligence

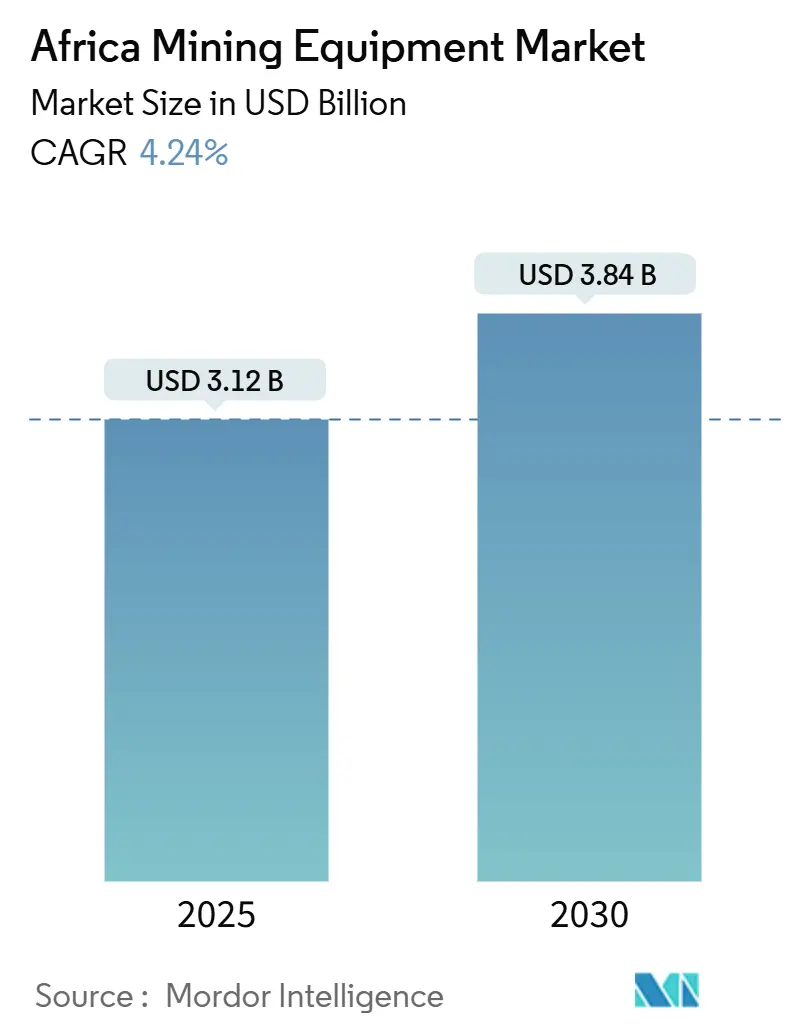

The Africa mining equipment market size is valued at USD 3.12 billion in 2025 and is forecast to reach USD 3.84 billion by 2030, reflecting a 4.24% CAGR through the period. This steady expansion stems from sustained demand for minerals that underpin global energy transition goals, large-scale surface mining projects in copper and iron-ore belts, and accelerating adoption of automated and battery-electric fleets across key producing nations. Heightened investment in decarbonization technologies, continued localization of original-equipment manufacturer (OEM) facilities, and government infrastructure programs that stimulate aggregates and iron-ore production collectively reinforce long-term equipment procurement cycles. Meanwhile, the automation revolution is reshaping operating models, with miners balancing the productivity benefits of advanced systems against the affordability of conventional machinery. Supply-chain vulnerabilities, regulatory uncertainty, and counterfeit component proliferation remain the leading challenges that temper headline growth expectations.

Key Report Takeaways

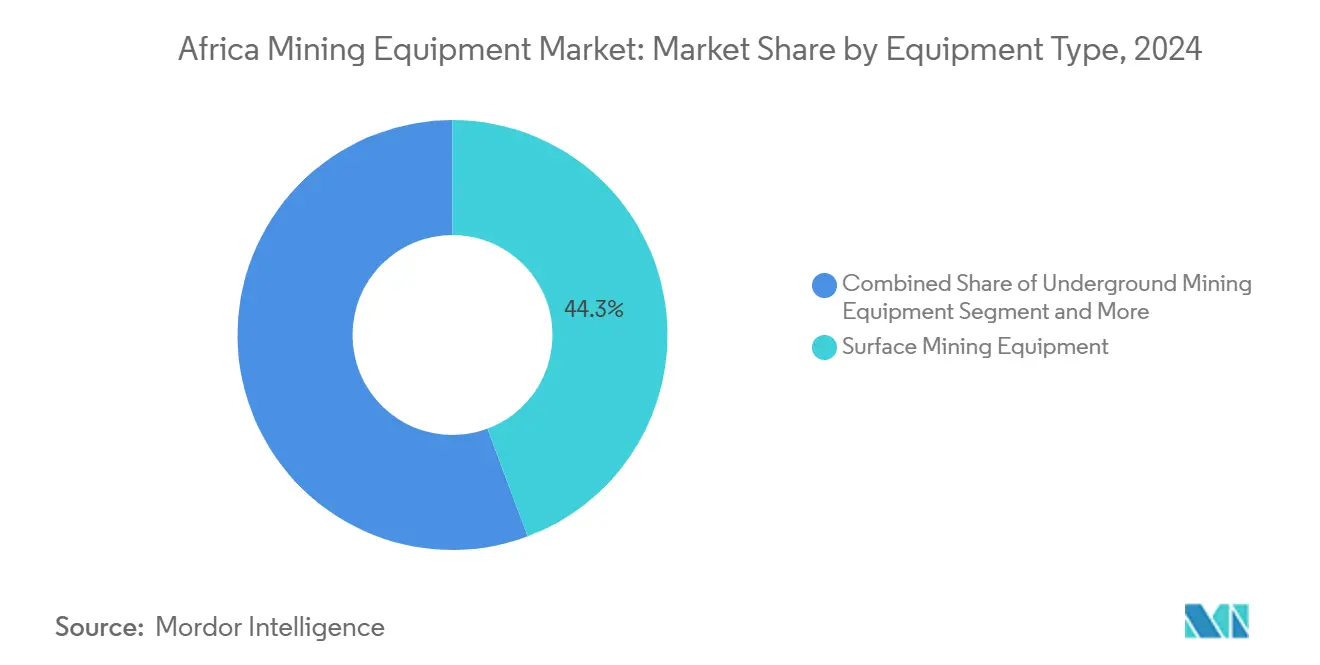

- By equipment type, Surface mining equipment captured 44.31% of the Africa mining equipment market share in 2024; loaders and haul trucks are projected to record the fastest 4.88% CAGR through 2030.

- By automation level, Manual equipment accounted for 66.73% of the Africa mining equipment market size in 2024, while fully autonomous systems are poised for a 28.36% CAGR to 2030.

- By powertrain type, Internal-combustion powertrains retained 72.45% of the Africa mining equipment market size in 2024, even as battery-electric fleets expand at an 8.55% CAGR to 2030.

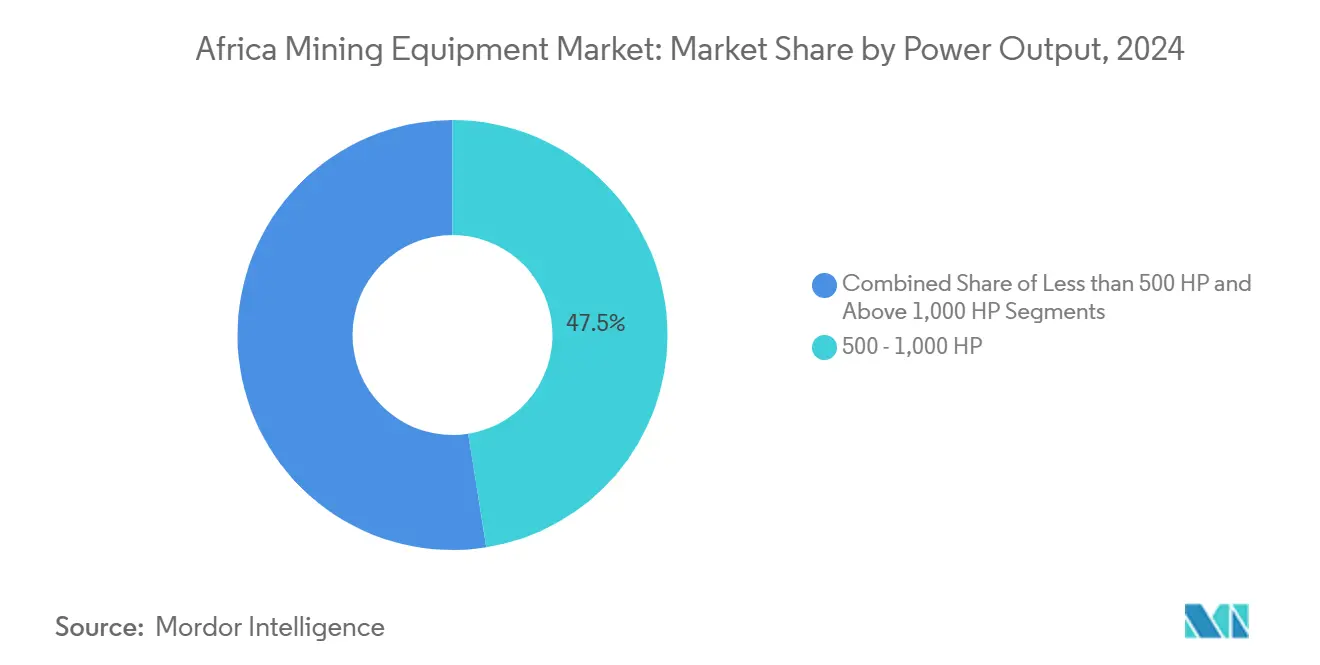

- By power output, the 500–1,000 HP category led with a 47.53% share of the Africa mining equipment market size in 2024; sub-500 HP units are forecast to post a 6.12% CAGR through 2030.

- By application, Metal mining represented 53.71% of the Africa mining equipment market size in 2024, whereas mineral mining is projected to advance at a 5.63% CAGR by 2030.

- By Country, South Africa led with a 39.66% revenue share in 2024, while the Democratic Republic of Congo is the fastest-growing market with a projected 6.48% CAGR to 2030.

Africa Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Surface Mining in Africa | +1.5% | DRC, Guinea, South Africa | Medium term (2-4 years) |

| Infrastructure Projects Driving Iron-Ore & Aggregates | +1.2% | South Africa, Guinea, Algeria, Nigeria | Short term (≤ 2 years) |

| Investments in Electric Mining Trucks | +0.8% | South Africa, DRC, Ghana, Nigeria | Long term (≥ 4 years) |

| Rare-Earth Exploration Boosting Drilling Demand | +0.6% | South Africa, DRC, Niger, Algeria | Medium term (2-4 years) |

| Predictive Maintenance via Satellite Connectivity | +0.4% | South Africa and major operations continent-wide | Short term (≤ 2 years) |

| OEM Assembly & Rebuild Localization in Africa | +0.3% | South Africa, Botswana, Nigeria, Ghana | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Surface Mining Projects in Africa

Mega-projects such as Guinea’s USD 11.6 billion Simandou iron-ore development, which demands over 600 km of rail and ultra-class haulage fleets, exemplify the scale driving equipment procurement. South Africa’s Kumba Iron Ore added R7.6 billion (USD 428 million) in processing upgrades at Sishen mine, extending life to 2044 and boosting premium ore output, reinforcing the need for higher-horsepower machinery [1]Kumba Iron Ore, “Sishen UHDMS project update,” kumba.co.za. In the DRC, copper output climbed 12.6% to 3.3 million t in 2024, underscoring sustained investment in 1,000 HP-plus equipment that supports rising strip ratios. Demand multipliers radiate across drills, blasthole rigs, and autonomous trucks that can safely operate in deepening open pits, prompting OEM product development focused on durability, payload, and digital readiness.

Government-Led Infrastructure Programs Boosting Iron-Ore and Aggregates Demand

South Africa’s Critical Minerals and Metals Strategy 2025 targets 2.3 million new jobs through local beneficiation, spurring purchases of crushers, screens, and bulk handling systems [2]Department of Mineral and Petroleum Resources, “Critical Minerals and Metals Strategy 2025,” dmre.gov.za. Nigeria’s Presidential Mining Roadmap aims to raise mining’s GDP share from 0.77% to 10% by 2026, triggering equipment investments in processing hubs and limestone quarries. Algeria’s liberalized mining code now welcomes foreign partners in zinc and copper projects, expanding demand for exploration rigs and material-moving systems. Such public-sector spending sets local-content thresholds that encourage OEMs to establish assembly lines, thereby anchoring longer-term parts and service demand.

Rising Investments in Battery-Electric Mining Trucks

Electrification gains traction as miners seek to cut diesel costs and comply with decarbonization targets. Gold Fields’ South Deep mine validated Sandvik’s LH518B battery loader at 3 km depth, proving 30% lower maintenance expenditure relative to diesel counterparts. Epiroc reported 17% order growth in Q1 2025, citing SEK 2.2 billion in autonomous and electric surface-equipment contracts, most notably in Africa[3]Epiroc Group, “Q1 2025 results,” epiroc.com. Hydropower-rich DRC offers favorable economics for battery-electric haulage that eliminates local diesel volatility. R&D advances have doubled battery energy density since 2022, enabling 40-tonne articulated trucks to complete full shifts without recharging, a milestone expected to accelerate fleet conversion once charging infrastructure scales.

Growth in Rare-Earth Exploration Driving Specialized Drilling Demand

Exploration for lithium, neodymium, and cobalt intensifies across the continent as global consumption of rare-earth elements is projected to quadruple by 2030. Niger’s state-owned Cominair SA plans expanded copper and lithium programs in Agadez that require advanced core-drill platforms capable of continuous operation in arid conditions. KoBold Metals committed USD 1 billion to DRC’s Manono lithium deposit, deploying AI-guided drilling that demands high-precision rigs with real-time sample analysis. The complex geology of strategic mineral deposits necessitates equipment with adaptive torque control and minimal environmental footprint, pushing suppliers to innovate around modular mast designs and energy-efficient hydraulics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity Price Volatility | -0.7% | South Africa, DRC, Ghana | Short term (≤ 2 years) |

| Critical Component Supply Disruptions | -0.5% | Landlocked regions such as DRC, Niger | Medium term (2-4 years) |

| High Cost of Autonomous & Electric Equipment | -0.4% | South Africa, Ghana, Nigeria | Long term (≥ 4 years) |

| Counterfeit Parts Undermining OEM Trust | -0.3% | South Africa, Nigeria, West Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Commodity-Price Volatility Affecting CAPEX Cycles

Fluctuating commodity prices create stop-start procurement cycles that disrupt OEM production planning and depress equipment utilization rates. Platinum dipped to USD 960 /oz in 2024, prompting South African miners to defer fleet renewals and instead prioritize maintenance over replacement. Historical patterns indicate that equipment orders typically lag commodity recoveries by up to 18 months, prolonging the revenue trough for suppliers. Smaller operators lacking robust balance sheets are especially sensitive, often resorting to leasing or renting older machines, which dampens fresh demand in the Africa mining equipment market.

Persistent Supply-Chain Disruptions for Critical Components

The Southern African Institute of Mining and Metallurgy (SAIMM) notes semiconductor and hydraulic component shortages pushing average lead times for drilling rigs to 14 months in 2025. Landlocked producers in the DRC face further delays due to congested ports and limited road infrastructure, inflating landed costs and deferring commissioning schedules. While some miners explore local sourcing, the continent’s capacity to machine complex parts remains nascent, extending dependence on overseas suppliers and constraining the Africa mining equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Equipment Maintains Leadership

Surface mining machinery retained 44.31% of the Africa mining equipment market in 2024, buoyed by extensive open-pit copper and iron-ore operations that depend on large excavators, high-capacity haul trucks, and rotary drills. Guinea’s Simandou and the DRC’s Kamoa-Kakula exemplify projects that collectively require hundreds of pieces of heavy iron, sustaining OEM order books.

Loaders and haul trucks form the fastest-growing subcategory with a 4.88% CAGR forecast to 2030, reflecting increasing fleet standardization and the onset of autonomous haulage. Underground equipment remains essential for deep-level gold operations in South Africa, yet it expands at a slower pace given limited new mine development. Crushing and screening units experience revitalized demand due to beneficiation mandates that aim to process ores domestically and thus enlarge the Africa mining equipment market.

By Automation Level: Autonomous Uptake Accelerates

Manual equipment still dominated 66.73% of the Africa mining equipment market in 2024 because of its lower entry cost and broad operator familiarity, especially in established gold and diamond districts. Semi-autonomous rigs act as a transitional step, offering collision-avoidance and drill-string automation without full network investment.

Fully autonomous fleets, however, are scaling rapidly at a 28.36% CAGR, highlighted by the Syama underground gold mine in Mali that operates driverless trucks, loaders, and drills around the clock. Technology suppliers now bundle autonomy kits with tele-operation centers, making adoption more feasible for mid-sized properties and enlarging the Africa mining equipment market.

By Powertrain Type: Zero-Emission Fleets Gain Momentum

Internal-combustion engines commanded 72.45% of 2024 demand, benefiting from existing fuel logistics and proven field reliability. Hybrid units provide incremental fuel savings but have yet to scale beyond pilot fleets.

Battery-electric vehicles rise at an 8.55% CAGR, driven by ventilation savings in deep underground mines and increased availability of renewable power in the DRC and Zambia. Sandvik and Epiroc offer loaders and haul trucks exceeding 18 t payload with swappable battery packs, a signature development likely to reshape long-term emissions profiles within the Africa mining equipment market.

By Power Output: Mid-Range Machines Balance Productivity and Agility

Equipment rated 500–1,000 HP secured 47.53% of the Africa mining equipment market in 2024, striking a balance between fuel efficiency and payload across copper belts and iron-ore pits. OEMs standardize parts across this range, easing maintenance and procurement.

Machines under 500 HP, encompassing exploration drills and small loaders, post the quickest 6.12% CAGR as juniors intensify prospecting to replenish declining reserves. Ultra-class trucks above 1,000 HP cater to high-volume pits but face site infrastructure constraints that cap broader penetration.

By Application: Metals Mining Remains the Anchor

Metal mining accounted for 53.71% of 2024 equipment demand thanks to copper, gold, and platinum projects spread across Southern and Central Africa. Established underground and open-pit operations provide a steady replacement cycle, offering stability to the Africa mining equipment market.

Mineral mining, led by lithium and rare-earth exploration, grows at a 5.63% CAGR as global EV battery supply chains diversify away from traditional sources. Coal retains localized importance for power generation in South Africa and Botswana, but encounters mounting ESG pressures that temper new mine approvals.

Geography Analysis

South Africa retained leadership with 39.66% of 2024 revenue, underpinned by century-old infrastructure, entrenched OEM dealer networks, and a manufacturing base that includes components and rebuild centers. Investments such as Kumba Iron Ore’s R7.6 billion processing upgrade at Sishen underscore the drive to lift productivity through equipment modernization. Nonetheless, energy constraints and policy ambiguity weigh on growth prospects, compelling miners to prioritize efficiency over capacity expansion.

The Democratic Republic of Congo is the fastest-rising market with a projected 6.48% CAGR to 2030 as copper, cobalt, and emerging lithium projects draw global capital. Ivanhoe Mines’ Kamoa-Kakula complex delivered 437,061 t of copper in 2024 and completed the continent’s largest copper smelter, signaling sustained fleet purchases for both open-pit and concentrator operations. Chinese partnerships further spur equipment imports while incentivizing OEMs to establish service outposts in Kolwezi and Lubumbashi.

Nigeria, Algeria, and other West and North African jurisdictions represent the next frontier as governments loosen ownership rules, slash import duties on machinery, and advertise critical-mineral potential. Algeria’s Tala Hamza zinc project and Nigeria’s drive to lift mining’s GDP share herald multi-year fleet build-outs that should broaden the Africa mining equipment market footprint beyond traditional hubs.

Competitive Landscape

The Africa mining equipment industry exhibits moderate concentration, with Caterpillar, Komatsu, Liebherr, Sandvik, and Epiroc accounting for a majority of installed fleets. These firms leverage deep product portfolios, autonomous-system roadmaps, and continent-wide dealer alliances such as Barloworld Equipment in Southern Africa and BIA Group in West Africa. Localized rebuild centers lower the total cost of ownership and secure recurring parts income.

Competitive dynamics intensify as Chinese brands introduce lower-priced haul trucks and drills, forcing incumbents to emphasize reliability, digital services, and sustainability credentials. Komatsu’s acquisition of GHH bolsters underground offerings tailored to Southern Africa’s hard-rock conditions, while Epiroc’s battery-electric line garners early orders in the DRC’s hydro-powered provinces. OEMs also partner with satellite and analytics providers to wrap predictive maintenance into long-term service contracts.

Supply-chain uncertainty and counterfeit parts oblige market leaders to invest in traceability, blockchain-based authentication, and technician upskilling. Firms that integrate digital monitoring, autonomous kits, and low-emission powertrains into comprehensive lifecycle solutions are positioned to capture incremental share in the Africa mining equipment market despite macro volatility.

Africa Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Liebherr-International AG

Sandvik AB

Epiroc AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: TAKRAF India won an equipment order for a North African phosphate mine covering four compact spreaders with bridging conveyors.

- September 2024: Komatsu Mining Technologies announced a hard-rock miner launch in South Africa for limestone and industrial mineral applications.

- August 2024: Sumitomo Corporation partnered with BIA Group to enhance Komatsu's distribution of mining machinery across 20 African nations.

- January 2024: Komatsu debuted the WXO7 loader, ZJ21 jumbo, and ZB21 bolter for underground use at Mining Indaba.

Africa Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills and Breakers |

| Crushing, Pulverizing and Screening |

| Loaders and Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 – 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| South Africa |

| Nigeria |

| Algeria |

| Democratic Republic of Congo (DRC) |

| Libya |

| Rest of Africa |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills and Breakers | |

| Crushing, Pulverizing and Screening | |

| Loaders and Haul Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 – 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining | |

| By Country | South Africa |

| Nigeria | |

| Algeria | |

| Democratic Republic of Congo (DRC) | |

| Libya | |

| Rest of Africa |

Key Questions Answered in the Report

How large is the Africa mining equipment market in 2025?

The market stands at USD 3.12 billion in 2025 and is set to expand at a 4.24% CAGR to USD 3.84 billion by 2030.

Which equipment type leads current sales across Africa?

Surface mining machinery, including excavators and haul trucks, holds 44.31% of 2024 revenue thanks to extensive open-pit copper and iron-ore projects.

What is the fastest-growing powertrain option?

Battery-electric vehicles are advancing at 8.55% CAGR, propelled by underground ventilation savings and decarbonization objectives.

Which country offers the highest growth potential?

The Democratic Republic of Congo is forecast for a 6.48% CAGR through 2030, driven by copper, cobalt, and emerging lithium investments.

Page last updated on: