Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

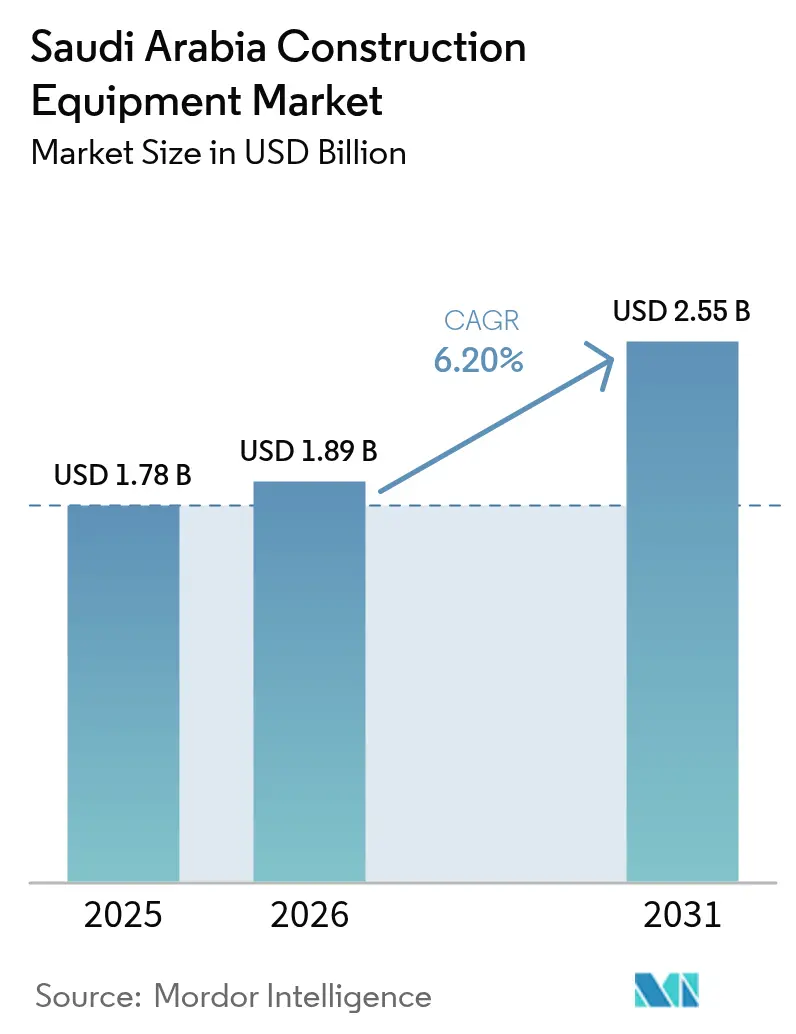

| Base Year Market Size (2025) | USD 1.78 Billion |

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.55 Billion |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Construction Equipment Market Analysis by Mordor Intelligence

The Saudi Arabia construction equipment market size is expected to grow from USD 1.78 billion in 2025 to USD 1.89 billion in 2026 and is forecast to reach USD 2.55 billion by 2031 at 6.2% CAGR over 2026-2031. The expansion is powered by the USD 1.5 trillion Vision 2030 giga-project pipeline, rental-driven fleet optimization, and accelerating demand for earth-moving machines fitted with telematics. Equipment localization incentives, mandatory AI-based safety features in public tenders, and draft Tier-4f emission norms add structural tailwinds. Meanwhile, volatile steel prices, a skilled operator shortage, and grid limitations for on-site charging place measurable, yet manageable, constraints on market velocity. Competitive intensity is rising as Chinese manufacturers gain share through pricing, and global OEMs form Saudi joint ventures to satisfy local-content rules, all of which reshape service models and technology roadmaps in the Saudi Arabia construction equipment market.

Key Report Takeaways

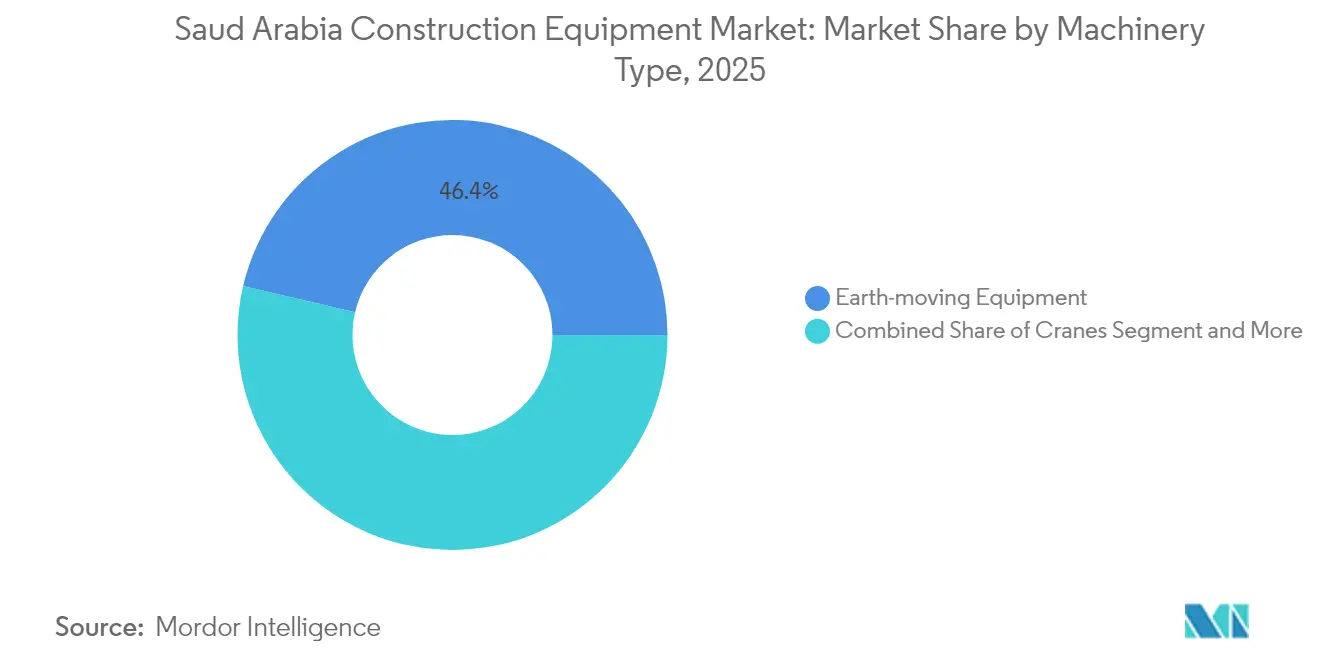

- By machinery type, earth-moving equipment held 46.35% of the Saudi Arabia construction equipment market share in 2025, while excavators are projected to record the fastest 8.30% CAGR through 2031.

- By power source, diesel maintained a 78.95% share of the Saudi Arabia construction equipment market size in 2025, whereas battery-electric equipment is forecasted to grow at a 20.10% CAGR to 2031.

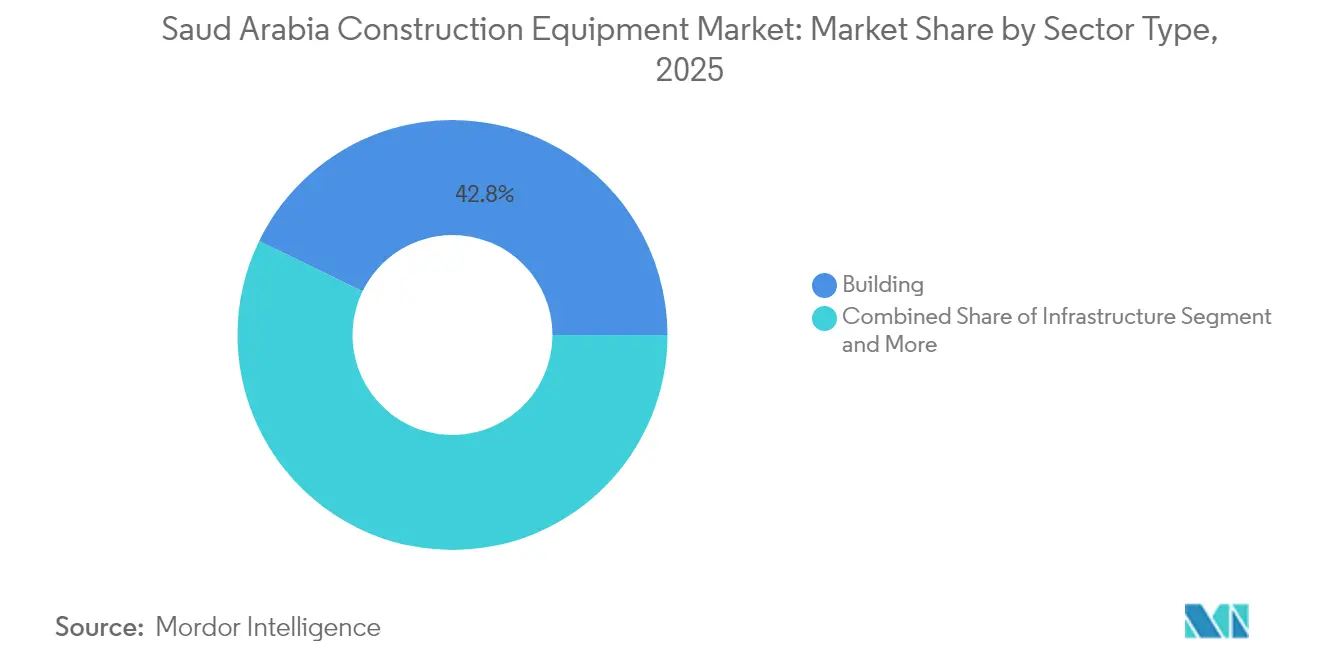

- By sector type, building applications accounted for 42.80% of the Saudi Arabia construction equipment market size in 2025; infrastructure is projected to advance at an 11.10% CAGR through 2031.

- By power output, the 201–400 HP class led with 37.10% of Saudi Arabia construction equipment market share in 2025, while units below 100 HP are projected to exhibit the highest 9.55% CAGR.

- By region, Central Saudi Arabia commanded 35.40% of the Saudi Arabia construction equipment market share in 2025; the Western region is projected to show the strongest 8.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision-2030 Giga-Project Pipeline | +1.2% | Central, Western, Eastern | Long term (≥ 4 years) |

| Demand for NEOM/Red Sea | +0.9% | Western, Northern | Medium term (2-4 years) |

| Rental Preference Cutting Capex and Labour Costs | +0.7% | Central, Western, Eastern | Short term (≤ 2 years) |

| Local-Content Rules | +0.5% | Central, Eastern | Medium term (2-4 years) |

| AI-Telematics Mandate | +0.3% | Central, Western | Short term (≤ 2 years) |

| Tier-4f Emission Norms | +0.2% | Central, Western, Eastern | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision-2030 Giga-Project Pipeline Worth USD 1.5 Trillion

The pipeline of mega-developments such as NEOM, the Red Sea Project, Diriyah Gate, and Qiddiya is recalibrating demand toward high-capacity excavators, autonomous bulldozers, and specialized tunneling rigs. NEOM alone is investing heavily for robotic construction systems, compelling OEMs to integrate AI telematics and remote operation modules into Saudi Arabia construction equipment market offerings. Contractors prefer long-term rental agreements because equipment life cycles trail the multi-decade project timelines, lowering balance-sheet stress while meeting rapid technology refresh needs. Government bond issuances and sovereign wealth fund spending smooth cash-flow visibility, providing contractors with financing certainty that reinforces equipment procurement planning[1]“Giga-Projects Pipeline Overview,” vision2030.gov.sa Source: Public Investment Fund, “Infrastructure Investment Strategy,” Vision 2030 Program, pif.gov.sa.

Earth-Moving Demand for NEOM/Red Sea

NEOM’s 26,500 km² desert terrain requires continuous grading, cut-and-fill operations, and large-scale soil stabilization, driving 24/7 deployment of crawler excavators, articulated dump trucks, and motor graders. Coastal elements of the Red Sea Project call for amphibious excavators and low-vibration piling rigs to protect coral ecosystems. Sustainability clauses built into both projects favor diesel-electric hybrids and battery-powered compact loaders, catalyzing power-source diversification in the Saudi Arabia construction equipment market. Remote locations elevate the value of predictive maintenance software and on-site parts stock, differentiating OEMs with robust service footprints[2]“Sustainable Development Requirements,” NEOM Company, neom.com.

Rental Preference to Cut Capex and Labor Costs

Rental penetration in the Saudi Arabia construction equipment market is rising as contractors hedge against steel-price volatility and compressed project margins. Full-service rental contracts include certified operators, thereby mitigating the Kingdom’s skilled operator shortage and keeping projects in regulatory compliance. Fleet owners scale assets up or down in line with project phases, reducing idle-time overhead. Rental firms are standardizing telematics across mixed OEM fleets, enabling contractors to benchmark machine utilization and fuel burn, which further strengthens the rental value proposition in cost-sensitive bids.

Local-Content Rules Driving OEM Localization

Saudi-made content thresholds incentivize global OEMs to assemble excavators, tower cranes, and concrete pumps within the Kingdom. Partnerships with domestic industrial groups give OEMs duty exemptions and preferential treatment in public tenders. Local sourcing requirements extend to hydraulics, undercarriage components, and control software, injecting new revenue potential for Saudi suppliers and shortening lead times for end-users. SASO certification aligns localized production quality with international standards, ensuring machines remain export-eligible to the wider Middle East and North Africa region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Steel and Freight Prices | -0.8% | Central, Eastern, Western | Short term (≤ 2 years) |

| Skilled Operator Shortage | -0.6% | Central, Western, Eastern | Medium term (2-4 years) |

| Grid Limits | -0.4% | Western, Northern | Medium term (2-4 years) |

| Water Scarcity | -0.3% | Northern, Eastern | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel and Freight Prices

Surging global steel benchmarks raise manufacturing costs for excavator booms, crane masts, and chassis frames. Though new Saudi steel capacity aims to inject supply stability, rapid infrastructure demand keeps domestic prices elevated, compelling OEMs to implement quarterly price surcharges. Ocean-freight spikes tied to Red Sea security disruptions layer further cost pressure, nudging buyers toward localized assembly where shipping exposure is limited. Higher acquisition costs speed up the shift to rental contracts, as contractors offload price risk onto fleet owners.

Skilled Operator Shortage

Amendments to the 2025 Labor Law mandate structured training programs for Saudi nationals, yet heavy-equipment operation remains outside traditional engineering curricula. Contractors report bid delays because qualified operators for 200-ton cranes and GPS-guided graders are scarce. OEMs respond by embedding joystick-mode assist, automated grade control, and augmented-reality diagnostics to lower skill thresholds. The skills gap also pushes higher wages, which in turn intensifies demand for autonomous and semi-autonomous machinery within the Saudi Arabia construction equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Earth-Moving Equipment Dominates Mega-Projects

Earth-moving equipment captured 46.35% of Saudi Arabia construction equipment market share in 2025, underscoring its indispensability to desert grading, megacity foundation work, and logistics-corridor construction. Excavators top the growth chart at 8.30% CAGR, empowered by Vision 2030 backlogs that demand high-cycle duty across multiple simultaneous giga-sites. Bulldozers and graders benefit from multi-lane highway projects that interconnect Riyadh, NEOM, and Red Sea corridors, while crawler cranes sustain mid-single-digit growth on the back of vertical mixed-use towers. Concrete pumps and mixers remain essential for residential output bursts, whereas aerial work platforms stake relevance amid stricter worker-safety codes in urban settings.

The machinery mix is trending toward specialized sub-categories. Tunnel borers find niche acceleration in Riyadh Metro extensions, and stone crushers anchor aggregate self-sufficiency drives in Tabuk Province. High-capacity material-handling trucks serve port modernizations at King Abdullah Port, feeding export supply chains. Precision drilling rigs align with renewable-energy park installations, while compact backhoe loaders service urban infill projects. The broader Saudi Arabia construction equipment market therefore demands product diversity, pushing OEMs to widen portfolios and engage in selective local assembly of high-volume models.

By Power Source: Electric Transition Accelerates Despite Diesel Dominance

Diesel engines sustained a wide 78.95% share of the Saudi Arabia construction equipment market in 2025, owing to their high power density and ubiquitous service infrastructure. Yet battery-electric units clock a 20.10% CAGR to 2031, supported by sustainability mandates at giga-projects and falling lithium-ion pack costs. Interim hybrid platforms grow in step with Tier-4f emissions compliance, blending fuel savings with dependable refueling logistics.

Grid constraints at remote Western and Northern job sites complicate rapid electrification, but developers are piloting solar-plus-storage microgrids to solve charging bottlenecks. Hydrogen fuel-cell prototypes are undergoing field trials tied to the Kingdom’s green-hydrogen export ambitions. Diesel OEMs defend market share via telematics-based fuel-efficiency upgrades, while rental companies hedge with blended fleets that meet current diesel demand and emergent electric requirements within the Saudi Arabia construction equipment market.

By Sector Type: Infrastructure Growth Outpaces Building Dominance

Building applications held a 42.80% share of the Saudi Arabian construction equipment market in 2025, feeding Riyadh’s skyline and residential expansions across secondary cities. Nonetheless, infrastructure spending posts an 11.10% CAGR through 2031, powered by 10,000 km of new highways, regional airport upgrades, and nationwide rail connectivity that dovetail with the logistics strategy under Vision 2030. Energy-sector equipment demand stabilizes as combined-cycle power plants and wind farms replace aging oil-fired assets.

Mining requisitions strengthen as the Kingdom unpacks mineral riches ranging from phosphates to rare earths. Sector diversification yields mixed equipment needs: twin-boom tunneling rigs for metro systems, tower cranes for high-rise hotels, amphibious excavators for coastal tourism marinas, and heavy-duty forklifts for petrochemical terminals. Emerging industrial clusters at Ras Al Khair and Jazan call for grader fleets and batching plants, adding multi-year depth to the Saudi Arabia construction equipment market booking pipeline.

By Power Output: Mid-Range Equipment Leads Market Positioning

Machines rated 201–400 HP dominated with 37.10% of Saudi Arabia construction equipment market share in 2025, balancing torque demands with transport and fuel-burn efficiency. Below-100 HP units post the fastest 9.55% CAGR, aided by alleyway projects, smart-city retrofits, and the rental sector’s appetite for versatile skid-steers. The 101–200 HP tranche supports mid-rise commercial builds, while 400-plus HP giants remain staples for mass earth-moving and quarrying, albeit under rising fuel-economy scrutiny.

Product selection is migrating toward intelligent power management. OEMs employ load-sensing hydraulics and idle-shutdown logic to cut fuel consumption across size classes. Operators in densely populated zones gravitate toward compact electric mini-excavators that comply with noise ordinances, while 600 HP bulldozers reserved for NEOM’s backbone infrastructure increasingly feature pre-wired autonomous-ready controls, evidencing a nuanced segmentation of the Saudi Arabia construction equipment market.

Geography Analysis

Central Saudi Arabia preserved a 35.40% share of the Saudi Arabia construction equipment market in 2025 on the strength of Riyadh’s public and private capex cycle. Projects such as New Murabba, King Salman Park, and multiple data-center campuses demand an array of earth-moving and vertical-construction machinery. A mature dealer network ensures rapid parts availability and comprehensive service programs, lowering machine downtime and sustaining long-term fleet utilization. Continuous metro expansions and high-capacity bus corridors reinforce recurrent demand for compact graders, tunnel-boring machines, and road pavers. Steady municipal spending cushions Central region contractors from commodity-price turbulence, sustaining predictable ordering patterns within the Saudi Arabia construction equipment market.

The Western region ranks pole in growth with an 8.30% CAGR through 2031. Coastal topography necessitates specialized amphibious excavators, corrosion-resistant cranes, and low-ground-pressure loaders. Makkah and Madinah’s Hajj modernizations inject seasonal demand peaks for tower cranes, modular accommodation handlers, and rapid-set concrete pumps. Jeddah’s commercial redevelopment, port capacity expansions, and “New Jeddah Downtown” transform the city into a logistics and tourism nexus, requiring a diversified equipment palette and bolstering service footprints. Western region contractors increasingly value rental contracts bundled with OEM maintenance to offset harsh saline operating environments.

Eastern, Northern, and Southern regions deliver moderate yet resilient upside. The Eastern Province leverages petrochemical and steel investments, relying on heavy-duty crawlers, forklifts, and concrete batch plants. Northern corridors benefit from rail extensions toward Jordan and Iraq, stimulating orders for tracklaying machines and ballast regulators. Southern agriculture zones adopt compact tractors, excavators, and self-propelled sprayers to modernize irrigation networks. While these regions lag in dealer density, Vision 2030’s geographic-diversification push continues to unlock distributed demand pockets across the Saudi Arabia construction equipment market.

Competitive Landscape

The Saudi Arabia construction equipment market is moderately fragmented. Caterpillar leads through its joint venture with Zahid Tractor, showcasing the strategic value of integrated sales, rental, and service hubs in Riyadh, Jeddah, and Dammam. Komatsu trails, though fiscal-year unit deliveries dipped because of delayed governmental purchasing cycles, prompting investment in local remanufacturing to fortify after-sales income streams. Chinese brand XCMG advances by fielding cost-competitive loaders and cranes bundled with extended-warranty packages. European tower-crane maker Wolffkran broke ground on an assembly plant, reflecting how local-content mandates reshape fixed-asset localization strategies.

Hitachi Construction Machinery’s high-tonnage ZX890LCH-7G excavator launch introduces bulk-earth-moving competence suited for giga-site basements, signaling larger payload trends in the Saudi Arabia construction equipment market. Competitive differentiation is migrating toward digital service ecosystems. OEMs deploy cloud-based telematics suites for fuel tracking, preventive maintenance, and remote diagnostics. Rental companies like Bin Quraya integrate mixed-OEM data flows into single dashboards, empowering contractors with machine-level cost analytics. Regulatory rigor around SASO certification and AI-based safety systems sets a baseline compliance hurdle, likely nudging smaller import-only entrants to either partner locally or exit.

Green-finance incentives tied to lower-emission machinery create white-space for innovators delivering battery-electric or hydrogen-fuel-cell platforms, reshaping future share dynamics. Long-term, OEMs able to blend technology innovation, local manufacturing, and rental-ready financial solutions are best positioned to defend and grow their footprints. Consolidation remains a credible scenario as capital-intensive localization weeds out suppliers lacking balance-sheet depth, supporting a gradual upward drift in market concentration within the Saudi Arabia construction equipment market.

Saudi Arabia Construction Equipment Industry Leaders

Komatsu Ltd

Volvo Construction Equipment Corporation

Caterpillar Incorporation

Hitachi Construction Machinery Co. Ltd

XCMG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Hitachi Construction Machinery Middle East delivered 7th-generation ZX890LCH-7G excavators to dealer Arabian Truck & Construction Equipment Co (ATEC), targeting heavy-duty excavation and vacuum-lifting tasks.

- June 2025: Wolffkran secured a turnkey contract for 21 tower cranes to build the Prince Mohammed bin Salman Stadium in Qiddiya, with expansion clauses for additional units.

- May 2025: Hyundai Motor Company and the Public Investment Fund broke ground on a USD 500 million vehicle-assembly facility in King Abdullah Economic City, generating incremental equipment demand for plant construction and logistics yards.

- January 2025: Saudi crane-rental specialist Amhec ordered 100 Tadano GR-800EX rough-terrain cranes, marking the largest single Tadano fleet purchase for the GCC region.

Saudi Arabia Construction Equipment Market Report Scope

The Saudia Arabia Construction Equipment Market covers current and upcoming trends with recent technology developments. The report will provide detailed analysis on various areas of the market by machinery type and by sector. The market share of significant construction equipment across the Saudi Arabian market will be provided in the report.

By Machinery Type

| Cranes | |

| Earth-moving Equipment | Motor Graders |

| Excavators | |

| Loaders (Wheel, Backhoe, Skid-steer) | |

| Material Handling Equipment | Telescopic Handlers |

| Forklifts | |

| Bulldozers | |

| Dump Trucks | |

| Aerial Work Platforms | |

| Road Construction Equipment (Pavers, Compactors) | |

| Concrete Equipment (Mixers, Pumps) | |

| Drilling and Foundation Equipment | |

| Stone Crushers and Screening Equipment | |

| Tunnelling Equipment |

By Power Source

| Diesel |

| Hybrid |

| Battery-Electric |

| Hydrogen Fuel-cell |

By Sector Type

| Building (Residential, Commercial, Mixed-use, Airports, Sports) |

| Infrastructure (Roads, Bridges, Rail, Ports, Waste-water) |

| Energy (Oil and Gas, Power and Water) |

| Mining and Quarrying |

| Industrial (Manufacturing, Logistics) |

| Utilities (Desalination, Renewable Energy) |

By Power Output

| Below 100 HP |

| 101 to 200 HP |

| 201 to 400 HP |

| Above 400 HP |

By Region (Saudi)

| Central |

| Western |

| Eastern |

| Northern |

| Southern |

| By Machinery Type | Cranes | |

| Earth-moving Equipment | Motor Graders | |

| Excavators | ||

| Loaders (Wheel, Backhoe, Skid-steer) | ||

| Material Handling Equipment | Telescopic Handlers | |

| Forklifts | ||

| Bulldozers | ||

| Dump Trucks | ||

| Aerial Work Platforms | ||

| Road Construction Equipment (Pavers, Compactors) | ||

| Concrete Equipment (Mixers, Pumps) | ||

| Drilling and Foundation Equipment | ||

| Stone Crushers and Screening Equipment | ||

| Tunnelling Equipment | ||

| By Power Source | Diesel | |

| Hybrid | ||

| Battery-Electric | ||

| Hydrogen Fuel-cell | ||

| By Sector Type | Building (Residential, Commercial, Mixed-use, Airports, Sports) | |

| Infrastructure (Roads, Bridges, Rail, Ports, Waste-water) | ||

| Energy (Oil and Gas, Power and Water) | ||

| Mining and Quarrying | ||

| Industrial (Manufacturing, Logistics) | ||

| Utilities (Desalination, Renewable Energy) | ||

| By Power Output | Below 100 HP | |

| 101 to 200 HP | ||

| 201 to 400 HP | ||

| Above 400 HP | ||

| By Region (Saudi) | Central | |

| Western | ||

| Eastern | ||

| Northern | ||

| Southern | ||

Key Questions Answered in the Report

What is the forecasted value of the Saudi Arabia construction equipment market by 2031?

The market is expected to reach USD 2.55 billion by 2031, growing at a 6.2% CAGR.

What is the market size of the Saudi Arabia construction equipment market in 2026?

The market size is USD 1.89 billion in 2026.

Which machinery type currently holds the largest share in Saudi Arabia?

Earth-moving equipment leads with a 46.35% share.

Which power source is growing fastest in the Kingdom’s construction equipment space?

Battery-electric equipment is projected to expand at a 20.10% CAGR through 2031.

Which region is the fastest-growing market within Saudi Arabia?

The Western region, driven by Red Sea and Hajj projects, posts an 8.30% CAGR.

How are local-content rules affecting global OEM strategies?

They push OEMs to establish Saudi assembly plants and source components locally to qualify for public-tender advantages and tariff relief.

What is the biggest short-term restraint on market growth?

Volatile steel and freight costs reduce purchasing budgets and encourage rental over ownership.

Page last updated on: