South Korea Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

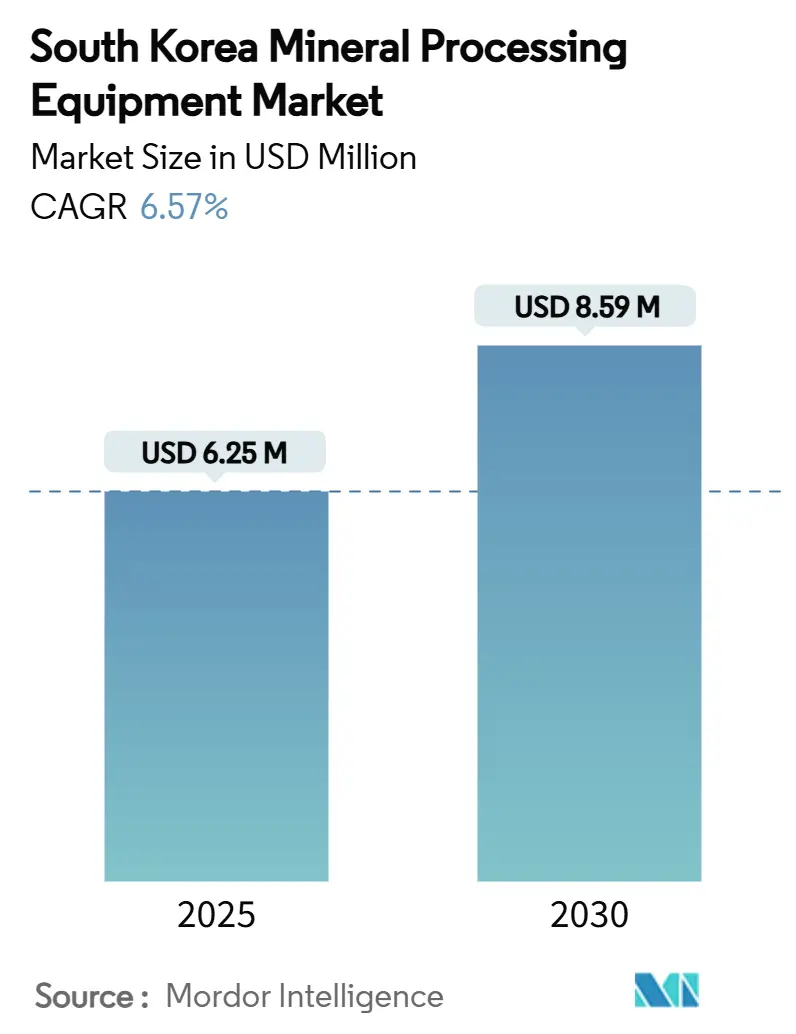

| Market Size (2025) | USD 6.25 Million |

| Market Size (2030) | USD 8.59 Million |

| Growth Rate (2025 - 2030) | 6.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Mineral Processing Equipment Market Analysis by Mordor Intelligence

The South Korea mineral processing equipment market size stands at USD 6.25 million in 2025 and is projected to reach USD 8.59 million by 2030, translating into a 6.57% CAGR over the forecast period. Accelerated investment in domestic battery-metal supply chains, rapid adoption of digital process automation, and policy-led capital incentives collectively underpin the near-term trajectory of the South Korea mineral processing equipment market. Public-sector funding for critical-mineral technologies is mandatory, as tailings-dam upgrades amplify demand for high-efficiency dewatering systems across active mines. Medium-scale quarry operators adopt semi-automated crushing circuits to comply with tightening emission norms. In contrast, blue-chip battery-metal producers allocate capex to fully-automated grinding, classification, and filtration platforms that trim cycle times and energy intensity. As equipment lifecycles exceed 15 years, aftermarket service contracts evolve into a strategic profit center for OEMs and domestic fabricators alike, reinforcing a hybrid ecosystem where imported core technologies merge with local engineering expertise.

Key Report Takeaways

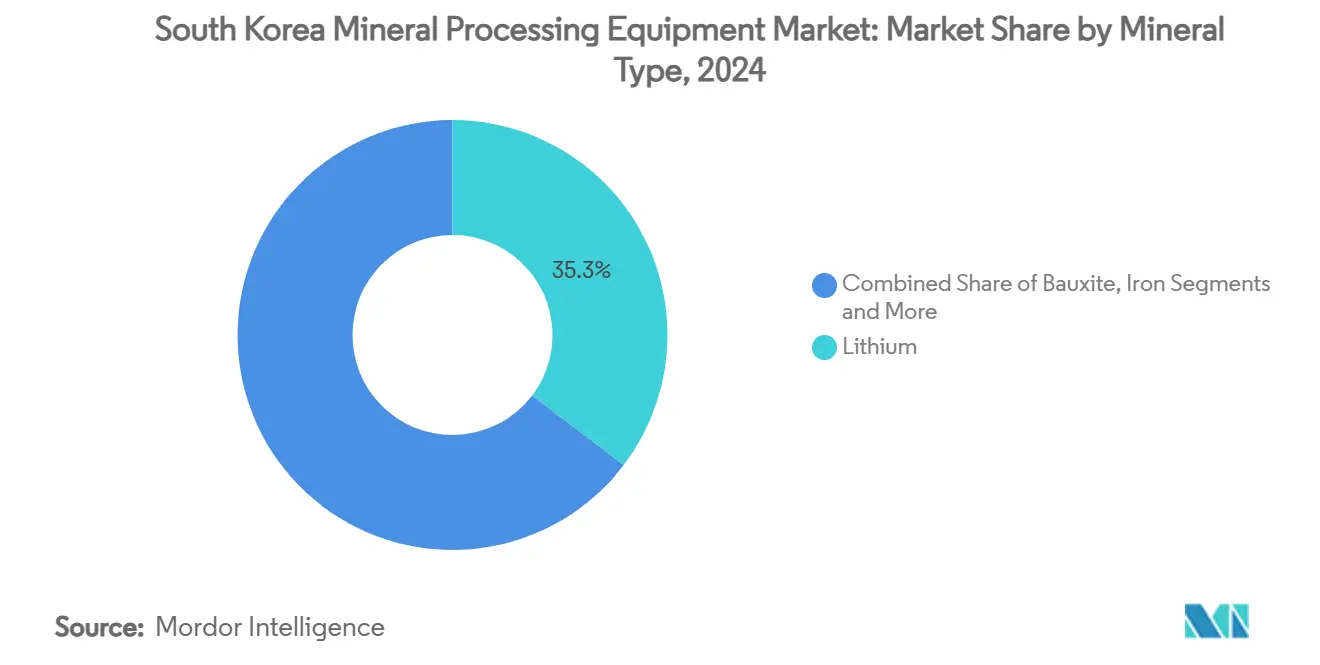

- By mineral type, lithium held 35.34% of the South Korea mineral processing equipment market share in 2024, while rare-earth oxides are forecast to expand at a 9.46% CAGR through 2030.

- By equipment type, crushers commanded 28.72% of the South Korea mineral processing equipment market size in 2024, whereas tailings dewatering systems are slated to advance at a 9.23% CAGR up to 2030.

- By mining method, surface operations represented 64.26% of 2024 revenue, yet underground mining is projected to lead growth at a 10.28% CAGR through 2030 as automation lowers subsurface extraction risk.

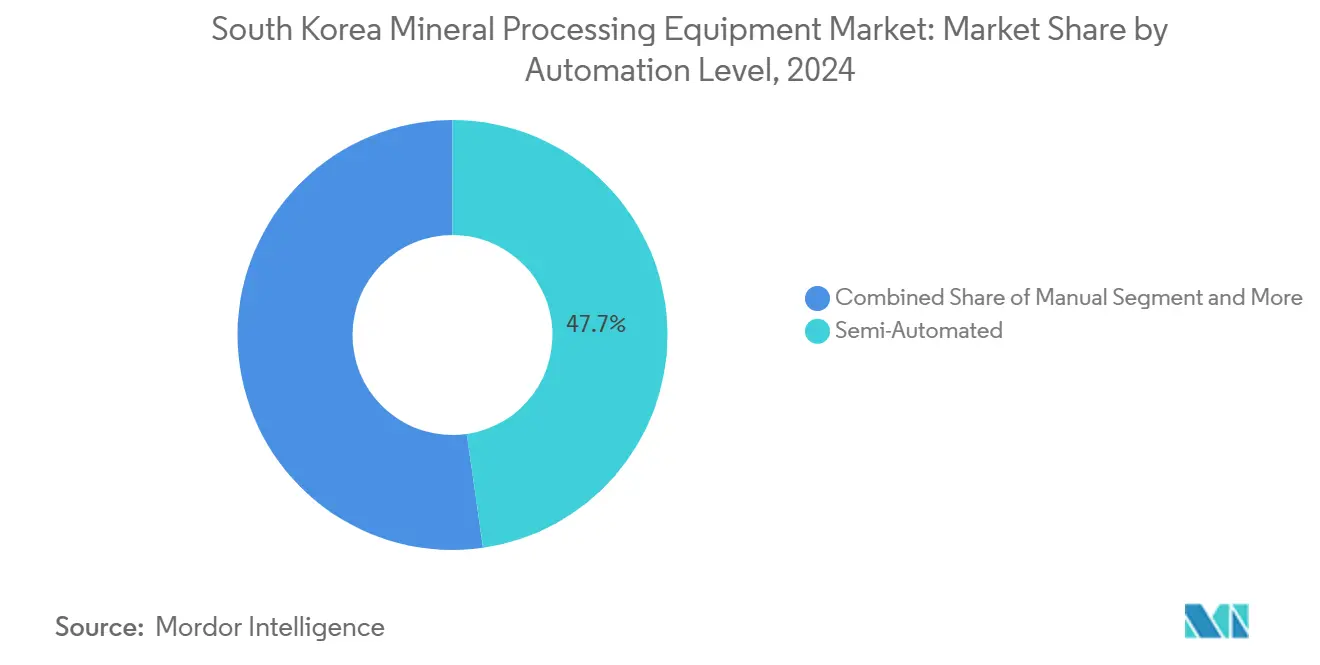

- By automation level, semi-automated lines controlled 47.74% of 2024 revenue, but fully-automated installations are set to post a 10.37% CAGR, mirroring the national digital-manufacturing roadmap.

- By procurement model, new-equipment purchases captured 71.19% of 2024 value, although aftermarket and spare-parts services are expected to grow faster at 9.43% CAGR to 2030.

Relative standing becomes clear only when country-level and regional contributions are evaluated alongside one another at a global level. Mordor Intelligence's mineral processing equipment market share coverage captures this comparative structure.

South Korea Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery-metal Boom | +1.8% | Gyeonggi and Gangwon provinces | Medium term (2-4 years) |

| Fiscal Incentives | +1.2% | Nationwide, strategic mining regions | Short term (≤2 years) |

| Recycling Demand | +0.9% | Industrial clusters in Gyeonggi and South Chungcheong | Medium term (2-4 years) |

| Tailings Upgrades | +0.7% | Active mining areas, notably Gangwon Province | Long term (≥4 years) |

| Strategic Stockpiling | +0.6% | National reserves and processing facilities | Long term (≥4 years) |

| AI Condition Monitoring | +0.4% | Advanced mining operations nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Mineral Production for Battery-Metal Supply

South Korea’s electrification strategy triggers a cascade of mineral-processing investments, especially in lithium hydroxide, nickel sulfate, and rare-earth extraction lines. POSCO’s KRW 760 billion lithium-hydroxide complex in Gwangyang targets 43,000 tons per year and relies on robust crushing, milling, and hydrometallurgical modules[1]“Gwangyang Lithium Hydroxide Project Update,”, POSCO Holdings, posco.com. National procurement programs prioritizing 10 strategic minerals ensure multi-year demand visibility for separation, filtration, and drying units. Also, each additional battery-precursor refinery stimulates parallel orders for feeders, conveyors, and bagging stations, creating a multiplier effect across the South Korean mineral processing equipment market. Government targets to cut critical mineral import dependence from 80% to 50% by 2030, further cementing a stable pipeline of green-field and brown-field equipment contracts.

Expansionary Fiscal Incentives for Domestic Mining Modernization

The Corporate Growth Ladder Establishment Plan approves KRW 200 billion in subsidies with up to 80% ceilings for strategic mining equipment upgrades, accelerating project feasibility for small and medium-sized processors[2]“Tax Credit Expansion for High-Tech Equipment,”, Ministry of Trade, Industry and Energy, motie.go.kr. Seven-year capital-goods tax holidays lower total installed cost, prompting rapid replacement of legacy cone-crushers with energy-efficient hybrid gyratory units. The Ministry of Trade, Industry, and Energy extends R&D tax credits on advanced flotation reagents, allowing OEMs to co-develop bespoke reagent-to-machine packages. Dedicated low-interest loan windows inside the Growth Ladder Jump-Up Program simplify working-capital cycles, enabling mid-tier equipment shops to scale fabrication of custom screens and cyclones. A newly launched M&A facilitation center streamlines the acquisition of niche automation houses by larger conglomerates, accelerating the diffusion of AI-enabled machine-health analytics throughout regional mines.

Surge in Demand for Industrial By-Product Recycling Plants

A national mandate to elevate mineral-recycling rates from 2% in 2024 to 20% by 2030 unlocks sustained demand for shredders, leach reactors, and hydrometallurgical purifiers configured for urban-mining flowsheets[3]“Urban Mining Economic Impact,”, Korean Society of Mineral and Energy Resources Engineers, ksmer.or.kr. POSCO’s USD 101 million black-mass plant in South Jeolla processes 12,000 tons per year, consuming a full suite of high-g-force cyclones, magnetic separators, and vacuum filters that minimize reagent losses. As semiconductor fabs struggle with gallium and germanium supply risks, secondary-source extraction of critical elements cements the recycling segment as a structural growth pillar for the South Korea mineral processing equipment market.

Mandatory Tailings-Dam Upgrades Boosting Equipment Retrofits

Recent stability audits at Yeonhwa II and Okdong tailings dams reveal pore-pressure anomalies that trigger regulatory orders for real-time piezometer arrays and high-capacity pressure-plate filters. Mines retrofit high-pressure dewatering rolls that achieve approximately 80% dry-solid cakes, cutting freshwater make-up by approximately 60% relative to thickener-based practices. Integrating fiber-optic sensing with SCADA dashboards offers continuous slope-movement detection, ensuring compliance with global best-practice guidelines derived from Canadian and Australian standards. Operators recycle low-grade waste rock through regrind mills and gravity concentrators, extending asset lives and deferring costly green-field disposal sites. These systemic overhauls elevate the installed base of tailings-specific pumps, screens, and ecological monitors, reinforcing a multi-year revenue channel for domestic and international OEMs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GHG and Water Rules | -0.8% | National, stricter enforcement in industrial zones | Short term (≤ 2 years) |

| High Power Tariffs | -0.5% | National, particularly affecting energy-intensive processing | Medium term (2-4 years) |

| Shortage of Mechatronics Technicians | -0.4% | Industrial clusters in Gyeonggi, Gangwon, and Chungcheong provinces | Medium term (2-4 years) |

| Import-Dependence Risk | -0.3% | National, affecting equipment maintenance and replacement cycles | Long ter |

| Source: Mordor Intelligence | |||

Tightening GHG and Water-Discharge Regulations

South Korea’s 2050 carbon-neutral blueprint mandates 20% renewable-energy penetration by 2030, tightening the carbon intensity of mineral grinders, regrind mills, and roasting furnaces. Heavy-metal soil assessments near abandoned mine sites pinpoint arsenic and antimony leachates, forcing operators to install supplemental ion-exchange columns and membrane bioreactors that escalate operating costs[4]“Heavy-Metal Contamination near Abandoned Mines,”, Korea Institute of Geoscience and Mineral Resources, kigam.re.kr. New water-quality rules dictate minimum recycle ratios, compelling tailings operators to upgrade to paste-thickening trains or risk production curtailment. While these interventions elevate environmental performance, they burden cash flows of smaller quarries that struggle to meet upfront compliance outlays. Consequently, some projects defer procurement decisions, dampening immediate equipment order volumes despite long-run sustainability advantages.

Elevated Industrial Electricity Tariffs

Successive tariff revisions since 2024 push grid-power costs above KRW 126 per kWh for mid-voltage users, directly inflating grinding and crushing cost curves at zinc, tungsten, and vanadium plants[5]“Electricity Tariff Trends 2024-2025,”, Korea Energy Agency, energy.or.kr. Korea Zinc’s 2025 earnings guidance cautions a profit squeeze despite higher indium and antimony recovery rates, underscoring the vulnerability of energy-intensive circuits. Process engineers therefore specify variable-speed drives, high-efficiency motors, and ore-breakage simulation software to shave power draw without degrading throughput. Equipment vendors with proven kWh-per-ton metrics gain tender preference, reinforcing technology differentiation within the South Korea mineral processing equipment industry. Nonetheless, if tariff escalations outpace efficiency gains, marginal underground projects could slip below economic break-even, restraining future capex commitments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Type: Battery-metal Demand Sustains Value While Rare-earths Quicken Pace

Lithium equipment led 2024 revenue with a 35.34% South Korea mineral processing equipment market share, anchored by sizeable hydroxide, carbonate, and sulfate projects that feed the nation’s cathode plants. The South Korea mineral processing equipment market size allocated to lithium lines consequently stayed higher than any other mineral category, reflecting reliable order books for crushing, calcining, and purification units tied to electric-vehicle battery supply contracts. Concentrator upgrades at existing spodumene conversion sites and brown-field brine-to-lithium-hydroxide retrofits further widened the installed base of mills, thickeners, and filter-presses. Automation retrofits on brine evaporation ponds lowered reagent use, creating pull for embedded sensors and predictive-maintenance software. Lithium’s capital intensity kept service backlogs robust, enabling OEMs to capture recurring revenue from replacement parts and consumables.

Rare-earth oxides record the fastest trajectory, advancing at a 9.46% CAGR through 2030 as domestic magnet and semiconductor supply chains localize separation capacity. New solvent-extraction circuits with high-gradient magnetic separators lift neodymium-praseodymium yields, prompting rush orders for corrosion-resistant pumps and mixing settlers. Pilot lines for dysprosium-terbium coproducts introduce niche specification skids, while by-product cerium polishing-powder plants create secondary demand for drying and micronizing systems. Government procurement guarantees for strategic-mineral output shorten payback periods on rare-earth projects, reinforcing supplier confidence in multi-year equipment pipelines despite raw-material price volatility.

By Equipment Type: Primary Crushers Dominate Spend as Tailings Technologies Outstrip Growth

Crushers commanded 28.72% of 2024 turnover, cementing their role as the first-stage workhorse across iron, lithium, and tungsten flowsheets. Open-pit operations favored heavy-duty gyratory units rated above 10,000 t/h, whereas underground projects opted for compact jaw crushers fitted with dust-suppression hoods to meet ventilation limits. Power-draw optimization via variable-speed drives reduced kWh-per-metric-ton indices, encouraging retrofits that prolong equipment life cycles beyond 20 years. Standardized crusher modules eased spare-parts logistics for remote mines, enabling distributors to stock universal wear liners and eccentric bushings.

Tailings dewatering systems post the fastest 9.23% CAGR, driven by stricter water-recycle mandates and dam-stability codes. High-pressure plate filters delivering cakes below 15 % moisture displace traditional thickener-pond architectures, shrinking footprints and freeing land for reclamation. Facilities upgrade to smart sensor suites that log underflow density and feed pump vibration, allowing real-time adjustments which cut polymer costs. Dewatered tailings find secondary use in cemented paste backfill, tying dewatering investments to underground productivity gains. As mines seek insurer compliance with global stewardship standards, vendors bundling monitoring software with mechanical packages gain competitive advantage.

By Mining Method: Surface Operations Sustain Volume While Automated Underground Mines Accelerate

Surface mining retained 64.26% share in 2024 because iron-ore, limestone, and aggregates pits rely on cost-efficient truck-shovel fleets and fixed crushing stations. Equipment orders center on high-capacity apron feeders, overland conveyors, and mobile in-pit sizing units that match strip-ratio economics. Environmental upgrades such as fog-based dust suppression and low-emission diesel engines allow operators to satisfy local ordinances without curtailing production rates. Fleet-management software overlays GPS dispatching and payload weighing, improving haul-road cycle times and reducing fuel burn.

Underground mining expands fastest at a 10.28% CAGR as tungsten, molybdenum, and rare-earth deposits move from care-and-maintenance to commercialization. Battery-electric load-haul-dump vehicles with fast-swap packs shrink ventilation power draws, justifying investment in charger-banks and automated traffic-management beacons. Drill-and-blast faces deploy LiDAR-guided jumbo booms, cutting overbreak and saving explosives. Conveyorized ore-handling systems replace diesel trucking in narrow veins, boosting throughput consistency. Autonomous survey drones transmit 3-D cavity scans to mine-planning suites, enabling rapid geotechnical decisions that keep ore extraction aligned with mill feed targets.

By Automation Level: Semi-automated Lines Dominate Today; Full Autonomy Captures Future Gains

Semi-automated plants held 47.74% of 2024 revenue because operators blend human oversight with programmable-logic control of crushers, float cells, and filter presses. Touch-screen HMIs streamline start-up sequences, while plant-wide SCADA dashboards alert teams to bearing-temperature anomalies, containing unscheduled downtime. Hybrid staffing models let firms train technicians for higher-value data roles, easing resistance to technology adoption. Retrofit kits such as optical-ore-sorting add-ons and AI-condition-monitoring servers lengthen equipment life without wholesale replacement.

Fully-automated configurations grow at 10.37% CAGR, spearheaded by green-field lithium refineries and rare-earth separation hubs that value process repeatability. Closed-loop advanced-process-control algorithms balance pH, reagent dosage, and pulp density within narrow windows, protecting product purity needed for battery and semiconductor customers. Robotic sampling labs deliver sub-hour assay turnarounds, accelerating grind-size and reagent adjustments. Digital twins simulate wear profiles on liners and cyclones, allowing just-in-time parts dispatch that cuts inventory costs. As labor scarcity and safety regulations intensify, capex justification for lights-out operations strengthens, lifting demand for integrated automation suites.

By Procurement Model: New Equipment Anchors Spend Yet Lifecycle Services Outpace Growth

New equipment purchases accounted for 71.19% of 2024 spend, reflecting a wave of capacity expansions across lithium conversion, iron-ore beneficiation, and tungsten restart projects. Turnkey EPC contracts bundle engineering, procurement, and commissioning services that fast-track project timelines to meet tight battery-supply milestones. Capital goods benefit from tax holidays and state subsidies, lowering hurdle rates for mine developers. High-throughput primary grinders and flotation cells represent the largest single-line items, often financed under vendor-backed deferred-payment schemes.

Aftermarket and spare-parts services generate a faster 9.43% CAGR through 2030 as operators prioritize uptime over outright replacement. Predictive-maintenance platforms feed vibration and oil-analysis data into cloud-based analytics, triggering autoreplenishment of critical components such as screen panels, pump impellers, and crusher mantles. OEM field teams execute mill-reline campaigns during scheduled shutdowns, capturing labor, tooling, and liner supply in bundled contracts. Performance-based service agreements guarantee throughput or energy-consumption targets, aligning vendor incentives with plant economics. This shift converts once-cyclical capex to steady recurring revenue, deepening supplier–operator collaboration throughout the asset life cycle.

Geography Analysis

Gangwon Province commands iron-ore dominance through the Sinyemi Mine and anchors 96% of national output, driving continuous demand for primary crushers, magnetic separators, and dust-collection systems. Gyeonggi Province evolves into a multi-mineral processing nerve center: lithium-hydroxide plants in Gwangyang, vanadium-magnetite beneficiation at Gwan-in, and the KRW 622 trillion semiconductor mega-cluster push aggregate process-equipment orders to record highs. South Jeolla hosts USD 101 million battery-recycling facilities, creating a specialized pull for black-mass shredders, solvent-extraction mixers, and high-vacuum drying ovens. Chungcheong provinces complement the mix with uranium pilot plants and coal-washing units that source domestic spiral concentrators, while North Chungcheong’s Ochang complex scales nickel-cobalt sulfate refining lines.

Gyeongsang provinces split functionality: South Gyeongsang focuses on copper, gold, and tungsten concentrators, whereas North Gyeongsang supports POSCO’s vertically integrated steel-and-battery material campus, expanding off-gas cleaning and slag-granulation equipment portfolios. Jeolla’s dual-province dynamic sees North Jeolla advancing molybdenum leaching plants while South Jeolla refines lithium-nickel-manganese precursors; combined, they strengthen logistics synergies through well-connected container ports. Collectively, the geographic mosaic underpins localized equipment demand clusters that allow OEMs to establish regional service hubs within one-day trucking distance, enhancing response times and reducing inventory carrying costs across the South Korea mineral processing equipment market

Analysis of the mineral processing equipment market by Mordor Intelligence is supported by country-level insights for Australia, China, Mexico, Oman, Egypt, Morocco, South Africa, Italy, and Brazil, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The ecosystem balances international scale with local specialization. FLSmidth, Metso, and Sandvik deploy global R&D depth, premium process guarantees, and integrated lifecycle-service offerings, yet rarely undercut Korean peers on lead times for custom parts. Domestic manufacturers—KOTRACK, CRUTEC, and SAMYOUNG PLANT—capitalize on intimate knowledge of local regulatory codes, currency advantages, and flexible fabrication of bespoke jaw-crusher plates and polyurethane screen decks. Atlas Copco’s KRW 60 billion purchase of Kyungwon Machinery embeds air-compression capabilities directly inside Korean value chains, shortening delivery cycles for mine-site compressed-air stations.

Technology capture defines strategic differentiation: Komatsu fields 700+ autonomous haul trucks globally and now pilots battery-electric LHD units adapted for narrow-vein Sangdong stopes, aligning with Korean decarbonization goals. Metso’s pCAM solution integrates precipitation reactors and calcination kilns calibrated to Korean cathode chemistries, ensuring >95% yield consistency. White-space contenders include mid-sized automation boutiques integrating 5G-enabled machine-vision stacks into hydro-cyclone clusters; such offerings promise 4% extra metal recovery, presenting a credible challenge to incumbents in high-grade battery-metal circuits.

Pricing remains disciplined due to high technical-barrier entry, but customer willingness to pay premiums for guaranteed uptime and energy savings sustains EBITA for tier-one OEMs. Local content clauses in government-funded mining projects, however, preserve a significant value for Korean suppliers, encouraging joint-venture licensing formats that fuse foreign process IP with domestic manufacturing. This hybrid model tempers consolidation, maintaining moderate competitive intensity within the South Korean mineral processing equipment industry.

South Korea Mineral Processing Equipment Industry Leaders

Metso Oyj

FLSmidth A/S

Sandvik AB

Weir Group PLC

Komatsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Atlas Copco acquired Kyungwon Machinery Industry Co. for KRW 60 billion (USD 41.23 million), expanding localized compressor production capability.

- January 2025: The Korean government unveiled a KRW 55 trillion (USD 37.83 billion), three-year supply-chain stabilization package, earmarking KRW 25 trillion (USD 17.19 billion) for core R&D, including mineral-processing technologies.

South Korea Mineral Processing Equipment Market Report Scope

| Bauxite |

| Iron |

| Lithium |

| Rare-earth Oxides |

| Others |

| Crushers |

| Mills & Grinders |

| Feeders |

| Conveyors |

| Drills & Breakers |

| Separators (Magnetic, Electrostatic) |

| Screens & Cyclones |

| Tailings Dewatering Systems |

| Others |

| Surface Mining |

| Underground Mining |

| Marine & Dredge Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| New Equipment |

| Aftermarket / Spare Parts |

| By Mineral Type | Bauxite |

| Iron | |

| Lithium | |

| Rare-earth Oxides | |

| Others | |

| By Equipment Type | Crushers |

| Mills & Grinders | |

| Feeders | |

| Conveyors | |

| Drills & Breakers | |

| Separators (Magnetic, Electrostatic) | |

| Screens & Cyclones | |

| Tailings Dewatering Systems | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| Marine & Dredge Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated | |

| By Procurement Model | New Equipment |

| Aftermarket / Spare Parts |

Key Questions Answered in the Report

How large is the South Korea mineral processing equipment market in 2025?

The market is valued at USD 6.25 million in 2025, with a forecast to reach USD 8.59 million by 2030.

Which mineral type commands the biggest equipment demand?

Lithium leads, accounting for 35.34% of 2024 revenue amid rapid battery-metal supply-chain expansion.

Why is underground mining expected to grow faster than surface mining?

Automation advances lower subsurface extraction costs, driving a forecast 10.28% CAGR for underground operations.

How do fiscal incentives support equipment modernization?

Subsidies covering up to 80% of capital spend and seven-year tax holidays accelerate replacement of legacy machinery.

Which procurement model shows stronger growth?

Aftermarket and spare-parts services are expanding at a 9.43% CAGR, reflecting the shift toward lifecycle-service revenue.

Page last updated on: