South Africa Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

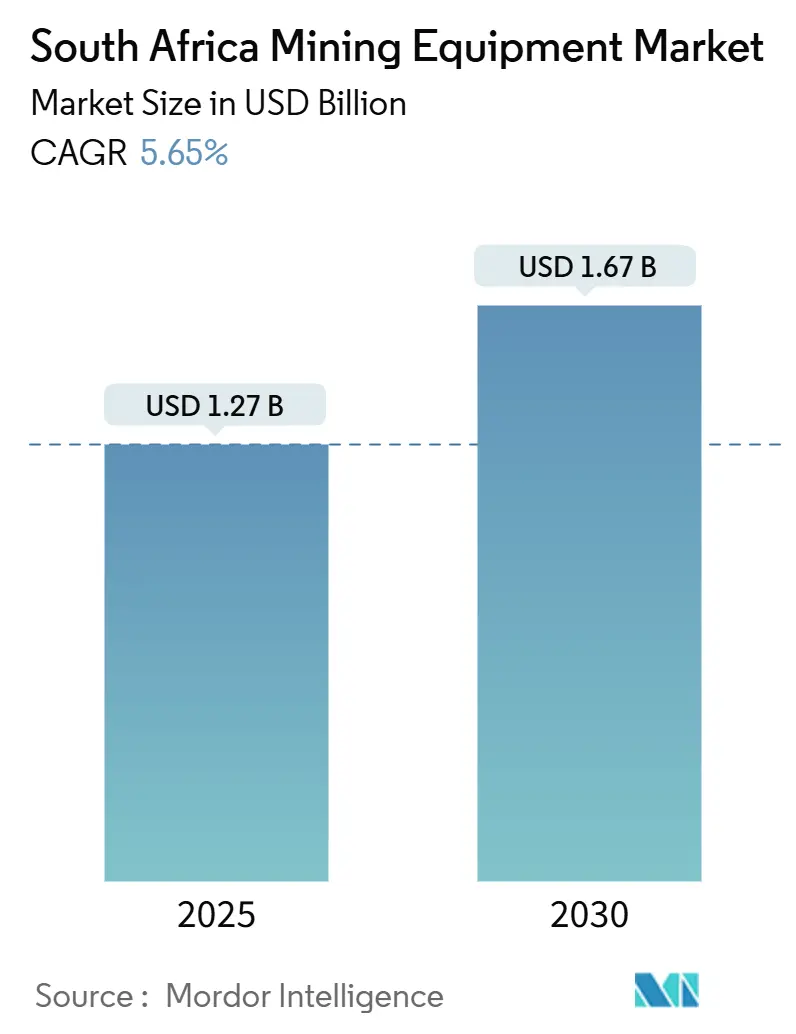

| Market Size (2025) | USD 1.27 Billion |

| Market Size (2030) | USD 1.67 Billion |

| Growth Rate (2025 - 2030) | 5.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Mining Equipment Market Analysis by Mordor Intelligence

The South African mining equipment market size stands at USD 1.27 billion in 2025 and is projected to reach USD 1.67 billion by 2030, reflecting a 5.65% CAGR over the forecast period. Rising commodity prices, removing load-shedding since April 2024, and focused government incentives strengthen capital expenditure programs and underpin steady equipment demand. Fresh exploration funding, performance-based haulage reforms, and a rebound in energy availability foster confidence among operators navigating rail bottlenecks and policy uncertainty. International OEMs retain a strong presence, yet local manufacturers gain ground through localization mandates, while Chinese second-hand imports intensify price competition. Growing commitments to zero-emission fleets and mandatory Level 9 safety systems accelerate technology upgrades even as skills shortages slow the pace of full automation. Collectively, these dynamics keep the South African mining equipment market on a firm, though uneven, growth trajectory.

Key Report Takeaways

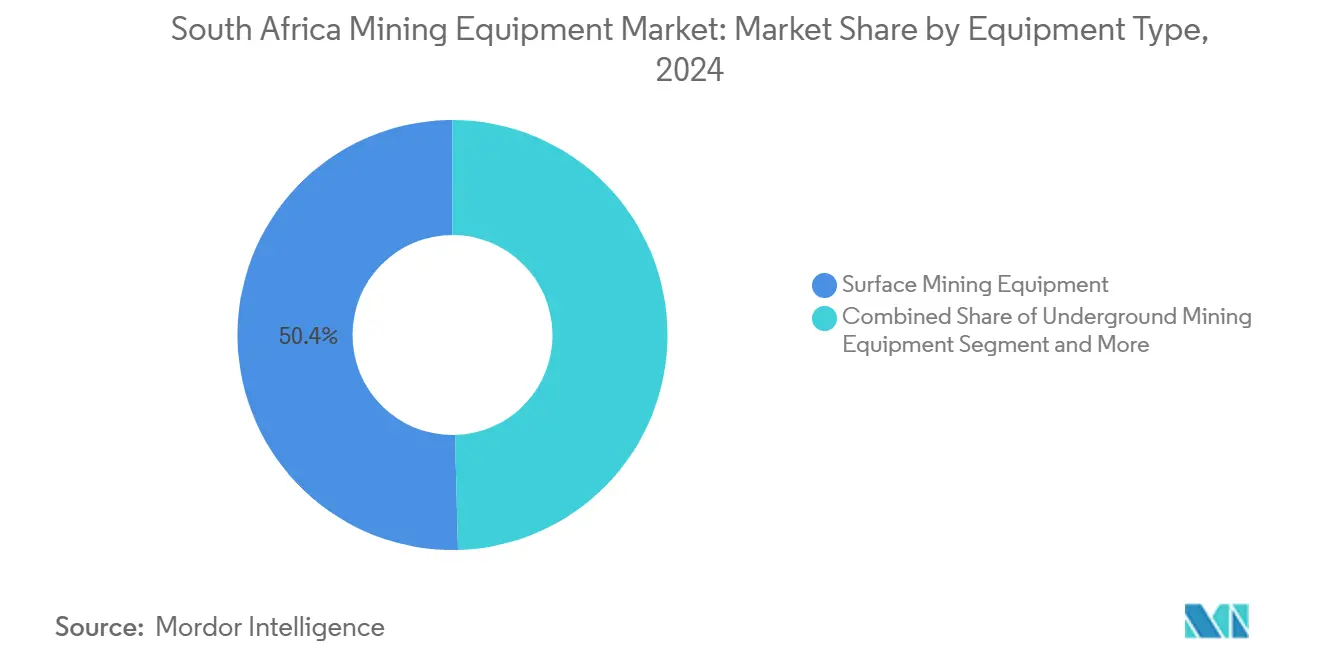

- By equipment type, surface mining equipment led the South Africa mining equipment market with a 50.41% revenue share in 2024, while underground equipment posted the highest CAGR at 8.61% to 2030.

- By automation level, manual machines held 75.17% of the South Africa mining equipment market share in 2024, yet fully autonomous solutions are set to expand at a 10.34% CAGR through 2030.

- By powertrain, internal combustion units accounted for 82.43% of the South Africa mining equipment market in 2024, whereas battery electric vehicles are forecast to accelerate at an 11.82% CAGR by 2030.

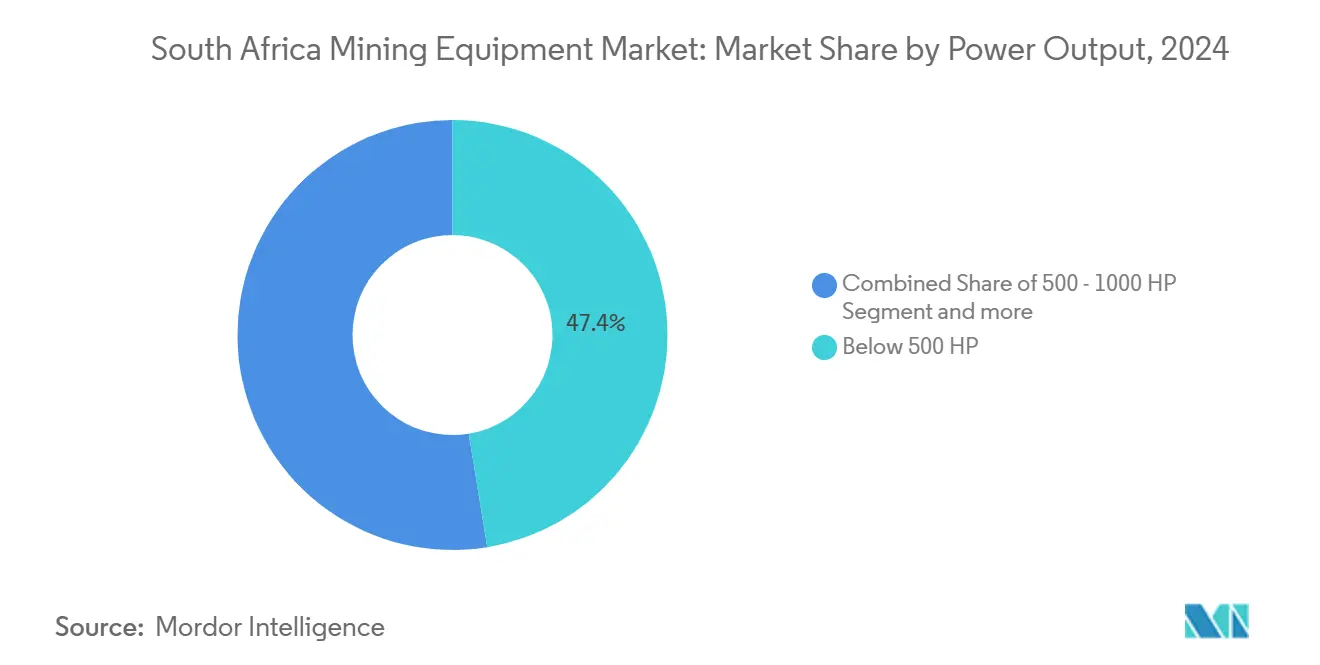

- By power output, sub-500 HP machines represented 47.42% of the South Africa mining equipment market size in 2024 and are advancing at a 7.37% CAGR to 2030.

- By application, coal operations captured 44.71% of the South Africa mining equipment market share in 2024, while mineral mining equipment demand is projected to rise at a 9.39% CAGR through 2030.

South Africa Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CAPEX Rebound | +1.2% | Limpopo, North West, Mpumalanga | Medium term (2-4 years) |

| IPAP Localization Boost | +0.9% | Gauteng manufacturing hub | Medium term (2-4 years) |

| Fast-Track Critical-Minerals Licensing | +0.8% | Northern Cape, Limpopo | Long term (≥ 4 years) |

| PBS-Driven Fleet Upgrades | +0.6% | National transport corridors | Short term (≤ 2 years) |

| BEV Green-Bond Funding | +0.4% | Major mining houses nationwide | Long term (≥ 4 years) |

| Level-9 Safety Mandate | +0.3% | Underground operations nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Commodity-Price Driven CAPEX Rebound

Platinum group metals and other critical minerals rallied in 2024, prompting miners to lift capital by spending, with examples such as Thungela’s ZAR 3.9 billion program covering new surface and underground gear[1]“Thungela details ZAR 3.9 billion CAPEX”, Mining Weekly, miningweekly.com. Deferred investments made during earlier price weakness are now being released, and improved grid stability since April 2024 lets operators fully utilize fresh assets. Higher CAPEX flows mostly favor surface fleets, which are still the largest segment of the South African mining equipment market.

Localization Incentives Under IPAP

Rules under the Industrial Policy Action Plan mandate a minimum local content for capital goods. These rules aim to promote domestic manufacturing and reduce reliance on imports. When paired with the Black Industrialist Scheme, which supports the growth of black-owned businesses in key industries, these regulations channel demand towards Gauteng-based manufacturers like Bell and Barloworld. This initiative boosts local production and fosters economic empowerment within the region. Original Equipment Manufacturers (OEMs) lacking assembly lines respond to these requirements by increasing knock-down kit operations. This strategy enables them to assemble products locally, ensuring compliance with the regulations and securing their foothold in the competitive South African mining equipment market.

Green-Bond Financing for BEV Fleets

Anglo American's 290-ton hydrogen haul truck showcases the commercial potential of zero-emission heavy machinery, marking a significant step toward sustainable mining practices. This innovation highlights the growing feasibility of integrating hydrogen-powered equipment into mining operations, reducing reliance on fossil fuels and lowering carbon emissions. Meanwhile, green bonds, structured in line with National Treasury guidelines, play a pivotal role in facilitating the adoption of such technologies by reducing financing costs for eco-friendly acquisitions. These bonds provide an attractive financing option for companies transitioning toward cleaner energy solutions. Although their market share remains modest, battery electric vehicles are rapidly gaining traction in South Africa's mining equipment sector. This steep adoption curve reflects the increasing demand for sustainable alternatives, driven by regulatory pressures, environmental concerns, and the long-term cost benefits of zero-emission technologies.

Mandatory EMESRT Level 9 Safety Adoption

Under the revised Mine Health and Safety Act codes, mobile equipment must now be equipped with collision-avoidance technology to enhance operational safety and reduce accidents. Original Equipment Manufacturers (OEMs) respond to this mandate by factory-installing ISO 21815-2 interfaces, ensuring their equipment meets the required standards. This development aligns with the industry's growing safety and regulatory compliance emphasis. Furthermore, underground mining sites, with a strong focus on achieving zero-harm objectives, proactively allocate budgets to upgrade loaders, trucks, and drills to comply with these regulations. These investments reflect the sector's commitment to fostering safer working environments while adhering to evolving safety standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power and Rail Bottlenecks | -1.1% | Coal and iron-ore corridors | Medium term (2-4 years) |

| Low-Cost Chinese Imports | -0.9% | Smaller operations nationwide | Short term (≤ 2 years) |

| Permit and Policy Uncertainty | -0.7% | New project pipeline | Long term (≥ 4 years) |

| Automation Skills Gap | -0.6% | Gauteng and Western Cape | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Electricity and Rail Constraints

As Transnet's coal-rail volumes dwindled, miners increasingly relied on pricier road networks to transport coal, significantly raising logistical costs. Over the past decade, electricity tariffs surged annually, further tightening profit margins for mining companies. This consistent rise in operational costs has placed additional financial strain on the sector. Funds that could have been allocated for acquiring new and advanced mining equipment are now being redirected towards diesel generators to mitigate power outages and alternative transport solutions to address rail inefficiencies. These challenges have collectively dampened the overall growth of South Africa's mining equipment market, limiting its potential for expansion and innovation.

Skilled Technician Shortage for Automation

Implementing the Fourth Industrial Revolution, characterized by advancements in automation, artificial intelligence, and the Internet of Things (IoT), faces significant delays in regions where a lack of skilled personnel persists. The shortage of adequately trained professionals hampers the adoption of these transformative technologies, creating bottlenecks in industries aiming to modernize their operations. Addressing this skills gap is critical for ensuring the seamless integration of innovative solutions and maintaining competitive advantages in the global market. Gauteng workshops report lengthy recruitment cycles for mechatronics and data analytics roles, slowing the uptake of autonomous rigs and trucks[2].“4IR Skills Gap in Mining”, ITWeb, itweb.co.za

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Resilience Spurs Underground Upswing

Surface mining equipment anchored 50.41% of the South Africa mining equipment market in 2024, benefiting from truck and shovel fleets deployed in coal and iron-ore pits. Underground machinery is catching up fast with an 8.61% CAGR, driven by deeper platinum and gold orebodies and Sandvik’s automated drill packages that increase meter-per-shift productivity. Automated crushers and screens also find traction as beneficiation quotas rise under the Critical Minerals Strategy, widening the technology gap between global OEMs and low-cost entrants.

Underground demand strengthens the South African mining equipment market size for high-power loaders and roof-support systems. Meanwhile, drills and breakers remain steady across both mining environments. Environmental rules push haul-truck suppliers to introduce battery or hydrogen variants, aligning with miners’ decarbonization targets and fortifying aftermarket opportunities for advanced powertrain retrofits.

By Automation Level: Manual Dominance, Autonomous Momentum

Although manual rigs and vehicles still claim 75.17% of the South Africa mining equipment market share, fully autonomous assets are scaling at 10.34% CAGR, spurred by safety and productivity mandates. Semi-autonomous platforms are transitional solutions, exposing operators to remote control and data analytics without full workforce displacement.

Automation vendors bundle training and remote diagnostic services to mitigate skills shortages constraining rollouts. OEMs stress ergonomic cabins, digital dashboards, and software over-the-air updates to keep manual fleets competitive and protect revenue while the South African mining equipment market gradually pivots toward autonomy.

By Powertrain Type: Conventional Strength Meets Electric Acceleration

Internal combustion models will still dominate, with an 82.43% share of the South Africa mining equipment market in 2024. Still, battery electric alternatives will grow at an 11.82% CAGR during the forecast period, as green bond finance becomes mainstream. Early adopters such as Anglo American validate performance parity, and suppliers now market modular battery packs and hydrogen retrofit kits.

Hybrid drivetrains bridge infrastructure gaps, allowing miners to cut diesel consumption while charging networks expand. Therefore, the South African mining equipment market accommodates overlapping generations of technology, creating layered demand across maintenance, spares, and digital-monitoring services.

By Power Output: Mid-Range Utility Retains Appeal

Machines under 500 HP claimed 47.42% of the South Africa mining equipment market size in 2024 and continue to grow at a 7.37% CAGR through 2030. Their versatility suits varied pit geometries and mixed-ore deposits. The 500–1,000 HP bracket supports large surface mines, while above-1,000 HP units remain essential for high-volume coal and iron-ore loading despite environmental headwinds.

Suppliers utilize standard chassis designs across various power bands to enhance production efficiency and reduce manufacturing complexities. Additionally, service contracts are structured in tiers based on horsepower class, catering to diverse customer needs and strengthening customer retention by creating a deeper level of dependency on the supplier's offerings.

By Application: Coal Bulk Holds, Minerals Surge

Coal retained a 44.71% share of the South Africa mining equipment market in 2024 amid export commitments to Asia and domestic power demand. Mineral mining, however, is expanding at a 9.39% CAGR due to government-backed critical mineral projects that need sophisticated beneficiation gear.

Platinum, vanadium, and titanium operations demand specialized crushers, mills, and sensor-based sorters. These capital-intensive lines raise average order values and lengthen service relationships, tilting long-term growth of the South African mining equipment market toward mineral applications even as coal delivers near-term volumes.

Geography Analysis

Gauteng hosts the majority of mining input suppliers, forming a dense ecosystem of OEMs, fabricators, and MRO specialists that supports fast turn-rounds for equipment overhauls[3]“Cluster Mapping of Mining Suppliers”, Southern African Institute of Mining and Metallurgy, saimm.co.za. Limpopo, North West, and Mpumalanga remain core production provinces. Limpopo’s Mogalakwena platinum complex, the launchpad for hydrogen haulage trials, stands out as a technology testbed.

The Northern Cape is poised for the strongest growth as titanium, vanadium, and manganese projects receive streamlined licenses. Specialized mineral-processing lines fuel incremental orders for high-pressure grinding rolls, fine-screen circuits, and automated lab equipment. Mpumalanga, dominated by coal, underwrites baseline demand for trucks, shovels, and draglines but suffers from logistics cost inflation as rail constraints worsen.

Western Cape’s engineering clusters contribute automation software, advanced sensor packages, and mechatronics services, partially offsetting technician shortages nationwide. Regional gaps in rail capacity push miners to procure lighter, road-legal PBS combinations, stimulating incremental sales of specialized trailers and containerized loading systems.

Cross-border expansion through the African Continental Free Trade Area presents new growth corridors for Gauteng-based OEMs, who leverage South Africa’s significant share of the continent’s rail backbone to serve copper and cobalt belts north of the Limpopo. Export incentives in the Industrial Policy Action Plan further encourage local manufacturers to establish parts depots in Botswana, Zambia, and the DRC, widening the regional footprint of the South African mining equipment market.

Competitive Landscape

Global heavyweights Caterpillar, Komatsu, and Sandvik anchor premium segments with full-line portfolios, telematics suites, and extensive service networks. Bell Equipment and Barloworld Equipment exploit localization credits and proximity to mines, strengthening bids through faster spares delivery and B-BBEE compliance advantages. Chinese brands undercut pricing in entry-level loaders and trucks, capturing smaller operations and pressuring mid-tier OEM margins.

Strategic activity centers on sustainability and digital integration. Sandvik’s intelligent drilling platform delivers automated bit change and cloud-linked analytics, while Caterpillar partners with Gauteng tech start-ups to embed collision-avoidance modules factory-ready. Finance arms are equally pivotal: green-bond instruments back BEV conversions, and supplier-linked credit lines soften up-front costs for new fleets.

Partnership ecosystems widen beyond traditional sales. Anglo American’s hydrogen haul-truck consortium unites fuel-cell firms, electrolyzer manufacturers, and haulage OEMs, accelerating commercialization cycles. Service differentiation grows as vendors bundle operator training, remote diagnostics, and predictive-maintenance scheduling, a response to acute skills shortages inhibiting automation uptake.

South Africa Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Sandvik AB

Epiroc AB

Bell Equipment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Bell Equipment unveiled its latest lineup of motor graders in Ballito, KwaZulu-Natal, South Africa. The launch event aimed to captivate audiences beyond the earthmoving and surface mining sectors.

- September 2024: Komatsu Mining Technologies has launched a hard rock miner in South Africa, paving the way for its expansion into commodities like industrial minerals, potash, and limestone, moving beyond its traditional focus on coal.

South Africa Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills & Breakers |

| Crushing, Pulverizing & Screening |

| Loaders & Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 - 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills & Breakers | |

| Crushing, Pulverizing & Screening | |

| Loaders & Haul Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 - 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining |

Key Questions Answered in the Report

How large is the South African mining equipment market in 2025?

The South African mining equipment market size is USD 1.27 billion in 2025.

Which equipment segment is expanding fastest?

Underground mining equipment is growing at 8.61% CAGR as miners access deeper platinum and gold reserves.

What drives adoption of battery electric vehicles in mining?

Access to green-bond finance and successful hydrogen haul-truck trials are pushing BEV fleet conversions.

Why is localization important for equipment suppliers?

Industrial Policy Action Plan rules grant procurement preference and incentives to locally assembled machines, boosting domestic manufacturers.

What is the main regulatory driver for safety technology upgrades?

The mandatory adoption of EMESRT Level 9 collision-avoidance systems obliges mines to retrofit or replace older fleets with compliant machines.

Page last updated on: