Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 22.56 Billion |

| Market Size (2026) | USD 23.26 Billion |

| Market Size (2031) | USD 27.10 Billion |

| Growth Rate (2026 - 2031) | 3.10% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Kuwait Retail Market Analysis by Mordor Intelligence

The Kuwait retail market size is expected to grow from USD 22.56 billion in 2025 to USD 23.26 billion in 2026 and is forecast to reach USD 27.1 billion by 2031 at a 3.1% CAGR over 2026-2031, which frames the Kuwait retail market size and its expected trajectory. Households are blending physical store visits with digital checkouts as instant payments scale, which is reshaping footfall patterns and digital conversion in core governorates that anchor the Kuwait retail market. Expatriates constitute the bulk of the workforce, which sustains consumption velocity across key categories and supports higher transaction frequency in modern formats central to the Kuwait retail market [1]Times Kuwait, "Expats account for over three-quarter of workforce," Times Kuwait, timeskuwait.com. Proposed mortgage legislation would unlock long-term credit and reallocate household spending toward home-linked categories, amplifying downstream retail demand for furnishings, appliances, and electronics that define the Kuwait retail market. Operators are rebalancing store networks and supply chains to absorb imported inflation and secure resilience amid supply cost swings, while leveraging payment rails and loyalty ecosystems to sustain share in the Kuwait retail market. Franchise realignments, including brand exits and local rebranding, also underscore the critical role of portfolio agility in protecting margins and maintaining assortment breadth in the Kuwait retail market.

Key Report Takeaways

- By product, Food, Beverage, and Tobacco led the Kuwait retail market with 46.19% share in 2025; Pharmaceuticals, Luxury Goods, and Others are forecast to expand at a 5.04% CAGR through 2031.

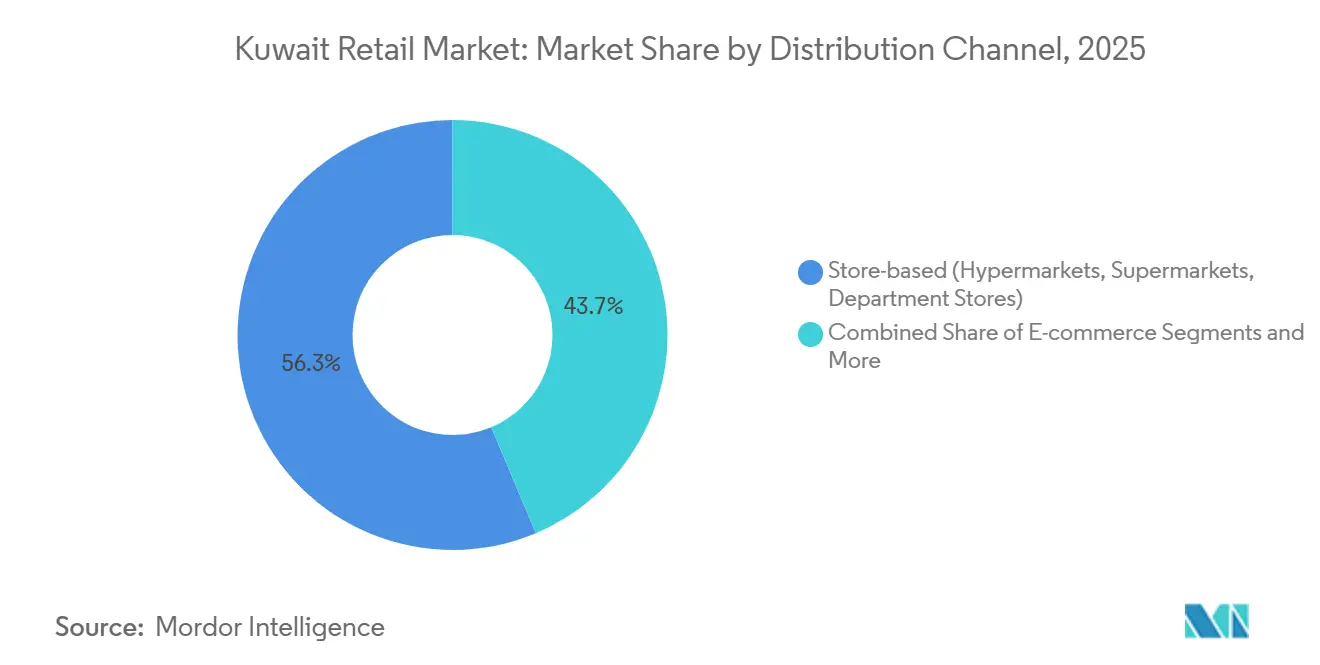

- By distribution channel, the store-based format held 56.34% of the Kuwait retail market share in 2025, while e-commerce posted the highest projected CAGR at 5.13% through 2031.

- By geography, Kuwait City Governorate accounted for a 43.43% share of the Kuwait retail market size in 2025, while Hawalli is advancing at a 5.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kuwait Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes driving youth-centric market growth | +0.8% | Global, with concentration in Kuwait City and Hawalli governorates, hosting professional and expatriate cohorts | Medium term (2-4 years) |

| E-commerce and omni-channel ecosystem expansion | +0.7% | Global, early gains in Kuwait City, Hawalli, Farwaniya | Short term (≤ 2 years) |

| Expatriate workforce boosting consumer market demand | +0.6% | Global, spill-over to all governorates as expatriates disperse across residential zones | Short term (≤ 2 years) |

| Mortgage law unlocking consumer credit opportunities | +0.5% | National, with early gains in suburban governorates such as Al Mutlaa and Sabah Al Ahmad | Medium term (2-4 years) |

| Vision 2035: infrastructure and government reforms | +0.4% | National infrastructure corridors, with retail adjacency in the Capital, Ahmadi, and Jahra | Long term (≥ 4 years) |

| Retail-media networks creating revenue growth opportunities | +0.1% | Global digital reach, with physical nexus in high-traffic malls in Kuwait City and Hawalli | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes Driving Youth-Centric Market Growth

Kuwait’s population reached 5.1 million in mid-2025, boosting the consumer base that retailers target, with value and premium ranges aligned to income cohorts. The age structure skews young, and the large working-age share creates favorable conditions for multi-year consumption growth as cohorts move through peak earning periods. Non-oil real activity improved in 2025, which supported household purchasing power and helped stabilize discretionary spending categories targeted by modern trade. The Central Bank of Kuwait reduced its discount rate to 3.75% in September 2025, lowering borrowing costs and favoring big-ticket categories such as electronics and home goods [2]Central Bank of Kuwait, “Press Statement on Economic, Financial and Banking Developments,” Central Bank of Kuwait, cbk.gov.kw. Spending normalization from elevated post-pandemic baselines remains a near-term feature, yet retailers that tailor assortments to youth preferences and rising income tiers sustain volume and category mix gains.

E-Commerce and Omni-Channel Ecosystem Expansion

Instant payments launched in June 2024 through the WAMD system and grew to over 1 million registered accounts within a year, accelerating a structural shift toward electronic and contactless transactions across retail journeys. Point-of-sale transactions increased in 2025, while cash withdrawals declined, confirming greater digital acceptance among both consumers and merchants. Major chains are scaling online fulfillment and robotics to improve pick accuracy, reduce cycle times, and support same-day delivery, which boosts conversion rates for Click and Collect and ship-from-store services. Retailers with strong loyalty ecosystems and first-party data are monetizing audiences through retail media placements that complement low-margin categories, supporting profitability as digital penetration inches up. Friction-reducing features such as QR-code point-of-sale and Request-to-Pay are expected to deepen adoption, thereby sustaining the channel’s growth advantage in the Kuwait retail market.

Expatriate Workforce Boosting Consumer Market Demand

Expatriates account for most private-sector employment, which anchors steady spending on food, apparel, electronics, and household goods. Remittance outflows rose in 2025, which signals strong labor-market conditions despite the outbound transfer of income, and the associated wage base still supports daily and weekly consumption cycles. Infrastructure activity linked to national development plans boosted demand for skilled and unskilled labor, expanding the consumer base in suburban catchments near new housing and logistics corridors. Category preferences among expatriate cohorts sustain high velocity in essentials and grow wallet share for convenience and quick-commerce formats, strengthening format diversity across the Kuwait retail market. Retailers with deep private-label programs and supplier partnerships can hold prices under import pressure, helping retain expatriate shoppers who are price-sensitive but convenience-oriented.

Retail-Media Networks Creating Revenue Growth Opportunities

Omnichannel leaders built first-party data assets through loyalty programs and fulfillment upgrades, which enable high-margin advertising placements and sponsored listings that complement low-margin grocery and commodity lines. Loyalty linkages to the majority of transactions create closed-loop attribution, which is attractive to brand partners seeking measurable conversions and category lift in the Kuwait retail market. As WAMD expands features such as QR-code point-of-sale and Request-to-Pay, retailers add more deterministic identity signals, enhancing audience addressability and supporting media monetization. Kuwait’s population scale places a natural cap on total media budgets, yet high mall footfall and strong digital penetration in affluent catchments deliver high-quality reach, sustaining retail media growth despite a smaller base than those of larger Gulf peers. This revenue stream is becoming a structural lever to protect margins as input costs and rents rise, which supports more resilient earnings models across leading chains in the Kuwait retail market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy dependence on imports and cost volatility | -0.6% | National, with port-dependent governorates such as Ahmadi and Al-Jahra exposed to freight-cost pass-through | Short term (≤ 2 years) |

| Prime mall saturation and increasing rental costs | -0.4% | Kuwait City CBD and Salmiya in Hawalli, where ground-floor rents exceed KD 30 per sqm monthly | Medium term (2-4 years) |

| Cross-border shopping reduces local sales revenue | -0.3% | Global digital reach, with stronger effects in tech-savvy cohorts in Kuwait City and Hawalli | Short term (≤ 2 years) |

| Shortage of digital talent in retail logistics | -0.2% | National workforce challenge, acute in fulfillment clusters in the Farwaniya industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heavy Dependence on Imports and Cost Volatility

Kuwait depends on imports for many basic commodities, which expose retailers to global price cycles, freight spikes, and currency-linked pass-through, affecting shelf prices and basket composition. Headline inflation moderated in 2025, yet food and beverage prices continued to rise faster than the general index, tightening real purchasing power and tilting spending toward essentials in the Kuwait retail market. Energy-cost dynamics influence maritime rates and logistics fees, which filter into retail pricing even when large chains use hedging or direct-sourcing buffers. Merchants respond with assortment edits, private-label substitutions, and supplier negotiations to manage unit economics, stabilizing price perception but not fully offsetting external cost shocks. Inflationary pressure remains a headwind for discretionary categories with elastic demand, slowing premium upgrades outside essential categories in the Kuwait retail market.

Cross-Border Shopping Reduces Local Sales Revenue

Online spending measured across websites and digital platforms decreased from 2024 to 2025, which analysts in Kuwait partly attribute to cross-border purchases that bypass domestic retailers. The strength of the dinar and subsidized or free international shipping on large platforms encourage purchases of electronics, apparel, and specialty goods outside Kuwait, diluting local e-commerce share despite higher digital usage. POS growth alongside a dip in online totals indicates fragmented spend across geographies, complicating inventory and pricing strategies for domestic players in the Kuwait retail market. Domestic payment infrastructure improvements support convenience but do not confer an advantage in cross-border checkout flows, which still run through global card networks and wallets. Local chains compete on speed, localized assortments, omnichannel services, and experiential formats that international marketplaces cannot replicate, making this the near-term playbook to stem leakage in the Kuwait retail market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Essentials Anchor, Premium Health Ascends

Food, Beverage, and Tobacco accounted for 46.19% of value in 2025, supported by large-format chains that scale procurement and pricing for a population where essentials dominate the monthly basket. Grocery leaders have expanded footprints and online capabilities to secure frequency and broaden private-label penetration, which protects value perception as import costs fluctuate across the Kuwait retail market. Pharmaceuticals, Luxury Goods, and Others is the fastest-growing group, with a 5.04% CAGR through 2031, reflecting increased health awareness and premium beauty demand driven by higher female workforce participation and young demographics. Pharmacy networks are expanding into prime locations in malls, co-ops, and clinics, increasing proximity and cross-category discovery and reinforcing this segment’s growth path in the Kuwait retail market. Food price inflation in 2025 pressured household budgets toward essentials, yet premium and wellness sub-categories maintained traction, with loyalty and promotions targeting high-intent shoppers.

Electronics and Home Appliances benefit from the shift in payments and the adoption of instant pay, which supports higher average order values and reduces checkout friction both online and in-store across the Kuwait retail market. Apparel, Footwear, and Accessories are recalibrating assortments between value and premium to match rising youth cohorts who shop frequently in malls and online, helping sustain blended channel growth in Kuwait City and Hawalli. Furniture, Toys, and Hobby shows sensitivity to mortgage policy and housing deliveries, which drive cyclical upgrades in furnishings and kids’ categories as new residential areas populate in the Kuwait retail market. Industrial and Automotive retail ties to logistics and service corridors, which capture maintenance and parts demand as mobility and e-commerce networks expand to new hubs. The Kuwait retail market size for essentials remains the anchor for volume, while premium beauty and health categories lead forecast growth as omnichannel engagement lifts discovery and repeat purchases.

By Distribution Channel: Physical Footprint Yields to Digital Velocity

Store-based channels accounted for 56.34% in 2025, led by hypermarkets and supermarkets, which concentrate on breadth of assortment and price leadership in high-traffic corridors. Retailers are moving toward neighborhood and express formats to ease rent pressure, capture quick trips, and address emerging residential clusters in suburban governorates that are central to the Kuwait retail market. E-commerce is set to grow at a 5.13% CAGR through 2031 as payments become instant and checkout frictions fall, thereby enhancing conversion rates for multi-category platforms and brand sites in the Kuwait retail market. Robotics in fulfillment and scalable delivery fleets are improving speed and reliability, widening the addressable online basket beyond small electronics and beauty products into bulky goods such as furniture and appliances. Direct selling and institutional retail serve targeted needs with high-touch service and contracts, which remain less susceptible to pure-play e-commerce substitution given the service intensity in the Kuwait retail industry.

Franchise portfolios are being restructured when conditions warrant local brand pivots, as evidenced by the 2025 brand transitions that reset operating models and supply partnerships. Store fleets adapt with self-checkout, click-and-collect, and ship-from-store capabilities that improve throughput and user experience, narrowing the differentiation gap with online-only players in the Kuwait retail market. Retailers invest in cybersecurity and compliance aligned with financial-sector standards, which raise fixed costs but improve resilience as more transactions migrate to digital. The Kuwait retail market, tied to store-based retail, still dominates the base, but digital velocity shifts the growth mix toward omnichannel leaders that combine footprint strength with data-driven online capture. Execution depends on last-mile density, digital talent, and loyalty monetization, which together support sustainable growth and share defense in the Kuwait retail market.

Geography Analysis

Kuwait City Governorate captured 43.43% of sales in 2025, driven by destination malls and CBD daytime footfall, which reinforced weekday frequency and high average transaction values in leading complexes. Hawalli is the fastest-growing governorate at a 5.68% CAGR to 2031, supported by dense residential districts and strong convenience corridors that align with quick trips and value formats in the Kuwait retail market. Emerging residential cities in Ahmadi and the south are attracting flagship investment and convenience networks following infrastructure buildout, which improves access and raises spend capture in new catchments. Rents and yields vary by submarket, with prime locations trading at the highest absolute prices, encouraging operators to balance flagship presence with suburban expansion to strengthen coverage of daily missions in the Kuwait retail market.

Policy measures to improve real estate transparency require proof of payment through the banking system for transactions, which supports cleaner underwriting and reduces risk in site-selection decisions for the Kuwait retail market. Commercial land prices remained higher in the capital than in other governorates, with indicative capital-area plots at USD 28,675.9 per sqm (KWD 8,840 per sqm), compared with Hawalli at USD 12,800.4 per sqm (KWD 3,946 per sqm) and Farwaniya at USD 8,833.1 per sqm (KWD 2,723 per sqm), which shapes the economics of format choice and network density [3].Kuwait Finance House, “KFH Local Real Estate Report Q1 2025,” Kuwait Finance House, kfh.com Kuwait City’s role as the administrative and corporate hub sustains higher weekday demand for quick service, convenience, and premium categories, which complements Hawalli’s residential density that supports frequent trips and neighborhood baskets. Suburban expansion targeting Al Mutlaa and Sabah Al Ahmad follows a ten-minute drive coverage strategy, which indicates how retailers balance accessibility and rent dynamics to optimize returns in the Kuwait retail market.

Footfall and spending patterns vary through the week, with CBD office traffic supporting weekday daytime peaks and residential zones driving evening and weekend activity, which encourages tailored labor scheduling and delivery routes in the Kuwait retail market. Operators focused on data-driven site selection are pairing flagship malls with community centers, which helps capture both destination shopping and routine baskets across governorates. As infrastructure completes and mortgage lending unlocks, suburban governorates should gain share incrementally, while the capital maintains its anchor role as the highest-value catchment in the Kuwait retail market. This redistribution benefits chains that plan logistics nodes, last-mile fleets, and omnichannel services that align with household routines and commuting flows in the Kuwait retail market.

Competitive Landscape

Kuwait’s retail sector combines family-owned conglomerates, listed Gulf operators, and specialized franchisees, which produces moderate concentration and a wide variety of operating models in the Kuwait retail market. Omnichannel adoption is advancing through self-checkout, upgraded fulfillment, and loyalty ecosystems, positioning leaders to monetize retail media and personalize assortments to drive higher conversion in the Kuwait retail market. Suburban expansion is a common theme, with new flagships and convenience formats targeting emerging residential clusters to capture daily missions and ease exposure to prime rents. Payment infrastructure upgrades reinforce this omnichannel push and enable faster checkouts, supporting seamless journeys across store and digital channels in the Kuwait retail market.

Strategic moves include franchise brand updates and rebranding when conditions require local control and supplier flexibility, which demonstrates how operators protect price architecture and category depth in the Kuwait retail market. Beauty, fashion, and home categories expanded with first-in-region openings and redesigned flagships, which capture demand from young and high-discretionary-spend cohorts in leading malls. Specialty players in electronics and home remain anchored in physical showrooms while deepening their digital services to preserve consultation-led journeys, reflecting hybrid models in the Kuwait retail industry. Automotive retail groups illustrate vertical integration through showrooms, service centers, and parts distribution, an approach that multi-category retailers study for loyalty and lifecycle value.

Investment in loyalty and media monetization is growing as chains aim to improve the margin mix, reducing reliance on vendor support and discounts for low-margin staples in the Kuwait retail market. Digital and data capabilities remain competitive differentiators, and leaders with stronger engineering and analytics teams deploy faster feature cycles in checkout, personalization, and last-mile optimization. Compliance and cybersecurity standards are rising and increasing fixed costs, yet they also strengthen consumer trust, which is essential as digital penetration in the Kuwait retail market increases. Over 2026, chains that combine footprint strength, digital velocity, and monetizable data are best placed to gain share and protect margins in the Kuwait retail market.

Kuwait Retail Industry Leaders

-

Alshaya Group

-

Lulu Hypermarket

-

The Sultan Center

-

X-cite (Alghanim Electronics)

-

HyperMax (Majid Al Futtaim)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Alshaya Group and Primark inaugurate the first Middle East store at The Avenues, Kuwait. Primark opened its inaugural Middle East flagship at Grand Avenue – The Avenues in October 2025, under Alshaya franchise operations. The retailer announced five additional stores across the UAE, Bahrain, and Qatar in 2026. The expansion indicates confidence in mall-led discretionary spend in Kuwait City.

- October 2025: H&M unveiled a redesigned store at The Avenues, Kuwait, following a full-scale refurbishment. The 15,000-square-foot Grand Avenue store adds immersive fitting rooms, self-checkout, and an expanded beauty assortment. The format upgrade supports omnichannel journeys and re-engagement of young fashion shoppers. The reopening is part of a broader regional refresh in late 2025.

- October 2025: Sultan Center opened its 52nd Kuwait store at Gate Mall, Egaila, advancing toward ten-minute drive coverage. The 2,000-square-meter flagship extends reach into high-density residential zones. The company also committed to three additional flagships across Capital, Ahmadi, and Hawalli in 2026. The strategy pairs large stores with convenience formats to balance basket sizes and trip missions.

- August 2025: Spinneys and Alshaya Group announced a joint venture to enter the Kuwait market with the first store opening in 2026. Spinneys, a Dubai-listed premium supermarket operator, formed a strategic partnership with Alshaya Group to establish ten stores in Kuwait, with Spinneys holding a 51% controlling stake and managing operations. The venture targets Kuwait's affluent consumer base and high disposable income. The partnership marks Spinneys' fourth GCC market after the UAE, Oman, and Saudi Arabia.

Kuwait Retail Market Report Scope

The retail market is the final stage of the distribution chain, where consumer goods such as food, apparel, electronics, and household items are sold directly to end users. The Kuwait retail market combines physical stores, shopping malls, and e-commerce platforms, driven by connected retail models and high-frequency online shopping trends.

The Kuwait retail market report is segmented by product (food, beverage, and tobacco, personal and household care, apparel, footwear and accessories, furniture, toys and hobby, industrial and automotive, electronics and home appliances, pharmaceuticals, luxury goods and others), distribution channel (store-based (hypermarkets, supermarkets, department stores), e-commerce, others (drugstores, institutional retail)), and geography (Kuwait City Governorate, Hawalli Governorate, Farwaniya Governorate, Al-Ahmadi Governorate, Al-Jahra Governorate, Mubarak Al-Kabeer Governorate). The market forecasts are provided in terms of value (USD).

By Product

| Food, Beverage and Tobacco |

| Personal and Household Care |

| Apparel, Footwear and Accessories |

| Furniture, Toys and Hobby |

| Industrial and Automotive |

| Electronics and Home Appliances |

| Pharmaceuticals, Luxury Goods and Others |

By Distribution Channel

| Store-based (Hypermarkets, Supermarkets, Department Stores) |

| Direct Selling |

| E-commerce |

| Others (Drugstores, Institutional Retail) |

By Geography

| Kuwait City Governorate |

| Hawalli Governorate |

| Farwaniya Governorate |

| Al-Ahmadi Governorate |

| Al-Jahra Governorate |

| Mubarak Al-Kabeer Governorate |

| By Product | Food, Beverage and Tobacco |

| Personal and Household Care | |

| Apparel, Footwear and Accessories | |

| Furniture, Toys and Hobby | |

| Industrial and Automotive | |

| Electronics and Home Appliances | |

| Pharmaceuticals, Luxury Goods and Others | |

| By Distribution Channel | Store-based (Hypermarkets, Supermarkets, Department Stores) |

| Direct Selling | |

| E-commerce | |

| Others (Drugstores, Institutional Retail) | |

| By Geography | Kuwait City Governorate |

| Hawalli Governorate | |

| Farwaniya Governorate | |

| Al-Ahmadi Governorate | |

| Al-Jahra Governorate | |

| Mubarak Al-Kabeer Governorate |

Key Questions Answered in the Report

What is the current size and expected growth of the Kuwait retail market?

The Kuwait retail market stands at USD 23.26 billion in 2026 and is projected to reach USD 27.10 billion by 2031 at a 3.10% CAGR, indicating steady expansion across store and digital formats.

Which channels are growing fastest in Kuwait's retail market?

E-commerce is expected to record a 5.13% CAGR through 2031, supported by instant payments, robotic fulfillment, and omnichannel services, while store-based formats remain the value base with network optimization underway.

Which product categories drive sales and growth in Kuwait's retail market?

Essentials remain the anchor with Food, Beverage, and Tobacco leading overall value, while Pharmaceuticals, Luxury Goods, and Others lead forecast growth, driven by premium beauty and health demand.

How are macro policies affecting retail demand in Kuwait?

The Public Debt Law enhances fiscal flexibility and infrastructure funding, and the proposed mortgage law is expected to unlock long-term consumer credit, lifting home-linked retail categories once implemented.

What are the main geographic hotspots for retail in Kuwait?

Kuwait City holds the largest sales base due to destination malls and CBD footfall, while Hawalli shows the fastest growth as dense residential zones support convenience retail and quick trips.

What structural challenges could limit Kuwait's retail growth?

Key headwinds include import dependency and supply-chain cost volatility, saturation and rising rents in prime malls, cross-border online leakage, and digital-talent shortages that can slow technology deployment.

Page last updated on: