France Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

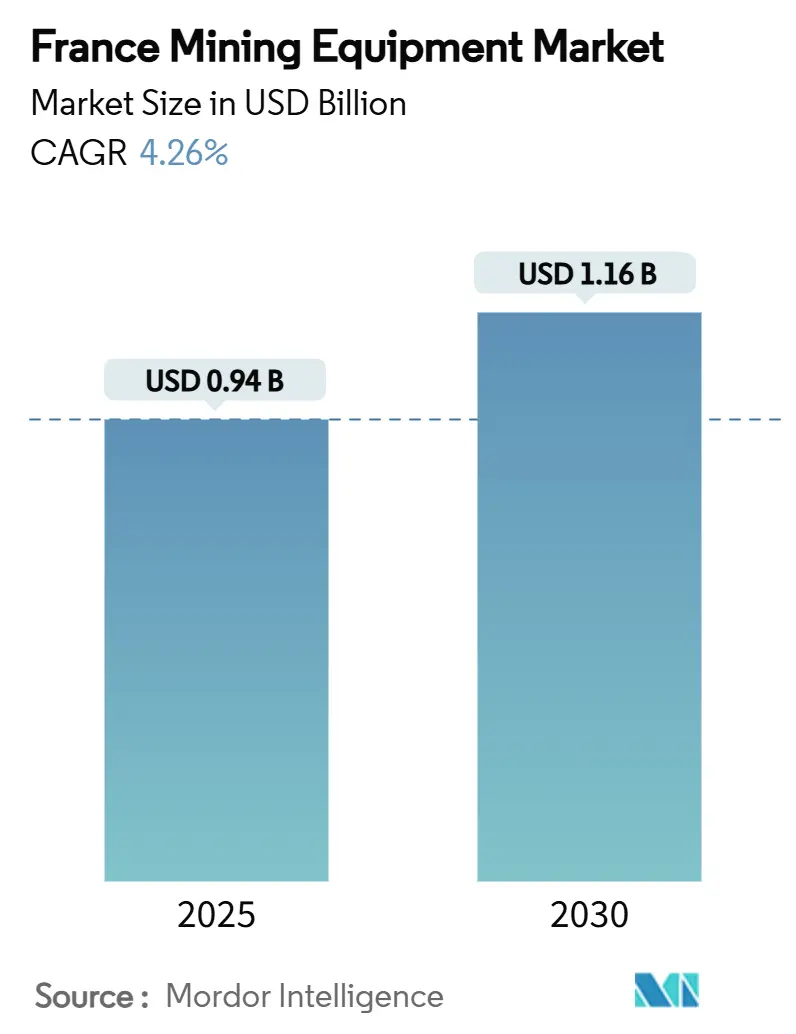

| Market Size (2025) | USD 0.94 Billion |

| Market Size (2030) | USD 1.16 Billion |

| Growth Rate (2025 - 2030) | 4.26% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Mining Equipment Market Analysis by Mordor Intelligence

The France mining equipment market size stands at USD 0.94 billion in 2025 and is forecast to reach USD 1.16 billion by 2030, registering a 4.26% CAGR. This expansion reflects the country’s strategic shift toward critical mineral extraction under the EU Critical Raw Materials Act, accelerating investment in lithium, copper, and rare earth projects. Operators continue to favor diesel machinery, yet battery-electric models are gaining ground as ventilation cost savings and carbon-neutrality targets converge. Simultaneously, the shortage of skilled technicians is spurring automation, with fully autonomous systems securing rapid adoption. Global OEMs leverage long-standing dealer networks, while niche automation firms target white-space opportunities in underground and lithium-processing applications.

Key Report Takeaways

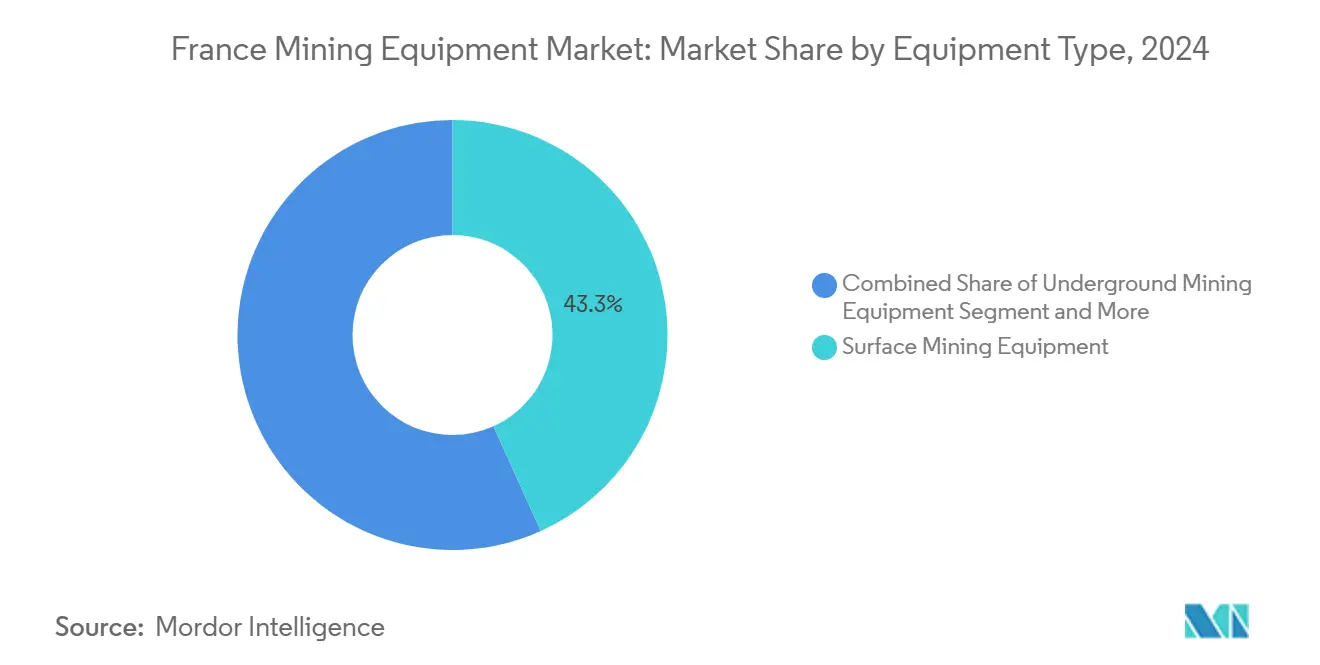

- By equipment type, surface mining led with 43.27% share of the France mining equipment market size in 2024; underground equipment is advancing at a 6.46% CAGR through 2030.

- By automation level, manual machinery held 63.72% share of the France mining equipment market size in 2024, whereas fully automated systems are expanding at an 8.43% CAGR to 2030.

- By powertrain, internal-combustion models dominated, with an 87.62% share of the France mining equipment market in 2024, while battery-electric vehicles posted the fastest 8.28% CAGR through 2030.

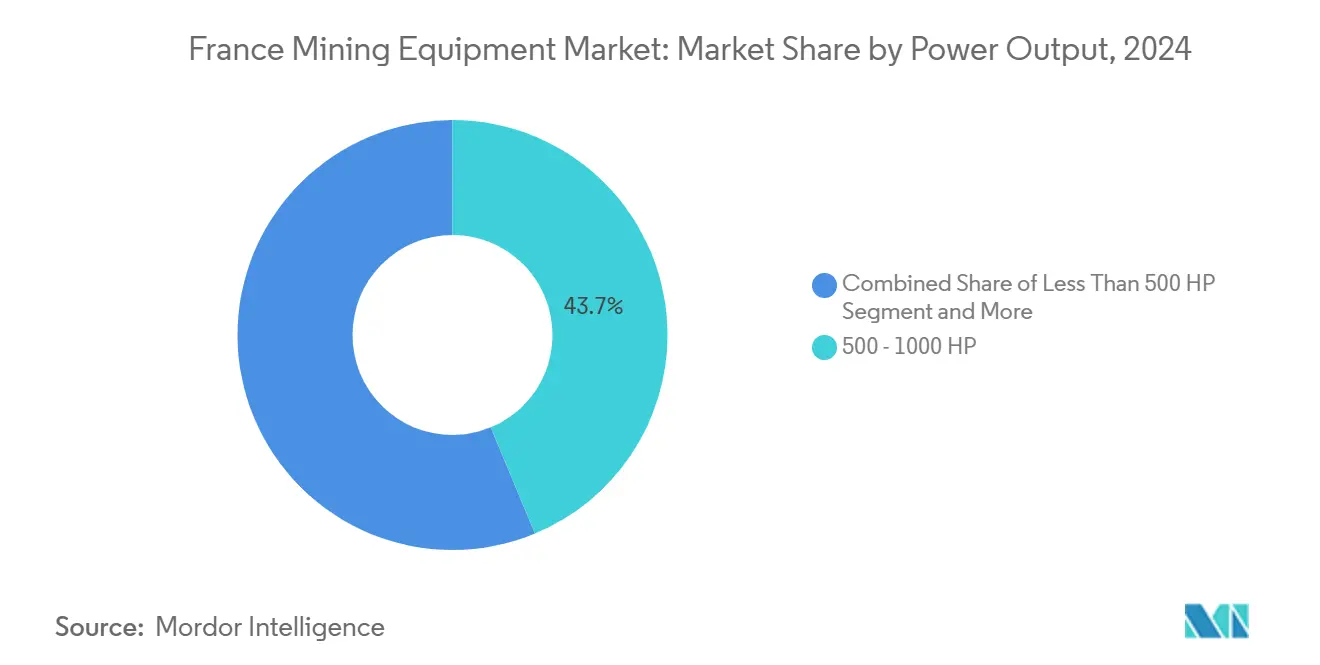

- By power output, the 500-1,000 HP class captured a 43.74% share of the France mining equipment market size in 2024; sub-500 HP units recorded the highest 7.37% CAGR to 2030.

- By application, metal mining accounted for a 52.53% share of the France mining equipment market size in 2024, and mineral mining is growing at a 7.43% CAGR from 2025 to 2030.

France Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CRMA Boosts Domestic Mining | +1.2% | National, with concentration in Allier, Alsace, Lorraine | Medium term (2-4 years) |

| Automation and Electrification Lift Safety and Productivity | +0.8% | National, with early adoption in active mining regions | Long term (≥ 4 years) |

| France 2030 Fund Fuels Critical-Mineral Projects | +0.9% | National, focused on lithium and rare earth deposits | Medium term (2-4 years) |

| Stage V / Euro VI Rules Spur Fleet Renewal | +0.7% | National, affecting all mining operations | Short term (≤ 2 years) |

| BRGM Subsurface Survey Drives Exploration Spend | +0.4% | National, with focus on 5 targeted regions | Long term (≥ 4 years) |

| Copper and Lithium Revival Raises Specialized-Equipment Need | +0.6% | Regional, concentrated in Brittany, Allier, Alsace | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Critical Raw Materials Act Accelerates Domestic Mining Investment

The Act mandates 10% domestic extraction capacity by 2030, cutting permitting times by up to 50% and compressing equipment procurement cycles[1]“Regulation (EU) 2024".establishing a framework for ensuring a secure and sustainable supply of critical raw materials,” European Commission, europa.eu. Equipment suppliers that meet traceability and low-emission criteria are gaining an edge, as operators increasingly align with EU sustainability disclosures. This alignment is driven by the growing emphasis on environmental, social, and governance (ESG) standards, which are becoming critical for businesses to maintain compliance and competitiveness in the market. Furthermore, the legislation spurs regional workforce programs to enhance local employment opportunities and skill development. These initiatives, in turn, are boosting the demand for after-sales services, as a skilled workforce is essential for maintaining and servicing equipment effectively, ensuring operational efficiency and customer satisfaction.

France 2030 Fund Spurs Critical-Minerals Projects

Among the winning bids, Eramet's geothermal lithium project locks in predictable capex phases. This predictability ensures a steady demand for critical equipment such as specialty pumps, brine-handling systems, and sensor suites, essential for the project's operational efficiency. Additionally, compliance criteria now significantly emphasize low-carbon processes to align with global sustainability goals. As a result, vendors offering advanced solutions, such as electric drivetrains and energy-efficient comminution technologies, gain a competitive edge by scoring higher during evaluations. These technologies not only meet regulatory requirements but also contribute to reducing the overall environmental footprint of such projects.

Automation and Electrification Boost Safety-Productivity Economics

Recruitment bottlenecks affect projects in mining basins, intensifying interest in autonomous haulage and drill rigs. Automation delivers productivity gains and mitigates accident exposure in underground headings. Electrified fleets complement autonomy by lowering ventilation costs and cutting diesel particulate emissions to zero, easing compliance with Stage V limits. Lifecycle analysis shows lower operating costs versus diesel, even after accounting for battery replacement. Government carbon-neutrality timelines tip total-cost-of-ownership in favor of automated BEVs, prompting mines to pilot mixed autonomous-electric fleets before full rollout.

Tight NRMM / Euro VI Emissions Rules Drive Fleet Renewal

Stage V standards enforce particulate and NOx thresholds that older engines cannot meet without expensive retrofits[2]“Emissions solutions for Stage V compliance”, Caterpillar Inc., caterpillar.com. The compliance cliff covering engines above 560 kW spurs accelerated scrappage of high-hour units, boosting orders for new loaders and haul trucks equipped with diesel particulate filters and SCR systems. Aligning mining and logistics regulations tightens demand for low-emission support vehicles, further enlarging the total addressable market for clean-diesel and hybrid equipment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX And Long ROI Slow Autonomous / BEV Uptake | -0.8% | National, affecting all mining operations | Medium term (2-4 years) |

| Skilled-technician Shortage Hampers Advanced Systems | -0.6% | National, acute in mining basins | Long term (≥ 4 years) |

| Coal Phase-out Reduces Demand For Legacy Machinery | -0.5% | National, concentrated in former coal regions | Long term (≥ 4 years) |

| Lengthy Consultations Delay Permits Under New Mining Code | -0.3% | National, with regional variations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Domestic Coal Decline Curbs Demand for Certain Machinery

France closed its final primary coal operations in 2024, eliminating longwall systems and washeries that once formed a steady revenue base[3]“Fin de l’activité charbonnière en France”, Cour des Comptes, ccomptes.fr. Demand now centers on niche monitoring gear for subsidence and water management, volumes too slim to offset lost extraction orders. OEMs pivot toward copper and lithium tools, requiring design shifts from bulk-handling equipment to precision crushing and selective mining units. Redevelopment of coal sites into industrial parks adds some earth-moving sales, but at lower power levels, dampening the average unit value.

High CAPEX and Long ROI for Autonomous / BEV Fleets

Capital outlays for fully autonomous BEV haul trucks often triple those of conventional diesel machines, stretching payback to 7-10 years, beyond some operators’ investment horizons. Financing hurdles intensify for smaller mines that lack balance-sheet leverage, even as they face labor shortages that automation could solve. Infrastructure investment for high-capacity charging and grid upgrades further delays breakeven. Vendors counter with leasing models and retrofit kits, yet residual-value uncertainties weigh on adoption speed, tempering near-term demand growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Dominance Drives Underground Innovation

Surface mining accounts for 43.27% of the France mining equipment market's revenue 2024. Demand is anchored in accessible deposits such as Brittany’s andalusite pits, where wheel loaders and hydraulic excavators predominate. The mechanized nature of open-pit work sustains orders for high-capacity haul trucks and drills as exploration extends to lateral ore bodies.

Underground equipment is the fastest-rising category, projected to compound at 6.46% through 2030 as lithium and copper projects deepen. Battery-powered LHDs reduce ventilation costs up to 40%, improving economics for deeper headings. Automation suites—encompassing autonomous drilling and tele-remote bolting—address workforce shortages and enhance safety. Mineral-processing lines also gain traction, with France mining equipment market share for crushers and screens advancing as operators invest in on-site value addition to align with EU strategic-materials policies. This shift from bulk extraction toward refinement fosters growth in high-precision conveying, sorting, and milling systems.

By Automation Level: Manual Operations Face Skilled-Labor Constraints

Manual machinery still accounts for 63.72% of France mining equipment market share in 2024. Most small and mid-scale quarries rely on operator-controlled loaders, drills, and trucks that require limited up-front capex and enable flexible scheduling. However, chronic recruitment difficulties and rising wages intensify automation interest. Semi-autonomous systems provide a stepping-stone, integrating collision-avoidance, payload monitoring, and operator-assist features that lift productivity.

Fully automated fleets record the highest 8.43% CAGR to 2030, catalyzed by vendor financing packages and improved interoperability standards. Mines in Allier and Alsace pilot autonomous drill rigs whose AI-driven pattern optimization trims cycle time and cuts explosives. Training centers launched by OEM dealers bridge the skills gap, offering certification programs for remote operators and data analysts. Improved reliability metrics and uptime are prompting operators to accelerate conversion programs, indicating a pronounced tilt toward autonomy in the next planning cycle.

By Powertrain Type: ICE Dominance Faces Electrification Pressure

Internal-combustion engines represent 87.62% of France mining equipment market share in 2024, yet their share erodes under dual pressure from emission compliance and fuel-price volatility. The France mining equipment industry recorded its first bulk order for 60-tonne battery-electric haul trucks in 2025, signaling mainstream acceptance. BEV adoption rises fastest in underground headings, where eliminating diesel particulates allows operators to downsize ventilation fans. Hybrid power-splits serve as transitional options in surface pits lacking grid capacity.

France's mining equipment market size linked to BEVs is forecast to expand at an 8.28% CAGR through 2030, propelled by the critical metals fund that co-finances electrified fleets and charging stations. Component suppliers benefit from rising demand for high-voltage drivetrains, thermal-management modules, and fast-charge connectors. In parallel, clean-diesel engines with advanced DPF and SCR packages secure orders from operators opting for lower-risk compliance strategies.

By Power Output: Mid-Range Equipment Serves Diverse Applications

Equipment in the 500-1,000 HP envelope captures 43.74% of the France mining equipment market size in 2024, thanks to its versatility across quarry, open-pit, and underground haulage duties. They balance productivity with maneuverability, making them the default choice in medium-scale lithium and andalusite pits. Sub-500 HP units exhibit the sharpest 7.37% CAGR through 2030, underpinned by selective mining of narrow veins and the proliferation of autonomous micro-fleets that spread operating risk.

Above-1,000 HP equipment remains niche, confined to large limestone and iron-ore operations. However, OEMs have introduced hybrid drive modules to cut idle fuel burns in oversized trucks, nudging the total cost of ownership downward. The power-output trend mirrors an operational philosophy of deploying multiple right-sized units rather than single oversized machines, enhancing flexibility and uptime.

By Application: Metal Mining Leadership Drives Mineral Acceleration

Metal-mining applications represented 52.53% of France mining equipment market share in 2024. Copper redevelopment in Brittany’s Armorican Massif and rare-earth processing at Lacq sustain healthy demand for smelter-grade crushers and autoclaves. Demand is bolstered by defense-sector requirements for high-purity alloys, encouraging investment in precision comminution and sorting solutions.

Mineral mining shows the fastest 7.43% CAGR to 2030. Andalusite operations at Glomel, supplying a significant portion of the world's output, prompt steady orders for blast-free extraction tools and magnetic separators. Coal-related machinery declines, with residual demand limited to site-rehab earthmovers and water-quality monitoring packages. Equipment vendors refocus R&D toward specialty minerals, integrating inline analytics and modular processing skids to shorten commissioning times.

Geography Analysis

Regional demand clusters around Brittany, Allier, and Alsace, home to producing or near-term lithium and andalusite mines. Alsace hosts Europe’s first geothermal-lithium brine operation, which requires corrosion-resistant pumps and high-temperature heat exchangers.

Former iron-ore and coal regions such as Lorraine and Nord-Pas-de-Calais are shifting to remediation and potential re-exploration, purchasing monitoring drones and ground-stability sensors, yet accounting for a modest share of France's mining equipment market revenue. Regional permitting sophistication varies: Alsace offers expedited geothermal approvals, while Brittany enforces longer public consultations, influencing delivery schedules.

Infrastructure readiness favors established basins: Brittany and Lorraine possess rail spurs and maintenance depots dating from historical mining, cutting logistics costs for new entrants. Conversely, Allier requires grid upgrades to accommodate high-capacity BEV chargers, prompting joint ventures between mines and utilities. Government co-funding programs offset part of the capex, accelerating site electrification and enabling faster BEV deployment.

Competitive Landscape

France mining equipment market exhibits moderate consolidation, with Caterpillar, Komatsu, and Sandvik anchoring a significant amount of revenue through dealer reach, parts availability, and financing packages. Komatsu’s 2024 roadmap commits to net-zero by 2050, fielding hybrid haul trucks and Smart Construction digital suites.

Meanwhile, niche firms like Aramine specialize in narrow-vein electric LHDs, addressing sub-500 HP growth pockets. Start-ups backed by France 2030 explore AI-enabled sorting and modular lithium-processing skids, threatening to disrupt incumbent aftermarket dominance.

OEM strategies prioritize integrated offerings: hardware, software, and lifecycle services under a single contract. This bundled value proposition mitigates buyer risk in adopting unproven technologies. Partnerships with utilities and telecom operators emerge to deliver site electrification and private 5G, reinforcing equipment interoperability and data analytics. Overall, competitive intensity hinges on technology leadership rather than capacity, rewarding players that can compress commissioning time and reduce the total cost of ownership.

France Mining Equipment Industry Leaders

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Sandvik AB

-

Epiroc AB

-

Liebherr-International AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Imerys launched the EMILI lithium mica mining project at the Beauvoir site, investing over EUR 1 billion (USD 1.17 billion) to produce 34,000 t of lithium hydroxide annually by 2028.

- March 2025: Under the Critical Raw Materials Act, the European Commission has committed EUR 22.5 billion to 47 Strategic Projects spanning extraction, processing, and recycling.

- April 2024: France announced measures to revive copper mining and expedite lithium and geothermal permits to halve research-permit timelines.

France Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills and Breakers |

| Crushing, Pulverizing and Screening |

| Loaders |

| Mining Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 - 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills and Breakers | |

| Crushing, Pulverizing and Screening | |

| Loaders | |

| Mining Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 - 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining |

Key Questions Answered in the Report

What is the current value of the France mining equipment market?

It is valued at USD 0.94 billion in 2025 and is projected to reach USD 1.16 billion by 2030.

Which equipment segment is growing the fastest in France?

Underground mining machinery posts the highest 6.46% CAGR through 2030 as deeper lithium and copper projects scale.

How do Stage V emissions rules influence equipment demand?

They accelerate fleet renewal toward new diesel models with particulate filters and stimulate interest in battery-electric alternatives to meet compliance.

Why is automation gaining momentum in French mines?

Labor shortages, with majority of the basin projects struggling to hire technicians, combined with safety and productivity gains, drive rapid autonomous adoption.

Which regions generate the most equipment demand?

Brittany, Allier and Alsace lead due to active andalusite production and large-scale lithium projects backed by national and EU funds.

Page last updated on: